CORPORATE CONTROL AND FIRM PERFORMANCE: DOES THE TYPE OF OWNERS MATTER?

Teks penuh

Gambar

Dokumen terkait

Practical Implications: The study thus concluded that firm size had a buffering effect in the link between corporate diversification and the financial performance of

Findings – This study concludes that the implementation of corporate governance (board meeting and board size) in the non- financial sector, has a positive

The dependent variable in this research is CSR, while the independent variables are the ownership structure consisting of institutional ownership, managerial ownership and

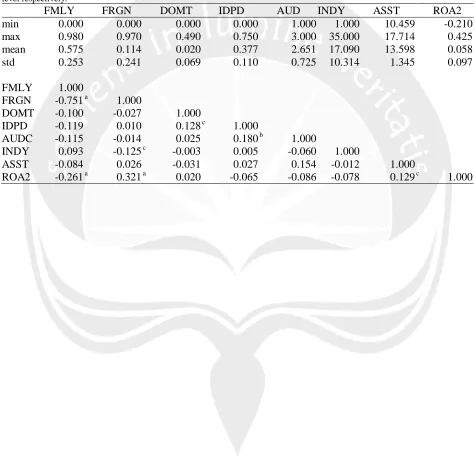

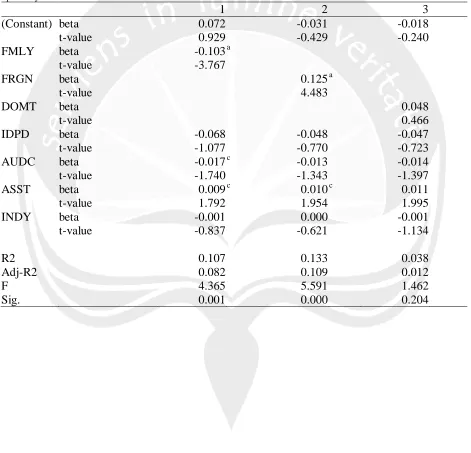

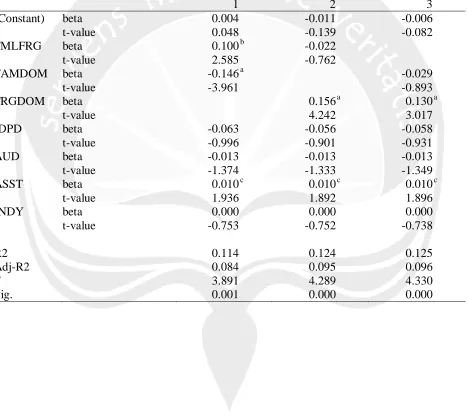

CONCLUSION From the test results it can be concluded that the variables of institutional ownership, family ownership, managerial ownership, founders on the board of directors, size of

Hypothesis Development: The direct and indirect effects of ownership concentration on board size We employ three measures of ownership concentration: The direct share ownership of

The test results in the Inmek research prove that institutional ownership has no effect on firm value, managerial ownership does not affect firm value, independent commissioners

The result implies that corporate social responsibility, corporate governance managerial ownership, independent commissioners, audit committees, and firm size may explain 64.9% of the

2011 27 banks from GCC countries except Kuwait from 2008 Dependent: Return on Assets ROA Independent: Block holders, Board Size, CEO Duality, Foreign ownership and