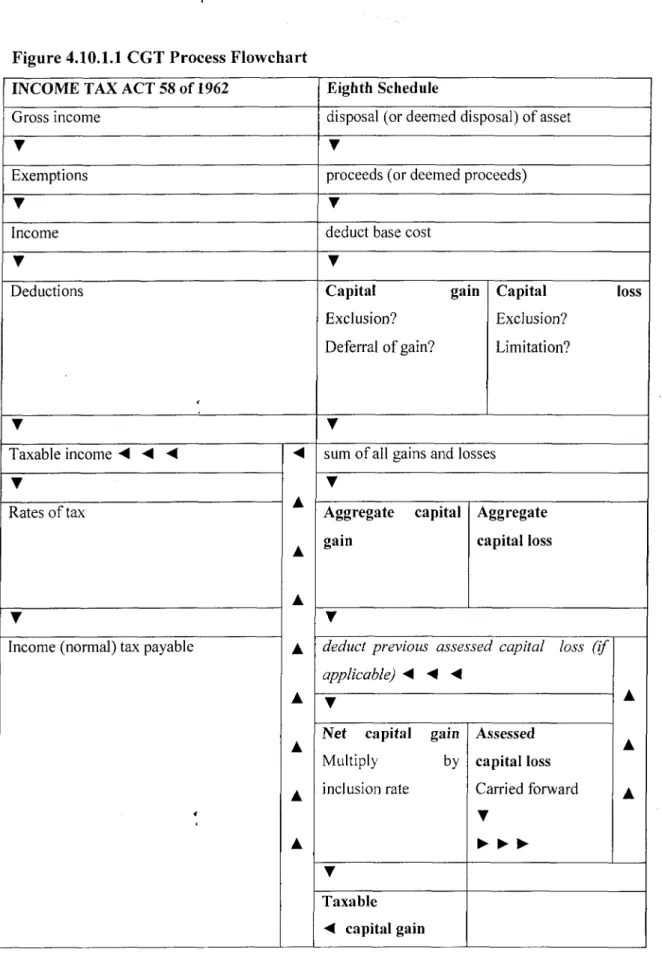

The Eighth Schedule to the Income Tax Act 58 of 1962 deals with disposals and deemed disposals. Any event, act, tolerance or operation of the law as contemplated in paragraph 11 of the Eighth Schedule, and.

Exclusions

The cost of valuing an asset for the purposes of calculating the capital gain or loss in respect of the asset. 20% of the proceeds upon realization can be considered as the basic cost (without records); or

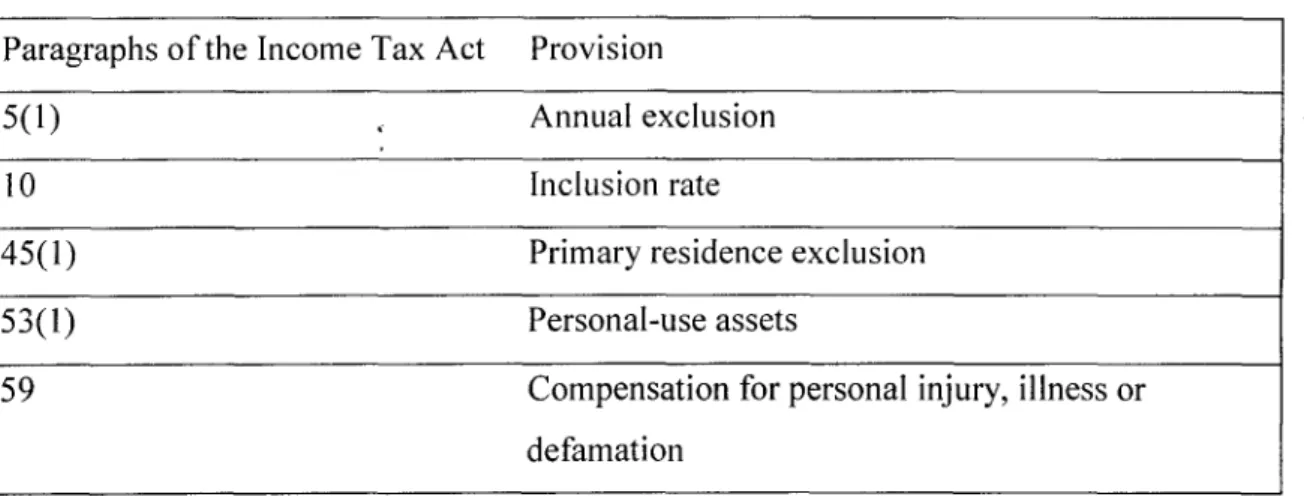

Annual exclusions

Taxable capital gain

Transitional measures relating to requirements relating to the valuation of assets at the date of assessment are contained in paragraph 29 of the Eighth Schedule to the Income Tax Act 58 of 1962. This is the responsibility of the taxpayer and the burden of proving a valuation belongs to the taxpayer.

CONCLUSION

If the Land Bank valuation is not used, it would be best for the taxpayer to record the details.

INTRODUCTION

General principles and definitions (paragraphs 44-46)

Because the maximum size of land that qualifies for the principal residence exclusion is two. The home is the eligible person's sole principal residence during the rental period.

Transitional rules on transfers from a company or trust (paragraph 51 of the Eighth Schedule to the Income Tax Act)

He was neither temporarily absent from the Republic during the rental period nor was employed or engaged in carrying on a business in the Republic at a place further than 250 kilometers from the residence during that period". and one year after the rental activity The qualified person is employed or engaged in carrying on business in the Republic in a place further than 250 kilometers from the residence or is temporarily absent from the Republic.

The natural person must have held, alone or together with his or her spouse, the entire share capital or membership interest of the company (from April 5, 200 I until the date of registration of the transfer in the register of deeds) or the natural person or his or her The spouse must have transferred the home to the trust by way of a gift, settlement or other disposition, or made money available to the trust to acquire and improve the home . The individual must have lived personally in the dwelling alone or together with his or her spouse and used the dwelling primarily for domestic purposes as his or her or their habitual residence from April 5, 200 I to the date of registration of the transfer in the deed register.

Multiple primary residences

Disposals

If the capital gain realized by the trust on disposal of the asset to a third party should accrue to a beneficiary of the trust in the same year as it arises, the capital gain must be ignored in the hands of the trust and treated as beneficiary gain. The receiver may not necessarily have the cash to pay the COT obligation if the trustee did not distribute the proceeds of the disposal to the receiver. The trustee now continues to hold the asset only in a representative capacity "on behalf of" the beneficiary.

The Eighth Schedule also provides that a capital gain arising by virtue of vesting a trust asset in a resident beneficiary must be disregarded in the hands of the trust and treated as beneficiary gain. Therefore, where the trustee distributes such an asset to a beneficiary with a vested right over the asset, there will be no CGT liability.

Donation to a trust

It must be registered in the name of the person who made the donation, settlement or other similar disposition, or financed all the expenses, or in their name together with the person's spouse, in order to be entitled to the transfer tax exemption. The natural person acquires this residence from the relevant company or trust on or after the publication of the Tax Law, 2001, but no later than the 30. The natural person or together with his spouse directly owned the entire share capital of the relevant company. company from 5 April 2001 to the date of registration in the deed book of the residence in the name of the natural person concerned or his spouse or in their name jointly, or.

The natural person alone or together with his spouse or his habitual residence from 5 April 2001 to the date of registration, and. Registration of the place of residence in the name of the natural person or his spouse or in a partnership takes place no later than 31 March 2003.

Loan account with trusts

Taxpayers may take advantage of the above concessions with effect from the date of promulgation of the Act". The annual remission or reduction of a loan to a trust amounting to R30 000 would therefore result in a capital gain of R30 000 in the hands of the trust, which However, if the lender should also be a beneficiary (or a relative of the beneficiary) of the trust, the capital loss realized by the lender on the partial reduction or waiver of the loan will be capped.

It has been suggested that one must annually surrender R30 000 of the loan into the trust, effectively extinguishing a loan to that extent and avoiding the adverse COT consequences of a loan write-off or reduction. However, care must be taken that the transaction may not be viewed as 'abnormal', thereby meeting one of the requirements of the anti-avoidance provisions in the Income Tax Act."

Conclusion

Inheritance rights on the acquisition of the home that will constitute that person's primary residence (section 9 of the Inheritance Act, No 40 of 1949). The transfer must be exempt in terms of either section 9(16) or 9(17) of the Transfer Rights Act. b). The natural person acquires the residence of the company on or after the promulgation of the Tax Laws Amendment Act, 200 I but not later than 30 September 2002;.

The natural person alone or together with his spouse lived personally and usually in the residence and used it mainly for domestic purposes as his or her usual residence from 5 April 2001 until the date of the registration; and. The registration of the residence in the name of the natural person or his spouse or in their names jointly takes place no later than 31 March 2003.

The residence and use requirement

34;Direct" means that the share or interest in the company must be registered in the names of the individuals concerned and for their own benefit. The exception applies to the primary residence and the land on which it is located, including unconsolidated Land exceeding two hectares will not be eligible until exempt and will therefore be subject to transfer duty and CGT.

For exempt spouses, whose residence is the company, it cannot be transferred in the name of the spouse who does not have shares. If each spouse owns a percentage of the shares (insignificant amount), the sum of which constitutes 100% of the shares, the transfer of residence in the name of each of the spouses or in their joint names will qualify for exemption”.

THE CAPITAL GAINS TAX FOR COMPANIES

The Eighth Schedule provides four key definitions that form the basic building blocks in determining a person's capital gain or loss. However, the improvement or expansion must be reflected in the condition or nature of the asset at the time of disposal. As this is the first year that CGT has been introduced, XYZ (Pty) Limited has no estimated capital loss compared to the previous year.

Note that an estimated capital loss can only be deducted from capital gains and added to capital losses. The taxable capital gain will be included in the taxable income of the company and will be taxed at the rate of 30%, i.e.

Conclusion

TRANSFER DUTY

Residential Properties held in Discretionary Trusts

These settlements will be in terms of the settlement provisions contained in Section 88D of the Income Tax Act, 1962, which shall apply mutatis mutandis to the Transfer Duty Act. 34; No duties are payable in respect of the acquisition of real estate by: (a) The government and the provincial government; The exemption from transfer tax under section 9 (15) of the Transfer Duty Act, No. 40 of 1949 applies only if: A).

SARS receives many declarations that are filled in incorrectly or where the signatures on the documents are clearly not those of the transferors and transferees. Customers involved in such schemes are advised that there are provisions in section 50A of the VAT Act to prevent VAT avoidance in these circumstances.

Estate agents required to report certain transactions

The acquisition of the home must be by a natural person and that home must constitute that person's primary residence for CGT purposes when it is acquired by that natural person. The person in question or his spouse must have habitually resided in this residence and used it mainly for domestic purposes as his or her residence from 5 April 2001 to the date of registration in the deed book of the residence in the name of the person in question and that person's spouse; and. All the shares in a company must have been owned by the natural person or his spouse between 5 April 2001 and the date of the registration of the property in the land register.

After division or disposal, the property must meet the criteria of being the principal residence of the person making the transfer; Taxpayers should benefit from the above with effect from the date of promulgation of the law.”

CONCLUSION

A property investor will be liable to pay income tax on the rental income and capital gains tax (CGT) on the profit made on the sale of the property in the normal way you would expect. A real estate dealer (also known as a trader) will find that all of their profit from the sale of a property is taxed as income tax rather than capital gains. The profit inclusion rate is 25% and they also enjoy an exemption of RIO 000 on the capital gains they have made.

For SARS to increase their income, they need to reduce the exemption from R1 million to R500 000 per primary residence, and also increase the inclusion rate from 25% to 50% on capital gains obtained from the sale of primary residence, and finally increase the exemption from RIO 000 to R 15 000 and the tax payers can appreciate it. The treatment for CBT at the disposal of their residence is not similar with individuals.