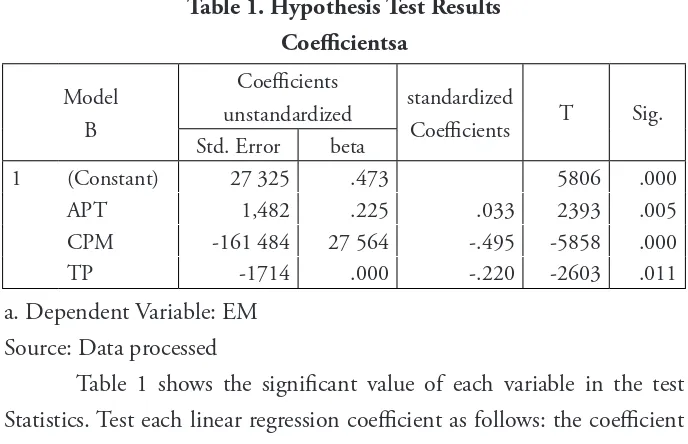

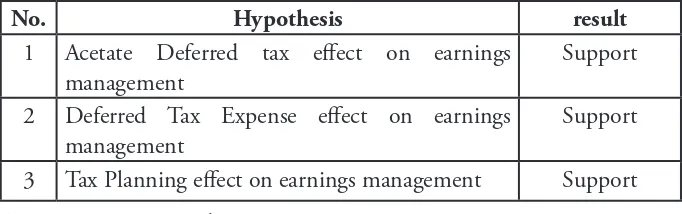

Deferred Tax Assets and Deferred Tax Expense Against Tax Planning Profit Management

Teks penuh

Gambar

Dokumen terkait

Menurut Skousen dan stice (2009: 563) Pendapatan (revenue) “ merupakan arus masuk atau peningkatan aktiva lainnya sebuah entitas atau pembentukan utangnya atau sebuah

Tujuan penelitian ini adalah menganalisis respon mekanik produk Speed Bump dari bahan Concrete Foam diperkuat serat tandan kosong kelapa sawit (TKKS) yang dikenai beban impak

resistansi dan sensitvitas sensor gas dengan variasi tekanan : 3×10 -2 , 4×10 -2 , 5×10 -2 , 6×10 -2 ,dan 7×10 -2 Torr masing-masing dengan waktu deposisi selama : 30, 60, 90

Sementara itu, Bappenas lebih berperan pada sisi perencanaan, yaitu mulai dari desain awal kajian yang ditujukan untuk mengakomodasi berbagai masukan

Mengenai pimpinan RUPS yaitu Direktur Utama, dan jika tidak dapat dipimpin oleh direktur utama alternatifnya RUPS dipimpin oleh Komisaris utama atau Presiden

Penggunaan periode pengumpulan data dengan menggunakan periode laporan keuangan triwulan bank syariah yang terdaftar di Bursa Efek Indonesia yaitu dua tahun sebelum dan

land pozzolan, semen bara dan semen portland yang dimodifisir dengan bara. Semen portland bara yang dikeringkan dalam dapur api mempunyai panas hidrasi yang lebih rendah

Tujuan penelitian ini adalah membangun sebuah Sistem Informasi Akuntansi berdasarkan komputer yang dapat diaplikasikan pada UKM Kampung Kue Rungkut Surabaya sehingga memudahkan