NATURE AND SCOPE OF THE STUDY

INTRODUCTION

PROBLEM STATEMENT

OBJECTIVES OF THE STUDY

- Primary objective

- Secondary objectives

SCOPE OF THE STUDY

RESEARCH METHODOLOGY

- Literature study

- The empirical study

LIMITATIONS OF THE STUDY

LAYOUT OF THE STUDY

CHAPTER SUMMARY

THE THEORY ON ACTIVITY BASED COSTING

INTRODUCTION

To maintain high levels of competition, companies must seek to provide low costs, high quality services and products in a very short period. The results of an ABC analysis were used to find the optimal costs and prices of the services produced by the Education and Training department in order to suggest a service costing framework through an activity-based costing system.

NON-PROFIT ORGANISATIONS

Another responsibility is to manage all actions aimed at the accreditation and approval of providers and courses in terms of the Pharmacy Act and the South African Qualifications Authority Act (SAQA) and so on. The main activities involved before a person is declared qualified and subsequently registered with the Council include, but are not limited to, the management of the pharmacy traineeship programme, the recognition of foreign pharmacy qualifications, the management of processes related to the training of pharmacy support staff and the recognition of prior learning.

SERVICE ENTERPRISES

According to Correia et al there are problems with conventional costing systems in service enterprises. According to Correia et al, service firms are an ideal environment for implementing ABC.

OVERHEAD COSTS IN SERVICE FIRMS

According to Develin, research shows that, as cited by Lin et al., overhead costs account for approximately 37 percent and 66 percent of total costs in manufacturing and service companies, respectively. The ever-increasing overhead costs and lack of understanding of these overheads will threaten the service ability of the organization to meet customer requirements in the near future, which will also leave the customers dissatisfied and frustrated.

ACTIVITY-BASED COSTING

- The genesis of activity-based costing

- Definition and the components of an ABC system

- The implementation of Activity-Based Costing

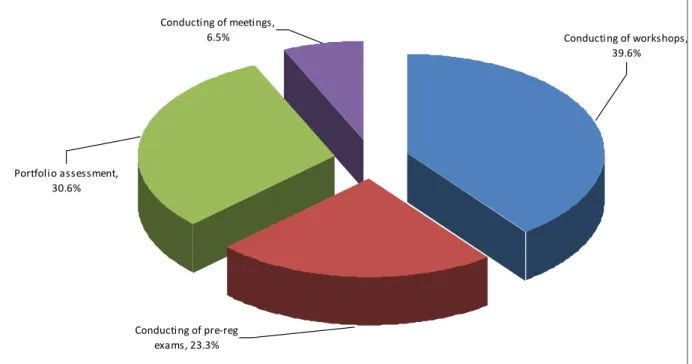

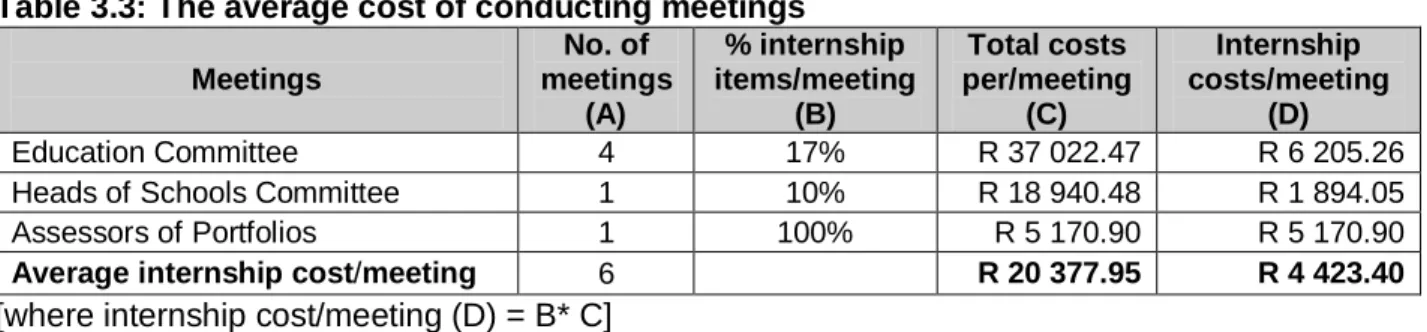

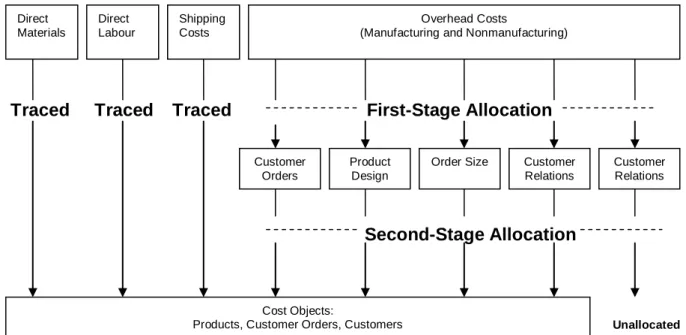

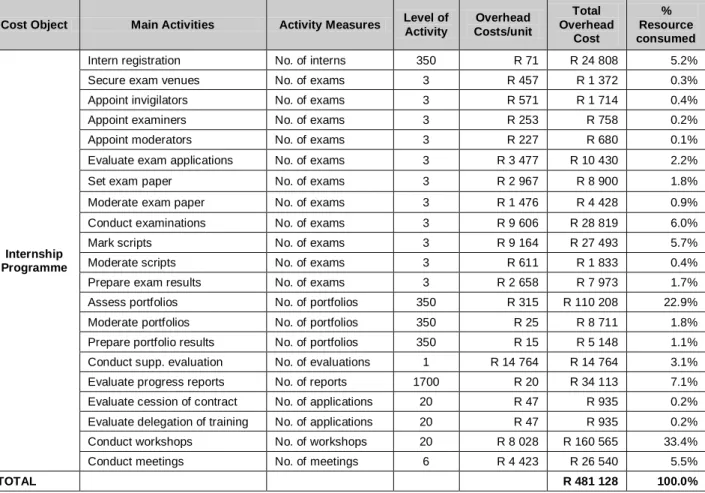

After finding activity costs (cost pools), ABC allocates activity costs to cost objects (ie, products, product lines, processes, customers, channels, markets, etc.). The development of meetings was found to consume less resources allocated to the provision of the internship program (6.5%). Appointments accounted for the smallest portion of the total costs incurred in delivering the internship program to registered interns.

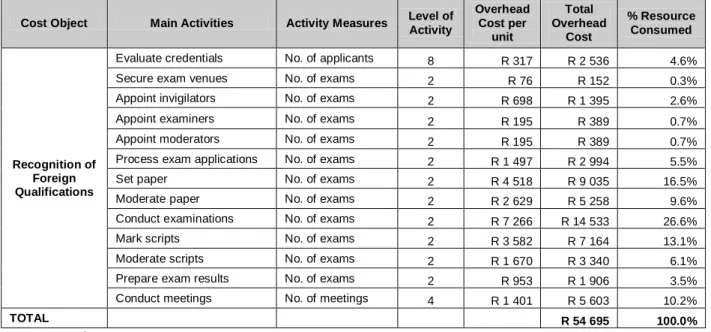

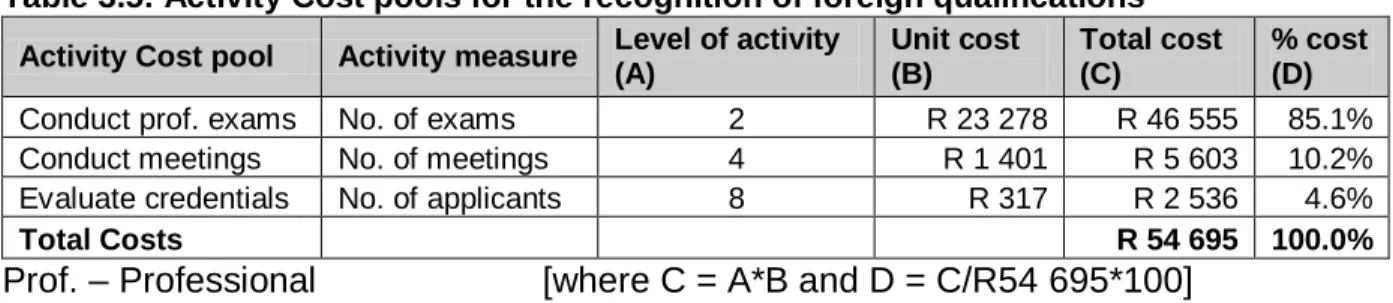

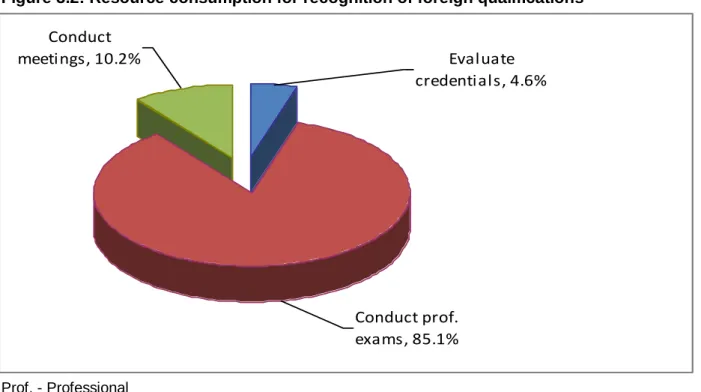

Conducting professional exams consumed 85.1% of the resources allocated to the cost object (figure 3.2). The development of the meeting consumed 10.2% of the resources allocated to the cost object, the recognition of foreign qualifications (figure 3.2). The general costs incurred by the KSAF Education and Training department were presented in previous chapters.

An ABC analysis was successfully applied to the cost data related to the Education and Training department of the SAAR. One of the major cost drivers in the Education and Training Department of the SAAR is the administration of the internship program.

Define and identify activities, activity cost pools, and activity measures

Assign overhead costs to activity cost pools

Garrison et al refer to the allocation of costs in this phase of an ABC system as first-phase allocation, where functionally organized overhead costs derived from a company's general ledger are assigned to activity cost pools. Normally, department managers are interviewed to determine how non-personnel costs should be allocated to activity cost pools (Garrison et al.

Calculate activity rates

Assign overhead costs to cost objects using activity rates and activity measures

Prepare management reports

- Advantages of an Activity-Based Costing system

- Disadvantages and challenges of implementing an Activity-Based Costing system

- Success factors in the implementation of an Activity-Based Costing system

- The extent and reasons for the adoption of Activity-Based Costing by firms

- TRADITIONAL COSTING VERSUS ACTIVITY-BASED COSTING

- CHAPTER SUMMARY

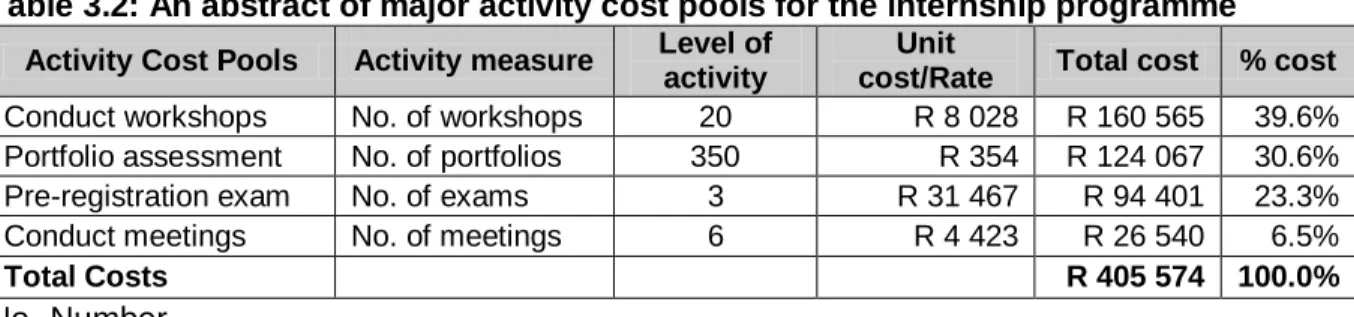

A total of 20 workshops are conducted during the implementation of the internship program (eight workshops with information sessions, one workshop for training the facilitator and eleven workshops for the empowerment of trainees and teachers). The portfolio assessment, taking the pre-enrolment exams and providing the internship workshops contributed significantly to the costs of the internship program.

THE APPLICATION OF AN ACTIVITY- BASED COSTING MODEL

INTRODUCTION

- The South African Pharmacy Council (SAPC/Council)

- Broad functions of the Education and Training Department

The following section discusses the main functions performed by the Education and Training Department to achieve the objectives of the Council. The following sections of this report provide a comprehensive cost analysis of the activities carried out in the Education and Training Department when the services were produced.

GATHERING OF DATA

- Identifying activities, activity measures and activity cost pools

- Assigning of costs to activities

- Computing of activity rates

- Assigning of overhead costs to activity cost pools

- Preparing of management reports

An ABC approach was applied to analyze the overhead costs incurred by the Education and Training Department in providing services to its registered members. In this step, the ABC-determined overhead costs were allocated to all the cost objects identified in step one.

RESULTS AND DISCUSSION

- The internship programme

- Overhead costs associated with the conducting of internship workshops

- Overhead costs associated with the assessment of the portfolio

- Overhead costs associated with conducting the pre-registration examinations

- Conducting of the meetings

- Recognition of foreign qualifications

- Conducting of the professional examinations

- Conducting of meetings

- Evaluation of the credentials

- Monitoring of Pharmacists Assistants’ in-service training

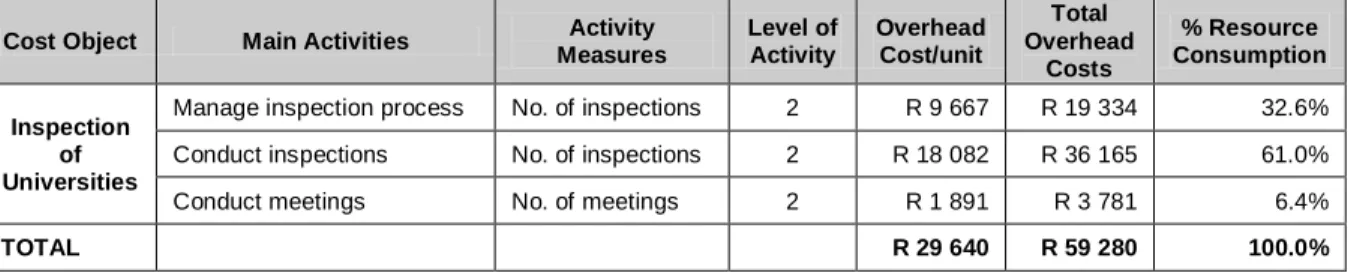

- Conducting of university inspections

- Summary of costs for the Education and Training Department

- Management reports

There are a number of sub-activities involved during the conduct of the pre-registration tests. All calculations in connection with the costs for assessment of the examination paper appear in appendix 12. The meetings of the education committee consumed 10.2% of the resources (figure 3.2) allocated to the delivery of the cost object, recognition of foreign qualifications.

This cost pool consumed 4.6% of the resources allocated for the cost object, recognition of foreign qualifications (figure 3.2).

CHAPTER SUMMARY

As can be seen from the review of departmental overhead costs presented in Figure 3.3 in the previous chapter, the implementation of the internship program for interns consumed the most resources allocated to the cost center. There is also a lack of understanding of the clients the department serves;. In addition to the high incremental overhead costs associated with internships, delivering the program itself is labor intensive.

The administration of the Council's graduate pharmacist traineeship program appears to be the main driver of resources in the department.

CONCLUSIONS AND RECOMMEDNDATIONS

INTRODUCTION

Managing and controlling overhead costs through the application of an ABC system has proven to be a complex and laborious process to undertake, especially if done manually. It is also worth noting that in its efforts to provide quality services to members, overheads were inevitable for the Council, especially for an enterprise that produces as its output, services to its members. Based on the summary of the overall costs caused by the identified cost objects and the profitability analysis of these cost objects, recommendations and conclusions are drawn in this chapter.

From a realistic and practical point of view, the following sections of this report present the conclusions and recommendations to be considered in overhead management based on the previously presented costing results.

CONCLUSIONS

- Specific conclusions

- General conclusions

Similarly, there is an inverse relationship between the rate at which resources are consumed by the activities involved in administering the pre-enrolment exams and the value placed on the written exam for final assessment. The most profitable cost object is the monitoring of pharmacy assistant training, which generates 85% of the contribution margins compared to other cost objects. While some form of budgetary control existed for the responsibility center, in this case the Education and Training Department of the SAPC, it lacked a detailed service cost accounting system or framework.

The following general conclusions regarding the inefficiency of the current cost structure for services can be drawn. A).

RECOMMENDATIONS TO BE CONSIDERED

Differentiating service features observed in relation to apprenticeship provision included the number of examination attempts allowed in the year prior to enrolment, a high number of workshops held to support apprentices and the logistics involved in managing portfolio assessment. Shortening some of these service features and activity levels will reduce the overall costs incurred in providing this cost object. Therefore, most trainees who attempt the exam for the first time in a registration year are during the second exam, which usually takes place in June or July.

Introduce an online method of evaluating submitted evidence and reflection to reduce the logistics involved in managing a portfolio assessment.

ACHIEVEMENT OF THE STUDY’S OBJECTIVES

RECOMMENDATIONS FOR FUTURE RESEARCH

The cost related to the use of the registry system, other IT programs, computer equipment and its depreciation are not included in this analysis. The register system is used throughout the organization and the costs of its acquisition and maintenance can be traced directly to various cost objects in the department. Other fixed costs that include rent, office equipment and furniture, and other utilities were not tracked to identified cost objects.

Once fixed costs have been calculated, break-even points must be calculated to support decisions about eliminating or improving certain cost objects.

CHAPTER SUMMARY

Controlling the cost of providing products and services to customers requires an understanding of the costs that will be incurred at different levels of activity. These costs are related to exam logistics, support workshops for the interns, and other indirect labor hours spent on the general administration of the internship program. Some of these logistical activities include the successful delivery of the internship assessments (e.g. exam and portfolio administration processes and successful delivery of workshops to stakeholders).

It will be interesting for the organization's management to be able to use ABC data to make informed decisions about the mix of processes in providing services to its customers.

INTERN REGISTRATION

SECURE EXAM VENUES

APPOINT INVIGILATORS

APPOINT EXAMINERS

APPOINT MODERATORS

EVALUATE EXAM APPLICATIONS

SET PAPER

MODERATE PAPER

CONDUCT EXAMINATIONS

MARK SCRIPTS

MODERATE SCRIPTS

PREPARE EXAM RESULTS

12 Weeks: First Personal and Professional Development 280 24 Weeks: Second Personal and Professional Development 280 36 Weeks: Third Personal and Professional Development 280 45 Weeks: Fourth Personal and Professional Development 280. 12 Weeks: First Personal and Professional Development 40 24 Weeks: Second Personal and Professional development 40 36 Weeks: Third Personal and Professional development 40 45 Weeks: Fourth Personal and Professional development 40. cost/unit quantity total cost. Average cost of evaluation by Committee per meeting R 1 400.86 Average cost of evaluation by Committee per applicant R 188.88.

I would like to request permission to use the Council's data to fulfill the requirements for the compilation of an MBA mini-dissertation as required for the successful award of the degree by North-West University (NWU). The report on this analysis will be classified as confidential according to the rules established by the NWU Senate and the prescriptions established by the Senate regarding the examination process. The registered title will be indicated as well as the number of copies to be submitted for examination.

PORTFOLIO ASSESSMENT

PORTFOLIO MODERATION

PREPARE PORTFOLIO RESULTS

CONDUCT SUPPLEMENTARY EVALUATION

EVALUATE PROGRESS REPORTS

EVALUATE CESSION OF CONTRACT

EVALUATE DELEGATION OF TRAINING

CONDUCT WORKSHOPS

CONDUCT MEETINGS

COURIER SERVICES COSTS

EVALUATION OF CREDENTIALS

SECURE EXAM VENUES

APPOINT INVIGILATORS

APPOINT EXAMINERS

APPOINT MODERATORS

EVALUATE EXAM APPLICATIONS

SET PAPER

MODERATE PAPER

CONDUCT EXAMINATIONS

MARK SCRIPTS

MODERATE SCRIPTS

PREPARE EXAM RESULTS

EVALUATE PROGRESS REPORTS

The Council's information/data confidentiality policy should in principle be followed at all stages of report development. The promoter/supervisor hereby confirms that the student has completed the minimum period of study and that all aspects related to the registration of the student's title and. Indien u nie indien soos u kennis geige het nie, moet u weer drie maande voor die volgende indieningsdatum kennis gee.

If you do not submit as planned, you will be required to give three months' notice before the next submission date.

MANAGE INSPECTION PROCESS

EDUCATION COMMITTEE MEETING

GENERAL LEDGER OVERHEADS ACCOUNTS

REQUEST FOR AUTHORISATION TO USE COUNCIL DATA

DISSERTATION TITLE REGISTRATION

APPROVAL/AUTHORISATION TO USE COUNCIL DATA