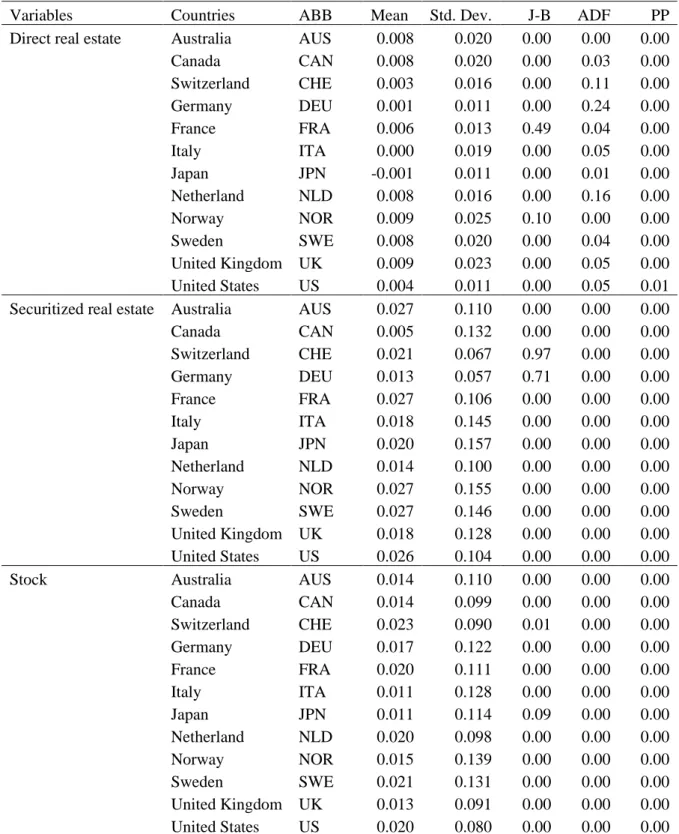

Notably, our analysis includes two classes of real estate markets, namely securitized real estate and direct real estate. Taking the role of the securitized real estate market in relation to the conventional real estate market as an example. Pairwise net linkage analysis allows us to explore the hybrid feature of the securitized real estate market.

The finding is in good agreement with the literature, as it confirms the hybrid characteristic of securitized real estate. Nevertheless, in the 1990s, the real estate market characteristic of securitized real estate increased significantly, reflecting the nature of the underlying direct real estate. Data on securitized real estate are taken from the latest international Standard and Poor (S&P) Global property research (GPR) database.

Both real estate investment trusts (REITs) and investment and development real estate companies are included in the indexes (Stevenson, 2016). The data on the securitized real estate and equity markets are extracted from Thomson Reuters Eikon. As a result, a remarkable stock market crash followed in both securitized real estate and general stock market.

Questions remain, however, about how the relationship fluctuates over time, and whether the securitized real estate market is more closely related to the direct real estate or stock markets.

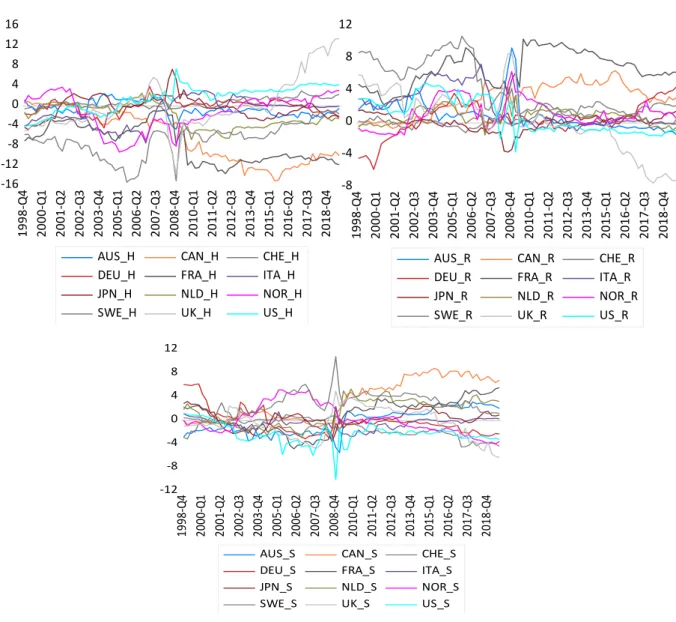

Dynamic net directional connectedness

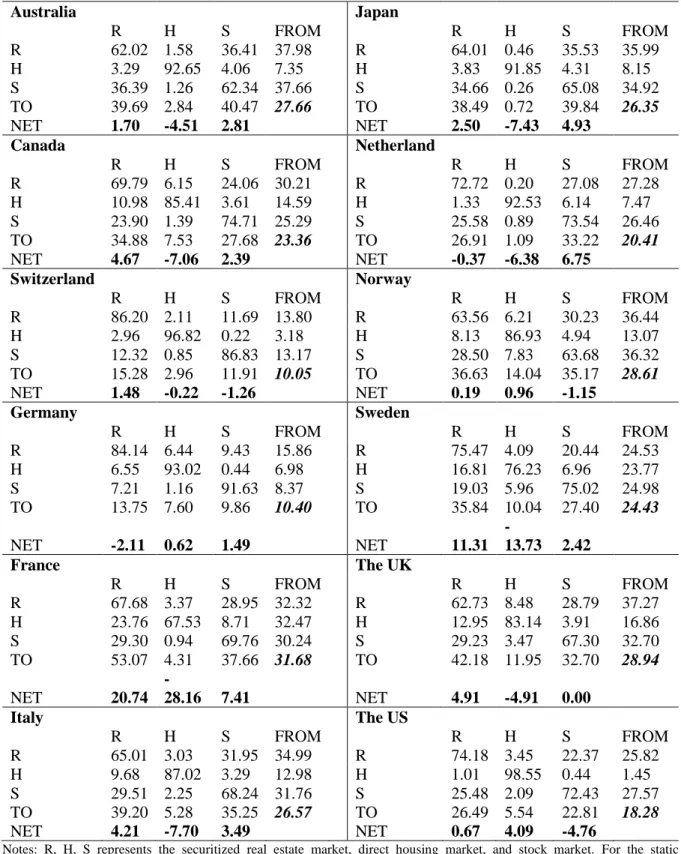

In Australia, the shock-transmitting role of securitized real estate during the financial crisis is clearly visible as the net connectedness of securitized real estate reaches unprecedented levels, implying its significant influence on the equity and direct real estate markets. We also found strong evidence of the leading role of securitized real estate in Canada, France, the Netherlands, Norway, Sweden and the United Kingdom. While the securitized real estate market tends to provide information to shape the other markets during the financial crisis, the opposite pattern is observed given the US context.

Although securitized real estate is found to be the net shock transmitter during the economic calm phase, the GFC sees its move to become the net shock receiver. Conversely, the US direct housing market appears to stimulate the adjustments of the other markets during the onset of the GFC, reflected by its high positive level of net connectedness. As previously mentioned, the GFC is associated with the failure of the direct housing market and its adverse impact on the other financial markets is probably the key explanation for the transferability of the direct property.

In line with our article, a study by Miyakoshi, Shimada, and Li (2016) covering the period from 2003 to 2014 showed that the fundamental value of J-REIT was mainly explained by its real estate price. In particular, the effect of real estate on securitized real estate has been strengthened as a result of the 2008 crisis. The dependence of securitized real estate on the conventional real estate market, as suggested by Miyakoshi et al. 2016), was determined by the country's 'scarcity' and 'safety' norms in real estate development.

That the securitized real estate that has their attention in terms of efficiency and strong seismic safety will obtain higher real estate income explains why the securitized real estate is affected by the real estate price. It has been suggested that the US subprime crisis will boost Japan's direct real estate market (Seko et al., 2012), as market yields fell by 10% in 2009 alone. Japan's real estate market was also the only one of all real estate markets studied to register negative average returns over the sample periods.

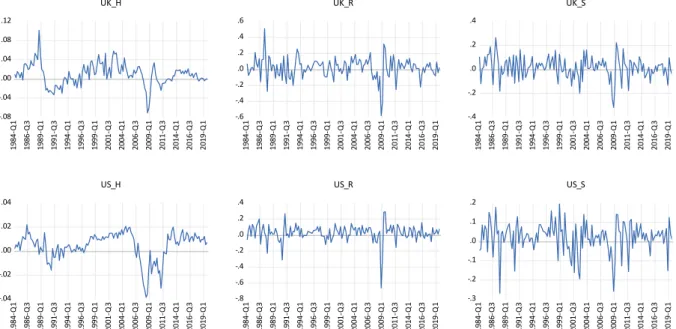

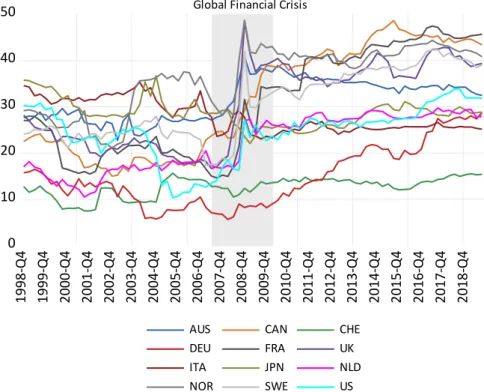

Given the importance of Japan's direct housing market, coupled with the fall in house prices as a result of the GFC, it is highly likely that securitized property will be hit hard. Overall, Figure 3 establishes the dominant role of the securitized real estate market as a net transmitter, while the direct housing market appears to be influenced by others. During the GFC period, some countries (the UK, Norway and Sweden) recorded positive net stock market correlation, while others (Australia, France, the Netherlands, Japan and the United States) had a negative value.

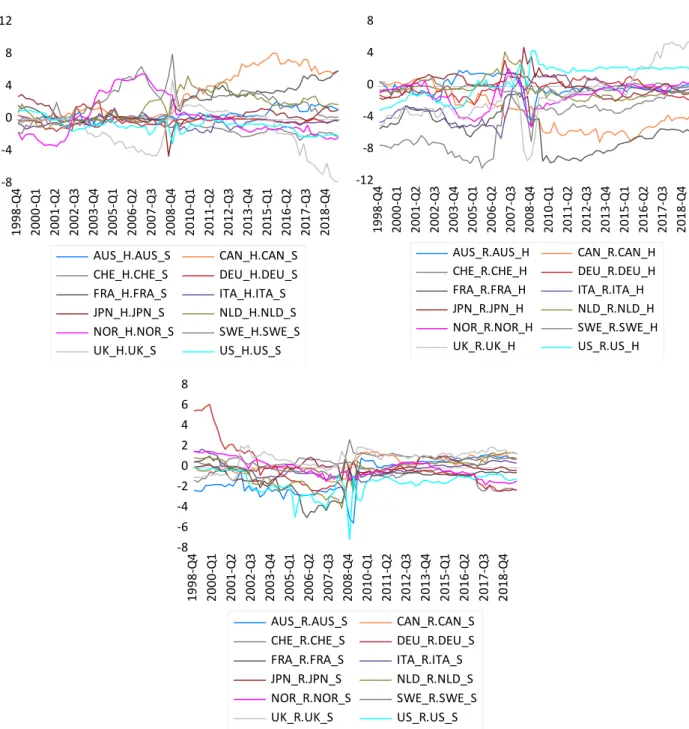

Dynamic net pairwise connectedness

The role of the securitized real estate market in transmitting information to the underlying real estate market is actually nothing new in the literature (see Barkham and Geltner (1995); Giliberto (1990); Gyourko and Keim (1992). Market liquidity partially justifies the faster response to securitized real estate market information than direct market. Specifically, during the onset of the GFC, the Australian securitized property market was identified as a key source of turmoil.

Likewise, Canada, France, Great Britain, the Netherlands, Norway and Sweden register the shocks that are transmitted from the securitized real estate market to the private housing market. On the other hand, in the United States, although the leading role of the securitized real estate market over the direct housing market is dominant, the GFC provides an unprecedented opportunity to observe the change in the position of direct real estate, from mainly receiving shocks to spread shocks to the securitized property. According to Damianov and Elsayed (2018), the direct housing market was generally found to be a transmitter of information during recessions and housing busts, but in the recent GFC period it was a recipient of spillovers from the securitized property market.

In detail, the shock in the period of the global financial crisis first occurs at the country level, from the direct housing market to the securitized real estate market in the US. Therefore, the result highlights the shock-transmitting capacity of the securitized real estate, which partly explains the global impact of the subprime mortgage crisis, starting in the US direct real estate market and affecting the housing markets of a number of countries. Given the low connectivity between Japan and the US among securitized real estate, the impact of the GFC on Japanese securitized real estate is less clear.

Instead, the GFC observes the key role of the Japanese securitized real estate as the net shock receiver, which is significantly affected by the alternation of the conventional housing market. In addition, it is important to determine whether securitized real estate is more connected to the direct real estate market or the stock market. Similarly, Clayton and MacKinnon (2003) specified increasing sensitivity of direct real estate REITs through time.

The growth in the maturation of the securitized market since 1992 provides a plausible explanation for the increasing connection between two real estate markets (Clayton & MacKinnon, 2003). The growth and maturation of the securitized real estate market actually makes information more accessible and easier to distribute. Finally, regarding the last pair of the direct property and stock markets (H-S), while the connection between them is clear (Antonakakis & Floros, 2016;.

6 Conclusion

The former two effects suggest the positive correlation between the stock and housing markets, while the substitution effect implies the negative relationship between them. Given the higher returns of real estate compared to the stock market, an outflow of capital from the latter to the former and vice versa is expected. Overall, these effects illustrate the relationship between the housing market and the stock market.

Thus, Ali and Zaman's (2017) study on 22 OECD countries confirmed the asymmetric relationship between two markets. It means that country-specific events and market characteristics play a crucial role in explaining the transmission of the shock between markets. Also, the conclusion that the securitized real estate is able to spread shocks to the immediate housing market opens up a research venue for exploring the potential directional factors.

Securitized real estate and its relation to financial assets and real estate: an international analysis. Co-movement and causality between the US housing and stock markets in the time and frequency domain. Paper presented at the seminar of Narodowy Bank Polski: Recent trends in the real estate market and its analysis-2015.

The impact of the global financial crisis on Asia-Pacific real estate markets: Evidence from Korea, Japan, Australia and US REITs. Notes: AUS, CAN, CHE, DEU, FRA, ITA, JPN, NLD, NOR, SWE, UK and US stand for Australia, Canada, Switzerland, Germany, France, Italy, Japan, Netherlands, Norway, Sweden, the United States Kingdom and the United States. AUS, CAN, CHE, DEU, FRA, ITA, JPN, NLD, NOR, SWE, UK and US stand for Australia, Canada, Switzerland, Germany, France, Italy, Japan, Netherlands, Norway, Sweden, United Kingdom , and the United States.