The fact is, you can build the kind of wealth you will need to pay for your long-term goals. Or you can skip any of these steps and jump straight to what interests you the most.

PART ONE

Between the tech stock crash of 2000 and the Enron fiasco of 2002, it's enough to make you want to put your retirement savings under a mattress and forget about it. Back in our premiere issue in April 1992, when the US was still recovering from a recession and the crippling savings and loan debacle, we produced an article called "The 10 Stocks for the '90s."

Stocks

Growth investors look for stocks that grow earnings and sales at market-beating annual rates, and they're willing to pay a big price for such a stock -- generally speaking. Value investors, on the other hand, want bargains or stocks that are trading at a discount — and that discount can be measured in a number of different ways relative to the market or a stock's peer group.

Big Stocks

They build up expectations, and in the end they get quite disappointed,". the low end of this group, while giants like Citigroup and Exxon Mobil weigh more than $225 billion. The two most-watched stock market indexes—the Dow Jones Industrial Average and the Standard & Poor's 500-stock index (S&P 500)—are both composed of large-cap stocks.

Small Stocks

Small companies are significantly more volatile than large companies—. which means there is much more downside risk. As the global economy slowed in 2000, for example, inventories in most areas of the world also declined.

Tech Stocks

Mutual Funds

Thanks to their expertise, you don't have to keep track of dozens of stocks yourself. Managers are known to deviate from this strategy – something to watch out for – but the good managers stick to the line.

Index Funds

Since the fund manager doesn't have to go out and search for stocks, these funds are relatively cheap to use. The Vanguard 500 Index fund, for example, has an incredibly low annual fee of 0.18 percent of your investment.

Actively Managed Funds

But if growth slows, beware—the more momentum a stock has, the harder it's likely to fall if and when the news turns bad. Add it up and value funds are best suited for the most conservative and tax-averse investors.

International Funds

In early 2002, Oakmark International Small Cap, on the other hand, had significant exposure (23 percent of the portfolio) to some of the world's traditionally most volatile regions: Japan, Hong Kong and South Korea. Sector funds do what their name implies: They invest in stocks in a particular segment - or sector - of the market.

Charges and Fees

These deferred fees are basically a tactic to keep you invested in the fund for the long term. Note that once the 12b-1 fee rises above 0.25 percent, the fund is no longer considered unencumbered.

Share Classes

If a 12b-1 fee puts a fund's expense ratio above the average for that fund class, think twice before buying. We suggest you check out SmartMoney.com's interactive Fund Fee Analyzer to see for yourself how much a high load or expense ratio can eat into returns.

Taxes

A high turnover ratio can be a sign of a high distribution of capital gains below. As seen recently, funds with significant shareholder redemptions can also produce capital gains liabilities.

Bonds

Short-term gains are taxed as ordinary income instead of the lower 20 percent tax on long-term capital gains. And all that trading can leave you with a capital gains liability unless the manager is able to offset his or her gains with losses.

Buying Directly from the U.S. Treasury

Agency Bonds

Muni Bonds

What about Corporates?

If interest rates fall and the value of the bonds rise, the corporation can call them, cutting off your expected income stream and cutting off a potential capital gain. Meanwhile, if interest rates rise, you're stuck holding a less valuable security that's yielding below-market rates.

Up the Ladder

Bond Funds

If you could retire with an annual after-tax income of about $100,000, life would be pretty sweet. But even if you've put off saving until now, you can still get there.

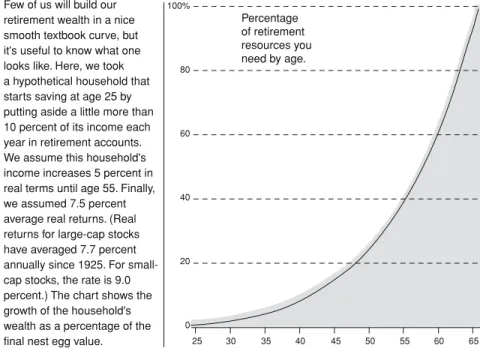

How Much Will You Need?

If you're way behind on your retirement savings, real estate isn't your best investment. If you can wait until you're 591/2 before draining this money, take the IRA rollover.

How Did the 401(k) Plan Get Started?

So, if you're like many people, you now find yourself in your mid-to-late 40s or even older, realizing that you're nowhere near where you need to be with your retirement investing. As we discussed back in Chapter 2, chances are you'll need to save more money than your 401(k) allows if you plan to fund a luxurious retirement life.

Six-Step Strategy for Retirement Savers

Maximize Your 401(k) Contributions

These limits become a real nuisance if you started saving for retirement late in life and need to spend as much as possible over the next few years. The same is true if you are young and want to push hard for early retirement.

What the New 401(k) Rules Really Mean for You

Open a Roth IRA

After you've already put money into your 401(k) plan, put your next retirement savings dollars into a Roth IRA—which you can do if you earn less than. With the pre-tax money you have in your 401(k), you will eventually owe taxes at the income tax rate.

Your 401(k) versus Roth IRA and Other Investments

Maximize Your Nonmatched 401(k) Contributions

That means you're saving, depending on your tax bracket, probably 27 to 35 cents on every dollar (and that's not even including city and state taxes) as it adds up over time. It's true that you will eventually owe income tax on the money and gains that accrued when you started drawing down your 401(k).

The Best Way to Roll Over Your 401(k)

Open a Nondeductible IRA

Yes, you get the money back as income tax, but who wants to deal with that. Is this really who you want in control of your retirement money now that you've left the company.

IRA Participation

Invest in Stocks

Qualifying for the 20 percent rate means holding your shares for at least 12 months—longer, if possible—and choosing mutual funds with low annual turnover (the rate at which the fund manager buys and sells holdings). . Since the law requires that mutual funds' profits from the sale of shares be distributed to fund investors, the higher the turnover rate, the greater the amount of your return each year that will be subject to tax—and that amount may be taxed at higher rates .

Forget Variable Annuities

The key to choosing taxable investments for your retirement savings is to keep your expenses down and make the most of the 20 percent long-term capital gains. If you don't retire for a while, you may qualify for the new 18 percent rate, which is open to anyone in the 27 percent income tax bracket and above who has held a security for more than five years.

The ABCs of Retirement Accounts

Investment gains aren't taxed until withdrawn, but once withdrawn, the money is taxed as income. Translation: Once the money is in, it can grow and grow and grow and you never have to pay a penny in tax on it.

PART TWO

Meanwhile, say you'd put all your money into international stocks for the past 30 years. At the end of the year, you will have a choice of ways to restore balance.

The SmartMoney Allocation Principles

It will also add a significant amount of discipline to your investing: it will encourage you to take the right amount of risk when you feel overly cautious, and it will keep you in check during those times when the sky seems to be the limit. With the new money, you can cheaply buy more shares of small companies, as well as new parts of bonds and cash.

The SmartMoney One Worksheet

To see how much income you can safely draw from your retirement portfolio each year, divide the present value of your investments by $1,000 and multiply the result by the appropriate dollar amount in Table 4.4. This is especially true when you start putting aside large chunks of your retirement savings.

Portfolio Size

The more money you save each year, the more risk you can take on in your allocation. The reason: A steady flow of new savings each year gives you the chance to absorb losses if part of your portfolio takes a hit.

Spending Needs

Investment Income

Federal Tax Bracket

Volatility Tolerance

Do you tend to buy stocks only after your friends and acquaintances have already bought. Are you worried about the value of your home, even though you have no intention of selling?

Economic Outlook

Do you only look at stock charts on days when the market is up. These answers will put less of your wealth into stocks and bonds and move it into super safe cash.

Interest-Rate Exposure

We wanted funds that outperformed the market and the average funds in their peer groups for the past five-, three- and one-year periods (ending December 2001). To measure the funds' short-term volatility, we looked at each fund's three-month rolling returns.

Large-Cap Funds

Since opening in the mid-1990s, the fund has finished in the top 20 percent of its large-cap peer group every year but one. Due to the fund's strict value orientation, Gerber and co-manager Andrew Ngim were sidelined in 1999 as technology stocks rallied.

Small-Cap Funds

According to Morningstar, the fund has a good 13 percent return over five years, which ranks it among the top 3 percent of foreign funds. Third, manager James Moffett keeps individual stock positions to less than 3 percent of the fund.

Four Common Mistakes of Bond Investors

Because of the higher yields on long-term Treasuries, many investors consider them the best buy-and-hold investments. As we said in Chapter 1, you can certainly buy bonds yourself—and there are real advantages to doing it that way—but many people use mutual funds to round out their bond portfolios.

The Bond Allocation Worksheet

Market Outlook: You should increase the safe portion of your bond holdings if you are pessimistic about interest rates (that is, if you think they are likely to rise). The sum of all five scores indicates the percentage of your bond portfolio that should be spent on safe income.

Conservative Bond Funds

An alternative is the lower-fee Fremont Bondfund (FBDFX, also managed by Gross), which has a similarly impressive performance record, ranking in the top 2 percent over the five-year period by investing heavily in government bonds. In addition, it has been consistently ranked. in the highest decile for the past ten-, five- and three-year periods.

More Aggressive Bond Funds

Over the past three years, this fund has consistently delivered an annualized return of more than 7 percent. Just over 21 percent of the fund is invested in BBB-rated bonds, but the rest of the fund is invested in AAA (61 percent) or AA (5 percent) and A (13 percent) bonds.

Uh-Oh: What to Do If You’re Getting a Late Start on Saving

It's the easiest way to do that if you don't have a lot of money to invest in multiple funds at once. That's why we think your chances get even better if you stick to what some investors call "the arms dealers." These are the companies that provide the know-how, specialized equipment or new technology.

Technology

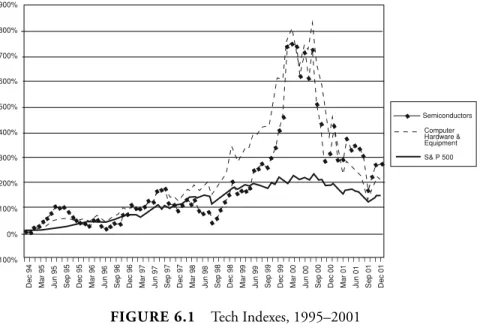

The following is our look at two sectors that we believe are well-positioned for above-average growth in the coming years. and wireless manufacturers to PC hardware, business servers, and data storage—and we haven't even mentioned the chip business. Take a look at Figure 6.1 and you'll see how two different areas of technology have performed over the past few years compared to the S&P 500.

Health Care

The growth in health spending is largely fueled by rapid increases in prescription drug spending; drug spending increased 19.2 percent in 1999 and 17.3 percent in 2000, the sixth consecutive year of double-digit growth.

Boosting Your Returns with Sector Funds

Rowe Price Media & Telecommunications 800-638-5660/PRMTX

Last year's 7 percent loss, while nothing to write home about, was the second-best showing in the category. He trimmed the fund's holdings in equipment makers and emerging companies such as Cisco and Nokia, which were some of the worst-performing areas in the sector in 2001.

Exchange-Traded Funds

Bets on international wireless stocks have also helped - 35 percent of the fund is invested in foreign stocks. In SmartMoney's latest survey of the largest corporate 401(k)s, the soft drink giant described its 401(k) as "the most advanced plan on the market today." Not cutting edge for this generation.

Company Contributions

More common is a 50 percent match (50 cents on every dollar); about 35 percent of all companies do. After the oil company's stock fell below $1 from a peak of $89, Enron's 401(k) plan -- which matches company stock -- lost more than 90 percent of its value.

What to Do If Your 401(k)

Match Comes in Company Stock

Obviously, you don't want to invest in a fund that has your company as the top team. And if you work for a large growth company such as Cisco Systems, you might want to invest in a solid value fund rather than a growth fund.

Enrollment and Vesting

Investment Options

Investment Performance

Fees

Monitoring

Service

Ten Things Your Benefits Department Won’t Tell You

According to David Wray, president of the Profit Sharing/401(k) Council of America, 4 to 5 percent of the U.S. Meanwhile, 25 percent of other companies have increased the share of annual premiums early retirees must pay; .

Grading Your 401(k)

Finally, a note about matching: If your employer offers a graduated match, such as dollar for dollar on the first 3 percent of wages you contribute and 50 cents per dollar on the next 3 percent, skip lines 1 through 3 and complete lines 4 through 7. For the rest of the questions, simply fill in the information and add points each time your 401(k) qualifies.

The 401(k) Worksheet

Does the plan offer a cash option (including money market, stable value, or short-term bond). Does the plan offer a brokerage window option (allowing 401(k) participants to access a broader set of investment options through a brokerage of the employer's choosing).

The 401(k) Manifesto

Demand No. 1: Reduce the Fees That Are Nibbling Away Our Retirement Money

If a company has a billion dollars they're bringing to the table, they have the ability to negotiate,” says Michael Scarborough of the Scarborough Group, which specializes in 401(k) planning. If the fees drag down your investments, just think what they do to your boss.

To find out what you're paying, check fund prospectuses, summary plan descriptions or quarterly statements; you may also need to call your benefits department. I often see four or more [large-cap] funds with different names in a plan, but they are all S&P surrogates.

Demand No. 3: Let Us Max Out Our Contributions

In January 2000, the company allowed employees to transfer only part of the match to other investments. David Wray, president of the Profit Sharing/401(k) Council of America, says company stock "builds a bond with the workforce." Well, okay.

The 401(k) Crusaders

How to do it: Before you roll your 401(k) into an IRA or take a distribution, you're allowed to withdraw some or all of the company's stock without penalty. Within weeks, the site had become the talk of the water cooler and the subject of many emails between the office.

Do Your Homework

"In recent years, I've seen a lot of interest from employees in changing their 401(k)s," says Ted Benna, the benefits consultant who, in the early 1980s, identified the hidden tax loophole that led to the 401 (k) revolution. All the red tape, red tape, and short answers in the world won't stop true believers in what may ultimately be the real 401(k) revolution: Employees looking for—and sometimes getting—a retirement plan with which they can retire.

Size Doesn’t Matter

Four months later, at a meeting of managers, the company's president tapped him on the shoulder and said, “Your efforts have paid off. But when you're a small business, people won't go out of their way to attract your business.

You Can Start Something from Scratch

If it doesn't conflict with the pension plan, we may be able to do that. O'Connor wanted to be prepared in case he got the thumbs up, so he started calling the trusts to get information.

It Never Hurts to Ask

We focused our research on the 10 mutual fund companies with the most 401(k) assets, as tracked by the publication Pensions & Investments. Then we examined the most popular 401(k) funds at each of those fund companies, using an exclusive rating system created with the help of Morningstar.

Fidelity

Rowe PriceSmall-Cap StockSmall blend11,232039 American CenturyEquity Growth Inv.Large blend9,303742 American CenturyGrowth Inv.Large growth9,903065 American CenturyIncome & Growth Inv.Large value9,863129 American CenturyInternational Growth Inv.Tuja delnica7,8 71333 American CenturySelect Inv.Velika rast9 .563543 American CenturyStrat. Inv.Domači hibrid8,434710 American CenturyUltra Inv.Large growth8,175073 American CenturyValue Inv.Mid-cap value11,242037 Merrill LynchBalanced Capital ADomači hibrid6,466816 Merrill LynchBasic Value ALarge value9,813227.

How to Evaluate the Funds in Your 401(k) Plan on Your Own

Ratings, which range from one to five stars (five being the best), take into account both a fund's performance and risk over the life of the fund. In the 48 one-year periods we tested, Asset Manager returned returns of 10 percent or more 63 percent of the time.

Vanguard

A Final Word on Vanguard Index Funds: Vanguard is arguably the largest family of retail index funds in the country. Moreover, bond lovers need not worry about the overall bond market index. It's what its name suggests, and according to our research, it stands out by every measure.

American Funds

You will notice that the bond funds or funds that are heavily weighted in bonds, such as American BalancedandIncome Fund of America (both domestic hybrids) and Bond Fund of America, earn poor records in the growth screen. But the Bond Fund of America is in the middle to top third of all bond funds, with a 36th percentile ranking in that particular screen.

Putnam

It is a more stable fund, and thus its five-year record of 11.3 percent beats the Income Fund of America's return of 9.2 percent. If you really need the stability of bonds, it's not a bad choice, but you can buy a stronger bond fund outside of your 401(k) — in your IRA or Roth IRA, for example — and keep your 401(k ) money invested in the US funds' stock portfolios instead.

Janus

Rowe Price

And not only because the two funds have the highest five-year returns of the group. The winners are the Rowe Price funds, which perform better on both screens, but when viewed as a whole Growth Stock and Mid-Cap Growth.

American Century

We would wait and see how the fund performs, given that our scoring is based on five-year returns. The fund ranks in the top 20 percent in our table because we compare it to the broader group—.

Merrill Lynch

But the fund has got a new manager, who has only been at the helm for just over two years. MFS Emerging Growth was once a superstar fund, but now the fund has a pathetic five-year record of 3.2 percent, which ranks it in the 79th percentile of all large growth funds.

Franklin Templeton

Still, according to our screens, this fund is fairly stable, ranking in the 17th percentile of all domestic equity funds in our volatility screens. The fund gets a 4-star rating from Morningstar because it ranks in the top 20 over the long term (however you look at it, 15 years, 10 years, 5 years or 3 years). percent of all intermediate government bond funds.

Scudder Kemper

The Scudder's Balanced fund might have won our nod as a decent – but not great – overall fund because it has a fairly strong 5-year track record (8.5 percent ranks in the top 26th percentile of its peers). But it has a new manager who has run the fund for just two years, and the three-year record is nothing to write home about (3.2 percent; ranks in the top 47 percent).

What If the Funds in My Retirement Plan Are Dogs?

It ranks below average – 59 percent – in our volatility screen and well below average – 94 percent – in our screen for consistent returns above 10 percent. Or your spouse's plan may have winning funds to invest in the asset classes that your plan lacks.

PART THREE