Topic: Internship report submission on 'Analysis of Credit Management System of Bangladesh Krishi Bank (BKB): Study on Karwan Bazar Branch, Dhaka'. I have prepared my internship report on Credit Management System Analysis of Bangladesh Krishi Bank (BKB): A Study in Karwan Bazar Branch, Dhaka'. I am pleased to confirm that the internship report on Credit Management System Analysis of Bangladesh Krishi Bank (BKB): A Study on Karwan Bazar Branch, Dhaka' conducted by Arifa Afroze Mousumi with No. MBA Program ID, Department of Business Administration has been approved for submission and defense.

Jasmin Akter worked as an intern under my supervision at Bangladesh Krishi Bank (BKB): A Study on Karwan Bazar Branch, Dhaka. Bangladesh Krishi Bank (BKB), the country's largest specialized bank, was established under President Order No. In this report, I have discussed in detail about the “Credit Recovery and Disbursement” of Bangladesh Krishi Bank.

In the third chapter, the evaluation of the lending policies and activities of the credit management system of Bangladesh Krishi Bank is described in depth. Throughout this report the discussion about the credit management system of Bangladesh Krishi Bank are drawn up step by step.

Secondary Sources

Overview of the Organization

2.1) Overview of Bangladesh Krishi Bank

To manage the bank in accordance with the government's policies and supervisory bodies, BKB has a distinguished board consisting of the chairman and ten other board members appointed by the government. It gives credit to farmers, marginal farmers, extreme poor, sharecroppers and also to the mass population of Bangladesh who are the real players in creating agricultural production and success in the rural economy. It conducts its business in all types of export, import, remittance and other types of foreign exchange business.

This helps in developing the marketing channels of the agricultural products of the companies under easy terms and at a lower interest rate. Bangladesh Krishi Bank was established under the order of BKB`1973 with the objective of strengthening the rural economy by extending credit support to agricultural and agricultural sectors. In order to be prepared for survival and growth in a dynamic market environment, banks strive.

Keeping this in mind Bangladesh Krishi Bank has introduced digitized system, Computerized Banking and Core Banking Solution (Online Banking), Automated Teller Machine (ATM), BACH, RTGS, NPSB services. BKB takes steps towards digitization to provide its valuable customers with modern and high level banking facility.

2.2) Mission

2.3) Vision

2.4) Core Values

2.5) Corporate Profile

2.6) Hierarchical Structure of BKB

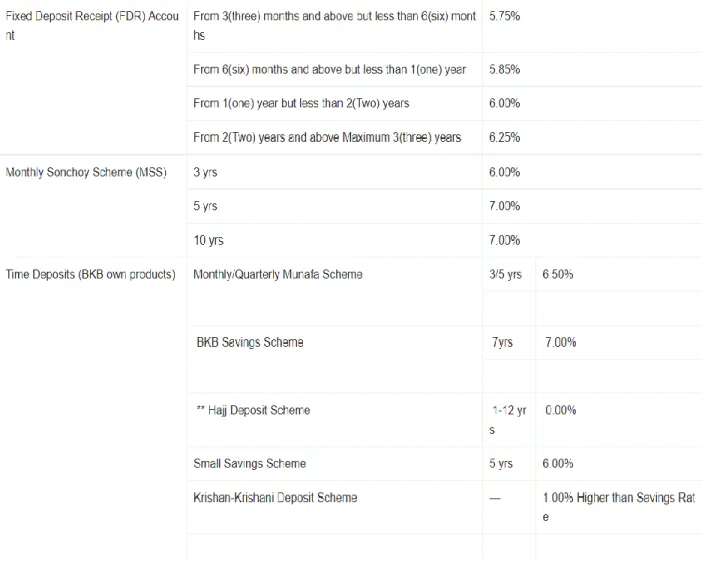

2.7) Types of Deposit

2.8) Types of Credit

Analysis of Credit Management System of BKB

Short term loan 2. Medium term loan

It is very certain that agriculture is still the most important and productive sector in Bangladesh. It plans to develop infrastructure for credit purposes so as to provide credit to all agro-based sectors. The amount allocated annually to the credit system, of which 60% is fixed for the agricultural crops sector.

Fish growing in fresh water, for example we can say that water growing in canal ponds and other fresh water sources are part of this program. Production of shrimp fingers in fresh water using the modern and up-to-date technology. With a view to creating self-reliance for the poor and unemployed of the country, the bank has introduced a new program titled “Beef Fattening”.

The bank provides revolving loans for various types of activities such as cash credit/short-term working capital loans. To meet the changing demands of this sector, BKB offers credit facilities for both the production and marketing of various agricultural and agricultural machinery, including irrigation equipment. All types of irrigation equipment such as LLP, HPTW, STW, DTW are eligible for the sector.

Being an agriculture-based country, various types of crops and fruits are regularly produced in this country. The agro-based industries are poultry farms, dairy farms, food processing plants, fish freezing/processing industries etc. Recognized and reputed businessmen and foreign investors are encouraged by the bank to set up any type of agro-processing industry in Bangladesh.

Over time, the traditional farming system is replaced by machines and modern tools. In order to accommodate this change, Krishi Bank has offered loans which are efficient for both parties involved in production and marketing of allied sectors. BKB has just declared the political strategies and financing norms in accordance with the business policy 2005 regarding SMEs.

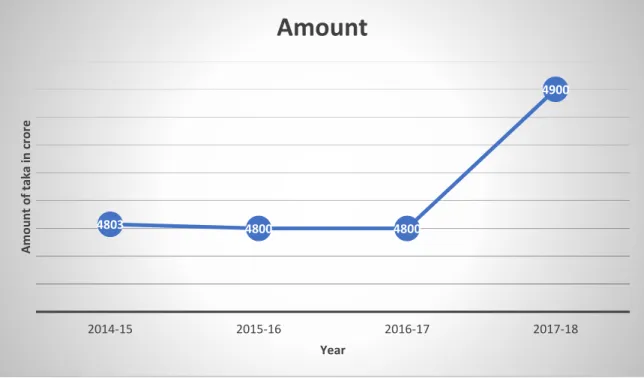

In Crore Tk)

Change

Chart: Loan Disbursement Scenario of Total Agricultural Loan

Amount

3.336 Million

It is on its way to its goal of bringing more people under this credit scheme, so that more people can benefit, more people can develop their situation and generally have an impact on countries' development.

Chart: Total Loan Recover in Percentage

Sector wise Disbursement of credit

Table of Crops Sector Credit Disbursement

Chart: Crops Sector Credit Disbursement

Table of Fisheries Sector Credit Disbursement

Table of Livestock Sector Credit Disbursement

Chart

Table of Agricultural Equipment Sector Credit Disbursement

Table of SME Sector Credit Disbursement

3.7) The salient features of the credit management of Krishi bank is mentioned below

SWOT ANALYSIS of BKB

5.1) SWOT ANALYSIS OF BANGLADESH KRISHI BANK

Basically, there have been some weaknesses of this bank since it started, which is related to in general cases for borrowers as well as the bank itself, the salient features of the weakness in BKB are briefly described below. The Barga-chashis, who are the major sections of the fastidious society, could not be brought under this loan or credit system due to the issue of mortgage or any security factor. Sometimes, in order to get loans, people have to appease the organizations or people who are in the government and have muscle power.

Sometimes the village head uses muscle power to exploit the people who want to borrow from the bank.

Findings, Recommendations & Conclusions

6.1) Findings

6.2) RECOMMENDATIONS

Since in today's busy life there is very little time for people going to the bank to withdraw money, it will be time consuming. Everyone prefers to be able to withdraw money quickly in case of emergency, hence the need for ATMs. In case of agriculture-based industry loans and revolving credits etc., an online credit disbursement program should be introduced.

More transparency, accountability, and complete professionalism should be ensured in the delivery of loans from branches other than the bank. Borrowers should submit all kinds of necessary documents and documents to the bank before availing the loan facilities so as to avoid any kind of complexity for both the parties. Fake loans, such as loans to non-existent people, can be reduced if a branch makes public loans at the syndicate level.

For the sake of transparency in credit disbursements, emphasis has been placed on public disbursement of loans at the union level by the bank.

6.3) CONCLUSION