He serves as a member of the Planning Committee for the Advanced International Oil and Gas Management Program and as a technical update editor for the Petroleum Accounting and Financial Management Journal. He was president of COPAS of Dallas and president of the North American Petroleum Accounting Conference. Brock, CPA, is director of oil and gas programs and director of the Institute for Professional Development's International School of Accounting and Financial Management for Oil and Gas.

Brock was chairman of the FASB Task Force on Financial Accounting and Reporting in the Extractive Industries.

AN INTRODUCTION TO THE PETROLEUM INDUSTRY

At the end of World War II, two events contributed to the tremendous growth of the natural gas industry. Later, eight other countries joined OPEC: the United Arab Emirates and Qatar in the Middle East; the African countries of Algeria, Gabon, Libya and Nigeria; and the countries Indonesia and Ecuador. The 1990s were characterized by five trends: (1) growing use of oil and gas futures, (2) growth in US natural gas production and value, (3) US restructuring.

In the late 1980s, the United States was considered a poor area of the world for new discoveries.

PETROLEUM ECONOMICS

Such an analysis is illustrated in Chapter Thirty on the Valuation of Proven Oil and Gas Properties. The top ten countries have almost 80 percent of the world's oil and gas reserves and the majority of the world's current production. Sixty-four percent of the world's proven oil reserves are in five Middle Eastern countries, and the majority of the world's proven oil reserves are in five Middle Eastern countries.

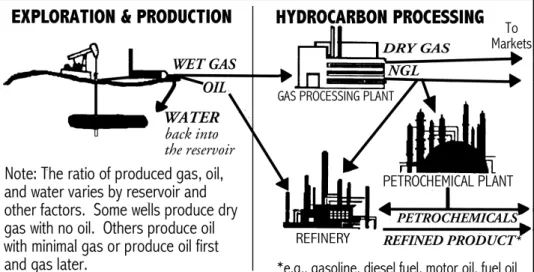

The products of the oil and gas industry are essential to the continued well-being and security of this country for the foreseeable future.

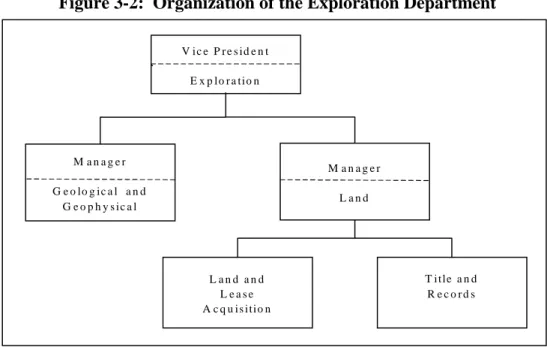

ORGANIZATION OF AN E&P COMPANY

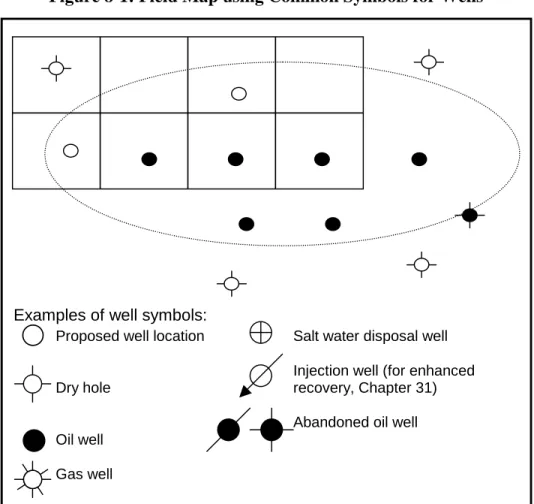

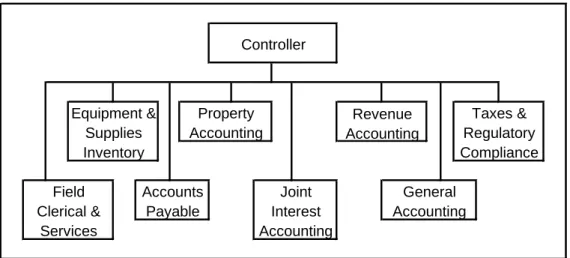

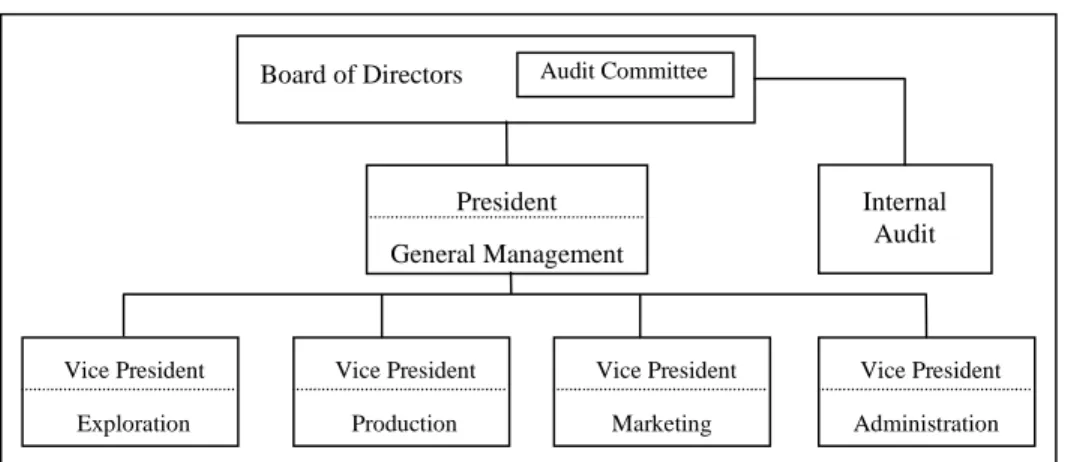

Production engineers deal with both drilling and production, i.e., the day-to-day management of producing fields, including drilling, well completion, treatment and production handling, and equipment selection and design. The organization of the accounting function in an independent oil and gas company is shown in Figure 3-5. A modified organizational chart of the accounting department in the manufacturing division of an integrated company is shown in Figure 3-7.

In 1988, SPEE developed the guidelines for applying the definitions for oil and gas reserves.

ACCOUNTING PRINCIPLES FOR OIL AND GAS PRODUCING ACTIVITIES

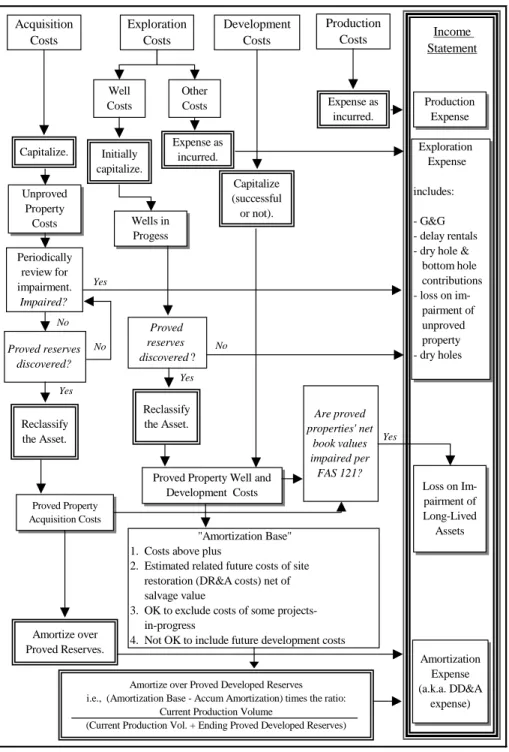

In the following pages, the key provisions for the successful full cost accounting efforts and methods adopted by the SEC are summarized. The characteristic features of the successful efforts and the full-cost methods are centered around which costs must be capitalized and how these costs must subsequently be amortized. Production costs are the costs of activities that involve lifting oil and gas to the surface and gathering, treating, processing and storing them in the field.

Some of the accounts in the chart relate to oil and gas activities and will be briefly explained. Many of the accounts in Exhibit 5 (Our Oil Company's Chart of Accounts) are not unique to the petroleum industry. 291 Deferred loss on hedging future 761 Amortization of capitalized costs of production oil and gas assets.

Accounts 210 through 218 are used to accumulate the cost of the company's mineral rights to unproven properties (properties on which oil or gas reserves do not exist with sufficient certainty to be classified as proven). Most of the costs associated with an oil and gas exploration and production company are found in accounts 700 through 806. The direct costs of operating the production of oil and gas properties are charged to account 710, Operating Expenses lease.

Thus, a single oil and gas asset account (or similarly titled account) could be used for each country to accumulate costs in that country. Generally, no gain or loss is recognized on the sale or disposal of oil and gas assets under the full value method.

GEOLOGICAL AND GEOPHYSICAL EXPLORATION

The inorganic theory recognizes that hydrogen and carbon are present in natural form below the earth's surface (for example, diamonds indicate the presence of carbon in the earth's mantle). Pressure is believed to have caused a primary migration of the oil and gas from the source beds to reservoir rocks with properties favorable for their accumulation. The pore spaces can account for up to 30 percent of the volume of the reservoir rocks that are relatively close to the surface.

More often, however, movements in the Earth's crust caused additional shifting, folding, flexures and fissures, and a secondary migration of the oil and gas occurred through porous layers until another impermeable seal was reached. Faults are formed by the breaking or shearing of strata as a result of significant shifting or movement of the Earth's crust. Shifting of the earth's crust caused a porous bed to abut against an impermeable layer, causing a possible trapping of hydrocarbons.].

Stratigraphic traps are formed by differences in the properties of strata at various points where oil and gas are trapped in the porous portions of the formation and surrounded by non-porous portions. Structural surface maps depict the underground topography of the potential reservoir in the same way that topographic maps show contours of the Earth's surface. Just as there are differences in the gravitational pull at different places on the earth's surface, there are also deviations from the normal pattern of the magnetic fields.

When hitting a hard or dense layer, part of the pressure wave is reflected back to the surface. Interpretations of the subsurface now require a multidisciplinary approach combining geological, geophysical and engineering disciplines.

ACCOUNTING FOR EXPLORATION COSTS

Adoption of the AFE does not require a registration in the formal accounting registers; its purpose is the internal control of expenses. Although research budgets are somewhat flexible, AFE charges a portion of the budget. Since the project is not yet complete, a company with successful efforts should reverse the above entry at the beginning of the next accounting period in order to continue the project in progress.

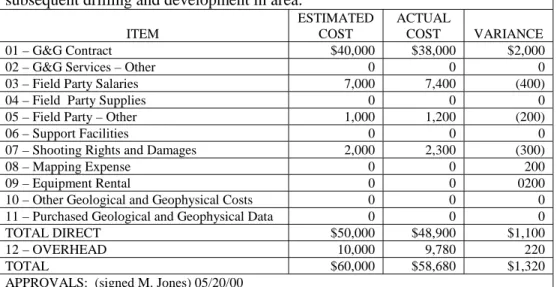

This entry records the completion of the project and the posting of all costs to expenses. The option contract may specify the amount to be used for the shooting rights and separately state the cost of the option. In this case, exploration rights costs will be treated in the same way as all other exploration costs.

However, if no cost sharing is included in the contract, the entire payment should be treated as applying to the option to acquire acreage. At full cost, all test well contributions are activated as part of the cost pool. Upon completion of the work, whether or not the outcome is successful, Outside Company will receive a one-fourth interest in the property.

G&G surveys may be performed on a property owned by another person in exchange for an interest in the property if proven reserves are found, or for reimbursement of costs if proven reserves are not found. If proven reserves are found, the Outside Company must be awarded one-sixth of the operating interest in the property.

UNPROVED PROPERTY ACQUISITION, RETENTION, AND SURRENDER

Paying the bonus and signing the lease keeps the contract in effect for one year. The amount of late rent is declared on a per hectare basis and is normally much less than the rental bonus. Normally the option specifies the bonus amount per acre to be paid if and when the lease is subsequently executed.

On the other hand, the lessor has the right to receive a certain partial share of the minerals extracted from the property or its value. We find three other types of non-operative shares, all of which are created from the working share. In theory, the allocation would be made based on the relative fair market values of the two holdings.

A property tax on mineral rights owned by the tenant is simply another carrying cost of the property and is charged at cost. The majority of respondents also considered (1) other wells drilled in the area, (2) the geologist's valuation of the lease, and (3) remaining months in the lease's primary term. If drilling is only probable, the company's appraised value of the lease may be significantly less than the original cost.

The first year's depreciation should reflect both (1) the 9 percent of the cost and (2) a portion of the 81 percent of the total lease purchase cost that will be determined worthless in the first term. The non-operational interests arising from the working interest can be retained or split off. The decisive royalty is very similar to the basic royalty rate, except that it arises from the working interest.

It assigns to Investor Company a one-fourth interest in the net profits of the lease for a consideration of $100,000.

DRILLING AND DEVELOPMENT

A level location is required to install the drilling rig, power supplies, mud pits and other components. The drilling contractor is paid a certain amount for each day he works on the well, regardless of the number of feet drilled. The benefit to the operator is obvious: whatever problems arise, the total cost of the well is the contract price.

The disadvantage for the drilling contractor is that the contractor must complete the well as specified, regardless of cost. The drill is attached to the bottom of the drill chain, which consists of the drill, drill bits, drill pipe and kelly. Drill clamps attached between the bit and the drill pipe are heavy, thick-walled pipes that add weight to the bottom of the drill string.

Circulating drilling mud suspends and brings cuttings of the formation being drilled to the surface. Drilling mud also lubricates and cools the drill bit and coats the wellbore, sealing the formations and making the wellbore more stable. The weight of the drilling mud also helps prevent blowouts caused by high pressures in the formation being drilled.

The mixture of materials used in the liquid determines the weight of the liquid column. At the drill bit, the drilling fluid washes the cuttings out of the drill bit and the bottom of the hole and carries them back to the surface through the ring (6).