It is these twin forces that have done so much to strengthen our view of the marketplace. It is a Darwinian process where the successful few live off the rest of the market.

Losers Anonymous

We could say that risk is in the eye of the beholder, that it is dynamic and rarely completely predictable. Of course, in the long run, they will be crushed by the game's negative math.

Past Masters

Along with Gould, he was heavily involved in the financing of the early American railroad network. Keynes spent much of the 1920s speculating on his own account in the currency and commodity markets, often with rather dismal results.

Basic Building Blocks

We can describe volatility as the measure of the rate of change in the price of an asset over a specified period of time. It is usual to calculate this in terms of the standard deviation of the average price of the asset.

Mental Curves

Unfortunately, inaction is one of the biggest killers in the management of financial risk, and it is doubtful if there is anything that can protect the investor from himself. This is usually due to the dead hand of benchmarking – if a bond loses its coveted 'investment grade'. Portfolios to the right of the line (the shaded area) are achievable combinations but take unnecessary risks for the expected return.

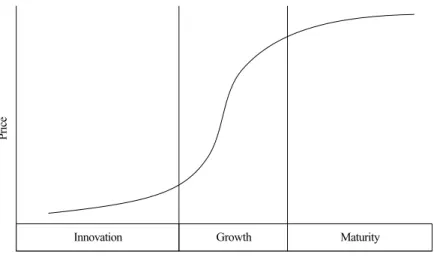

It is often in this part of the curve that opponents fall into the trap of trading too soon. The peak of the momentum curve is equal to the very steepest part of the 'S' curve. Finally, it is impossible to resist the observation that the heads of the investors must have been in the sand.

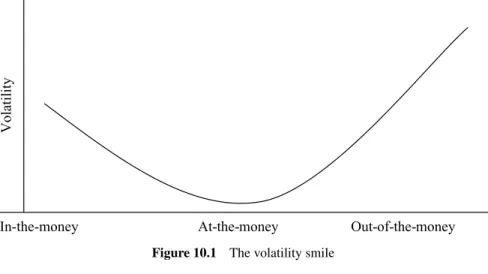

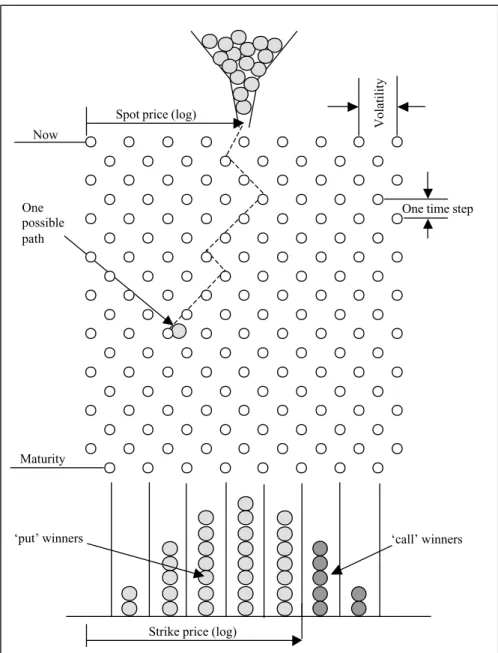

In Figure 4.5, the put option is “in the money” while the call option is “out of the money”. The model also highlights the arbitrary nature of the underlying assumptions of the Black–Scholes formula. This seems quite normal and reasonable and at first glance unlikely to contradict the classical idea of the rational investor at all.

Assorted Killers

It is a telltale sign of the newcomer or inexperienced market player who believes these costs are marginal; They are anything but, and they can easily turn profitable strategies into losses. They cannot be avoided or ignored, but must be part of the calculus of trading. A superstition that seems to be related to the massacre of the Templars by the French King Philip the Fair in Paris in 1307!).

This is possibly another example of the self-fulfilling aspect of so many market-generated ideas. Obviously, it is common sense for the order maker to avoid such outcomes, but markets still see large amounts of orders placed at the magnetic pull of the round number. After the perceived excesses of the 1990s, and the shock-horror revelations that all was not well in the world of finance and accounting, the regulators are back in force.

Of course we've been here before; the bull market collapse of the 1920s also saw its introduction. Then, after a decade or so, people eventually realize that this stifles competition and choice and some of the machinery (although rarely all) is dismantled. Command economy thinking paralyzed much of the Western economy until the whole cycle started again in the 1980s.

Chartists, Economists and Gurus

There are a number of versions of the idea, with Paulos illustrating the idea with stock index forecasts. Second, there was the advent of the personal computer in the brokerage office, the bank dealing room and the trading booth on the trading floor. This group also discovered that they had a small problem: the programs didn't seem to work, or at least not in the hands of the average person in the trading room.

The bank or brokerage firm economist always seems to be in demand, regardless of the state of the market. Away from the big financial institutions are another group of seers – in some ways the most exotic of the lot – the gurus. Membership of the Guru Club appears to be exclusively male; we are still waiting for our first market priestess.

One of the most powerful effects of the e-commerce environment has been to lower the barriers to entry for many businesses; this is true in the world of financial information. In many ways, this group is a hybrid of the previous groups we've looked at. Applying the system's rules to the data set in question and finding a 'reasonable' fit that is not an increase in results.

Quantum(ish) Finance

In the last chapter we mentioned the weather forecaster – this is an example of a stranger who reports on change, or rather in this case seeks to predict future changes. For example, government regulatory activity in the California electricity market is a good, if rather extreme, example of the dangers of their involvement. Trying to understand market motives is extremely difficult, endless actions and reactions merge together to provide a very complex picture.

This is an almost perfect example of the closed loop of information that often circulates in the marketplace. It is very difficult to keep a cool head, given the megaphone volume of the 'investigation'. Unfortunately, virtually all correlation analysis work is inherently highly mathematical and tends to put the market to sleep.

Investors' views and ideas about the past undoubtedly color their trading habits – although ironically they seem to have a really great understanding of the market. Rather than being bad news, this should have been welcome, in the mysterious world of "them" it is comforting to at least know some of the weaknesses of your potential trade opponents. As well as being the main drivers in the ebb and flow of the regulatory cycle, they are in some cases central to the functioning of many markets.

This is the First Time since the Last Time

This bias, or perhaps the timing difference, is due to the discounting element in financial trading: it is almost always the case that markets look to the future rather than the present. Firstly, there is the actual price of the commodity as quoted on the various stock exchanges or in the open market, secondly, there are the shares in the. It was the end of wild stock speculation in the first days of trading in London, in a company with no revenue but "enormous future potential".

In the first half of the nineteenth century, there was strong evidence of a 10-year boom-and-bust cycle, but this changed over time. It's certainly easier to spot the bullish and bearish market cycles in the stock markets than trying to figure out some of the dumber propositions of the business cycle. Readers will recognize in this sentiment all the signs of a terrible bias for sunk loss.

This is the world of asset strippers, buying undervalued companies, breaking them up, and extracting more money than they paid for them. Clearly, one of the most dangerous parts about cycles and the like is the temptation to chase precision that doesn't exist. One of the consequences of this mindset is the risky way in which many spread positions are traded.

The Divine Right of Failure

The rating agencies have also been active, as have the originators of the idea in the first place: newspaper publishers. Going back to the hall of mirrors analogy, these activities can have a significant distorting effect on the markets. This has been particularly the case in the post-bubble burst of telecommunications debt, which has created quite a remarkable failure among certain sectors of the debt market.

This is a strange angle of attack, benchmarks may appear to make investments more transparent and help assess risk, but there is an argument to be made that they are part of the problem, and certainly not the solution. So much for benchmarks and measuring performance, it is now time to consider the other side of the coin, measuring risk. As a result, markets lose diversification and break one of the simplest rules in the risk book.

This is perhaps one of the best examples of the concept of distorted mirrors in financial markets, risk managers are not only outside the market looking into it; they are more and more directly embedded in its most vital structures. To try to shed more light on this, we need to focus on the most important and often very common part of business - losses. So the lesson about losses is to accept them as a normal part of the investment business, but be ruthless in managing them, if you don't, the market will be ruthless with you.

Signposts

Ultimately the game is about making money, which is only possible if you protect your capital. The remaining half of the position is protected by a stop further away than the first level. This was especially true as the final stages of the e-commerce bubble came to a head in the late 1990s.

It was the prevailing ethos of the London Stock Exchange that the market operated on the basis of 'my word is my bond'. They satisfy so many of the emotions and desires that speculators feel in the market. One could counter that it is no different than committing suicide by jumping from the eighth floor instead of the tenth.

To use an analogy with cricket (although American readers can see the same idea in baseball terms), it is better to score quick singles than to try to hit the ball out of the ground. In this concluding section I would like to reiterate some of the key themes of this book. Being able to close yourself off to these sirens is perhaps the hardest part of the job.