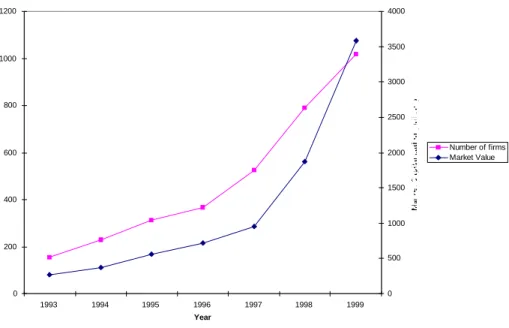

Exchanges such as JASDAQ (for Japan), KASDAQ (for Korea), and EASDAQ (for Europe) mirror the growth of NASDAQ. 3 In other words, much of the increase in the S&P 500 can be attributed to the rise in market value of technology stocks such as Microsoft and Cisco.

SHOW ME THE MONEY: THE FUNDAMENTALS OF DISCOUNTED

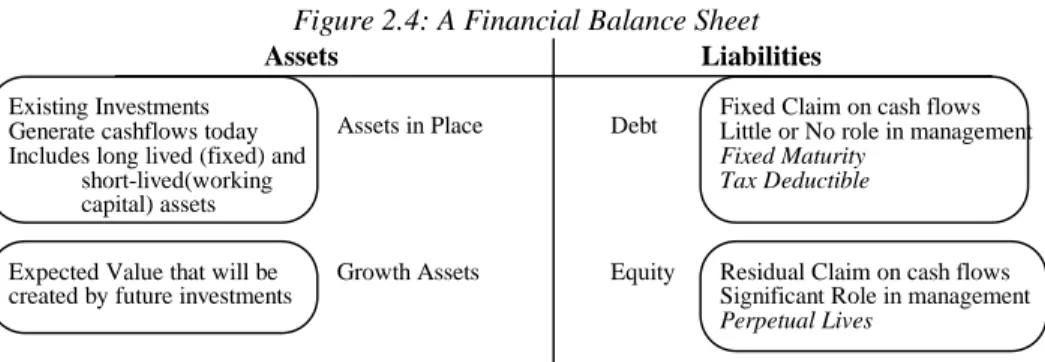

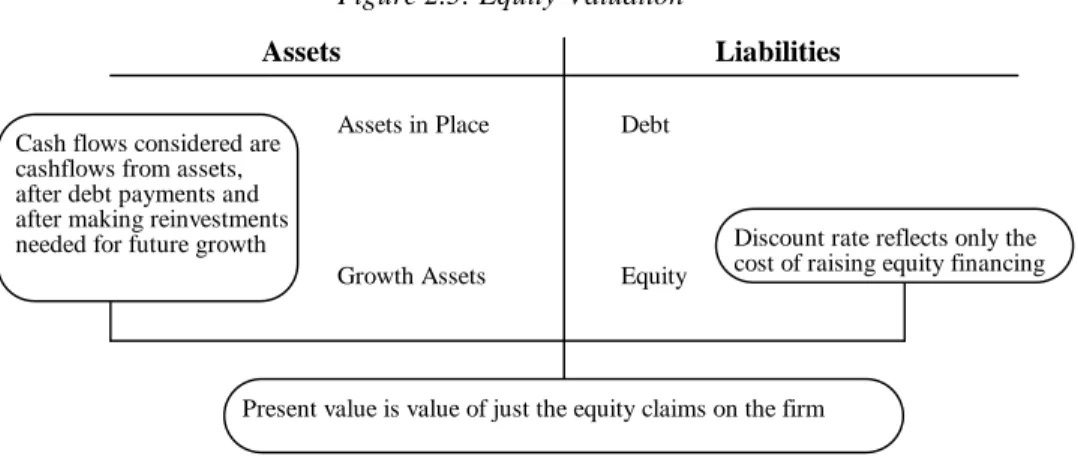

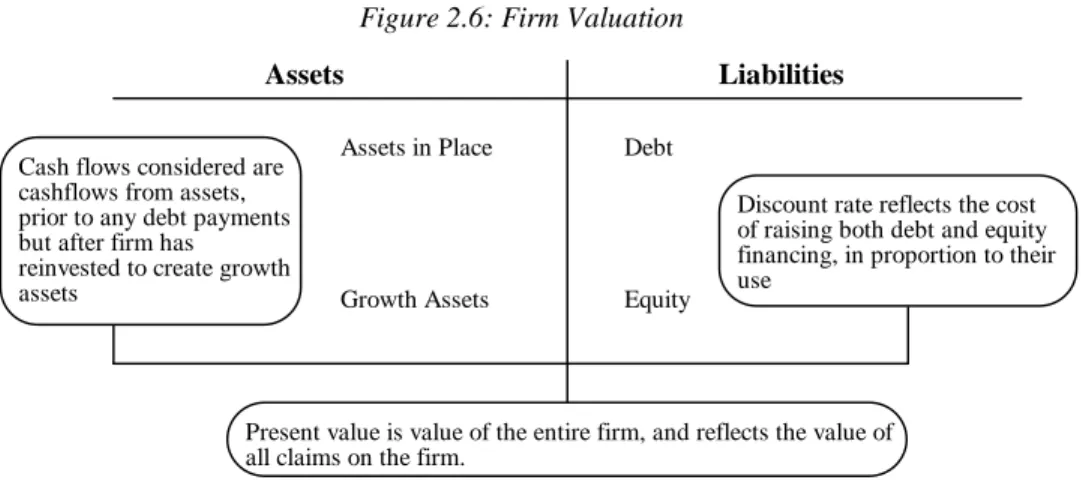

For example, the cash flows to equity investors (which take the form of dividends or share repurchases) are added to the cash flows to debt holders (interest payments, net of the tax benefit, and net debt payments) to arrive at the cash flow. The value of an asset is the present value of the expected cash flows generated by it.

THE PRICE OF RISK: ESTIMATING DISCOUNT RATES

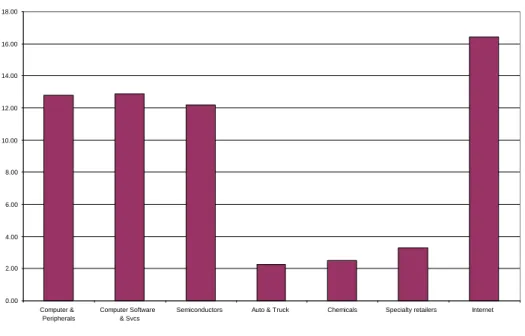

Thus, the cost of equity capital in the capital asset pricing model is a function of three inputs—the risk-free rate, the market portfolio risk premium, and the beta of estimated equity investments. In the arbitrage pricing model, the cost of equity capital is determined by the risk-free interest rate, the risk premiums for each of the factors in the model, and the betas of the asset with respect to each factor. Or we could estimate Cisco beta against the index of the stock exchange on which it is traded - the NASDAQ.

If all of the company's risk is borne by the shareholders (i.e., the debt beta is zero)13, and the debt provides a tax benefit to the company, then. Consequently, the beta for a company is a weighted average of the betas of all the different companies. For stock investors, this is the percentage they need to earn to be compensated for the risk they took in investing in the company's stock.

Estimate the market value of debt using the book value of debt, interest expense on debt, average debt maturity, and pre-tax cost of debt for each company.

CASH IS KING: ESTIMATING CASH FLOWS

Defining the Cash Flow to the Firm

Operating Earnings (EBIT)

3 the last quarter (which leads to estimation error). For example, firms do not reveal details

Trailing 12-month revenue is double the revenue reported in the most recent 10-K, and the company's operating loss and net loss have both increased more than fivefold. For Rediff.com, the filings the company filed with the Securities and Exchange Commission just before its initial public offering were used. The subsequent 4-quarter data on income, operating income and other costs is used as a basis for projections in the valuation.

Cisco's financial year ends in July, making its latest 10-K the most dated of the five companies analyzed. 5 Note that while the differences are large, they are not as dramatically different as they are.

5 Note that while the differences are large, they are not as dramatically different as they are

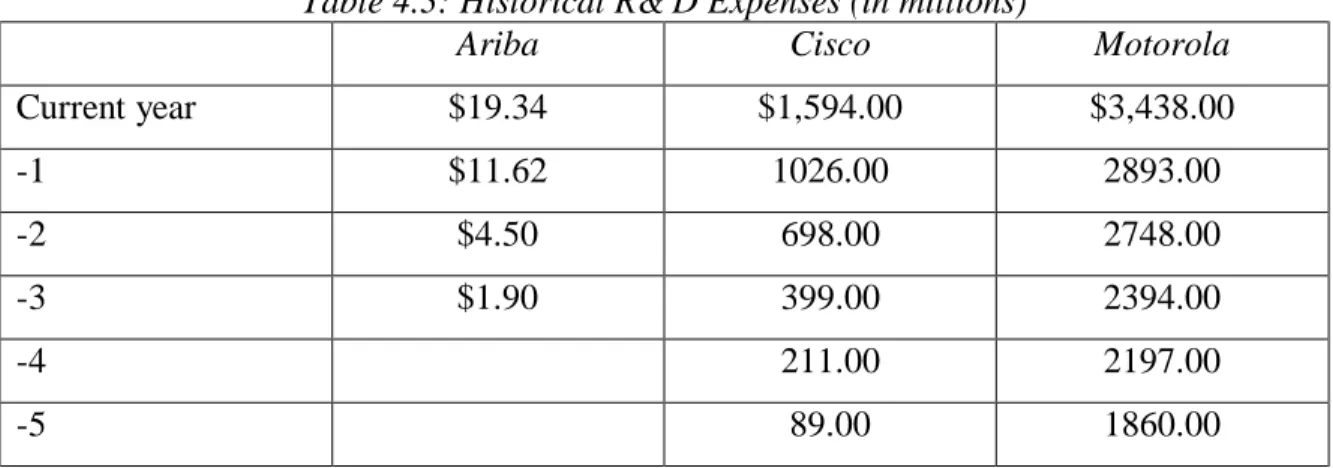

This life will vary between firms and reflect the commercial life of the products resulting from the research. Once the depreciable life of research and development expenditure has been estimated, the next step is to collect data on R&D expenditure over past years extending back over the depreciable life of the research asset. Thus, if the research asset has a depreciable life of 5 years, the R&D expenses must be incurred in each of the five years prior to the current one.

First, the R&D expenses that were deducted to arrive at operating income are added back to operating income, reflecting their recategorization as capital expenditures. Adjusted operating income will generally increase for companies with R&D expenditures that increase over time.

7 R&Dconv.xls: This spreadsheet allows you to convert R&D expenses from operating

The share of expenses in previous years that would have already been amortized and this year's amortization of each of these expenses are taken into account. This allows you to estimate the value of the research asset created in each of these companies and the amortization of research and development costs in the current year. The research asset value and current year depreciation are estimated and listed in Table 4.5 for Ariba and Motorola.

The final step in the process is to adjust operating income to reflect the capitalization of research and development expenditures. Estimate the value of the asset (similar to the research asset) created by these expenditures.

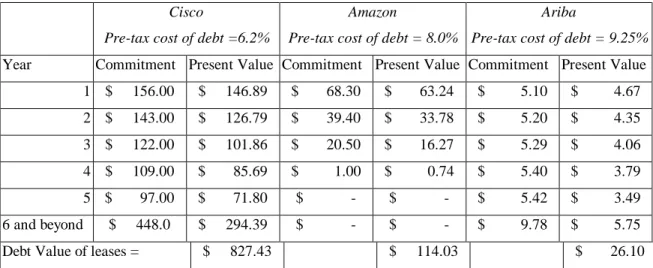

The present value of operating leases is treated as the equivalent of debt and added on top of the company's conventional debt. Finally, you adjust the operating income for the imputed interest expense on the debt value of operating leases. These imputed interest expenses will be added to the stated operating income to arrive at adjusted operating income estimates for each of these companies.

3 This is treated as a three-year annuity, reflecting average annual operating lease expenses over the first five years – approximately $145 million.

15 Oplease.xls: This spreadsheet allows you to convert operating lease expenses into

They are not, and the advent of "whispered earnings estimates" is in response to the consistent delivery of earnings that exceed expectations. Whispered earnings are implicit earnings estimates that firms like Intel and Microsoft must beat to surprise the market, and these estimates are usually a few cents higher than analysts' estimates. For example, on April 10, 1997, Intel reported earnings per share of $2.10 per share, beating analysts' estimates of $2.06 per share, but its stock price fell 5 points because the whispered earnings estimate was $2.15 .

Companies generally manage their earnings because they believe they will be rewarded by the markets for delivering earnings that are smoother and consistently above analyst estimates. 17 It may also be in the best interests of corporate managers to manage profits.

- Planning ahead: Firms can plan investments and asset sales to keep earnings rising smoothly

- Book revenues early: In an opposite phenomenon, firms sometimes ship products during the final days of a weak quarter to distributors and retailers and record the

- Capitalize operating expenses: Just as with revenue recognition, firms are given some discretion in whether they classify expenses as operating or capital expenses, especially

- Income from Investments: Firms with substantial holdings of marketable securities or investments in other firms often have these investments recorded on their books at

Write-offs: A large restructuring charge may result in lower income in the current period, but it provides two benefits to the firm that takes it. Microstrategy reported $17.5 million of the license fee as revenue in the third quarter, which closed four days earlier. The liquidation of these investments can therefore result in large capital gains which can increase income in the period.

Income smoothing, in itself, is not a problem as long as it is not seen as an indicator of risk (or lack thereof) in the firm. The two adjustments are for R&D (or S,G &A) expenses and operating leases, described in the previous sections.

The Tax Effect

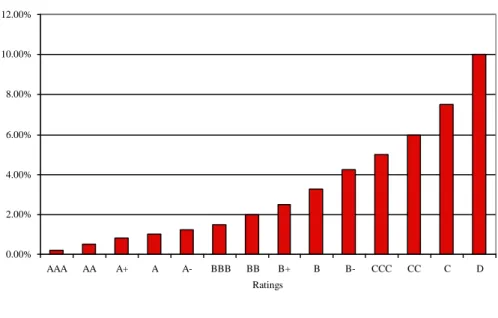

These credits, however, can reduce the effective tax rate below the marginal tax rate. In the later period, when the company pays deferred taxes, the effective tax rate will be higher than the marginal tax rate. It is crucial that the tax rate permanently used to calculate the final value is the marginal tax rate.

As the net operating losses decrease, the tax rates will climb to the marginal tax rate. When they do start paying tax, you will use the 35% marginal tax rate for them as well.

Reinvestment Needs

Thus, Cisco achieves a tax benefit that is $388 million higher because it can expense R&D expenses instead of capitalizing them. Note that Rediff.com and Ariba, which do not pay taxes, do not realize any marginal tax benefit right now, but will do so in future years.

27 expenditures. Consequently, when estimating the capital expenditures to use for

The second adjustment is to bring the effect of acquisitions that Cisco made in the last financial year. Note that both purchase and pool transactions are included, and that the sum of these acquisitions is added to the net investment in 1999. You assume, given Cisco's performance, that its acquisitions in 1999 are not unusual and reflect Cisco's reinvestment policy.

The amortization in connection with these acquisitions is already included as part of the company's depreciation12. To the extent that amortization is not tax deductible, you would look at EBIT before amortization and not consider it while estimating the net investments.

29 Table 4.14: Net Capital Expenditures

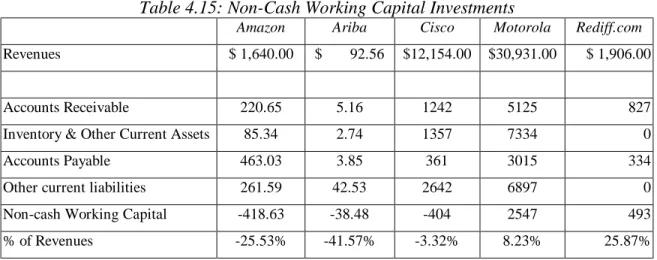

You can obtain the non-cash working capital as a percentage of revenue by looking at the firm's history or by looking at industry standards. It is prudent, when this happens, to set non-cash working capital requirements to zero13. The non-cash working capital investment varies widely across the five firms you value.

Noncash working capital is negative at three of the five firms you're analyzing—Ariba, Cisco, and surprisingly (for a retail firm) Amazon. When valuing these companies, you will need to make an assumption about non-cash working capital to estimate the firm's free cash flows.

Summary

Now that you have estimates of operating income, tax rate, net capital expenditures, and changes in non-cash working capital, you can estimate the company's free cash flows over the past period. Of the five companies you evaluate, four had negative free cash flows to the company in the most recent period. Of those three—Amazon, Ariba, and Rediff—had negative operating income, and Cisco had negative free cash flow because its reinvestment in 1999 was higher than its after-tax operating income.

The challenge you will face in the coming chapters is to estimate these cash flows in the coming years.

LOOKING FORWARD: ESTIMATING GROWTH

Changes in the marginal return on capital do not create a second-order effect, and the value of the firm is the product of the marginal return on capital and the reinvestment rate. In these firms, the expected growth rate will be much higher than the product of the reinvestment rate and the return on capital. The third is to assume that the firm's cash flows will grow at a constant rate forever—a sustainable growth rate.

The second relates to what the characteristics of the firm will be in stable growth, in terms of return on capital and cost of capital. In other words, increased value comes from companies that have a return on capital that is well in excess of the cost of capital. For all the firms, it is worth noting that by setting the return on capital above the cost of capital, you are assuming that excess returns persist forever.

During the transition phase, the company's beta, debt ratio, reinvestment rate, and growth rates adjust toward stable growth levels.