Linkage Investment Opportunity Set (IOS) with Financial Policy in Growing Companies in Indonesia Stock Exchange (BEI)

Teks penuh

Gambar

Dokumen terkait

medan, berasal dari daerah sub tropis sehingga akllil mengalami eekaman (stress) akihat perubahan suhu pemeliharaan, mab dicoba melakukan isolasi gen pcnyandi heat

Pembangunan Gedung Olahraga (Indoor) Serbaguna (FISIK), Lokasi : Palangka Raya sudah memasuki tahap Evaluasi Penawaran dan Evaluasi Kualifikasi dengan ini kami

Nyepi siaran kini bukan sekedar menjadi bentuk penghormatan lembaga penyiaran terhadap kearifan lokal masyarakat Hindu Bali tetapi juga bentuk implementasi dari upaya

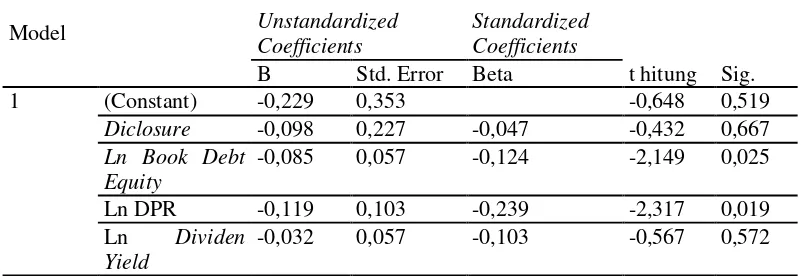

Untuk Tahun Yang Berakhir Tanggal 31 Desember

[r]

[r]

Metode penelitian yang digunakan dalam penelitian ini adalah metode eksperimen dengan metode pengambilan sampel adalah purposive sampling.. Teknik analisis data

Berdasarkan data yang di dapat pada Gambar 4a dan Gambar 4b ukuran panjang pesan sangat mempengaruhi berapa lama waktu komputasi yang dibutuhkan sistem untuk