The research reported in this dissertation/thesis is my own original research, except where otherwise noted. ii). The research method used was qualitative, and interviews were conducted on a sample of small and medium-sized enterprises in UMzimkhulu.

Introduction

Background and Context of the Study

The research into SMMEs' access to finance has been sparked by an interest in how SMMEs are progressing in UMzimkhulu in KwaZulu-Natal. It is against this background that this study believes that if an appropriate enabling environment and financial support can be created, SMEs in our country can develop to great heights and can have a positive impact on the country's economy (Gallagher and Robson, 1997).

Definitions

There are challenges faced by small and medium-sized enterprises, and these are particularly related to the support they receive from financing institutions. They are unlikely to operate in business or industrial premises or to be registered for tax purposes so that they can meet the required prerequisites for official registration.

Research Purpose

The small and medium enterprises make up the largest part of the known businesses, with employment varying between five and around 50 employees. In order to achieve the aim of the study as stated above, there are a number of key questions that were answered in the course of the study.

Rationale

The South African economy has been credited for surviving the economic meltdown that has destabilized the economies of first world countries since 2008. The system and government policies are seen as the reason for the survival of the South African economy.

Design and Methodology

Significance of this research

Limitations of the study

It is important that the support of stakeholders in SME support, especially in the field of funding such as the commercial banks, development bank, private sector government and NGOs, should always be for the benefit of the needy SMEs and not those that are already doing well. .

Synopsis of Chapters

Chapter 5, the last chapter of the thesis, contains a summary of the study's main conclusions. This chapter presents recommendations for further research, policy and practice related to funding interventions from different funding agencies.

Summary of Chapter One

In the early 2000s, the then President of South Africa, Mr Mbeki, was advised by business people and organizations such as the National Chamber of Commerce (NAFCOC) Business. There is a need to transform the SMEs so that they can meet the challenges of the market (Kayanila and Quatey, 2000).

Introduction

The Economic Standing of SMMEs

Not much was found in the literature on the level of access to financial services in South Africa and what is available is not easy to measure or define precisely. There are a number of reasons that can be given by those who choose not to use financial services.

Changing view and policy background on SMMEs

The law provided for the restructuring of existing institutions and the creation of others to support and finance SMEs to cater to unemployed youth and women. This was done to help the SMEs contribute to the growth of the country's economy through the creation of sustainable jobs through this sector (Mathibe and Van Zyl, 2011).

South African policy on SMME support programmes

Another stumbling block to the success of support structures is unclear priorities. There is a need for balance in the development objectives of the SMME and not one objective at the expense of the other (Rogerson 2004).

Government funding and support to SMMEs and their challenges

Finally, this chapter discussed some of the challenges the researcher faces when engaging in this. One respondent R said; “The government should also bring the offices in rural towns to us so that we can get help close to our homes.”

Challenges in accessing available government funding and services

Private sector funding and support to SMMEs and their challenges

Credit unions and stokvels

This chapter presents the analysis of data collected through qualitative research in the form of interviews. The above SME responses clearly indicated the challenge in obtaining information and advice.

NGOs and Private sector role

Microfinance

This sector has played a crucial role in the financing of SMEs due to the nature of its lending criteria, which are simpler than those of commercial banks.

South African banking sector and SMMEs

Here they look at the type of industry portfolio as they consider some industries to be high risk such as textiles. These criteria discourage SMEs from applying for funding or result in very few successful applications and a large percentage of SMEs are unable to access the available funds.

Challenges in accessing available private sector funding

SME owners' experiences with banks are that SMEs are prejudiced by banks' interest in the owner's skills and experience. Banks believe that the higher the managerial level of the owners, the greater will be the viability and potential survival of MSMEs. She will likely be successful and thus likely to have access to credit (Rudez and Mihahi, 2007).

GAP funding source for SMMEs

They also face problems in accessing information about creditworthiness and borrowing risk, as they do not have a credit history available to hand over to banks or credit bureaus (Falkena et al., 2013). There is less demand for loans in SMEs as many of them are reluctant to apply for a loan due to a number of perceived reasons such as fear of high rejection rates.

Equity and debt financing

The inability of SMME to afford the high costs associated with training and consulting services, and the other is that some see no need to improve their knowledge and skills (Aryeetey et al., 1994). According to the Finscope research (2010), the gap is further created by the number of people who do not use financial services or products and who use their own financing or financing from friends and family.

Summary of Chapter Two

This group does not even apply for financing because they have no knowledge about financial products and even if they did, they do not meet the minimum application requirements such as bank statements and financial credit information. This highlights the need for research to identify the challenges faced by SMEs in accessing financing support created for them.

Introduction

Study Design

Qualitative research

Why qualitative research was used in this study

Qualitative research methodology was used because the researcher considered this approach best for this research. Through qualitative research, the researcher comes face to face with the respondents, who share their personal behaviour, experiences and how their daily lives are affected (Eisner and Peshkin, 1990).

Data Collection

Ethical Issues

In this study, permission to conduct the study was sought from respondents who signed informed consent forms (Appendix 1), which set out the purpose and objectives of the study, as well as their rights to refuse to participate or withdraw to draw from the research. Respondents were informed that their names and companies would be kept confidential and that they would not be biased in any way.

Data Collection Process

- Primary data collection

- Secondary data collection

Wellman, Kruger and Mitchell (2005) stated the importance of ethical considerations in research, which ensure that researchers do not manipulate respondents and that they treat them with dignity when collecting data. The researcher followed the University of KwaZulu-Natal approved protocol for conducting the study prior to data collection (Appendix 3).

Interviews

Some notes were taken during the interview and later edited using the recoded interview. Some issues were not initially adequately explored in the way they would have liked.

Sampling method

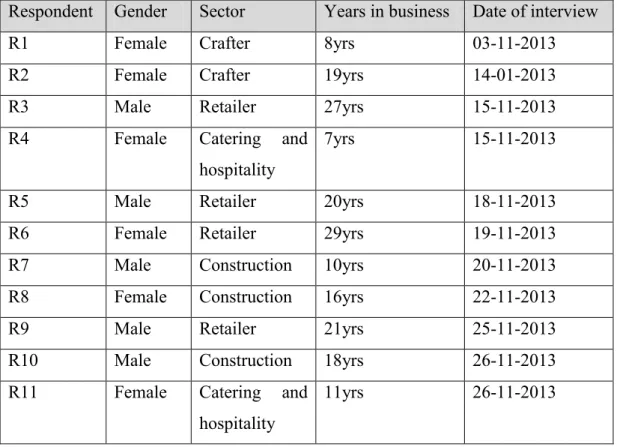

How is the information for financing disseminated so that the SMEs are informed about the available financing. Selection of different sectors was done to ensure that the sample used represented different sectors of UMzimkhulu SMMEs and the random selection method was used in each category to select SMMEs.

Data Analysis

Validity and Reliability

Limitation to methodology

Summary of Chapter Three

One of the questions asked in the interview wanted to know what the SMEs know about the government assistance financing schemes. The section above highlighted some of the suggestions and advice that the SMEs would give to prospective business owners.

Introduction

Requirements criteria from funders

Viable proposals or business plans

SMME’s as posing high risk

Their business was penalized for missing statements detailing the cash flow that would be demonstrated in the risk portfolio as part of the business plan. Previously disadvantaged SMEs have historically been undermined in the accumulation of traditional resources (Falkena et al., 2004).

Business regulations and legislation

On the topic of business registration, all respondents felt that it is difficult for rural SMEs as there are no institutions in UMzimkhulu that help with business registration. Thus, these respondents were of the opinion that it is very difficult in their geographical location to be able to fulfill all these legal requirements.

Lack of information and technology

Hence the lack of information about the various government funding schemes available for SMEs. From the information provided by the above respondents, it is clear that they still face the challenges of lack of information and technology.

Access to information and advice

Because of the imbalances of the past, the problem of information and advice is severe among the formerly disadvantaged, especially the blacks who are predominantly found in rural areas. There was also a proposal from the SMEs that the institutions providing support and advice should come to the rural areas to provide support and advice to the SMEs in the rural areas.

Lack of training in entrepreneurship and management skills

Here are some of the answers to a question about the source of funding for participating businesses. Most of the respondents indicated that when they started their businesses they had no knowledge of the organization of business finance issues and formalized financial management which was a disadvantage for them.

Required collateral security

There is a need for capacity development to be monitored and measured by the benefits received and the success of SME beneficiaries. How you applied for financing, describe the process step by step.

Summary o Chapter Four

Introduction

This research hopes to contribute to raising awareness of the funding needs of the entrepreneurs in rural areas such as UMzimkhulu Municipality. It is hoped that the research will also contribute to addressing the social imbalances of the past by categorizing funding according to the funding requirements of the SMEs such as start-up infrastructure for investment, capital for operating costs, a growth fund for business expansion and for those who funds needed for unexpected events that require urgent funding.

Short term recommendations

- Challenges with the banking sector

- Resolution on managerial skills and strategic planning

- Resolution on access to finance

- Resolution on Lack of Knowledge about funding available

- Access to banking services

The funders must also have motivated consultants and leadership in the institutions who have expertise in and understanding of the end user needs. The majority of the funding institutions require the financial statement for a minimum of three months which can only be provided by a person or business that has access to banking services.

Medium and long-term recommendations

Medium term recommendations

There is a need to do a research on the incentives that can be offered to these Business Angels. There is a need to introduce and promote subsidized credit and market it to SMEs.

Long-term recommendations

There is also a belief that they will develop innovation in the financial services sector and also increase competition in the financial services sector. To implement these recommendations, greater collaboration between different government departments, funding agencies and regulatory agencies is needed so that progress can be monitored and evaluated.

Conclusion

White Paper on the National Strategy for Small Business Development and Promotion in South Africa. DTI White Paper: "National Strategy for Small Business Development and Promotion in South Africa (1995)." published by the Department of Trade and Industry on 20 March 1995, (WPA/1995).