i

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

Sesuai dengan tujuan pendiriannya, MAIPARK

memberikan pelayanan bagi industri asuransi

Indonesia dalam hal pengetahuan dan statistik

mengenai risiko bencana. Inovasi terus kami

lakukan untuk menyempurnakan laporan statistik

ini, sehingga menjadi lebih akurat, rinci dan

komprehensif. Berikut kami sajikan Laporan

Statistik Asuransi Gempa Bumi Indonesia per Juni

2011 yang mencakup :

o

Inovasi terhadap sistem dan proses

pengolahan data statistik.

o

Peta Kejadian Gempa Bumi Indonesia.

o

Peta

Exposure

Gempa Bumi Indonesia.

o

Penggolongan tersendiri atas risiko multi

lokasi, dalam laporan profile risiko dan

klaim.

o

Analisa asuransi gempa terkait kondisi

makro ekonomi.

o

Current Seismic Analysis

.

o

Laporan dengan dua bahasa (Bahasa

Indonesia – Bahasa Inggris).

o

Panel navigasi yang akan memudahkan

dalam menelusuri laporan statistik ini.

o

Tabel, peta dan grafik yang kreatif.

Dengan semangat ”Go Green”, laporan tersebut

disajikan dalam bentuk soft copy dan tidak lagi

diproduksi dalam bentuk hard copy.

Usaha yang kami lakukan dalam menyempurnakan

laporan statistik ini tidak akan berarti apa - apa

tanpa dukungan dari seluruh perusahaan asuransi.

Data yang lengkap dan akurat akan sangat

menentukan kualitas dari hasil statistik ini.

In line with the objective of its establishment,

MAIPARK provide services for the insurance

industry

of Indonesia in

terms

of science and statistics on disaster risk. We keep

on doing to make this statistics report to be

more accurate, detailed and comprehensive. Herew

ith we present Indonesian Earthquake of As at

June 2011 which include:

o

Innovation

of

the

system and statistical data processing.

o

Map of

Indonesian

Earthquake

Occurrence.

o

Map of Indonesian Earthquake Exposure.

o

Separate classification of multi-location

risks in and Loss report.

o

Analysis of earthquake insurance related

to macro economic conditions.

o

Current .

o

Bilingual reports (Indonesian - English).

o

Navigation Panel to ease to trace

the statistical report.

o

Creative tables, maps and graphs.

With the spirit of "Go Green” the report is

presented in soft copy rather than hard copy.

Our efforts to continously improve this statistic

report are nothing without all insurance companies’

support. Complete and accurate data will

greatly determine the quality of these statistical

results.

ii

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

Kami berharap laporan statistik ini dapat

memberikan manfaat tidak hanya bagi perusahaan

asuransi yang menangani asuransi gempa bumi,

namun juga berguna bagi industri Asuransi Umum

di Indonesia.

We hope that this statistic report is useful for

both insurance companies having earthquake

business and general insurance industry in

Indonesia.

Salam Inovasi MAIPARK !!

iii

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

Daftar Isi

Kata Pengantar

... i

Daftar Isi

... iii

Informasi Statistik

... vi

Ikhtisar Kegiatan Asuransi Gempa Bumi

Indonesia per Juni 2011

...

A. Pendahuluan ... 1

B. Struktur Pasar ... 1

C. Pertumbuhan Premi Bruto ... 2

D. Jumlah Risiko ... 5

E. Kontribusi Asuransi Gempa Bumi

Indonesia ... 8

F. Pertumbuhan Klaim Terjadi ... 15

Exposure Asuransi Gempa Bumi Indonesia

...

Tabel 2.1. Exposure Per Cresta Zone ... 21

Tabel 2.2. Exposure Per Okupasi ... 23

Tabel 2.3. Exposure Per Interest ... 25

Tabel 2.4. Exposure Per Provinsi ... 27

Gross Premium Asuransi Gempa Bumi

Indonesia

...

Tabel 3.1. Gross Premium Per Cresta Zone

... 28

Tabel 3.2. Gross Premium Per Okupasi ... 30

Tabel 3.3. Gross Premium Per Provinsi ... 32

Jumlah Risiko Asuransi Gempa Bumi Indonesia

Tabel 4.1. Jumlah Risiko Per Cresta Zone . 33

Tabel 4.2. Jumlah Risiko Per Okupasi ... 35

Klaim Asuransi Gempa Bumi Indonesia

...

Tabel 5.1. Klaim Frekwensi Per Okupasi ... 37

Tabel 5.2. Klaim Frekwensi Per Cresta Zone

... 39

Tabel 5.3. Jumlah Klaim Per Okupasi ... 41

Tabel 5.4. Jumlah Klaim Per Cresta Zone .. 43

Profil Risiko dan Klaim

...

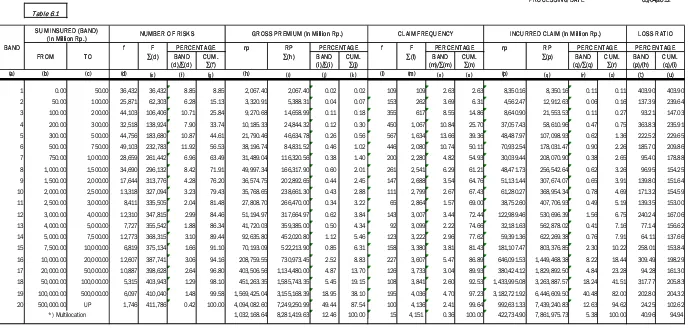

Tabel 6.1. Semua Tahun Underwriting,

Semua Okupasi, Semua Cresta Zone ... 45

Contents

Foreword ... i

Contents ... iii

Statistical Information ... vi

Summary of Indonesia Earthquake Insurance As

at June 2011 ...

Indonesia Earthquake Insurance Exposure

...

Table 2.1.Exposure By Cresta Zone

... 21

Table 2.2.Exposure By Occupation

... 23

Table 2.3.Exposure By Interest

... 25

Table 2.4.Exposure By Province

... 27

Indonesian Earthquake Insurance Gross

Premium

...

Table 3.1.Gross Premium By Cresta Zone

28

Table 3.2.Gross Premium By Occupation

.. 30

Table 3.3.Gross Premium By Province

... 32

Indonesian Earthquake Insurance Number of

Risk

...

Table 4.1.Number of Risk By Cresta Zone

33

Table 4.2.Number of Risk By Occupation

.. 35

Indonesian Earthquake Insurance Claim ...

Table 5.1. Claim Frequency By Occupation

... 37

Table 5.2. Claim Frequency By Cresta Zone

... 39

Table 5.3. Claim Amount By Occupation

... 41

Table 5.4. Claim Amount By Cresta Zone

.. 43

iv

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

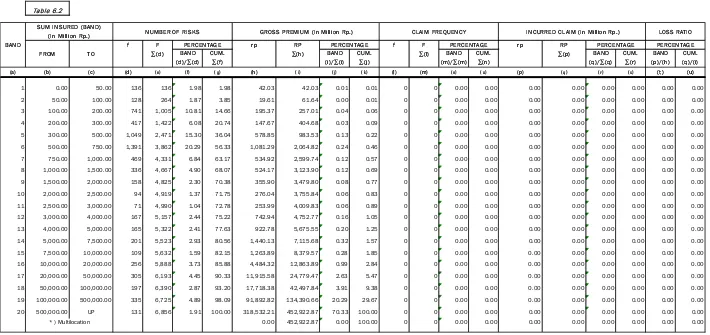

Tabel 6.2. Tahun Underwriting 2011, Semua

Okupasi, Semua Cresta Zone ... 46

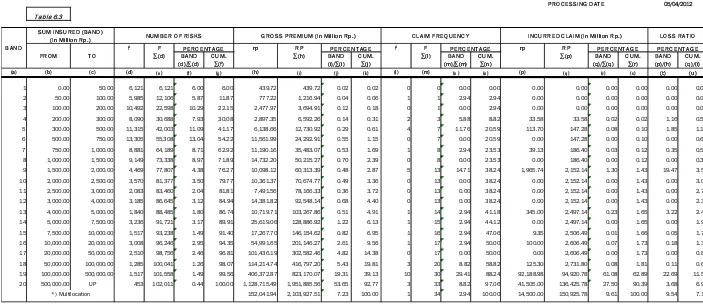

Tabel 6.3. Tahun Underwriting 2010, Semua

Okupasi, Semua Cresta Zone ... 47

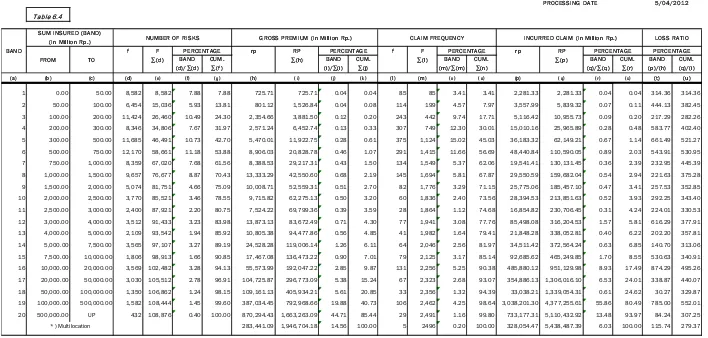

Tabel 6.4. Tahun Underwriting 2009, Semua

Okupasi, Semua Cresta Zone ... 48

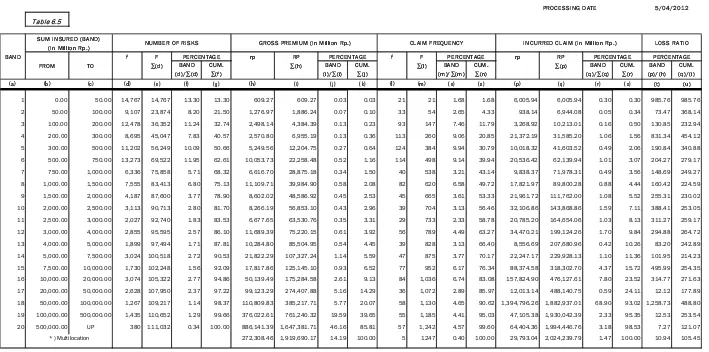

Tabel 6.5. Tahun Underwriting 2008, Semua

Okupasi, Semua Cresta Zone ... 49

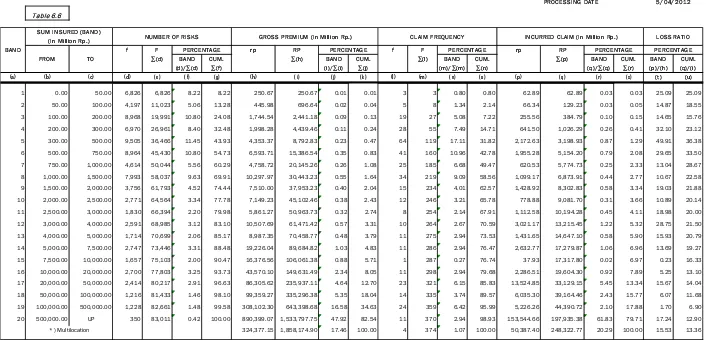

Tabel 6.6. Tahun Underwriting 2007, Semua

Okupasi, Semua Cresta Zone ... 50

Profil Risiko dan Klaim Tahun Underwriting

2011

...

Okupasi Agricultural By Cresta Zone ... 51

Okupasi Commercial By Cresta Zone ... 52

Okupasi Industrial By Cresta Zone ... 53

Okupasi Residential By Cresta Zone ... 54

Profil Risiko dan Klaim Tahun Underwriting

2010

...

Okupasi Agricultural By Cresta Zone ... 55

Okupasi Commercial By Cresta Zone ... 56

Okupasi Industrial By Cresta Zone ... 57

Okupasi Residential By Cresta Zone ... 58

Profil Risiko dan Klaim Tahun Underwriting

2009

...

Okupasi Agricultural By Cresta Zone ... 59

Okupasi Commercial By Cresta Zone ... 60

Okupasi Industrial By Cresta Zone ... 61

Okupasi Residential By Cresta Zone ... 62

Profil Risiko dan Klaim Tahun Underwriting

2008

...

Okupasi Agricultural By Cresta Zone ... 63

Okupasi Commercial By Cresta Zone ... 64

Okupasi Industrial By Cresta Zone ... 65

Okupasi Residential By Cresta Zone ... 66

Profil Risiko dan Klaim Tahun Underwriting

2007

...

Okupasi Agricultural By Cresta Zone ... 67

Okupasi Commercial By Cresta Zone ... 68

Okupasi Industrial By Cresta Zone ... 69

Okupasi Residential By Cresta Zone ... 70

Table 6.2. Underwriting Year 2011, All

Occupation, All Cresta Zone

... 46

Table 6.3. Underwriting Year 2010, All

Occupation, All Cresta Zone

... 47

Table 6.4. Underwriting Year 2009, All

Occupation, All Cresta Zone

... 48

Table 6.5. Underwriting Year 2008, All

Occupation, All Cresta Zone

... 49

Table 6.6. Underwriting Year 2007, All

Occupation, All Cresta Zone

... 50

Risk and Loss Profile Underwriting Year 2011

...

Agricultural Occupation By Cresta Zone

.. 51

Commercial Occupation By Cresta Zone

. 52

Industrial Occupation By Cresta Zone

... 53

Residential Occupation By Cresta Zone

... 54

Risk and Loss Profile Underwriting Year 2010

..

Agricultural Occupation By Cresta Zone

55

Commercial Occupation By Cresta Zone

56

Industrial Occupation By Cresta Zone

... 57

Residential Occupation By Cresta Zone

... 58

Risk and Loss Profile Underwriting Year 2009

...

Agricultural Occupation By Cresta Zone

. 59

Commercial Occupation By Cresta Zone

. 60

Industrial Occupation By Cresta Zone

... 61

Residential By Cresta Zone

... 62

Risk and Loss Profile Underwriting Year 2008

..

Agricultural Occupation By Cresta Zone

. 63

Commercial Occupation By Cresta Zone

. 64

Industrial Occupation By Cresta Zone

... 65

Residential Occupation By Cresta Zone

... 66

Risk and Loss Profile Underwriting Year 2007

..

Agricultural Occupation By Cresta Zone

67

Commercial Occupation By Cresta Zone

. 68

Industrial Occupation By Cresta Zone

... 69

v

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

Daftar Istilah ...

Lampiran

1.

Tarif Asuransi Gempa Bumi Indonesia

2.

Skala First Loss ...

3.

Tabel Jangka Waktu Pertanggungan

kurang dari satu tahun ...

4.

Tabel Indemnitas ...

Glossaries

...

Attachments

1.

Indonesian Earthquake Insurance Tariff

...

2.

First Loss Scale

...

3.

Short Period Table less than one year

period

...

vi

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

1.

Statistik dibuat berdasarkan Underwriting

Year yang tercatat sampai dengan posisi

30 Juni 2011.

2.

Sesi Limit

2.1.

Limit Sesi didasarkan atas setiap

risiko.

2.2.

Yang dimaksud dengan setiap

risiko (

anyone risk

) adalah

akumulasi (

aggregate

) jumlah

harga pertanggungan seluruh

risiko pada lokasi yang sama untuk

masing-masing perusahaan

asuransi. Definisi setiap risiko atau

setiap lokasi ditentukan oleh

perusahaan asuransi atau penerbit

polis sesuai dengan interpretasi

perusahaan asuransi dalam

underwriting

polis kebakaran.

2.3. Besarnya Limit Sesi atas setiap

risiko (

any one risk

) untuk

gabungan kerugian fisik dan

gangguan usaha adalah sebagai

berikut :

2.3.1.

Untuk daerah Jawa Barat,

Banten dan DKI : 5%

asuransi atau penerbit

polis.

2.3.2 Untuk daerah Indonesia

lainnya 25% (dua puluh

lima ratus ribu Dollar

1.

Statistics

are

prepared

on Underwriting Year basis, recorded as

at June 30 2011.

2.

Cession Limit

2.1.

Cession Limit is based on any one

risk.

2.2.

Anyone risk is the accumulation

of (aggregate) total sum insured of

all risks

at

the same

location for each insurance compan

y. The definition of anyone risk or

any location is specified by the

insurer or policy issuer in

accordance with the interpretation

of insurance companies in

underwriting fire policy.

2.3.

Cession Limit of any one risk for the

combined material and business

interruption damage are as follows:

2.3.1

For West Java, Banten and

DKI : 5% (five percent) of the

total sum insured, a maximum

of USD 2,500,000.00 (two

million five hundred thousand

U.S. Dollars) for any one risk,

each insurance company or

policy issuer

2.3.2

Other area within Indonesia

are 25% (twenty five percent)

of total sum insured,

maximum of USD

2,500,000.00 (two million five

hundred thousand U.S.

Dollars) for any one risk, each

insurance company or policy

issuer.

vii

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

Amerika) atas setiap risiko

setiap perusahaan

asuransi atau penerbit

polis.

2.4

Dalam hal penutupan secara

First

Loss Basis / Sub-limit

, jumlah yang

disesikan sebagaimana diatur

dalam butir 2.3. diatas, dikalikan

persentase

First Loss Basis /

Sub-limit Basis

.

2.5

Bilamana risiko ditutup secara

ko-asuransi, jumlah maksimum sesi

dari semua Anggota ko-asuransi

adalah sesuai dengan ketentuan

yang diatur dalam 2.3. diatas. Sesi

masing-masing perusahaan adalah

proporsional sebanding sahamnya

dalam ko-asuransi.

Dalam hal terdapat penutupan lain

selain polis ko-asuransi tersebut

ketentuan yang diatur pada butir

2.3.

3.

Tarif Premi

3.1. Penutupan dengan menggunakan

Full Value Basis mengaplikasikan

Tarif Premi Standar Gempa Bumi

Indonesia (lampiran 1)

3.2. Penutupan dengan First Loss /

Sub Limit Basis mengaplikasikan

standar First Loss Scale (lampiran

2)

3.3. Perhitungan premi untuk

penutupan kurang dari 12 (dua

belas) bulan diberlakukan skala

premi jangka pendek (lampiran 3)

3.4. Untuk perhitungan premi Business

Interruption diberlakukan Indemnity

Period Scale (lampiran 4)

2.4

In term of first loss basis / sub limit

policies, the amount cession are

stipulated in item 2.3 above, then

multiplied by the percentage of

First Loss Basis / Sub-limit Basis.

2.5

For coinsurance policies,

maximum cession from all

members of coinsurance is

stipulated in item 2.3 above. Each

ceding company cedes

proportionally depending on its

share.

In the even there are other policies

on the same risk beside that

coinsurance policy, insurer still can

cede such risks subject to the

maximum limit set out in item 2.3

3.

Premium Tariff

3.1.

For the coverage of Full Value

Basis, Indonesian earthquake rate

standard is applied (attachment 1).

3.2.

The coverage First Loss / Sub

Limit Basis uses standard First

Loss Scale (attachment 2).

3.3.

Premium calculation for short

period coverage is based on Short

Period Scale (attachment 3).

3.4.

Premium calculation for business

viii

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

4.

Obyek Pertanggungan

4.1.

Obyek pertanggungan yang dapat

disesikan adalah obyek

4.2 Penutupan sebagaimana

dimaksud pada butir 4.1. adalah

yang ditutup secara langsung

bulannya untuk semua risiko yang

ditutup pada bulan yang bersangkutan

dan sudah harus diterima

selambat-lambatnya pada akhir bulan berikutnya.

6.

Untuk kasus “Multi Location Risk” yang

mengalami kesulitan dalam memberikan

detail harga pertanggungan perlokasi

maka dengan persetujuan AAUI

pensesian risiko dan perhitungan premi

dilakukan pada zona-zona tertentu.

7.

Untuk menggambarkan premi dan harga

pertanggungan yang sebenarnya dalam

penutupan asuransi gempa bumi

berdasarkan ko-asuransi, diharapkan

agar seluruh anggota ko-asuransi

mensesikan risiko gempa bumi tersebut.

4.

Insured Objects

4.1.

Insured objects that can be ceded

are insured objects in fire policy.

such as :

4.1.1.

Material damage :

•

Buildings

•

Foundations

•

Excavation and the like

•

Stocks

4.2.

Insured objects referred in item 4.1

are objects from direct business

insurance, including coinsurance.

Indirect businesses cannot be

ceded.

5.

Bordereaux Report.

Bordereaux reports is submitted on a

monthly basis for all risk underwritten in

the month concerned and should be

received by the end of the following

month.

6.

In the case of Multi Location Risks with

no details of sum insured provided per

location, the risk cession and its premium

calculation specified zones after

approved by AAUI.

7.

In order to get overall pictures of each

1

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

A.

Pendahuluan.

Berdasarkan laporan Badan Pusat Statistik

tentang Pertumbuhan Ekonomi Indonesia

Triwulan II-2011, pertumbuhan ekonomi

Indonesia yang diukur berdasarkan kenaikan

Pendapatan Domestik Bruto (PDB) pada

semester I-2011 meningkat 6,5% dibandingkan

semester I-2010. Besaran PDB atas dasar

harga berlaku pada triwulan II-2011 mencapai

Rp. 1.811,1 Triliun. Ada tiga sektor yang

mendominasi tingkat pertumbuhan tertinggi

(perbandingan triwulanan dari tahun lalu) yaitu

sektor Perdagangan, Hotel dan Restoran

sebesar 4,8 %, Sektor Konstruksi sebesar 4,2

% dan Sektor Listrik, Gas dan Air Bersih

sebesar 4,0%. Tampak bahwa sektor yang

menduduki 2 (dua) peringkat teratas

mencerminkan pertumbuhan di Sektor Riil

secara keseluruhan, yang tentunya diharapkan

akan berdampak positif terhadap pertumbuhan

di bidang asuransi.

B. Struktur Pasar

Berdasarkan data yang berhasil kami

kumpulkan Per 30 Juni 2011, terdapat 84

perusahaan asuransi umum dan perusahaan

reasuransi umum yang memiliki izin beroperasi

di Indonesia. Dari 84 perusahaan tersebut, 18

perusahaan adalah perusahaan asuransi

patungan, 4 perusahaan adalah perusahaan

A.

Introduction

Based on the quarter II- 2011’s report on

Indonesian economic growth issued by Statistic

Central Agency, Indonesia’s economic growth

being measured by the increase of GDP at

semester I-2011 have increased by 6.5%

compared to the same period last year. The

GDP amount based on the current prices

reached Rp. 1,811.1 trillions. There are three

sectors dominating the highest increment

(quarter-to-quarter), i.e. Trade, Hotel and

Restaurant Sector at 4.8%. It is followed by

Construction sector at 4.2% and the last

Electricity, Gas and Water sector at 4.0%.

Especially for the first two highest sectors, it

may reflect the growth of Real Sector overall. It

is hoped that this will give positive impacts

towards the growth on insurance sector.

B. Market Structure

Based on the current that we collected per

30 June 2011, there are 84 general insurers

and general reinsurers in Indonesia having

operating licenses in Indonesia. Out of those 84

companies, 18 are joint-venture insurance

2

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

reasuransi dan 62 sisanya merupakan

perusahaan asuransi swasta nasional.

Sebagai perusahaan asuransi umum

satu-satunya di Indonesia yang mengkhususkan diri

pada risiko-risiko khusus seperti gempa bumi,

MAIPARK terus menerus melakukan perbaikan

dan pengembangan seperti dalam sistem

pengolahan data dan pembuatan laporan

statistik yang terdiri dari pensesian wajib dan

pensesian tidak wajib. Diharapkan dengan

semakin meningkatnya kualitas laporan statistik

maka industri asuransi dapat menarik manfaat

akan keberadaan MAIPARK melalui

output

yang dihasilkan, seperti laporan geologi terkait

usaha asuransi, suku premi asuransi gempa

bumi maupun laporan statistik ini sendiri.

C. Pertumbuhan Premi Bruto

Per 30 Juni 2011, pendapatan premi bruto

untuk tahun underwriting 2007 adalah sebesar

Rp. 1.858,2 miliar. Premi bruto untuk tahun

underwriting 2008 tercatat Rp 1.919,7 miliar,

sedangkan untuk tahun underwriting 2009

adalah Rp. 1.946,7 miliar. Dan untuk tahun

underwriting 2010 dan 2011 pendapatan

asuransi gempa bumi adalah Rp. 2.103,9 miliar

dan Rp. 452,9 miliar. Dikarenakan pencatatan

ini dilakukan pada pertengahan tahun maka

angka-angka yang tersaji di atas masih kecil,

terutama untuk tahun underwriting yang masih

muda seperti tahun underwriting 2010 dan

tahun underwriting 2011. Namun demikian,

companies and the remaining 62 are national

private insurance companies.

As the only one general insurance focusing

on special risks such as earthquake, MAIPARK

keeps on developing and enhancing the

existing system, including the process of

making statistic report comprising of

compulsory and non-compulsory cessions. It is

hoped that the development on the quality of

statistic report, the industry could take benefits

from the existence of MAIPARK through its

outputs, ranging from geological reports related

to insurance business, earthquake insurance

rates and also the statistic report itself.

C. Gross Premium Growth

Per 30 June 2011, the gross premium

income of underwriting year 2007 was Rp.

1,858.2 billion. At the same period in the first

semester 2011, the gross premium income for

underwriting year 2008 was Rp 1,919.7 billion.

For underwriting year 2009, it was Rp 1,946.7

billion. Finally, for underwriting year 2010 and

2011, they are Rp. 2,103.9 billion and Rp.

452.9 billion. Since these have not developed

yet in the first year, those figures were still little,

and would certainly increase until the end of

2011, especially for the figures of underwriting

3

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

angka tersebut dipastikan bergerak naik hingga

pencatatan di akhir tahun 2011.

Dari catatan statistik selama tahun

underwriting 2007 – tahun underwriting 2011,

okupasi industrial selalu memiliki rasio

pendapatan premi bruto terbesar dibanding 3

(tiga) okupasi lainnya, yaitu selalu di atas 55%.

Kemudian diikuti oleh okupasi komersial,

okupasi residensial dan okupasi agrikultural.

Hal ini logis dilihat dari perkembangan

bisnis keempat okupasi tersebut. Okupasi

Industrial yang didominasi oleh pabrik,

manufaktur dan sejenisnya memiliki nilai

pertanggungan yang pada umumnya besar

sehingga pendapatan premi yang diperoleh

juga besar. Sebagai contoh adalah pada tahun

underwriting 2007, Unit Pengolahan IV Cilacap

Pertamina sebagai pemasok 34% kebutuhan

BBM nasional atau 60% kebutuhan BBM di

pulau Jawa, memiliki pertanggungan tertinggi

yaitu sebesar Rp. 46,4 Triliun. Mengingat

laporan statistik ini memuat informasi selama 5

tahun terakhir (UY 2007 – UY 2011), maka

data tersebut masih tercatat dalam laporan.

Okupasi komersial yang didominasi gedung

bertingkat, gedung perkantoran, ruko (rumah

toko) dan rukan (rumah kantor) walaupun

memiliki tarip premi yang sama dengan okupasi

industrial, namun memiliki nilai pertanggungan

yang relatif kecil dibanding okupasi industrial

sehingga total premi yang diperoleh pun lebih

kecil dari okupasi lndustrial.

On our statistic report from underwriting year

2007 to underwriting year 2011, Industrial

occupation is always the biggest contribution

comparing to the remaining three occupations.

It always has percentage higher than 55%.

Then, it is followed by commercial occupation,

residential occupation and agricultural

occupation.

Having seen the development of those four

occupations, this is logical. Industrial

occupation which is dominated by business

such as factories, manufacturers etc usually

have big sum insured resulting big premium.

For example, in Underwriting Year 2007,

Refinery Unit IV Cilacap Pertamina as the main

provider of 34% Fuel Oil for national needs or

60% Fuel Oil in Java Island has the biggest

sum insured at Rp

.

46.4 trillion. Since this

statistic report contains the latest 5 year

information (UY 2007 – UY 2011), therefore

such data still appears in this report.

Commercial occupation being dominated

by high-rise buildings, office buildings,

shop-houses and office-shop-houses, having the same

premium rate with industrial occupation, have

relatively smaller sum insured compared to

industrial occupation. In total, the premium will

consequently be smaller than industrial

4

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

Meskipun okupasi residensial dan okupasi

agrikultur tidak memberikan kontribusi sebesar

okupasi industrial dan okupasi komersial

namun kedua okupasi tersebut mengalami

pertumbuhan premi bruto yang cukup tinggi.

Dengan mengasumsikan tidak ada

pertumbuhan premi yang berarti pada tahun

underwriting 2007 dan 2008 maka dapat

dikatakan premi bruto okupasi residensial pada

tahun underwriting 2008 meningkat sebesar

40,7% dibanding tahun sebelumnya dan premi

bruto okupasi agrikultur pada tahun

underwriting 2008 meningkat sebesar 74,3%

dari tahun sebelumnya

.

Tabel 1.1 di bawah ini menyajikan rincian

premi bruto berdasarkan jenis okupasi dari

tahun underwriting 2007 sampai semester

pertama tahun underwriting 2011.

Although residential occupation and agricultural

occupation do not give premium contribution as

much as industrial occupation and commercial

occupation, they have enough premium

increase growth. By assuming there are no

meaningful premium increase growth on

underwriting year 2007 and underwriting year

2008, we can say the gross premium of

residential occupation in underwriting year

2008 increased 40.7% comparing to the same

period last year. Also, the gross premium of

agricultural occupation in underwriting year

2008 increase 74.3% from last year.

The table 1.1 below presents the details of

gross premium based on the occupation type

from underwriting year 2007 to the first

semester underwriting year 2011.

Tabel 1.1. Tabel premi bruto masing-masing okupasi pada tahun underwriting 2007 – 2011 per 30 Juni 2011

Table 1.1. Table of gross premium of each occupation underwriting year 2007 – 2011 as at 30 June 2011

Per / As at 30 June 2011 Dalam Jutaan Rupiah

In Million Rupiah

Tahun

Underwriting

2007

9,949.0

0.54%

394,454.9

21.22% 1,300,315.7

69.98%

153,455.3

8.26% 1,858,174.9

2008

17,346.4

0.90%

456,031.0

23.76% 1,230,379.6

64.09%

215,933.2

11.25% 1,919,690.2

2009

16,613.9

0.85%

456,221.1

23.44% 1,195,083.2

61.39%

278,786.0

14.32% 1,946,704.2

2010

20,851.8

0.99%

373,764.3

17.77% 1,432,168.0

68.07%

277,143.4

13.17% 2,103,927.5

2011

1,943.9

0.44%

68,591.3

15.14%

258,501.1

57.07%

123,886.5

27.35%

452,922.9

Premi Bruto dan Rasio Berdasarkan Okupasi

Gross Premium and Ratio By Occupation

Okupasi

5

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

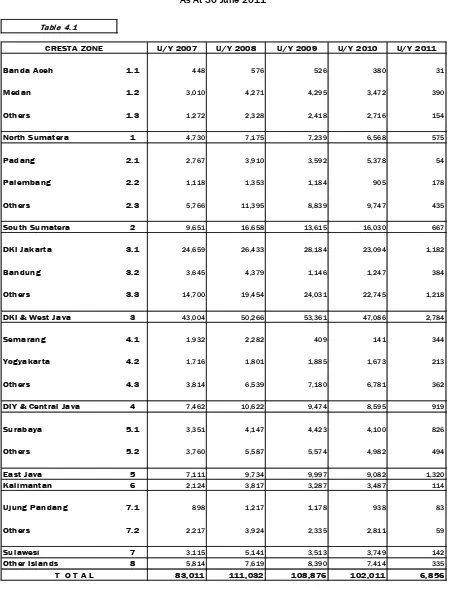

D. Jumlah Risiko

Tabel 1.2 dibawah ini menyajikan jumlah

risiko pada masing-masing tahun underwriting

yang tercatat sampai dengan 30 Juni tahun

2011, yaitu dari tahun underwriting 2007 hingga

tahun underwriting 2011. Tabel ini tidak

termasuk risiko multilokasi dimana kami

mengelompokkannya dalam satu kelompok

khusus dikarenakan kurang rincinya data yang

kami terima sehingga kurang tepat jika kami

memasukkan risiko yang tidak terindentifkasi

tersebut ke dalam jenis okupasi tertentu.

Kenyataan ini juga memberi pesan kepada

industri asuransi kerugian untuk mensesikan

data-data tersebut secara lebih akurat dan

lengkap untuk menyempurnakan laporan

statistik kami.

D. Number of Risk

Table 1.2 below shows number of risks on

each underwriting year recorded until 30 June

2011, ranging from underwriting year 2007 to

underwriting year 2011. This table does not

include multi-location risks - a special group

comprising of the inaccurate risk details. Due

to inaccurate risks details, it is not correct to put

this multi-location group into one of those four

occupation categories. This fact gives a

message to general insurance industry to cede

the earthquake cession more complete and

more accurate to make this statistic report more

perfect.

.

Tabel 1.2. Jumlah risiko masing-masing okupasi pada tahun underwriting 2007 - 2011 per 30 Juni 2011

Table 1.2. Number of risk of each occupation underwriting year 2007 – 2011 as at 30 June 2011

Chart 1.1. Diagram batang menunjukan jumlah risiko tiap okupasi pada tahun underwriting 2007 - 2011 per 30 Juni 2011

Chart 1.1. Bar chart showing number of risk each occupation underwriting year 2007 – 2011 as at 30 June 2011

Per / As at 30 June 2011

Agricultural 412 0.50% 599 0.54% 348 0.32% 265 0.26% 64 0.93%

Commercial 39,310 47.36% 64,507 58.10% 55,866 51.31% 47,881 46.94% 5,083 74.14%

Industrial 11,704 14.10% 9,682 8.72% 11,526 10.59% 10,553 10.34% 933 13.61%

Residential 31,585 38.05% 36,244 32.64% 41,136 37.78% 43,312 42.46% 776 11.32%

TOTAL 83,011 111,032 108,876 102,011 6,856

Jumlah Risiko Berdasarkan Okupasi Number of Risk By Occupation

Okupasi Tahun Underwriting / Underwriting Year

6

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

Berbeda dengan kontribusi premi bruto

terbesar yang ada pada okupasi industrial,

maka jumlah risiko terbesar untuk setiap tahun

underwriting, dalam hal ini dari tahun

underwriting 2007 sampai tahun underwriting

2011, ada pada okupasi komersial. Kemudian

diikuti oleh okupasi residensial, okupasi

industrial dan terakhir okupasi agrikultural.

Besarnya jumlah risiko pada okupasi

komersial adalah selain banyaknya gedung

bertingkat tinggi, bank dan perusahaan yang

memiliki cabang di beberapa wilayah Indonesia

juga karena rumah toko (

shop houses

) masuk

dalam kategori okupasi komersial. Rumah toko

memiliki kisaran nilai pertanggungan sekitar

Rp. 500 juta hingga Rp. 1 mililar atau lebih.

Dari segi nilai pertanggungan, rumah toko tidak

berbeda jauh dengan nilai pertanggungan pada

rumah biasa, namun dari segi kuantitas

banyaknya rumah toko (

shop houses

) secara

langsung menyumbang kontribusi jumlah risiko

yang besar pada okupasi komersial. Begitupun

pada okupasi residensial, jumlah risiko yang

tercatat cukup besar namun masih dibawah

jumlah risiko komersial. Sementara itu, okupasi

industrial sebagai penyumbang kontribusi

premi bruto tertinggi hanya menempati urutan

ketiga dalam jumlah risiko. Hal ini dikarenakan

lokasi dari okupasi industrial yang hanya

berada pada titik-titik tertentu dan tidak

tersebar di berbagai wilayah Indonesia,

contohnya, Unit Pengolahan Pertamina.

Terakhir, okupasi agrikultural memiliki jumlah

risiko yang paling rendah dibandingkan okupasi

Different from industrial occupation that has

given biggest premium contribution so far, the

commercial occupation contributes the highest

number of risks from underwriting year 2007 to

underwriting year 2011. Then, it is followed with

residential occupation, industrial occupation

and the last agricultural occupation.

In addition to the high number of high-rise

buildings, banks and companies having

branches in other area in Indonesia, the

shop-houses also contribute to the number of risks

on commercial occupation. Shop-houses have

sum insured range from Rp 500 million to Rp 1

trillion or more. From the sum insured side,

shop-houses are not far much different than

ordinary dwelling-houses. However; from the

quantity side, the large quantity of shop-houses

directly contribute to the number of commercial

occupation. Also, the residential occupation has

large number of risks but still below the number

of risks of commercial occupation. Meanwhile,

industrial occupation as the biggest premium

contributor only ranks third in terms of number

of risks. The reason is the industrial occupation

only locates on specific locations and not

located widespread all over Indonesia such as

Refinery Unit Pertamina. Lastly, agricultural

occupation has the least number of risks

compared to other occupations because

agricultural occupation is rarely insured with

7

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

lainnya karena sedikitnya okupasi ini yang

memiliki penutupan asuransi gempa bumi.

Sebagai sentuhan terakhir analisa pada

jumlah risiko, idealnya jumlah risiko terbesar

ada pada okupasi residensial yang diwakili

rumah tinggal. Namun kenyataannya okupasi

ini menempati peringkat kedua. Hal ini

diakibatkan selain sedikitnya rumah tinggal

yang memiliki asuransi gempa bumi, juga

jikapun terdapat rumah yang memiliki

asuransi gempa bumi, maka pertanggungan

gempa bumi tersebut berada pada paket

asuransi rumah tinggal (

house owners

insurance package

) yang tidak dimasukkan

dalam risiko asuransi gempa bumi yang

disesikan ke MAIPARK.

As the final touch on the analyze of number

of risks, ideally the number of risk lies on

residential occupation being represented by

dwelling houses. On the contrary, this

occupation ranks number two. The possible

reasons are there are little number of dwelling

houses having earthquake risks covers and if

they have, they have homeowners’ insurance

package which are not included in earthquake

8

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

E. Kontribusi Asuransi Gempa Bumi

Berdasarkan data dari Badan Pusat

Statistik dan Biro Perasuransian Indonesia

Bapepam LK tahun 2010, pertumbuhan

ekonomi Indonesia juga tercermin dalam

pertumbuhan industri asuransi, baik itu

asuransi jiwa maupun asuransi kerugian.

Dalam laporan yang dikeluarkan oleh Biro

Perasuransian Indonesia - Bapepam LK, yaitu

dalam buku Perasuransian Indonesia 2010,

tercatat penerimaan premi bruto asuransi di

tahun 2010 meningkat sebesar 17,5 % dari

tahun sebelumnya, yaitu dari Rp 106,4 triliun

menjadi Rp.125,1 triliun. Sedangkan

insurance

density

tahun 2010 tercatat sebesar

Rp.526.584 untuk jumlah penduduk Indonesia

sebanyak 237,6 juta jiwa di tahun 2010. Ini

berarti rata-rata penduduk Indonesia

menghabiskan Rp. 526.584 untuk membayar

premi asuransi. Sedangkan kontribusi premi

bruto sektor asuransi terhadap Produk

Domestik Bruto sebesar 1,95% pada tahun

yang sama. Hal ini berarti terjadi peningkatan

dari rasio tahun sebelumnya, yaitu sebesar

1,90%. Tabel 1.3 dibawah ini menjelaskan hal

tersebut dari tahun 2006 hingga tahun 2010.

.

E. Earthquake Insurance Contribution

Based on the data from Central Agency Of

Statistic and Indonesian Insurance Bureau –

Capital Market Investment Agency year 2010,

Indonesian economic development is reflected

on the insurance industry growth, either life

insurance or general insurance.

In the Insurance Directory 2010 report

issued by Indonesian Insurance Bureau of

Capital Market Investment Agency, the gross

premium income of 2010 increased 17.5 %

from Rp. 106.4 trillions to become Rp. 125.1

trillions. The insurance density in 2010

recorded Rp. 526,584 for Indonesia population

that reached 237.6 millions people. It also

means, each Indonesian resident spent Rp.

526,584 to buy insurance product. On the other

hand, gross premium income contribution

toward Gross Premium Products reached

1.95% in the same year. This ratio increases

from the last year’s ratio at 1.90%. Table 1.3

below shows such increment from year 2006 to

9

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

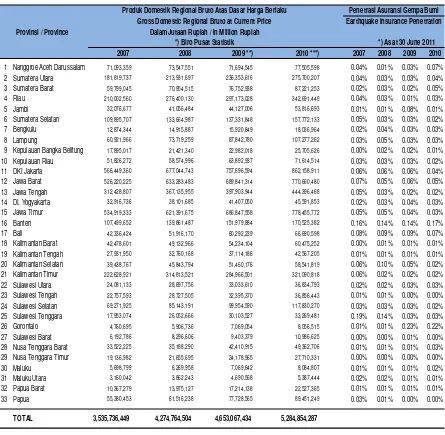

Dengan memperhatikan penyebaran

asuransi gempa bumi berdasarkan provinsi

maka selama tahun underwriting 2007 – tahun

underwriting 2010, rata-rata rasio premi bruto

tertinggi berada pada provinsi DKI Jakarta

(20,75%), Jawa Barat (18,93%), Jawa Timur

(14,35%) dan Banten (11,03%). DKI Jakarta

memiliki kontribusi premi asuransi gempa bumi

tertinggi selama tahun underwriting tersebut

karena selain sebagai pusat pemerintahan dan

pusat bisnis yang bernilai ekonomi tinggi,

masyarakat yang tinggal di ibukota negara

Indonesia ini relatif lebih memiliki kemampuan

finansial serta edukasi yang cukup baik tentang

asuransi.

Namun demikian jika dilihat dari kontribusi

asuransi gempa bumi terhadap pendapatan

domestik regional bruto atau penetrasi asuransi

per provinsi ternyata rata-rata rasio penetrasi

asuransi gempa bumi tertinggi selama tahun

By looking at the spread of earthquake

insurance by province during underwriting year

2007 – underwriting year 2010, the highest

average growth on gross premium is in DKI

Jakarta (20.75%), Jawa Barat (18.93%), Jawa

Timur (14.35%) dan Banten (11.03%). DKI

Jakarta gives the highest earthquake premium

contribution during those underwriting years

since DKI Jakarta is the capital city and the

central business having the highest economic

values. The people living in this capital city

relatively have good financial and insurance

educational background.

However, if we look at the earthquake

insurance premium contribution towards

regional GDP or insurance penetration per

province, the highest earthquake insurance

penetration ratio during underwriting year 2007

– underwriting year 2010 is in Banten Province

Tabel 1.3 Tabel Premi Bruto dan Produk Domestik Bruto 2006 - 2010Table 1.3 Gross Premiums and Gross Domestic Products 2006 – 2010 Table

Dalam Milyar Rupiah

1) Premi Bruto (termasuk Premi Program Jaminan Hari Tua (JHT)) = Premi Pos Langsung + Premi Reasuransi diterima dari Luar Negeri

Gross Premium (include Premium of Pension Benefits (JHT)) = Direct Premium + Reinsurance Premium Inward from Abroad

2) Sumber : Biro Pusat Statistik (BPS) berdasarkan Harga yang Berlaku

Source : Central Of Statistic Bureau (BPS) using Current Market Prices

10

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

underwiting 2007 – tahun underwriting 2010

terletak pada provinsi Banten yaitu sebesar

0,15% kemudian diikuti oleh Gorontalo sebesar

0,12%, Provinsi DKI Jakarta sebesar 0,06%

dan Provinsi Jawa Barat sebesar 0,06%.

Alasan mengapa penetrasi asuransi gempa

bumi tertinggi ada pada Provinsi Banten karena

selain memiliki rata-rata rasio premi bruto yang

cukup tinggi yaitu 11,03% , produk domestik

regional bruto Provinsi Banten relatif lebih kecil

dibandingkan DKI Jakarta dan Jawa Barat.

Industri baja, listrik, kimia dan pupuk

memberikan kontribusi terhadap pendapatan

premi bruto di provinsi ini. Yang cukup menarik

adalah provinsi Gorontalo sebagai peringkat

tertinggi kedua rata-rata rasio penetrasi

asuransi gempa bumi. Walaupun secara

rata-rata rasio premi bruto masih kecil, namun

jumlah premi bruto Provinsi Gorontalo di tahun

2009 mencapai Rp. 16.025,2 juta meningkat

2.649 % dari tahun sebelumnya Rp. 582,9 juta.

Begitupun di tahun 2010, premi bruto di

Provinsi ini tercatat sebesar Rp. 17.409,67 juta.

Kehadiran sektor perkebunan dan pupuk

memberikan kontribusi yang sangat besar

terhadap pendapatan premi bruto asuransi

gempa bumi pada provinsi ini. Selain itu,

produk domestik regional bruto Provinsi

Gorontalo relatif lebih kecil dibandingkan DKI

Jakarta serta Jawa Barat, sehingga penetrasi

asuransi gempa bumi provinsi ini menjadi

tinggi.

at 0.15% then Gorontalo Province at 0.12%,

DKI Province at 0.06% and West Java Province

at 0.06%.

The reason why the highest earthquake

insurance penetration ratio lies on Banten

Province is because Banten Province has an

average significant gross premium growth ratio

at 11.03% and the regional GDP of Banten is

relatively small compared to DKI Jakarta and

West Java. Steel manufacturer, Electricity,

Chemistry and Fertilizer gives contribution

towards gross premium income for this

province. The most interesting thing is

Gorontalo province ranks the second highest

earthquake insurance gross premium.

Although the average gross premium ratio is

still small, the gross premium income of

Gorontalo Province reached Rp. 16,025.2

million in 2009. It increased 2,649% from the

previous year at Rp. 582.9 million. In 2010, the

gross premium of this province recorded Rp

17,409.67 million. The existence of plantation

sector and fertilizer gives significant

contribution towards gross premium income for

this province. Moreover, the GDP of Gorontalo

is relatively small comparing to DKI Jakarta and

West Java and it makes the insurance

penetration ratio for this province becomes

11

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

Sebagai catatan, sesuai dengan yang

dilaporkan Badan Pusat Statistik (BPS) maka

tabel Produk Domestik Regional Bruto yang

ditampilkan hanya sampai tahun 2010,

sehingga pembahasan dan analisa untuk

penetrasi asuransi gempa bumi tahun 2011

akan dilakukan pada laporan semester

berikutnya.

Tabel 1.4 dibawah ini menyajikan

kontribusi pendapatan premi asuransi gempa

bumi yang dibagi berdasarkan provinsi, catatan

per tanggal 30 Juni 2011.

As a supplementary note, the GDP

Regional shown is only for the period until 2010

as being reported by Statistic Central Agency.

Therefore the presentation and analyze for

earthquake insurance penetration for 2011 will

be presented in the report next semester.

This following table 1.4 shows earthquake

insurance contribution by province, as at June

30, 2011.

Tabel 1.4 Premi Bruto Asuransi Gempa Bumi Berdasarkan Provinsi 2007 – 2011 Table 1.4 Earthquake Gross Premiums by Province 2007 - 2011

Dalam Jutaan Rupiah In Million Rupiah

2007 % 2008 % 2009 % 2010 % 2011 %

1. Nanggroe Aceh Darussalam 28,766.10 1.5% 6,056.94 0.3% 18,823.43 1.0% 56,476.14 2.7% 57.54 0.0%

2. Sumatera Utara 67,024.43 3.6% 62,159.08 3.2% 79,619.17 4.1% 117,390.13 5.6% 22,169.14 4.9%

3. Sumatera Barat 10,460.74 0.6% 20,362.62 1.1% 17,576.09 0.9% 41,270.02 2.0% 6,231.51 1.4%

4. Riau 73,686.77 4.0% 94,150.39 4.9% 44,559.52 2.3% 94,625.28 4.5% 6,612.75 1.5%

5. Jambi 4,161.64 0.2% 5,079.95 0.3% 33,240.67 1.7% 3,987.52 0.2% 253.06 0.1%

6. Sumatera Selatan 51,863.11 2.8% 34,390.65 1.8% 37,785.54 1.9% 31,430.67 1.5% 3,449.55 0.8%

7. Bengkulu 2,371.38 0.1% 6,065.30 0.3% 5,566.64 0.3% 5,524.20 0.3% 808.52 0.2%

8. Lampung 20,307.59 1.1% 35,398.58 1.8% 30,693.42 1.6% 30,699.54 1.5% 9,203.48 2.0%

9. Kepulauan Bangka Belitung 473.82 0.0% 3,308.46 0.2% 4,248.69 0.2% 3,203.27 0.2% 224.64 0.0%

10. Kepulauan Riau 16,466.74 0.9% 17,790.88 0.9% 17,165.29 0.9% 16,270.10 0.8% 3,383.94 0.7%

11. DKI Jakarta 366,667.61 19.7% 422,229.71 22.0% 446,256.16 22.9% 386,149.84 18.4% 110,453.44 24.4%

12. Jawa Barat 342,953.86 18.5% 335,091.75 17.5% 385,968.35 19.8% 418,980.57 19.9% 78,725.68 17.4%

13. Jawa Tengah 146,422.95 7.9% 127,092.83 6.6% 94,932.96 4.9% 107,000.11 5.1% 13,473.78 3.0%

14. DI. Yogyakarta 6,742.19 0.4% 12,570.39 0.7% 15,006.08 0.8% 15,166.51 0.7% 8,912.75 2.0%

15. Jawa Timur 260,796.85 14.0% 304,918.63 15.9% 284,784.55 14.6% 270,954.83 12.9% 74,078.14 16.4%

16. Banten 173,734.44 9.3% 193,894.47 10.1% 215,414.22 11.1% 286,165.13 13.6% 61,656.54 13.6%

17. Bali 33,147.17 1.8% 47,348.44 2.5% 53,148.99 2.7% 49,406.59 2.3% 10,008.56 2.2%

18. Kalimantan Barat 1,812.98 0.1% 3,243.69 0.2% 4,204.39 0.2% 3,403.95 0.2% 311.06 0.1%

19. Kalimantan Tengah 2,776.69 0.1% 3,603.39 0.2% 5,420.12 0.3% 4,796.22 0.2% 2,550.85 0.6%

20. Kalimantan Selatan 25,172.71 1.4% 45,826.94 2.4% 24,331.56 1.2% 11,580.16 0.6% 4,103.62 0.9%

21. Kalimantan Timur 134,804.71 7.3% 57,297.32 3.0% 53,905.95 2.8% 69,792.99 3.3% 6,187.39 1.4%

22. Sulawesi Utara 5,212.40 0.3% 5,963.57 0.3% 10,929.62 0.6% 10,691.00 0.5% 3,831.76 0.8%

23. Sulawesi Tengah 1,572.83 0.1% 1,838.98 0.1% 1,536.27 0.1% 1,619.98 0.1% 50.96 0.0%

24. Sulawesi Selatan 23,375.82 1.3% 24,170.27 1.3% 25,690.99 1.3% 17,730.37 0.8% 2,286.95 0.5%

25. Sulawesi Tenggara 34,445.67 1.9% 36,382.59 1.9% 8,814.04 0.5% 9,645.87 0.5% 18.98 0.0%

26. Gorontalo 574.73 0.0% 582.96 0.0% 16,025.17 0.8% 17,409.67 0.8% 23,065.15 5.1%

27. Sulawesi Barat 86.01 0.0% 117.89 0.0% 651.12 0.0% 507.72 0.0% 0.00 0.0%

28. Nusa Tenggara Barat 3,813.83 0.2% 2,905.63 0.2% 2,712.02 0.1% 13,726.21 0.7% 310.01 0.1%

29. Nusa Tenggara Timur 530.99 0.0% 738.08 0.0% 899.32 0.0% 1,146.29 0.1% 170.03 0.0%

30. Maluku 534.01 0.0% 513.23 0.0% 877.95 0.0% 1,562.24 0.1% 166.12 0.0%

31. Maluku Utara 706.34 0.0% 733.66 0.0% 579.35 0.0% 529.01 0.0% 3.83 0.0%

32. Papua Barat 1,168.85 0.1% 1,387.40 0.1% 1,615.79 0.1% 1,844.02 0.1% 4.84 0.0%

33. Papua 15,538.94 0.8% 6,475.53 0.3% 3,720.75 0.2% 3,241.36 0.2% 158.29 0.0%

TOTAL 1,858,174.90 100.0% 1,919,690.17 100.0% 1,946,704.18 100.0% 2,103,927.51 100.0% 452,922.87 100.0%

Provinsi / Province

PREMI BRUTO ASURANSI GEMPA BUMI

Premi Bruto Asuransi Gempa Bumi Berdasarkan Provinsi 2007 - 2011

Earthquake Gross Premium By Province 2007 - 2011

EARTHQUAKE INSURANCE GROSS PREMIUM *) As at 30 June 2011

12

S t a t i s t i k A s u r a n s i G e m p a B u m i I n d o n e s i a a s a t J u n e 2 0 1 1

Tabel 1.5 dibawah ini menyajikan penetrasi

asuransi gempa bumi per provinsi dan peta 1.1

menunjukkan distribusi eksposur asuransi

gempa bumi di Indonesia untuk tahun

underwriting 2011 berdasarkan provinsi,

catatan per tanggal 30 Juni 2011

This following table 1.5 shows earthquake

insurance penetration per province, and map

1.1 shows Indonesia earthquake exposure

distribution per province for underwriting year

2011 as at June 30, 2011

.

Tabel 1.5 / Table 1.5