THE ETHICS OF TAX EVASION:

AN EMPIRICAL STUDY OF UTAH OPINION

Robert W. McGee

Barry University, Miami Shores, FL 33161 USA, [email protected] (305) 899-3525 Sheldon R. Smith

Utah Valley State College, Orem, UT 84058 USA, [email protected] (801) 863-6153

ABSTRACT

The present paper is an empirical study, the goal of which is to determine the strength of the various arguments that have been used to justify tax evasion over the last 500 years. A survey was constructed using a seven-point Likert scale that included all three positions and all 18 arguments and distributed to 638 students at a large college in the western United States. The 18 arguments were ranked in terms of strength, from strongest to weakest. Comparisons were also made between male and female responses and between majors.

Keywords: tax evasion, ethics

Introduction

Most articles written on tax evasion are published in tax practitioner journals and take a practitioner or legal perspective. However, some authors have taken a philosophical approach (McGee, 1994). One of the most comprehensive analyses on tax evasion from a philosophical perspective was a doctoral thesis written by Martin Crowe in 1944. The Journal of Accounting,

Ethics & Public Policy published a series of articles on tax evasion from various religious,

secular and philosophical perspectives in 1998 and 1999. Most of those articles were also published in an edited book (McGee, 1998a). Since the publication of that book a few other articles have addressed the issue of tax evasion from an ethical perspective.

The ethics of tax evasion can be examined from a number of perspectives. Some of these are of a religious nature while others are more secular and philosophical. One approach is to examine the relationship of the individual to the state. Another is the relationship between the individual and the taxpaying community or some subset thereof. A third is the relationship of the individual to God. Martin Crowe (1944) examined the literature on these approaches, which are the three main approaches that have been taken in the literature over the past five centuries.

about tax evasion. McGee and Cohn (2006) surveyed the views of Orthodox Jews on the ethics of tax evasion. Not many empirical studies have been done on the ethics of tax evasion from a philosophical perspective. The present study is aimed at partially filling this gap in the literature. Review of the Literature

Although many studies have been done on tax compliance, very few have examined compliance, or rather noncompliance, primarily from the perspective of ethics. Most studies on tax evasion look at the issue from a public finance or economics perspective, although ethical issues may be mentioned briefly, in passing. The most comprehensive twentieth century work on the ethics of tax evasion was a doctoral thesis written by Martin Crowe (1944), titled The Moral Obligation of

Paying Just Taxes. This thesis reviewed the theological and philosophical debate that had been

going on, mostly within the Catholic Church, over the previous 500 years. Some of the debate took place in the Latin language. Crowe introduced this debate to an English language

readership. A more recent doctoral dissertation on the topic was written by Torgler (2003), who discussed tax evasion from the perspective of public finance but also touched on some

psychological and philosophical aspects of the issue. Alfonso Morales (1998) examined the views of Mexican immigrant street vendors and found that their loyalty to their families exceeded their loyalty to the government.

There have been a few studies that focus on tax evasion in a particular country. Ethics are sometimes discussed but, more often than not, the focus of the discussion is on government corruption and the reasons why the citizenry does not feel any moral duty to pay taxes to such a government. Ballas and Tsoukas (1998) discuss the situation in Greece. Smatrakalev (1998) discusses the Bulgarian case. Vaguine (1998) discusses Russia, as do Preobragenskaya and McGee (2004) to a lesser extent. A study of tax evasion in Armenia (McGee, 1999b) found the two main reasons for evasion to be the lack of a mechanism in place to collect taxes and the widespread opinion that the government does not deserve a portion of a worker’s income. A number of articles have been written from various religious perspectives. Cohn (1998) and Tamari (1998) discuss the Jewish literature on tax evasion and on ethics in general. Much of this literature is in Hebrew or a language other than English. McGee (1998d, 1999a) commented on these two articles from a secular perspective.

A few articles have been written on the ethics of tax evasion from various Christian viewpoints. Gronbacher (1998) addresses the issue from the perspectives of Catholic social thought and classical liberalism. Schansberg (1998) looks at the Biblical literature for guidance. Pennock (1998) discusses just war theory in connection with the moral obligation to pay just taxes, and not to pay unjust or immoral taxes. Smith and Kimball (1998) provide a Mormon perspective. McGee (1998c, 1999a) commented on the various Christian views from a secular perspective. The Christian Bible discusses tax evasion and the duty of the citizenry to support the government in several places. Schansberg (1998) and McGee (1994, 1998a) discuss the biblical literature on this point. When Jesus is asked whether people should pay taxes to Caesar, Jesus replied that we should give to Caesar the things that are Caesar’s and give God the things that are God’s

There are passages in the Bible that may be interpreted to take an absolutist position. For

example, Romans 13, 1-2 is read by some to support the Divine Right of Kings, which basically holds that whoever is in charge of government is there with God’s approval and anyone who disputes that fact or who fails to obey is subject to damnation. It is a sin against God to break any law. Thus, according to this viewpoint, Mao, Stalin and Hitler must all be obeyed, even though they were the three biggest monsters of the twentieth century, because they are there with God’s approval.

A few other religious views are also addressed in the literature. Murtuza and Ghazanfar (1998) discuss the ethics of tax evasion from the Muslim perspective. McGee (1998b, 1999a) comments on their article and also discusses the ethics of tax evasion under Islam citing Islamic business ethics literature (McGee, 1997). DeMoville (1998) discusses the Baha’i perspective and cites the relevant literature to buttress his arguments. McGee (1999a) commented on the DeMoville article. McGee (2004) discusses these articles in a book from a philosophical perspective. The Present Study

Methodology A survey instrument was constructed that included all three views on the ethics of tax evasion that Crowe (1944) identified in his thesis. Eighteen statements covering the 15 arguments that Crowe identified plus three more recent arguments were included. The survey was distributed to 638 students at a large college in the western United States. The statements generally began with the phrase “Tax evasion is ethical if …” Participants were asked to select a number from one to seven to reflect the extent of their agreement or disagreement with each statement. Results were tabulated and the arguments favoring tax evasion were ranked from strongest to weakest. Male and female scores were also compared, as well the scores by major area of study. The sample consisted of 456 males, 180 females and 2 unknown gender, or 638 in total. Categories by major were as follows: accounting 202, business & economics 300, legal studies 35, technology 34, and other 67.

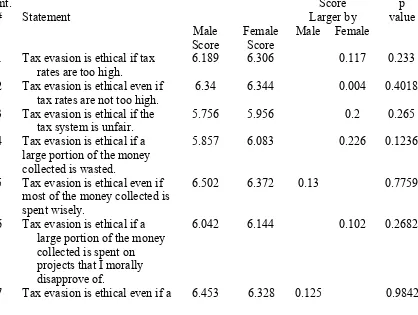

Survey Findings Table 1 shows the scores for each of the 18 statements, ranked according to the strength of each argument. Respondents were asked to select a number from 1 to 7 to indicate the extent of their agreement or disagreement with each statement, where 1 indicated strong agreement and 7 indicated strong disagreement.

One explanation for such a high score might be because 88% of the respondents were members of the Church of Jesus Christ of Latter-day Saints. The literature of this religion (Smith & Kimball 1998) strongly indicates that tax evasion is never justified. Another recent study (McGee & Cohn 2006) found that even Orthodox Jews strongly believe that Jews had an

obligation to pay taxes to Hitler. The score for this statement in the Orthodox Jewish survey also ranked as the strongest argument to support tax evasion, with a score of 3.12 using a similar survey instrument. Perhaps the reason why even Orthodox Jews believe there is an obligation to pay taxes to Hitler is because the Jewish literature takes the view that tax evasion is always, or almost always unethical (Cohn 1998; Tamari 1998).

Rank

Statement

Scores 1 Tax evasion would be ethical if I were a Jew living in Nazi Germany in

1940. (S16)

5.044 2 Tax evasion is ethical if the government imprisons people for their political

opinions. (S18)

5.511 3 Tax evasion is ethical if the government discriminates against me because

of my religion, race or ethnic background. (S17)

5.647 4 Tax evasion is ethical if a significant portion of the money collected winds

up in the pockets of corrupt politicians or their families and friends. (S11)

5.678 5 Tax evasion is ethical if the tax system is unfair. (S3) 5.816 6 Tax evasion is ethical if a large portion of the money collected is wasted.

(S4)

5.925 7 Tax evasion is ethical if I can’t afford to pay. (S14) 5.995 8 Tax evasion is ethical if a large portion of the money collected is spent on

projects that I morally disapprove of. (S6)

6.074 9 Tax evasion is ethical if tax rates are too high. (S1) 6.224 10 Tax evasion is ethical even if tax rates are not too high. (S2) 6.343 11 Tax evasion is ethical if some of the proceeds go to support a war that I

consider to be unjust. (S13)

6.345 12 Tax evasion is ethical if a large portion of the money collected is spent on

projects that do not benefit me. (S8)

6.405 13 Tax evasion is ethical even if a large portion of the money collected is spent

on worthy projects. (S7)

6.419 14 Tax evasion is ethical even if a large portion of the money collected is spent

on projects that do benefit me. (S9)

6.420 15 Tax evasion is ethical even if most of the money collected is spent wisely.

(S5)

6.467 16 Tax evasion is ethical if the probability of getting caught is low. (S12) 6.473 17 Tax evasion is ethical if everyone is doing it. (S10) 6.486 18 Tax evasion is ethical even if it means that if I pay less, others will have to

pay more. (S15)

6.497 Table 1: Ranking of Arguments

Three of the 18 statements in the survey (S16, 17 & 18) might be labeled as “human rights” arguments to justify tax evasion. These were the three arguments that Crowe (1944) did not identify in his research. These were also the three arguments that scored highest in the present survey, meaning that they were the three strongest arguments justifying tax evasion. But even these arguments were not regarded as strong by the participants, since their scores were 5.044, 5.647 and 5.511, respectively.

It was found that the arguments to justify tax evasion were stronger in cases where the government was corrupt or inefficient or where the system was perceived as being unfair. Inability to pay also ranked high, which lends support to the arguments put forth by a scholar who discussed tax evasion in the Latin culture (Morales 1998). Inability to pay was also identified as one of the most popular arguments favoring evasion in the Catholic religious literature (Crowe 1944). The weakest arguments were found to be the arguments that might be labeled as selfish reasons.

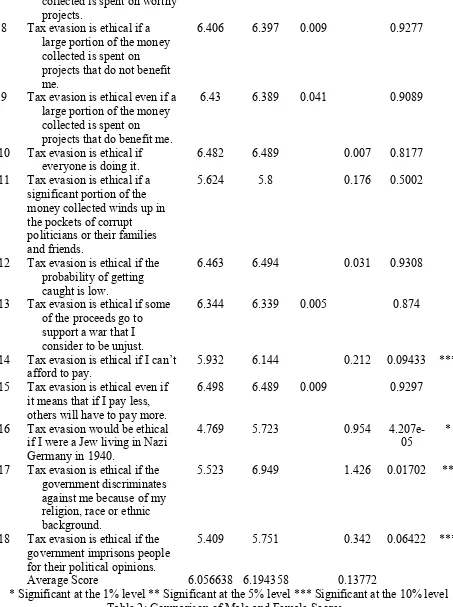

Table 2 compares male and female scores for each statement. Some studies in gender ethics have found that women are more ethical than men (Akaah & Riordan 1989; Baird 1980; Brown & Choong 2005; Sims, Cheng & Teegen 1996), while other studies found that there is no statistical difference between men and women when it comes to ethics (Roxas & Stoneback 2004; Sikula & Costa 1994; Swaidan, Vitell, Rose & Gilbert 2006). A few studies have found that men are more ethical than women (Barnett & Karson 1987; Weeks, Moore, McKinney & Longenecker 1999). It was thought that comparing the male and female scores would be interesting, although the comparison could not lead to any conclusion regarding the relative ethics of men and women. Stmt. tax rates are not too high.

6.34 6.344 0.004 0.4018

3 Tax evasion is ethical if the tax system is unfair.

5.756 5.956 0.2 0.265 4 Tax evasion is ethical if a

large portion of the money collected is wasted.

5.857 6.083 0.226 0.1236

5 Tax evasion is ethical even if most of the money collected is spent wisely.

6.502 6.372 0.13 0.7759

6 Tax evasion is ethical if a large portion of the money collected is spent on projects that I morally disapprove of.

6.042 6.144 0.102 0.2682

large portion of the money collected is spent on worthy projects.

8 Tax evasion is ethical if a large portion of the money collected is spent on projects that do not benefit me.

6.406 6.397 0.009 0.9277

9 Tax evasion is ethical even if a large portion of the money collected is spent on projects that do benefit me.

6.43 6.389 0.041 0.9089 money collected winds up in the pockets of corrupt

13 Tax evasion is ethical if some of the proceeds go to

15 Tax evasion is ethical even if it means that if I pay less, others will have to pay more.

6.498 6.489 0.009 0.9297

16 Tax evasion would be ethical if I were a Jew living in Nazi against me because of my religion, race or ethnic

Table 2 shows that the female scores were higher than the male scores in 12 of 18 cases. But applying Wilcoxon tests to the data found that female scores were significantly higher than male scores in only 4 cases. However, these findings do not allow us to conclude that women are more ethical than men. In order to arrive at that conclusion we must begin with the premise that tax evasion is unethical, which may or may not be the case. At least one author of the present study believes that tax evasion is not unethical for Jews living in Nazi Germany. Thus, all we can conclude is that women are sometimes more opposed to tax evasion than are men.

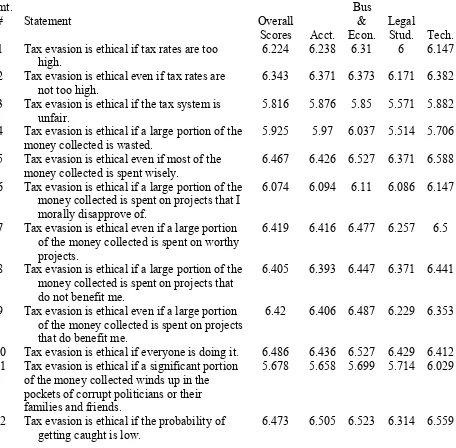

Table 3 compares the scores for each statement by major area of study. The technology majors (6.158) scored slightly higher than the business and economics majors (6.151), who scored somewhat higher than the accounting majors (6.119). The legal studies students scored the lowest of the four categories (5.958). But all four groups were strongly opposed to most of the tax evasion arguments. 1 Tax evasion is ethical if tax rates are too

high.

6.224 6.238 6.31 6 6.147 2 Tax evasion is ethical even if tax rates are

not too high.

6.343 6.371 6.373 6.171 6.382 3 Tax evasion is ethical if the tax system is

unfair.

5.816 5.876 5.85 5.571 5.882 4 Tax evasion is ethical if a large portion of the

money collected is wasted.

5.925 5.97 6.037 5.514 5.706 5 Tax evasion is ethical even if most of the

money collected is spent wisely.

6.467 6.426 6.527 6.371 6.588 6 Tax evasion is ethical if a large portion of the

money collected is spent on projects that I morally disapprove of.

6.074 6.094 6.11 6.086 6.147

7 Tax evasion is ethical even if a large portion of the money collected is spent on worthy projects.

6.419 6.416 6.477 6.257 6.5

8 Tax evasion is ethical if a large portion of the money collected is spent on projects that do not benefit me.

6.405 6.393 6.447 6.371 6.441

9 Tax evasion is ethical even if a large portion of the money collected is spent on projects that do benefit me.

6.42 6.406 6.487 6.229 6.353

10 Tax evasion is ethical if everyone is doing it. 6.486 6.436 6.527 6.429 6.412 11 Tax evasion is ethical if a significant portion

of the money collected winds up in the pockets of corrupt politicians or their families and friends.

5.678 5.658 5.699 5.714 6.029

12 Tax evasion is ethical if the probability of getting caught is low.

13 Tax evasion is ethical if some of the proceeds go to support a war that I consider to be unjust.

6.345 6.406 6.39 6.486 6.382

14 Tax evasion is ethical if I can’t afford to pay. 5.995 6.079 6.127 5.571 5.765 15 Tax evasion is ethical even if it means that if

I pay less, others will have to pay more.

6.497 6.495 6.533 6.457 6.618 16 Tax evasion would be ethical if I were a Jew

living in Nazi Germany in 1940.

5.044 5.26 4.949 4.829 4.971 17 Tax evasion is ethical if the government

discriminates against me because of my religion, race or ethnic background.

5.647 5.577 5.763 5.6 6

18 Tax evasion is ethical if the government imprisons people for their political opinions.

5.511 5.543 5.586 5.273 5.97

Average Score 6.098 6.119 6.151 5.958 6.158

Table 3: Comparison of Scores by Major (1= strongly agree; 7 = strongly disagree)

Concluding Comments

The goal of the present study was achieved. The major arguments that have been put forward to justify tax evasion in recent centuries have been ranked. As expected, some arguments proved to be stronger than others. None of the arguments proved to be very strong, however, as indicated by the high scores received for even the strongest arguments.

Women were more strongly opposed to tax evasion for the three human rights arguments and for the ability to pay argument but their scores were not significantly different from the men’s scores for the other 14 statements. Scores did not vary much by major, at least on average, although scores did at times diverge for individual statements.

REFERENCES

Akaah, I. P. and E. A. Riordan. (1989). Judgments of Marketing Professionals about Ethical Issues in Marketing Research: A Replication and Extension. Journal of Marketing

Research 26(1), 112-120.

Baird, J.S. (1980). Current Trends in College Cheating. Psychology in the Schools 17(4), 515-522, as cited in Brown & Choong (2005).

Ballas, A. A. and H. Tsoukas. (1998). Consequences of Distrust: The Vicious Circle of Tax Evasion in Greece. Journal of Accounting, Ethics & Public Policy, 1(4), 572-596. Barnett, J. H. and M. J. Karson. (1987). Personal Values and Business Decisions: An

Exploratory Investigation. Journal of Business Ethics 6(5), 371-382.

Brown, B. S. and P. Choong. (2005). An Investigation of Academic Dishonesty among Business Students at Public and Private United States Universities. International Journal of

Cohn, G. (1998). The Jewish View on Paying Taxes. Journal of Accounting, Ethics & Public

Policy 1(2): 109-120.

Crowe, M. T. (1944). The Moral Obligation of Paying Just Taxes, The Catholic University of America Studies in Sacred Theology No. 84.

DeMoville, W. (1998). The Ethics of Tax Evasion: A Baha’i Perspective. Journal of Accounting,

Ethics & Public Policy 1(3), 356-368.

Englebrecht, T. D., B. Folami, C. Lee and J. J. Masselli. (1998). The Impact on Tax Compliance Behavior: a Multidimensional Analysis. Journal of Accounting, Ethics & Public Policy

1(4), 738-768.

Gronbacher, G.M.A. (1998). Taxation: Catholic Social Thought and Classical Liberalism.

Journal of Accounting, Ethics & Public Policy 1(1), 91-100.

Inglehart, R., M. Basanez, J. Diez-Medrano, L. Halman and R. Luijkx (eds.). (2004). Human Beliefs and Values: a cross-cultural sourcebook based on the 1999-2002 values surveys. Mexico: Siglo XXI Editores.

McGee, R. W. (1994). Is Tax Evasion Unethical? University of Kansas Law Review 42(2), 411-435. Reprinted at HTUhttp://ssrn.com/abstract=74420UTH.

McGee, R. W. (1997). The Ethics of Tax Evasion and Trade Protectionism from an Islamic Perspective. Commentaries on Law & Public Policy 1, 250-262. Reprinted at

HTU

http://ssrn.com/abstract=461397UTH.

McGee, R. W. (ed.) (1998a). The Ethics of Tax Evasion. Dumont, NJ: The Dumont Institute for Public Policy Research.

McGee, R. W. (1998b). The Ethics of Tax Evasion in Islam: A Comment. Journal of

Accounting, Ethics & Public Policy 1(2), 162-168.

McGee, R. W. (1998c). Christian Views on The Ethics of Tax Evasion. Journal of Accounting,

Ethics & Public Policy 1(2), 210-225. Reprinted at HTUhttp://ssrn.com/abstract=461398UTH.

McGee, R. W. (1998d). Jewish Views on the Ethics of Tax Evasion. Journal of Accounting,

Ethics & Public Policy 1(3), 323-336. Reprinted at HTUhttp://ssrn.com/abstract=461399UTH.

McGee, R. W. (1998e). Ethical Views on Tax Evasion among Swedish CEOs: A Comment.

Journal of Accounting, Ethics & Public Policy 1(3), 460-467. Reprinted at

HTU

http://ssrn.com/abstract=713903UTH.

McGee, R. W. (1999a). Is It Unethical to Evade Taxes in an Evil or Corrupt State? A Look at Jewish, Christian, Muslim, Mormon and Baha’i Perspectives. Journal of Accounting,

Ethics & Public Policy 2(1), 149-181. Reprinted at HTUhttp://ssrn.com/abstract=251469UTH.

McGee, R. W. (1999b). Why People Evade Taxes in Armenia: A Look at an Ethical Issue Based on a Summary of Interviews. Journal of Accounting, Ethics & Public Policy 2(2), 408-416. Reprinted at HTUhttp://ssrn.com/abstract=242568UTH.

McGee, R. W. (2004). The Philosophy of Taxation and Public Finance. Boston, Dordrecht and London: Kluwer Academic Publishers.

McGee, R. W. and G. Cohn. (2006). Jewish Perspectives on the Ethics of Tax Evasion. Andreas School of Business Working Paper Series, September.

Morales, A. (1998). Income Tax Compliance and Alternative Views of Ethics and Human Nature. Journal of Accounting, Ethics & Public Policy 1(3), 380-399.

Murtuza, A. and S.M. Ghazanfar. (1998). Taxation as a Form of Worship: Exploring the Nature of Zakat. Journal of Accounting, Ethics & Public Policy 1(2), 134-161.

Nylén, U. (1998). Ethical Views on Tax Evasion among Swedish CEOs. Journal of Accounting,

Pennock, R. T. (1998). Death and Taxes: On the Justice of Conscientious War Tax Resistance.

Journal of Accounting, Ethics & Public Policy 1(1), 58-76.

Preobragenskaya, G. G. and R. W. McGee. (2004). Taxation and Public Finance in a Transition Economy: A Case Study of Russia. In Carolyn Gardner, Jerry Biberman and Abbass Alkhafaji (eds.), Business Research Yearbook: Global Business Perspectives Volume XI, Saline, MI: McNaughton & Gunn, Inc., 2004, pp. 254-258. A longer version, which was presented at the Sixteenth Annual Conference of the International Academy of Business Disciplines in San Antonio, March 25-28, 2004, is available at

HTU

http://ssrn.com/abstract=480862UTH

Reckers, P. M.J., D. L. Sanders and S. J. Roark. (1994). The Influence of Ethical Attitudes on Taxpayer Compliance. National Tax Journal 47(4), 825-836.

Roxas, M. L. & J. Y. Stoneback. (2004). The Importance of Gender Across Cultures in Ethical Decision-Making. Journal of Business Ethics 50,149-165.

Schansberg, D. E.. (1998). The Ethics of Tax Evasion Within Biblical Christianity: Are There Limits to ‘Rendering Unto Caesar’? Journal of Accounting, Ethics & Public Policy 1(1), 77-90.

Sikula, A., Sr. and A. D. Costa. (1994). Are Women More Ethical than Men? Journal of

Business Ethics 13(11), 859-871.

Sims, R. R., H. K. Cheng & H. Teegen. (1996). Toward a Profile of Student Software Piraters.

Journal of Business Ethics 15(8), 839-849.

Smatrakalev, G.. (1998). Walking on the Edge: Bulgaria and the Transition to a Market Economy. In Robert W. McGee (ed.),The Ethics of Tax Evasion. Dumont, NJ: The Dumont Institute for Public Policy Research, 1998, pp. 316-329.

Smith, S. R. and K. C. Kimball. (1998). Tax Evasion and Ethics: A Perspective from Members of The Church of Jesus Christ of Latter-Day Saints. Journal of Accounting, Ethics &

Public Policy 1(3), 337-348.

Swaidan, Z., S. J. Vitell, G. M. Rose and F. W. Gilbert. (2006). Consumer Ethics: The Role of Acculturation in U.S. Immigrant Populations. Journal of Business Ethics 64(1), 1-16. Tamari, M. (1998). Ethical Issues in Tax Evasion: A Jewish Perspective. Journal of Accounting,

Ethics & Public Policy 1(2), 121-132.

Torgler, B. (2003). Tax Morale: Theory and Empirical Analysis of Tax Compliance. Dissertation der Universität Basel zur Erlangung der Würde eines Doktors der Staatswissenschaften. Vaguine, V. V. (1998). The ‘Shadow Economy’ and Tax Evasion in Russia. In Robert W.

McGee, editor, The Ethics of Tax Evasion. Dumont, NJ: The Dumont Institute for Public Policy Research, 1998, pp. 306-314.