Full Terms & Conditions of access and use can be found at

http://www.tandfonline.com/action/journalInformation?journalCode=vjeb20

Download by: [Universitas Maritim Raja Ali Haji] Date: 11 January 2016, At: 19:08

Journal of Education for Business

ISSN: 0883-2323 (Print) 1940-3356 (Online) Journal homepage: http://www.tandfonline.com/loi/vjeb20

The Major Field Test in Business: A Direct Measure

of Learning in Common Business Disciplines

Susan A. Simmons, Wesley M. Jones Jr. & Cynthia E. Bolt

To cite this article: Susan A. Simmons, Wesley M. Jones Jr. & Cynthia E. Bolt (2015) The Major Field Test in Business: A Direct Measure of Learning in Common Business Disciplines, Journal of Education for Business, 90:2, 57-62, DOI: 10.1080/08832323.2014.973825

To link to this article: http://dx.doi.org/10.1080/08832323.2014.973825

Published online: 24 Nov 2014.

Submit your article to this journal

Article views: 79

View related articles

The Major Field Test in Business: A Direct Measure

of Learning in Common Business Disciplines

Susan A. Simmons, Wesley M. Jones, Jr., and Cynthia E. Bolt

The Citadel, Charleston, South Carolina, USA

Assurance of learning and its assessment are critical focal points in collegiate schools of business as programs strive to achieve or maintain Association to Advance Collegiate Schools of Business accreditation. Prior research suggests that student learning in business core disciplines can be measured by the Educational Testing Service Major Field Test in Business (MFT-B). What factors predict student performance on the MFT-B? The authors examined predictors of student learning not addressed in prior research. The analysis of this unique variable set consisting of high school grade point average, grade on an accounting competency exam, cumulative hours earned, and membership in the School of Business Mentor Association furnishes noteworthy, new insight to the understanding of factors that affect learning in business core disciplines.

Keywords: AACSB accreditation, assurance of learning, ETS Major Field Test in Business, student learning

Assurance of learning (AOL) and its assessment are critical focus points in collegiate schools of business as programs strive to achieve or maintain accreditation by the Associa-tion to Advance Collegiate Schools of Business (AACSB). In 2003, AACSB accreditation standards evolved to center on AOL along with direct measures of student learning (AACSB, 2007). This shifts the focus from what instructors teach to what students learn (Martell, 2007). The AACSB wants schools of business to define student learning goals, identify instruments and measures to assess learning, ana-lyze and operationalize assessment information for continu-ous improvement (AACSB, 2007). The most recent AACSB Eligibility Procedures and Accreditation Standards for Business Accreditation (AACSB, 2013) drafted by the organization declares student learning to be the fundamen-tal concern of collegiate education.

The continuing charge of collegiate business programs is assessment, which in the case of student learning requires mul-tiple approaches, projects, assignments, rubrics, and exams. The AACSB requirement that students have an understanding of business core disciplines provides one area for evaluation. A direct measure of student knowledge of these core concepts

comes from the Educational Testing Service (ETS; 2011) Major Field Test in Business (MFT-B).

BACKGROUND OF THE PROBLEM AND PURPOSE OF THE STUDY

Prior research demonstrated the MFT-B to be a valid method to gauge student learning in common business dis-ciplines (Bagamery, Lasik, & Nixon, 2005; Black & Duhon, 2003; Mirchandani, Lynch, & Hamilton, 2001). This past research suggests that student learning in business core disciplines can be measured by the MFT-B, and exten-sive research exists on the determinants of student perfor-mance on the exam. Using the categorization defined by Mirchandani et al. (2001), variables that influence MFT-B achievement can be classified as input variables, such as SAT scores, transfer grade point average (GPA), and gen-der; and process variables, such as course grades. Other research has expanded the input variable list to include ACT score, ethnicity, age (Black & Duhon, 2003), and transfer versus native student (Bagamery et al., 2005). The process variables list has expanded to include business core GPA as well as overall GPA (Allen & Bycio, 1997), student motivation (Bycio & Allen, 2007; Terry, Mills, & Sollosy, 2008), major, and course location (Bagamery et al., 2005).

Correspondence should be addressed to Susan A. Simmons, The Cita-del, School of Business Administration, 171 Moultrie Street, Charleston, SC 29409, USA [email protected]

ISSN: 0883-2323 print / 1940-3356 online DOI: 10.1080/08832323.2014.973825

Our research also addresses the research question: What factors predict student performance on the MFT-B? Predic-tor variables, some incorporated in prior research and some unique to our study, include: high school GPA, SAT score, cumulative hours earned, cumulative GPA, grade on an accounting competency exam, final grade in a required accounting course, and membership in the School of Busi-ness Mentor Association. Our research is the first to investi-gate the contribution of the following variables to student learning in business disciplines: high school GPA, final grade in the first required accounting course, grade on an accounting competency exam, cumulative hours earned, and student membership in the School of Business Mentor Association.

Our research continues with a background of AACSB accreditation and AOL, the literature review, method and description of the sample, results, and discussion.

Background of AACSB Accreditation, Assurance of Learning, and the MFT-B

In 1992 the AACSB replaced resource-oriented standards for business program accreditation with criterion that focused on continuous improvement (AACSB-The Interna-tional Association for Management Education, 1995). In 2003 the AACSB updated accreditation standards with a component that emphasized AOL. The AACSB instructed schools of business to define student learning goals and conduct direct assessments of learning to be used to improve curricula (AACSB, 2007). The AACSB (2007) guidance for AOL follows these five steps:

1. Definition of student learning goals and objectives; 2. Alignment of curricula with the adopted goals; 3. Identification of instruments and measures to assess

learning;

4. Collection, analysis, and dissemination of assessment information; and

5. Use of assessment information for continuous improvement of the program curriculum including documentation that the assessment process is being carried out in a systematic, ongoing basis.

In order to meet the AACSB’s AOL standards, the mis-sion and goals of the program must link directly to learning outcomes—what the students do, know, or value—and feedback on the learning outcomes needs to improve the program. This leads to a requirement for ongoing data gath-ering and analysis from appropriate sources (White, 2007).

The AACSB provides flexibility in identifying measures to assess the achievement of learning goals and objectives. One approach is to measure student achievement of learn-ing goals through stand-alone testlearn-ing, normally completed outside the classroom and using a standardized assessment exam. One direct measure of basic knowledge from a range

of business disciplines is the ETS MFT-B (Educational Testing Service, 2011). In our study, the MFT-B will serve as a direct measure of student learning in core business disciplines.

REVIEW OF THE LITERATURE

Several studies provide valuable insight into the pros, cons, and methods for using the ETS MFT-B for assessment of student learning as well as continuous improvement of business programs. Research on factors that influence stu-dent success on the MFT-B serve as a basis for our research.

Allen and Bycio (1997) studied students’ scores on the MFT-B to establish its relationship to GPA and measures of general intellect. The goal was to determine if the pattern of associations made sense, given that the test was intended to reflect business knowledge. The authors found that stu-dents with higher SAT scores and higher business core GPA performed better on the MFT-B.

Mirchandani et al. (2001) investigated the use of the ETS MFT-B as an assessment tool and focused on internal users of outcomes assessment (i.e., faculty members and administrators who use the test results to improve curricu-lum and programs). Mirchandani et al. identified two types of variables that could influence performance on the MFT-B: input (SAT scores, gender, transfer GPA) and process (grades in each of the business core courses). Their catego-rization of input and process variables carried into future research. Their research found that students’ SAT score and GPA in the quantitative courses had a significant influence on students’ MFT-B performance.

Black and Duhon (2003) discussed how to use standard-ized assessment tests to comply with the AACSB require-ment, AOL. Their intent was to improve assessment of student learning by (a) reviewing issues related to the appropriateness of a standardized test of student achieve-ment and (b) providing examples of ways the MFT-B results could be operationalized for continuous improve-ment of the curriculum, student learning, and program development (Black & Duhon, 2003).

Bagamery et al. (2005) integrated variables not yet ana-lyzed in MFT-B research by including the site for the course (on or off campus), transfer status, and GPAs for business core and business preadmission courses. The learning assessment program in the College of Business at Central Washington University provided a sample of 169 students who took the MFT-B as a component of a business capstone course. The four grade factors—general, quantitative, accounting, and management—along with gender and whether the student took the SAT were identified as significant indicators of MFT-B success. The results provide support for the conclusion that all business core courses lead to learning as measured by the MFT-B (Bagamery et al., 2005).

58 S. A. SIMMONS ET AL.

In an extension of their 1997 research (Allen & Bycio, 1997), Bycio and Allen (2007) assessed the impact of stu-dent motivation on MFT-B performance. A stustu-dent motiva-tion scale was created by summing student rankings to four statements regarding their motivation for taking the MFT-B. SAT scores, student major, and the student motivation scale were found to be significant predictors of MFT-B scores (Bycio & Allen, 2007).

The role of student motivation on MFT-B performance is further investigated by Terry et al. (2008). Reflecting on earlier student motivation research and its role in MFT-B performance (Allen & Bycio, 1997; Bycio & Allen, 2007) Terry et al. (2008) focus on student motivation to perform well on the MFT-B exam when their test score becomes part of their capstone course grade. Their analysis reveal a direct relationship between MFT-B performance, academic ability (ACT score), and academic performance (GPA). Student motivation variables, measured by the MFT-B score becoming either 10% or 20% of the student’s cap-stone course grade, are both significantly correlated with MFT-B score (Terry et al., 2008).

The MFT-B has been used as an assessment tool for fif-teen years at Virginia Military Institute (VMI) Department of Economics and Business and information gathered from the test results has led to changes in curriculum, faculty composition, and policies in the department. The evolution of these changes, which resulted from information gleaned from the MFT-B data, was outlined by Bush, Duncan, Sex-ton, and West (2008).

Contreras, Badua, Chen, and Adrian (2011) extended research by Allen and Bycio (1997); Bycio and Allen (2007); and DeMong, Lindgren, and Perry (1994) to inves-tigate the effects of age, gender, ethnicity, major, and aca-demic histories on student MFT-B scores. Based on the sample of 352 students Contreras et al. (2011) estimated multiple regression models that revealed age, male gender, ACT score, and overall GPA were significantly, positively correlated to MFT-B scores.

Another positive influence on ETS MFT-B perfor-mance comes from course-embedded assessments according to research by Barboza and Pesek (2012). Using a sample of 173 students, the authors found that course-embedded assessments have a statistically signifi-cant impact on MFT-B scores, after controlling for the influence of SAT score, GPA, major, and gender (Bar-boza & Pesek, 2012).

The research of Bielinska-Kwapisz, Brown, and Seme-nik (2012a and 2012b) addresses the issue of how to con-trol for changing student demographics so that MFT-B scores from one test date to another can be compared. They developed and tested a procedure that allows for interpretation of MFT-B scores coming from different student samples (Bielinska-Kwapisz, Brown, & Semenik, 2012a, 2012b).

Chowdhury and Wheeling (2013) examined how chang-ing student demographics influence the association between variables, such as SAT score and GPA, and the students’ performance on the MFT-B. They looked at unanswered questions regarding predictors of MFT-B scores and the consistency of predictor variables over time and different student cohorts.

With previous research into factors affecting student learning in business disciplines as a foundation, we make significant research contributions by investigating the role of learning predictors not studied previously. Our study uncovers the roles played by high school GPA, grade on an accounting competency exam, final grade in the first required accounting course, cumulative hours earned, and membership in the School of Business Mentor Association in learning in business disciplines. The outcomes lead to improvements and modifications in course content, curricu-lum, and student learning.

METHODS

Sample and Procedure

The School of Business at The Citadel, Charleston, South Carolina, administered the MFT-B during six test dates from fall 2002 through spring 2007 to undergraduate busi-ness majors enrolled in the capstone busibusi-ness course. A total of 405 student test results were collected. To improve student motivation to take the exam seriously and do well on the test, student performance on the MFT-B comprised 5% of their business capstone course grade.

Variables

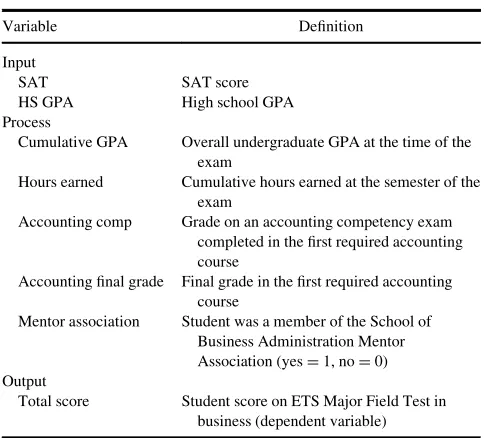

The purpose of this study is to examine the impact of explanatory variables on students’ performance on the MFT-B. The independent variables that were hypothesized to have a significant correlation with MFT-B scores were categorized as input variables (SAT score, high school GPA) and process variables (cumulative GPA, cumulative hours earned, final grade accounting, grade on an account-ing competency exam, and whether the student was a mem-ber of The Citadel School of Business Mentor Association). The dependent variable, student score on the MFT-B, served as a proxy for student learning and is categorized as an output variable.

Of the 405 students who took the MFT-B exam, com-plete data sets were collected on 226 students for all inde-pendent variables except accounting final grade and the grade on an accounting competency exam. For these two accounting related variables, the sample with complete data sets was 66 students. Table 1 gives the variable names and definitions.

RESULTS

Multiple regression analysis was used to examine the degree to which the entire set of predictors could account for MFT-B performance, the dependent variable, and a proxy for student learning. A multivariate regression model that includes all independent variables, along with a pfor each regression coefficient, is displayed in Table 2. Step-wise regression was used to develop a multivariate regres-sion model that contained statistically significant regresregres-sion coefficients. See Table 3 for the independent variables in the final regression model, regression coefficients, andpfor each regression coefficient.

DISCUSSION

MFT-B Performance and All Independent Variables

As Table 2 shows, we used multiple regression analysis to examine the degree to which our set of seven independent

variables made a significant contribution to the prediction of MFT-B performance. The predictors accounted for a sta-tistically significant 47.1% of the variance in MFT-B scores (p <.000). As seen in the regression model, Table 2, not all regression coefficients were statistically significant.

Collinearity, the condition of one independent variable being correlated with another independent variable, is a problem when all independent variables are included in the regression model. Because pairs of variables provide dupli-cate information, interpretation of individual regression coefficients would be unreliable. With collinearity, a vari-able may appear to be statistically significant when it is insignificant or vice versa (Render, Stair, & Hanna, 2009). Variables not significant at the 5% level included cumula-tive GPA, cumulacumula-tive hours earned, and the accounting var-iables. Possible reasons for the missing significance are explained in the Discussion section.

Stepwise regression was used to correct for multicolli-nearity and improve the statistical significance of the regression coefficients of the included variables. Our final model, shown in Table 3, explains a statistically significant 46.5% of the variance in MFT-B scores (p < .000). The final model is based on a sample of 226 students and con-tains two input variables, SAT score and high school GPA, and two process variables, cumulative GPA and student membership in the School of Business Mentor Association. All regression coefficients were statistically significant at the 5% or better level.

From this multiple regression model we found the following:

A one-point increase in cumulative GPA was

associ-ated with an 8.167-point increase in MFT-B score;

A one-point increase in high school GPA was

associ-ated with a 2.499-point increase in MFT-B score;

A one-point increase in SAT score was associated

with a 0.056-point increase in MFT-B score;

Being a member of the School of Business

Adminis-tration Mentor’s Association was associated with a 3.117-point increase in MFT-B score;

Our findings uncover significant relationships

between performance on the MFT-B and predictors of student learning not previously investigated: high

TABLE 1

Variable Notations and Definitions

Variable Definition

Input

SAT SAT score

HS GPA High school GPA Process

Cumulative GPA Overall undergraduate GPA at the time of the exam

Hours earned Cumulative hours earned at the semester of the exam

Accounting comp Grade on an accounting competency exam completed in the first required accounting course

Accounting final grade Final grade in the first required accounting course

Mentor association Student was a member of the School of Business Administration Mentor Association (yesD1, noD0)

Output

Total score Student score on ETS Major Field Test in business (dependent variable)

TABLE 2

Multiple Regression Results: All Predictor Variables

Variable t p

Cumulative GPA 0.0709 ns

Cumulative hours earned 0.178 ns

High school GPA 1.880 .071

SAT 3.650 .001

Accounting comp 0.924 ns

Accounting final grade 1.369 ns

Mentor association 2.250 .033

Note: nD66,R2D.471.Fsignificance (p)D.0000,dfD58.

TABLE 3

Multiple Regression Results: Final Model

Variable Regression coefficient p

SAT 0.056 .000

Cumulative GPA 8.167 .000

Mentor association 3.117 .023

High school GPA 2.499 .035

Note:Dependent variable: Educational Testing Service Major Field Test in Business score.nD226,R2D.465.FD48.084,pD.0000,df1D4,

df2D221.

60 S. A. SIMMONS ET AL.

school GPA and membership in the School of Busi-ness Mentor Association.

High School GPA and Membership in the Mentor Association

The continual flow of learning from high school through the undergraduate business program is evidenced by the signifi-cant association of high school GPA and MFT-B score. Studies prior to ours did not consider the contribution of high school GPA to learning in core business disciplines. Our study addresses this issue and finds a statistically sig-nificant connection between high school learning and col-lege-level learning.

Student membership in the School of Business Men-tor Association, a variable not included in prior research, exhibits a statistically significant relationship to MFT-B performance (see Table 3). A closer look at the components of the Mentor Association gives insight into the link between student membership and learning as measured by the MFT-B. The aim, as given in the Mission Statement of The Citadel School of Business Mentor Association, is to “Coach students to become ethical leaders of principle to serve others and to pursue lofty personal goals in business, the military, the profes-sions, nonprofit organizations, and public service” (The Citadel School of Business Administration Mentor Asso-ciation, 2011, p. 1). Participation in the Mentor Associa-tion is voluntary. This noteworthy finding of the contribution of an extracurricular activity to student learning is exclusive to this study. The association between MFT-B performance and membership in the Mentor Association may be indicative of high-achieving students self-selecting extracurricular activities. Their motivation to achieve includes both learning that comes from completing the courses required for the business degree as well as learning from opportunities outside the classroom.

Reinforcement of Prior Research

Our finding of the association between SAT scores and cumulative undergraduate GPA and performance on the MFT-B reinforces similar findings by Black and Duhon (2003), Mirchandani et al. (2001), Allen and Bycio (1997), Bycio and Allen (2007), Bagamery et al. (2005), Terry et al. (2008), and Contreras et al. (2011).

Excluded Variables

We investigated variables, not covered in prior research, which had a weak relationship with MFT-B scores: cumula-tive hours earned, final grade in the first accounting course, and grade on an accounting competency exam. The lack of significance makes an outstanding contribution to our

understanding of previously undocumented variables and requires analysis and explanation. The lack of significance for cumulative hours earned may derive from students hav-ing approximately the same number of earned hours when they sat for the MFT-B, and the lack of variability may explain the weak relationship.

The lack of significance of the final grade in accounting and the grade earned on an accounting competency exam derives from the small sample size and collinearity of these variables with each other as well as cumulative GPA. The accounting competency exam, administered to all students in the introductory financial accounting course, is designed to cover basic financial statement preparation and general accounting procedures and concepts. Students take the exam mid-semester and it comprises 5.25% of the student’s accounting course grade. Student performance on the com-petency exam often correlates to the student’s final grade in accounting.

SIGNIFICANT FINDINGS AND FUTURE RESEARCH

We identified several notable determinants of business stu-dent performance on the MFT-B, not previously studied. Our study, the first to evaluate the role of high school GPA, cumulative hours earned, membership in the Mentor Asso-ciation, and grades on an accounting competency exam and in an accounting course, adds important contributions to assurance of learning literature.

Another outstanding contribution to assurance of learn-ing derives from the sample of students from a small South-eastern regional state supported military college. The sample consists of members of the South Carolina Corps of Cadets (SCCC) who live in on-campus barracks and com-plete their degree program as a group. Their group dynam-ics and military lifestyle parallels the sample used in the VMI study (Bush et al., 2008) and reinforces their study by finding the MFT-B research useful in closing the assess-ment loop by providing insight into changes needed in cur-riculum and course content. Future studies could expand the set of possible process variables to include GPA in the five-course prebusiness core, course grades from each con-tent area on the MFT-B, student professional pathways within the business administration curriculum, student internship programs, and student membership in business honor societies and organizations.

Another research venue comes from the fact that data for this research was limited to a state college in the southeast-ern United States. Other research cited in our study had samples constrained to individual institutions or states, such as Ohio (Bycio & Allen, 2007), New Jersey (Mirchan-dani et al., 2009), and Kansas (Chowdhury & Wheeling, 2013). Future researchers should span several institutions from different states.

REFERENCES

Allen, J. S., & Bycio, P. (1997). An evaluation of the educational testing service major field achievement test in business.Journal of Accounting Education,15, 503–514.

Association to Advance Collegiate Schools of Business International (AACSB). (2007).Eligibility procedures and accreditation standards for business accreditation. Tampa, FL: Author.

Association to Advance Collegiate Schools of Business International (AACSB) (2013).Eligibility procedures and accreditation standards for business accreditation. Standard 8. Tampa, FL: Author.

Association to Advance Collegiate Schools of Business International (AACSB)-The International Association for Management Education. (1995). Achieving quality and continuous improvement through self-evaluation and peer review: Standards for accreditation, business administration and accounting. St. Louis, MO: Authors.

Bagamery, B. D., Lasik, J. J., & Nixon, D. R. (2005). Determinants of suc-cess on the ETS business major field exam for students in an undergrad-uate multisite regional university business program. Journal of Education for Business,81, 55–63.

Barboza, G. A., & Pesek, J. (2012). Linking course-embedded assessment measures and performance on the Educational Testing Service Major Field Test in Business.Journal of Education for Business,87, 102–111. Bielinska-Kwapisz, A., Brown, F. W., & Semenik, R. (2012a). Interpreting

standardized assessment test scores and setting performance goals in the context of student characteristics: The case of the major field test in busi-ness.Journal of Education for Business,87, 7–13.

Bielinska-Kwapisz, A., Brown, F. W., & Semenik, R. (2012b). Is higher better? Determinants and comparisons of performance on the Major Field Test in Business.Journal of Education for Business,87, 159–169. Black, H. T., & Duhon, D. D. (2003) Evaluating and improving student

achievement in business programs: The effective use of standardized assessment tests.Journal of Education for Business,79, 90–98. Bush, H. F., Duncan, F. H., Sexton, E. A., & West, C. T. (2008). Using the

Major Field Test-Business as an assessment tool and impetus for pro-gram improvement: Fifteen years of experience at Virginia military institute.Journal of College Teaching & Learning,5, 75–88.

Bycio, P., & Allen, J. S. (2007). Factors associated with performance on the educational testing service (ETS) major field achievement test in business (MFAT-B).Journal of Education for Business,82, 196–201.

Chowdhury, M., & Wheeling, B. (2013) Determinants of major field test (MFT) score for graduating seniors of a business school in a small mid-western university.Academy of Educational Leadership Journal, 17, 59–71.

The Citadel School of Business Administration Mentor Association. (2011).The Citadel school of business administration mentor associa-tion: Crossing the bridge. Retrieved from http://www.citadel.edu/ root/csb-clubs-organizations/48-academics/schools/business/badm/104-mentor-association

Contreras, S., Badua, F., Chen, J. S., & Adrian, M. (2011). Documenting and explaining major field test results among undergraduate students.

Journal of Education for Business,86, 64–70.

DeMong, R. F., Lindgren, J. H., & Perry, S. E. (1994). Designing an assessment program in accounting.Issues in Accounting Education,9, 11–27.

Educational Testing Service (ETS). (2011).Find out how to prove—And improve—The effectiveness of your business program with the ETS major field tests. Retrieved from http://www.ets.org/Media/Tests/MFT/ pdf/mft_testdesc_business_4cmf.pdf

Martell, K. (2007). Assessing student learning: Are business schools mak-ing the grade?Journal of Education for Business,82, 189–195. Mirchandani, D., Lynch, R., & Hamilton, D. (2001). Using the ETS major

field test in business: Implications for assessment.Journal of Education for Business,77, 51–56.

Render, B., Stair, R. M., & Hanna, M. E. (2009)Quantitative analysis for management(10th ed.). Upper Saddle River, NJ: Pearson Education, Inc.

Terry, N., Mills, L., & Sollosy, M. (2008). Student grade motivation as a determinant of performance on the Business Major Feld ETS exam.

Journal of College Teaching & Learning,5, 27–32.

White, B. (2007). Perspectives on program assessment: An introduction.

Journal of Education for Business,82, 187–188. 62 S. A. SIMMONS ET AL.