Journal of Accounting in Emerging Economies

Int ernet f inancial report ing in an emerging economy: evidence f rom Jordan Munther T. Momany Husam-Aldin N. Al-Malkawi Ebrahim A. MahdyArticle information:

To cite this document:Munther T. Momany Husam-Aldin N. Al-Malkawi Ebrahim A. Mahdy , (2014)," Internet financial reporting in an emerging economy: evidence from Jordan ", Journal of Accounting in Emerging Economies, Vol. 4 Iss 2 pp. 158 - 174

Permanent link t o t his document :

http://dx.doi.org/10.1108/JAEE-04-2012-0015

Downloaded on: 24 March 2017, At : 21: 10 (PT)

Ref erences: t his document cont ains ref erences t o 39 ot her document s. To copy t his document : permissions@emeraldinsight . com

The f ullt ext of t his document has been downloaded 466 t imes since 2014*

Users who downloaded this article also downloaded:

(2014),"Corporate governance efficiency and internet financial reporting quality", Review of Accounting and Finance, Vol. 13 Iss 1 pp. 43-64 http://dx.doi.org/10.1108/RAF-11-2012-0117

(2014),"The determinants of internet financial reporting in Slovenia", Online Information Review, Vol. 38 Iss 7 pp. 842-860 http://dx.doi.org/10.1108/OIR-02-2014-0025

Access t o t his document was grant ed t hrough an Emerald subscript ion provided by emerald-srm: 602779 [ ]

For Authors

If you would like t o writ e f or t his, or any ot her Emerald publicat ion, t hen please use our Emerald f or Aut hors service inf ormat ion about how t o choose which publicat ion t o writ e f or and submission guidelines are available f or all. Please visit www. emeraldinsight . com/ aut hors f or more inf ormat ion.

About Emerald www.emeraldinsight.com

Emerald is a global publisher linking research and pract ice t o t he benef it of societ y. The company manages a port f olio of more t han 290 j ournals and over 2, 350 books and book series volumes, as well as providing an ext ensive range of online product s and addit ional cust omer resources and services.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation.

*Relat ed cont ent and download inf ormat ion correct at t ime of download.

Internet financial reporting in

an emerging economy: evidence

from Jordan

Munther T. Momany

Faculty of Business, ALHOSN University, Abu Dhabi, United Arab Emirates

Husam-Aldin N. Al-Malkawi

Faculty of Economics and Administration, King Abdulaziz University,

Jeddah, Saudi Arabia, and

Ebrahim A. Mahdy

Faculty of Economics, Damascus University, Damascus, Syria

Abstract

Purpose– The purpose of this paper is to examine the status of financial reporting on the internet by companies operating in an emerging economy, namely Jordan.

Design/methodology/approach– The paper surveys 127 companies listed in the first market of Amman Stock Exchange (ASE) for the year ended 2008/2009. The primary sources of the data used in this study are the global and the Jordanian electronic web sites. The paper employs descriptive statistics and nonparametric tests to explore the internet financial reporting (IFR) practices among Jordanian companies.

Findings– The results show that 87 Jordanian companies (69 percent) possess web sites with about 51 percent (44 of the 87) include financial reports and 32 out of 44 companies (about 73 percent) disseminate all their financial information on their web sites. The paper also finds that the extent of disclosure of the corporate financial and nonfinancial information on the ASE web site is statistically different form the companies’ web sites. Furthermore, the current paper reveals that some firm-specific characteristics such as firm size; financial leverage, age, and ownership concentration may distinguish those companies who engage in IFR from their counterparts. Finally, the results suggest that the financial sector is more advanced in terms of using the internet to disseminate information when compared to the industrial and services sectors.

Originality/value– In the context of Jordan, there is limited number of studies attempted to address corporate financial reporting on the internet. Therefore, the present study makes significant contribution to the existing body of knowledge by shedding more light on the status of financial disclosure on the internet by companies operating in an emerging economy like Jordan. Also, the current paper explores the extent of corporate information disclosed on both the official web site of ASE and companies’ web sites.

Keywords Internet, Voluntary disclosure, Jordan, Financial reporting, Firm characteristics Paper type Research paper

1. Introduction

A firm’s accounting information system is an important part of its overall information system. It has a special purpose in collecting, processing, and presenting the financial data to all users. Firms can disseminate their financial information using different means either through specialized news papers (paper-based reports) or various electronic devices. The information technology witnessed significant changes especially by the end of the twentieth century. However, the use of internet for financial reporting is considered new phenomenon but rapidly growing (Oyelereet al., 2003). Internet financial reporting (IFR) can be defined as “the use of the firm’s web to disseminate information about

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/2042-1168.htm

Journal of Accounting in Emerging Economies

Vol. 4 No. 2, 2014 pp. 158-174

rEmerald Group Publishing Limited 2042-1168

DOI 10.1108/JAEE-04-2012-0015

158

JAEE

4,2

the financial performance of the corporations” (Mohamed and Oyelere, 2008, p. 36). Copious numbers of companies around the world publish their financial data on their web sites. The amount of information disclosed is actually varied among firms. Some companies publish comprehensive financial statements, while others publish partial or summary financial statements or just financial highlights.

There are number of advantages for using IFR as compared to the conventional reporting (Mohamed and Oyelere, 2008). These advantages can be summarized, for example, as follows: IFR is less costly; allows firms to communicate more information to a large number of stakeholders; improve financial disclosure by providing more timely information; increase frequency of financial disclosure; increase quantity of financial and nonfinancial information; increase the interest in the company by financial analysts and investors; and increase share liquidity and lowers the cost of capital. However, IFR suffers from several limitations related to regulations and standards, external audit issues, and nontechnological factors (see Momany and Al-Shorman, 2006, pp. 128-129).

Despite the large body of research on IFR practice[1], an examination of this issue in the Middle East region is currently not well established in the literature. In the context of Jordan, there is limited number of studies attempted to address corporate financial reporting on the internet. Therefore, the main purpose of the current study is to fill some of the gap in the literature by shedding more light on the practice of financial disclosure on the internet by companies listed on the Amman Stock Exchange (ASE). The objectives of the paper are threefold. First, to find whether Jordanian companies possess active web sites and what type of information they publish on these web sites. Second, to see whether the information disclosed in their web sites are different from those available on the ASE web site. Third, to reveal the relevant characteristics of those companies that uses the IFR.

The reminder of the paper is organized as follows. The next section discusses the significance and motivation of the study. Section 3 elaborates on the theoretical background. Section 4 provides a review of the literature. Section 5 describes the data collection and the methodology. The results of the study and the discussion are presented in Section 6. Summary and conclusions are presented in the final section.

2. Significance and motivation of the study

The Jordanian “government has long recognized the need for establishing business-enabling structures with strong investment incentives. Developing an efficient regulatory framework activates the role of the private sector, increases the volume of domestic investment, and attracts inward international investment. A wide-ranging legislative package has been drafted and introduced to foster a more efficient and transparent business environment” such as the Income Tax Law, Securities Law, Investment Promotion Law, and Companies Law (www.kinghusseine.gov.jo/economy3.html).

Jordan has adopted IFRS (IAS) since 1990 and all Jordanian companies must prepare and publish its financial statements in accordance with those standards. Nowadays, companies in Jordan make every possible effort to build more trust in their published financial statements which become the main source of information for all stakeholders in the securities markets, to attract more local and foreign investors, and decrease the cost of information process, by publishing their financial statements voluntarily on their web sites, particularly after the rapid increase in demand for internet lines in Jordan to almost 18 times within four years period, or 89 percent increase in 2006 compared to 2005. The last decade has witnessed significant increase in the number of the internet users in Jordan. For example, in 2010 the number of

159

IFR in an

emerging

economy

internet users has reached to 1,741,900 (27.2 percent of Jordan’s population) compared to 457,000 (8.7 percent of Jordan’s population) in 2002 (Internet World Stats: Usage and Population Statistics (2012)).

In addition, Jordan is considered to be one of most advanced countries in the Middle East region in terms of information and communication technology (ICT). To demonstrate, in 2010 the World Economic Forum and INSED published the Global Information Technology Report 2009-2010 which includes an index called Networked Readiness Index (NRI). This index “has provided a methodological framework that identifies the enabling factors for countries to fully benefit from ICT advances while highlighting the joint responsibility of all social actors, namely individuals, businesses, and governments, in this respect” (p. v). The findings of the NRI showed that Jordan appeared in the top half of the NRI rankings. It ranked 44 among 133 countries including developed and developing economies and only four countries from the Middle East region were ranked above Jordan. Therefore, these developments in the internet usage and ICT in Jordan have motivated the current study to examine the impact of these advances on IFR among Jordanian companies. Furthermore, although the present paper is an extension of prior research and builds on the same lines of research conducted earlier, this study, to the best of our knowledge, makes original contribution to the body of knowledge as it is the first study to examine whether the information disclosed on sample companies’ web sites are different from those available on the ASE web site, thus providing a more focussed and specific result. Finally, the study tries to disclose the relevant characteristics of those companies that use IFR in Jordan and also provides a valuable insight into IFR in such emerging economy which will benefit all stakeholders.

3. Theoretical background[2]

The current section provides an overview of some relevant theories which sets concrete and explanatory grounds for IFR. There are several fundamental theories in the context of the importance and necessity of IFR. The Shannon and Weaver (1949) model specifies three elements as fundamental to IFR namely the information source, the channel, and the destination. The company is regarded as the main source of information for the usage of internet while internet itself forms the channel of information distribution. The destination refers to the different users who base their investment decisions based on the online reports. Another theory backing IFR is the Entity Theory which emphasizes the role of accountability and satisfaction of legal requirements (Paton, 1962) which in turn satisfies various stakeholders and the regulatory bodies. Meanwhile the Enterprise Theory formulated by Suojanen (1954) share some similarity with the Entity Theory as it also regards a firm as a socially responsible institution whose decisions affect a vast number of stakeholders. Therefore, reliable and complete information has to be disseminated in order to satisfy these stakeholders. On the contrary, Posner (1974) advocated the Regulatory Capture Theory which relied on the concept that the regulated companies may come under less control of the regulatory bodies in the sense that companies who report online are not subjected to regulations over the quality of their reporting as they have already fulfilled the basic conditions of reporting online. Another theory backing the relevance of IFR is the “The User’s Cognitive Learning Process” as suggested by Hodgeet al.(2002). Here the theory emphasizes that the extent of information absorption is more online than from the main body of the financial statements. The Information Foraging Theory, developed by Pirolli and Card (1999) also echoes the same benefits of online reporting as discussed in the former theory. Both the theories emphasize the convenience and usefulness of online reporting for stakeholders and the satisfaction derived from it.

160

JAEE

4,2

The Information Overload Theory developed by Rao (2002) gives another dimension to the concept of IFR. The theory expressed the extent of pressure witnessed by users with the magnitude of information disseminated by companies. On the contrary if the company’s web site is structured and user friendly, the impact of information overload will be minimal, with the user being guided to the information desired, efficiently. Orlowski’s (2003) Quantum Theory supports the IFR in the context of the value of the information given online to different users, in the main language, as well as other languages.

In addition, the Post Modern Communication Theory by Massumi (1987) describes the nature of the information as either Arbolic: uniform and rigid or Rhizomatic, allowing company’s complete flexibility as to the kind of financial information placed on the web sites. Another well known theory acting as a fundamental base for IFR is the Upper Echelons Theory as propounded by Hambrick and Mason (1984). The theory focusses on the characteristics of the top management team, in particular, the upper echelon of an organization and explains that top managers differ in their perceptions and ideology, which provide signals of how they will act (Goll and Zeitz, 1991). Upper-echelon theory plays a role in disclosure (Lubatkinet al., 2007) since there is no current unifying theory of disclosure (Verrecchia, 2001). The theory states that the top executives have a significant role in influencing the decisions in an organization and have greater access and control over corporate information. This in turn leaves it to their discretion the extent of release of certain information, specifically voluntary information related to the firms.

Furthermore, Agency Theory offers explanations to the importance of IFR as the theory documents that voluntary disclosure lowers agency cost which arises from a difference of interest between the principal and agent. By disclosing material facts about the company through the internet, the company can win the support and trust of various stakeholders. Similarly, the Signaling Theory by Spence (1973) indicates that the extent of IFR distinguishes one firm from another on dimensions such as quality and performance. Online reporting reduces information asymmetry and such reports will be credential in terms of getting potential and prospective investors and creditors. Lastly the Innovation Diffusion Theory assumes that intra organizational structures such as accounting regulations and practices are largely influenced by external factors. The internal structures usually resonate the rules and procedures that are perceived to be “right” within the society (Meyeret al., 1983). Therefore, the extent of information released is dependent on the rules and regulations existing in the country.

An overview of the relevant theories surrounding IFR reveals that online reporting is mainly resorted to satisfy a wide group of stakeholders in order to assist them to take potential decisions. Xiaoet al. (2004, p. 198) reports that early adoption of IFR could be due to organizational characteristics suggested by economics based theories while later stages of adoption may be due to innovation diffusion theory.

4. Literature review

The past three decades have witnessed a large amount of literature that examines voluntary corporate financial reporting and how the internet can be used as a medium for dissemination of financial information. Several international accounting regulatory bodies and researchers have studied the IFR practice in several different countries including developed as well as emerging stock markets. For instance, in 1999 the International Accounting Standards Committee (hereafter IASC) published a report that surveyed the extent and intensity of web-based financial reporting of 660 largest companies operate across multiple countries (22 countries) and regions. IASC reported

161

IFR in an

emerging

economy

that 86 percent of the companies examined had web sites. The study also found that about 62 percent (410) of the companies have disclosed some form of financial information on their web sites. Of these 410 companies, about 80 percent (327) used Hypertext Markup Language (HTML) format and only 57 percent (234) report comprehensive set of data and in HTML (see IASC, 1999, p. 51). In 2000, the Financial Accounting Standards Board (FASB) published a report related to electronic business reporting. FASB examined the attributes of the Fortune 100 companies in the USA. The study found that 99 companies had web sites. Of these, 93 companies disclose financial information on their web sites.

Ashbauphet al.(1999) examined how US firms use internet to increase timeliness of their financial reporting. They explore the contents of firms’ web pages for a sample consists of 290 firms identified by the Association of Investments Management and Research. The study found that 87 percent of the firms have a web site, out of which 30 percent did not disclose financial data or disclosed only abbreviated financial data in these web sites. Also, they found that 70 percent of the firms engage in IFR by presenting in their web sites a comprehensive set of financial statements including footnotes and auditor’s report, and or have links to their annual reports, and or have a link to the Securities Exchange Commission (SEC) and EDGER system. The main characteristics of those firms that have a web site and engage in IFR are larger in size, have higher market returns, earn higher rate of return, have higher rating score, and have larger portion of their shares held by individual investor. To know the reasons behind establishing an internet presence, Ashbauphet al.(1999) distributed a survey to the 253 firms that have web sites. The results showed that firms establish web sites for multiple reasons such as: first, to communicate with existing and potential shareholders more than non-IFR firms; second, promoting electronic commerce; third, to promote brand identifications; fourth, to engage in corporate reporting which includes financial matters; fifth, to save distribution costs; and finally, serving as an intra-company information network.

In the UK, Craven and Marston (1999) investigated the extent of voluntary disclosure of financial information on the internet for the largest 200 companies in terms of market capitalization and attempted to explain the variability in financial disclosure on the Internet. The study found that that 74 percent of the companies have web sites or homepages. From this sample, 32.5 percent disclose detailed annual report, 20.4 percent disclose part or summaries and 21.3 percent have a web site but no financial information. In addition, the hypothesis testing showed that there is a positive relationship between all size variables and the extent of financial disclosure, while there is no relationship between industry type and the extent of disclosure.

In a more recent study using UK data, Xiaoet al.(2002) explored the nature and the extent of the impact that technology and nontechnology factors will have on financial reporting on the internet through sending a questionnaire to 20 pre-selected UK experts in accounting and or the internet. The findings of Xiaoet al.’s (2002) study showed that: first, the experts support that internet is mainly a communication system as opposed to data processing system, which will widen the information provided, increase the frequency of reporting, replace the traditional report for some user, improve interactivity between company and users, make information dissemination more quick and less costly, and increase growth in nonfinancial and qualitative information; second, the experts expect many problem would be created by financial reporting includes the difficulty to regulate financial reporting, increase the nonaudit financial and nonfinancial information, and the overload of information caused by

162

JAEE

4,2

internet reporting; and third, the experts view the internet reporting future as contingent on average technological and nontechnological factors includes, the motivation for the adoption of internet reporting, the lack of regulation and standard setting, little user demand for internet reporting except as an alternative for hard copy, the nature of internet as communication system, and the problem arising from internet reporting uneven access to the internet reporting.

Using a sample of 40 Thai-listed companies, Davey and Homkajohn (2004) found that 92.5 percent of those companies have web sites, 81 percent of them report comprehensive set of financial statement on their web sites, while 13.5 percent present partial financial statements. Moreover, 30 percent of the web sites sample companies present their financial information in Portable Document File (PDF) format, while 5 percent used HTML format. In the same vine, Smith and Peppard (2005) found out that 95 percent of the 43 general public Irish corporations have web sites, 93 percent of them disclosed complete set of financial statements on their web sites, and 98 percent of the web sites companies used PDF formats.

Celik et al. (2006) studied the impact of firm’s characteristics on the web-based business reporting, the types of information disseminated, and the effect of financial or nonfinancial information disclosed by 253 firms listed on the Istanbul Stock Exchange (ISE). Celik et al. (2006) constructed a disclosure index to associate the firm’s characteristics with the disclosure behavior. They have defined 162 items in a form containing the collection of disclosure items, 87 of the items are related to the disclosure of financial information on the web. The results revealed that 87.75 percent of the 253 firms had web pages, but the level of disseminated information is relatively low. The study revealed that disclosure index formed by evaluating the web sites of the firms quoted on the ISE is examined according to two groups. The averages of total disclosure index and financial disclosure index are 0.0912 and 0.0563, respectively, which indicate that Turkish firms are considerably reluctant in disclosing information on the web. Furthermore, financial information tends to be disclosed relatively less than other types of information. The results also showed that, size, industry classification, and internationalization could explain the level of information disclosed by the firms. Other factors such as technology, risk, and profitability are important determinants for the Total Disclosure Index but not for the Financial Disclosure Index. Other variables including ownership structure, institutional investors, and intangibles did not have significant association with the web-based disclosure behavior.

In the context of Jordan, Alkhalailehet al. (2005) surveyed the extent of using internet by companies listed on the ASE. The study revealed that only 82 out of the 183-listed companies (44.8 percent) have web sites and the banking sector was the leader in having web sites and most of banks were keen to use their web sites to be both investor and customer oriented in disclosing financial information. However, most other listed companies did not disclose annual report data and were more customers oriented. Company size and the percentage of foreign investor ownership were positively associated with availability of a web site, but no evidence found to support the association between the two variables and the extent of financial disclosure on the web site.

Another study by Momany and Al-Shorman (2006) examined the status of financial reporting on the internet for 60 companies listed in the first market of ASE. The authors excluded banks from the population of their study due to the fact that all banks have web sites and comprehensive set of financial statements. The findings showed

163

IFR in an

emerging

economy

that about 45 percent of the companies listed in first market of ASE have a web site and 70 percent of these companies report financial information. Companies report financial information were classified into three categories as follows: about 31.5 percent report comprehensive set of financial statements, 15.8 percent report partial or summary financial statements, and 52.7 percent report financial highlights. Moreover, those companies presented timely information such as stock price, or historical information such as archives for previous years financial statements or sales promotions. In addition, Momany and Al-Shorman (2006) reported that, on an average, companies report financial information on their web sites are larger, have more leverage, high ownership concentration, more international investors, and are more recent than non-IFR companies. More recently, Al-Hayale (2010) examined the extent of IFR by the industrial companies listed on the ASE. He analyzed the advantages and obstacles of online disclosure from the point of view of investors and financial managers. The study reported that 55 percent of the industrial companies have web sites and only 30 percent have utilized these web sites to disseminate financial information. Al-Hayale (2010) concluded that the cost of establishing and maintaining web sites and the lack of regulations were the key factors for the infrequent use of online reporting by Jordanian companies.

In another country in the Middle East region, Mohamed and Oyelere (2008) investigated IFR practices among 49 companies listed on the Bahrain Stock Exchange. The results revealed that 79 percent of the listed companies in Bahrain (39 out of 49) have their own web sites. Furthermore, all the companies maintain web sites provide variety of information on their web sites like company information, products, financial, and other information. However, 63.3 percent of the companies with web sites provide financial information on their web sites. In total, 27 companies out of the 31 (88 percent) that provide financial information on their web sites provide both annual reports and additional financial highlights, while the other four companies provide only financial highlights. The results also showed that 87 percent of the companies (27 out of 31) provide their financial information in PDF format. Two of the remaining four companies provide both annual reports and financial highlights in HTML format; the remaining two companies used HTML to provide financial highlights only. Having briefly reviewed the relevant literature, the next section will elaborate on the data collection and the methodology used in this study.

5. Data and methodology

The aim of the study is to survey the practice of IFR among Jordanian companies listed on the ASE. The current paper surveyed all the 127 companies listed on the first market of ASE at the end of 2008[3], which are divided into three sectors, based on ASE classification, 55 companies (43.31 percent) operate in the financial sector, and 45 companies (35.43 percent) in the industrial sector, and 27 (21.26 percent) in the services sector. We adopted the methodology used by Momany and Al-Shorman (2006) and Oyelereet al.(2003) in collecting the data. Therefore, www.yahoo.com and www.google.com were used as major search engines to gather data related to Jordanian companies. Furthermore, other Jordanian electronic search engines were used like (Jordan Export Association), www.jordanexporters.org (Jordanian Export Development and Commercial Centers Corporations), www.jedeco.gov.jo (Amman Today), www.ammantoday.com, and the electronic sites of both the Jordanian Securities and Exchange Commission, www.ase.com.jo, and the Securities Depository Center, www.sdc.com.jo

164

JAEE

4,2

The first stage in collecting the data, we used the above-mentioned global and Jordanian electronic web sites to search if a company has a web site or not. Then, based on the search results companies are classified into three categories:

(1) companies that posses web sites and report financial information;

(2) companies that possess web sites but do not report financial information; and

(3) companies that do not possess web sites at all.

Next, companies that possess web sites and report financial information (e.g. balance sheet, income statement, cash flow statement, and market data) are sub classified into three groups:

(1) companies that disclose comprehensive set of financial statements;

(2) companies that disclose partial statements or summary financial statements; and

(3) companies that disclose financial highlights.

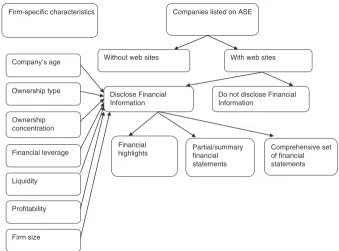

Furthermore, the current paper attempts to reveal the relevant firm-specific characteristics distinguish companies that possess web sites from those do not. The aforesaid processes can be summarized in Figure 1.

The data are analyzed using descriptive statistics, Mann-Whitney test and Kruskal-Wallis test. These tests are nonparametric alternative to the two-samplet-test. The advantage of the Mann-Whitney and Kruskal-Wallis tests is that they do not require any assumption about the shape of the distribution, i.e. normality.

With web sites

Financial highlights Company’s age

Do not disclose Financial Information

Without web sites

Partial/summary financial statements

Comprehensive set of financial statements Disclose Financial

Information Ownership type

Ownership concentration

Financial leverage

Liquidity

Profitability

Firm size

Companies listed on ASE Firm-specific characteristics

Figure 1. Summary of research methodology

165

IFR in an

emerging

economy

6. Results and discussion

This section presents the result of the study which will be classified into five subsections as follows: Jordanian companies who possess web sites; companies possess web sites and engage in IFR; type of information published on the web sites; IFR and firm-specific characteristics; and disclosure of corporate information on ASE web site vs companies’ web sites.

6.1 Jordanian companies with or without-web sites

Table I shows a classification of “with-website” and “without-website” companies listed on the ASE by industry. In total, 87 companies out of 127-listed companies (about 69 percent) have web sites and 40 out of 127 (about 31 percent) do not have web sites. The services sector has the highest proportion of corporate web sites (78 percent) followed by the financial sector (75 percent) and the industrial sector (56 percent)[4]. However, in terms of the number of companies that maintain web sites, the financial sector is leading with 41 companies followed by the industrial sector (25) and the services sector (21), respectively.

The above finding indicates significant improvement in the percentage of Jordanian companies that have web sites (69 percent) at the end of 2008 when compared with early studies conducted on Jordan. For example, in 2002 only 44.8 percent of the Jordanian companies possess web sites as found by Alkhalailehet al.(2005) with no significant increase in 2005 (45 percent) as reported by Momany and Al-Shorman (2006). In Section 3, we have established that Jordan has witnessed a significant development in ICT during the last decade which may explain the substantial growth in percentage of companies with web sites in Jordan. This result is consistent with the disclosure transformation theory which postulates that the advancement of technological factors boosts corporate IFR (see Al-Htaybat, 2011, p.18).

When compared to other regional markets, the percentage of companies with web sites reported in the current study for Jordan (69 percent) is higher than those reported, for example, for Oman (59 percent, see Mohamedet al., 2009), for Egypt (63 percent, see Alyet al., 2010), and for the United Arab Emirates (67 percent, see Kuruppu and Oyelere, 2010). It is also higher when compared with other emerging markets such as in Nigeria (54 percent, see Salawu, 2009) and in Malaysia (63 percent, see Keliwon and Mohamed, 2010). However, when compared with other developed countries like the USA, the UK, Australia, and New Zealand, the proportion of web site ownership among ASE-listed companies, is still low. This indicates that web sites ownership among companies operate in developed markets is greater than that among emerging markets (see Mohamedet al., 2009; Oyelereet al., 2003).

6.2 Companies possess web sites and engage in IFR

Table II presents the distribution of financial-information and nonfinancial-information of companies with web sites by industrial classification. It shows that 44 companies out of

Sector No. of companies With-web site % Without-web site %

Financial sector 55 41 75 14 25

Services sector 27 21 78 6 22

Industrial sector 45 25 56 20 44

Total 127 87 69 40 31

Table I.

ASE-listed companies with or without-web sites (by Industrial

Classification)

166

JAEE

4,2

87 (about 51 percent) of the ASE-listed companies have financial information on their web sites; while 43 out of 87 (about 49 percent) do not disclose financial information on their web sites. The financial sector companies got the highest proportion in presenting financial information on the web sites with 71 percent, followed by 38 and 28 percent in the services and the industrial sectors[5], respectively. The above results clearly show that the extent of disclosure on the internet among Jordanian companies is relatively weak (44 companies out of 87), which necessitate the regulatory bodies in Jordan to step forward and impose mandatory disclosures. Al-Hayale (2010) affirmed that the cost of establishing and maintaining web sites and the lack of regulations were the key factors for the infrequent use of online reporting by Jordanian companies.

This result is inconsistent with early findings of Momany and Al-Shorman (2006) which shows that 70 percent of the companies with web sites have financial information on their web sites. But, it is worth noting that the number of companies in the current study is double the number of their sample companies (19) at the time they have conducted their study.

6.3 Type of financial information published on the companies’ web sites

Table III shows the types of financial information provided on the web sites of the financial-information companies. About 73 percent (32 out of 44) of those companies provide a comprehensive set of financial statements, 16 percent (seven out of 44) provide partial or summary financial statements, while 11 percent (five out of 44) provide financial highlights, which represents the minimum level of disclosure. Table III also reveals that the financial sector has the highest proportion of corporations (79 percent) that provide a comprehensive set of financial statements, followed by the industry sector with 71 percent, and 50 percent in the services sector. Although, the majority of the financial-information companies in Jordan provide comprehensive set of financial statements (73 percent) on their web sites, there is still a room for improvement. As can be seen, the financial sector leads the other sectors in terms of online disclosure because this sector is subject to more regulations due to its nature of business which deals with large number of stakeholders. Also, the sector is more

Sector

No. of companies with-web sites

Financial

information %

Nonfinancial

information %

Financial 41 29 71 12 29

Services 21 8 38 13 62

Industrial 25 7 28 18 72

Total 87 44 51 43 49

Table II. Distribution of financial and nonfinancial information (by Industrial Classification)

Sector

No. of companies

Full comprehensive

set %

Partial or summary %

Financial highlights %

Financial 29 23 79 4 14 2 7

Services 8 4 50 2 25 2 25

Industrial 7 5 71 1 14 1 14

Total 44 32 73 7 16 5 11

Table III. Types of financial information (by Industrial Classification)

167

IFR in an

emerging

economy

open to the global financial markets and most of Jordanian banks offer online services (see Al-Htaybat, 2011).

6.4 IFR and firm-specific characteristics

In order to determine the characteristics of IFR companies, the descriptive statistics for financial-information companies, nonfinancial-information companies and all-companies, are presented in Table IV. It is worth to mention that companies without web sites and companies that have web sites but do not provide financial information on their web sites are classified in one group. We refer to this group as nonfinancial-information companies. Whereas, companies that report comprehensive set of financial statements or summary or partial financial statements or financial highlights are classified into another group. We refer to this group as financial-information companies.

Comparison between the two groups of companies reveals that financial-information companies, on an average, are larger in terms of total assets (954 vs 45 million), have more leverage, as measured by the debt ratio, (51.62 vs 30.46 percent), have less ownership concentration, as measured by the ratio of number of shares outstanding to the number of stockholders (13,734.64 vs 22,026.36), and older, as measured by company age (27.45 vs 19.70). To some extent, this finding is in line with the agency theory presented in Section 2. Generally, large companies with more leverage have higher agency problem. Therefore, these companies have more incentives to engage in online reporting to reduce information asymmetry and reduce agency problem.

Variable Statistic

Financial information companies

Nonfinancial information companies

All companies

Size (total assets) Mean 954,000,000 45,460,879.85 363,000,000 ( JD) SD 3,250,000,000 91,920,000 1,956,000,000

Median 73,427,578 18,242,891 25,158,515

Profitability (ROA) Mean 5.66 5.73 5.70

SD 5.58 7.73 7.03

Median 5.36 5.28 5.28

Leverage Mean 51.62 30.46 37.85

SD 29.68 17.87 24.75

Median 44.17 28.69 32.94

Liquidity Mean 3.95 3.01 3.34

SD 12.43 3.23 7.75

Median 1.17 1.91 1.73

Ownership

concentration Mean 13,734.64 22,026.36 19,153.64

SD 24,457.76 48,265.89 41,664.36

Median 4,492.50 3,784.00 4,086.00

% of Institutional

ownership Mean 0.05 0.03 0.04

SD 0.11 0.03 0.07

Median 0.03 0.02 0.02

% of Foreign investors Mean 0.06 0.05 0.06

SD 0.05 0.04 0.04

Median 0.06 0.05 0.05

Company age Mean 27.45 19.70 22.39

SD 17.10 11.70 14.22

Median 27 15 16

Table IV. Firm-specific characteristics and engagement in IFR (Descriptive Statistics)

168

JAEE

4,2

Other characteristics such as profitability (ROA), liquidity (current ratio), institutional ownership, and ownership of foreign investors, are almost the same among financial-information companies and nonfinancial-information companies, which indicate that those characteristics may not affect IFR for companies listed on the ASE. The evidence presented in the current study is consistent with the findings of Momany and Al-Shorman (2006) for Jordan with respect to company size, and leverage as factors that might affect IFR as a medium of voluntary disclosure. The results of this study also support their findings in relation to profitability and liquidity. However, contrary to their findings, the evidence presented in the present paper suggests that IFR companies have less ownership concentration and older than their counterparts, and there are no difference between companies in terms of both institutional ownership and the percentage of foreign investors. This could be due to the fact that Momany and Al-Shorman (2006) sample size was 60 companies while the current study surveyed 127 companies.

6.5 Disclosure of corporate information on ASE web site vs companies’ web sites

Information on companies in Jordan is available at the ASE web site and companies’ web sites. In order to see whether there are statistical differences between what is disclosed on ASE web site and on companies’ own web sites, we employed the Mann-Whitney

Utest. Table V reveals that there are statistically significant differences (p-value¼0.006) in disclosing financial and nonfinancial information between what is being disclosed on the web sites of the companies and what is being disclosed on the ASE web site. When compared with the mean rank it is clear that the disclosure of financial and nonfinancial information on ASE web site (97.87) is more than that (77.13) on the web sites of the selected companies under the study. This might be due to the fact that about 49 percent of the companies that have web sites do not provide financial information on their web sites and most of them are using it as a mean to promote the company and its products.

Table VI shows the results of Kruskal-Wallis test to determine whether there are any significant differences in the disclosure levels in the three sectors based on what is disclosed on ASE web site. The results reveal that there are no statistically significant differences (p-value¼0.579) in disclosing financial and nonfinancial information among the three sectors. This indicates that there is consistency in what is being disclosed on the web site of ASE about the companies under the study, and an effective

Disclosure of financial and nonfinancial information

No. of companies

Mean rank

Sum of ranks

Significance (p-value)

On the companies’ web sites 87 77.13 6,710 0.006

On ASE web site 87 97.87 8,515

Table V. Disclosure of corporate information on ASE web site vs companies’ web sites

Disclosure of financial and nonfinancial information No. of companies Mean rank

Significance (p-value)

Financial sector 41 45.67 0.579

Services sector 21 45.93

Industrial sector 25 39.94

Table VI. Differences in disclosure of information among the three sectors based on what is disclosed on ASE web site

169

IFR in an

emerging

economy

role of the Jordanian SEC in complying listed companies to provide a minimum level of financial and nonfinancial disclosure.

Table VII below reports the results of Mann-WhitneyUtest for the differences in disclosure between any of the three sectors within companies’ web sites and its counterpart within the ASE web site. The results indicate no significant statistical differences (p-value¼0.305) in disclosing financial and nonfinancial information between what is being disclosed on the web sites of companies in the financial sector and what is being disclosed on ASE web site for the same financial sector companies. However, the results show that there are significant statistical differences in disclosing financial and nonfinancial information between what is being disclosed on the web sites of the companies in both the services and the industrial sectors and what is being disclosed on the ASE web site for the same companies in the two sectors with 0.002 and 0.000 levels of significance, respectively. The mean rank also shows that the disclosure of the financial and nonfinancial information on ASE web site for companies in the services and industrial sectors is more than that disclosed on their web sites.

7. Summary and conclusions

Over the past ten years, the financial reporting on the internet witnessed an ever-increasing growth among companies adopted internet as a medium for voluntary disclosure. Several derivers promote companies to adopt IFR such as cost saving, disseminating information to larger number of users, and introducing new technologies for reporting. Furthermore, regulatory bodies started to issue research projects concerning this phenomenon such as, IASC (1999) and FASB (2000) and encourage companies to adopt IFR as a medium to exchange information.

This paper surveyed IFR among Jordanian companies listed on the ASE which are classified into three sectors, financial, services, and industrial. Data has been collected and analyzed on the entire 127 companies listed on the first market of ASE. In total, 87 of these companies (69 percent) were found to have web sites. Of the 87 companies maintain web sites, only 44 companies (about 51 percent) provide financial information on their web sites. Companies operate in the financial sector have the highest proportion in presenting financial information on their web sites with 71 percent, followed by 38 percent in the services sector and 28 percent industrial sector. About 73% of those companies

Disclosure of financial and

nonfinancial information No. of companies Mean rank Sum of ranks

Significance (p-value)

On the web sites of the financial sector

companies 41 44.18 1,811.50 0.305

On ASE web site for financial sector

companies 41 38.82 1,591.50

On the web sites of the services sector

companies 21 15.64 328.50 0.002

On ASE web site for the services

sector companies 21 27.36 574.50

On the web sites of the industrial

sector companies 25 18.16 454 0.000

On ASE web site for the industrial

sector companies 25 32.84 821

Table VII.

Differences in disclosure between any of the three sectors within companies’ web sites and its counterparts within ASE web site

170

JAEE

4,2

(32 out of 44) provide a comprehensive set of financial statements, 16 percent (seven out of 44) provide partial or summary financial statements, while 11 percent (5 out of 44) provide only financial highlights, which represents the minimum level of disclosure. This study also revealed that the financial sector has the highest proportion of corporations (79 percent) that provide a comprehensive set of financial statements, followed by the industry sector with 71 percent, and 50 percent in the services sector.

Based on our findings, one can conclude that there is an improvement in the percentage of Jordanian companies that have web sites and engage in IFR when compared with the results of earlier studies conducted on Jordan (see Alkhalailehet al., 2005 and Momany and Al-Shorman, 2006). This improvement has emanated from the significant development in ICT sector in Jordan during the last decade. This result is also consistent with the disclosure transformation theory which maintains that the advancement of technological factors enhances corporate IFR (Al-Htaybat, 2011). Furthermore, the IFR practices in Jordan are on the rise and currently are better than that in most of other countries in the Middle East region. However, when compared with the developed countries such the USA, UK, and Australia, IFR in Jordan is still lagging behind.

The current study also found that some firm-specific characteristics such as profitability, liquidity, institutional ownership, and ownership of foreign investors were almost the same among financial-information companies and nonfinancial-information companies, which indicate that those characteristics may not affect IFR in companies listed on the ASE. On the other hand, the results suggested that companies engaged in IFR were larger, have less ownership concentration, and older than their counterparts. By and large, these findings are consistent with the agency theory. Accordingly, companies with greater agency problem can increase the level of disclosure to reduce information asymmetry and, therefore, agency costs. However, further investigation is required to provide conclusive evidence on the determinants of IFR in Jordan.

Furthermore, the present study found that the disclosure of corporate financial and nonfinancial information on the ASE web site was more than that on the web sites of the selected companies under the study. This might be due to the fact that about 49 percent of the companies that have web sites do not provide financial information on their web sites and most of them are using it as a mean to promote the company and its products.

In this regard, ASE could monitor the compliance of disclosure by all Jordanian-listed companies which will increase the trust of information provided to different interested users as supported by Daviset al.(2003) study when they point out that communicating information on the internet will increase compliance with Regulation Fair Disclosure (“Reg FD”) – a rule that was adopted by the American SEC on August 10, 2000 – which requires companies to disclose information to the general public rather than to selected market. Additionally, ASE could modify its policies regarding disclosure by forcing listed Jordanian companies to disclose the same information contents on their web sites as it is being disclosed on ASE web site.

The results also revealed that there were no statistically significant differences in the level of disclosure of the financial and nonfinancial information among the three sectors on the ASE web site. This indicates that there is consistency in what is being disclosed on the web site of ASE about the selected companies under the study, and an effective role of the Jordanian SEC in complying listed companies to provide a minimum level of financial and nonfinancial disclosure. Finally, the results suggest that the financial sector is more advanced in terms of using IFR as compared to the industrial and services sectors. This can be attributed to the fact that financial institutions are subject to more regulations due to its nature of business which deals

171

IFR in an

emerging

economy

with large number of stakeholders. Also, the sector is more open to the global financial markets and most of Jordanian banks offer online services (see Al-Htaybat, 2011).

“The User’s Cognitive Learning Process” theory as suggested by Hodgeet al.(2002), emphasizes that the extent of information absorption is more online than from the main body of the financial statements. In this context, Jordanian companies that do not use IFR could benefit from the results of this study to disseminate their general purpose financial statements to enormous number of stakeholders at a low cost and on a timely basis which will have positive bearing effects on decision-making process by many users of financial information taken into consideration that there is rapid increase in demand for internet services in the Jordanian context. This supports the idea of information absorption as suggested by Hodgeet al.(2002). Moreover, the interaction between users and updated companies’ web sites will make it a learning process, more useful, convenient, efficient, and a fast method to collect relevant information for analysis purpose.

Although the current study has made significant contribution to the existing body of knowledge of IFR practices in an emerging economy namely Jordan, it suffers from two major limitations. First, although the present paper identified the firm-specific characteristics that may affect IFR in Jordan, it does not make serious attempt to examine those determinants using regression analysis. That would make an important future research topic. Second, the study included only companies that are listed in the first market of the ASE. Future research can include other companies listed in the second market of ASE.

Notes

1. For a good surveys of this literature see Mohamed and Oyelere (2008) and Mohamedet al. (2009). Most recently, Al-Htaybat (2011) provides a list of 37 empirical studies on IFR based on developed as well as emerging markets.

2. This section based heavily on Khan (2006).

3. There were no significant changes from 2008 to 2009 in the number of companies listed on the first market of ASE.

4. The result reported in the current study is consistent with Al-Hayale’s (2010) study who reported that 55 percent of the Jordanian industrial companies have web sites.

5. Al-Hayale (2010) showed that 30 percent of the industrial companies in Jordan use their web sites to disclose financial information which is consistent with the results presented in current paper.

References

Al-Hayale, T. (2010), “Financial reporting on the internet in the Middle East: the case of Jordanian industrial companies”, International Journal of Accounting and Finance, Vol. 2 No. 2, pp. 171-191.

Al-Htaybat, K. (2011), “Corporate online reporting in 2010: a case study in Jordan”,Journal of Financial Reporting and Accounting, Vol. 9 No. 1, pp. 5-26.

Alkhalaileh, M., Al-Qenae, R. and Abo Farha, H. (2005), “A preliminary investigation on the use of the internet for business reporting: a case study of companies listed on Amman Stock Exchange (ASE)”,Jordan Journal of Business Administration, Vol. 1 No. 1, pp. 167-176. Aly, D., Simon, J. and Hussainey, K. (2010), “Determinants of corporate internet reporting:

evidence from Egypt”,Managerial Auditing Journal, Vol. 25 No. 2, pp. 182-202.

Ashbauph, H., Johnstone, K. and Warfield, D. (1999), “Corporate reporting on the internet”, Accounting Horizons, Vol. 13 No. 3, pp. 241-257.

172

JAEE

4,2

Celik, O., Ecer, A. and Karabacak, H. (2006), “Impact of firm specific characteristics on the web based business reporting: evidence from the companies listed in Turkey”,Problems and Perspectives in Management, Vol. 4 No. 3, pp. 100-133.

Craven, B.M. and Marston, C.L. (1999), “Financial reporting on the internet by leading UK companies”,The European Accounting Review, Vol. 8 No. 2, pp. 321-333.

Davey, H. and Homkajohn, K. (2004), “Corporate internet reporting: an Asian example”,Problems and Perspectives in Management, Vol. 2 No. 2, pp. 211-227.

Davis, C.E., Clements, C. and Keuer, W.P. (2003), “Web-based reporting: a vision for the future”, Strategic Finance, Vol. 85 No. 3, pp. 45-49.

Financial Accounting Standards Board (2000), “Electronic distribution of business reporting information”, available at: www.fasb.org/brrp/brrp1.shtml (accessed June 28, 2012). Goll, I. and Zeitz, G. (1991), “Conceptualizing and measuring corporate ideology”,Organization

Studies, Vol. 12 No. 2, pp. 191-207.

Hambrick, D. and Mason, P. (1984), “Upper echelons: the organization as a reflection of its top managers”,Academy of Management Review, Vol. 9 No. 2, pp. 193-206.

Hodge, F., Kennedy, M. and Maines, L. (2002), “Recognition versus disclosure in financial statements: does search-facilitating technology improve transparency?”, working paper, University of Washington, Seattle, WA.

International Accounting Standards Committee (1999), “Business reporting on the internet”, available at: www.cs.trinity.edu/rjensen/Calgary/CD/iasb/busrepw.pdf (accessed June 28, 2012). Internet World Stats: Usage and Population Statistics (2012), available at: www.internetworldstats.

com/me/jo.htm (accessed July 6, 2012).

Keliwon, K.B. and Mohamed, Z.M. (2010), “Internet financial reporting disclosure strategy”, Proceedings of the International Conference on Business and Economic Research (ICBER), Kuching, Sarawak, March 15-16.

Khan, T. (2006), “Financial reporting disclosure on the internet: an international perspective”, unpublished doctoral thesis, Victoria University, Melbourne.

Kuruppu, N. and Oyelere, P. (2010), “Determinants of internet financial reporting in emerging economies: a study of listed companies in the United Arab Emirates”,Proceedings of the AFAANZ Annual Conference, Christchurch, July 3-6.

Lubatkin, M., Lane, P.J., Collin, S. and Very, P. (2007), “An embeddedness framing of governance and opportunism: towards a crossnationally accommodating theory of agency”,Journal of Organizational Behavior, Vol. 28 No. 1, pp. 43-58.

Massumi, B. (1987),Introduction: Rhizome. A Thousand Plateaus: Capitalism and Schizophrenia, University of Minnesota Press, Minneapolis, MN.

Meyer, J.W., Scott, W.R. and Deal, T.E. (1983), “Institutional and technical sources of organizational structure: explaining the structure of educational organizations”, in Meyer, J.W. and Scott, W.R. (Eds),Organizational Environments: Ritual and Rationality, Sage, Beverly Hills, CA, pp. 45-67. Mohamed, E. and Oyelere, P. (2008), “A Survey of internet financial reporting in Bahrain”,

Studies in Business and Economics, Vol. 14 No. 1, pp. 31-49.

Mohamed, E., Oyelere, P. and Al-Busaidi, M. (2009), “A survey of internet financial reporting in Oman”,International Journal of Emerging Markets, Vol. 4 No. 1, pp. 56-71.

Momany, M. and Al-Shorman, S. (2006), “Web-based voluntary financial reporting of Jordanian companies”,International Review of Business Research Papers, Vol. 2 No. 2, pp. 127-139. Orlowski, A. (2003), “A Quantum Theory of Internet Value”, The Register: Internet and Law, December. Oyelere, P., Laswad, F. and Fisher, R. (2003), “Determinants of internet financial reporting by New Zealand companies”,Journal of International Financial Management and Accounting, Vol. 14 No. 1, pp. 26-63.

173

IFR in an

emerging

economy

Paton, W. (1962),Accounting Theory, Scholars Book Company, New York, NY.

Pirolli, P. and Card, S. (1999), “Information foraging”,Psychological Review, Vol. 106 No. 1, pp. 643-675. Posner, R.A. (1974), “Theories of economic regulation”,Bell Journal of Economics, Vol. 5 No. 2,

pp. 335-358.

Rao, S. (2002), “Application of human- computer interaction theories to information design on internet portals”, unpublished master’s thesis, Virginia Polytechnic Institute and State University, Blacksburg, VA.

Salawu, R. (2009), “Financial reporting on the internet by quoted companies in Nigeria”, Proceedings of the 10th Annual International Conference, International Academy of African Business and Development (IAABD), Kampala, May 19-23.

Shannon, C. and Weaver, W. (1949),The Mathematical Theory of Communication, University of Illinois, Urbana-Champaign, IL.

Smith, P. and Peppard, D. (2005), “Internet financial reporting benchmarking Irish PLCs against Best Practice”,Accountancy Ireland, Vol. 37 No. 6, pp. 22-24.

Spence, A.M. (1973), “Job market signaling”,The Quarterly Journal of Economics, Vol. 87 No. 3, pp. 355-379.

Suojanen, W. (1954), “Accounting theory and the large corporation”,Accounting Review, Vol. 29 No. 3, pp. 391-398.

Verrecchia, R. (2001), “Essays on disclosure”,Journal of Accounting and Economics, Vol. 32 Nos 1-3, pp. 97-180.

World Economic Forum and INSED (2010), “Global information technology report 2009-2010”, available at: www3.weforum.org/docs/WEF_GITR_Report_2010.pdf (accessed July 7, 2012). Xiao, Z., Jones, M. and Lymer, A. (2002), “Immediate trends in internet reporting”,The European

Accounting Review, Vol. 11 No. 2, pp. 245-275.

Xiao, Z., Yang, H. and Chow, C. (2004), “Patterns and determinants of internet based corporate disclosure in China”,Journal of Accounting and Public Policy, Vol. 23 No. 3, pp. 191-225.

About the authors

Munther T. Momany is Professor of Accounting at the Faculty of Business, ALHOSN University, UAE. He received his PhD from the University of Santo Tomas Philippines. His research interests include accounting information systems, financial accounting, cost accounting, auditing and managerial accounting.

Dr Husam-Aldin N. Al-Malkawi is an Associate Professor of Finance at the Faculty of Economics and Administration, King Abdulaziz University, Saudi Arabia. He received his PhD from the University Western Sydney, Australia. He has more than 16 years teaching experience in the areas of finance, economics and statistics at various universities in Australia, Jordan, United Arab Emirates and Saudi Arabia. Dr Al-Malkawi is the author of more than 15 scholarly papers in scientific journals and serves as a Referee of several international journals. His research interests include corporate dividend policy, capital structure, financial economics, and corporate governance. Dr Husam-Aldin N. Al-Malkawi is the corresponding author and can be contacted at: [email protected]

Ebrahim A. Mahdy is a PhD candidate at the Damascus University. He received his Master Degree in Accounting from the Yarmouk University, Jordan.

To purchase reprints of this article please e-mail:[email protected]

Or visit our web site for further details:www.emeraldinsight.com/reprints

174

JAEE

4,2

This article has been cited by:

1. Mohd Noor Azli Ali KhanThe Practice of Internet Financial Reporting in Malaysia: Users’ Perceptions 687-699. [CrossRef]