maxi liesyaputra [email protected] +62 21 299 60 875 aZ researCH tOp piCKs: - ptpp - wton - jsmr

Strategy Report

Volatile IDr movementIDR has been cumulatively depreciating by 2.3% over a 2-month period up to 14 April 2015, exacerbated by the strengthening of the USD against major global currencies on the back of economic recovery in the U.S.A., accompanied by a lower BI rate. We believe that the Fed is not likely to increase the Fed rate in 2Q15 since the institution is very conservative in deciding rate movement, even though there is an estimate that the rate will reach 0.625% (median estimate) by the end of 2015.

Current IDR depreciation is different from the previous one, during the 2008 global crisis. Current IDR depreciation is not accompanied by any credit default swap (CDS) jump, unlike the IDR depreciation in 2008 which was followed by significant jump of CDS.

stable interest rate

We believe Bank Indonesia will maintain the benchmark rate of 7.50% in 2Q15 after lowering the rate in February 2015. The expectation is based on forecasted Indonesia’s inflation rate of 4.5-5% in 2015 and BI’s expectation to maintain IDR exchange rate against USD. In 2Q15, we expect inflation will be higher related to fuel price hike at end of March 2015, entering new education calendar and fasting month.

Low oil price phenomena

As demand relatively constant accompanied by increasing supply, world oil price shows tendency to decline. The new president Jokowi’s administration is benefited by the low oil price phenomena, which may allow the institution to reduce oil subsidy. Ron 88 premium oil subsidy has been revoked. The government only subsidizes diesel oil in certain amount per liter. At the end, the government will have room to reallocate the oil subsidy to infrastructure development, on the back of lack of infrastructure availability and quality in Indonesia. Beside using state budget, the government is also open for private sector participations in infrastructure development, since it needs a lot of fund. Therefore, the government’s efforts to attract both international and domestic investors are urgently required.

We believe that oil price will remain low in 2Q15 since there will not be any major demand improvement in that period.

society’s income increases

In 2009 – 2014 period, there was gradual improvement of Indonesia’s society disposable income. For range of more than USD5,000 up to USD7,500 per year (the largest portion), the percentage increased to 62.5% in 2014 from 54.6% in 2009. The same thing also happened for disposable income range of USD7,500 up to USD15,000 per year, the percentage improved to 41.1% in 2014 from 30.4% in 2009.

Benefited sectors in 2Q15

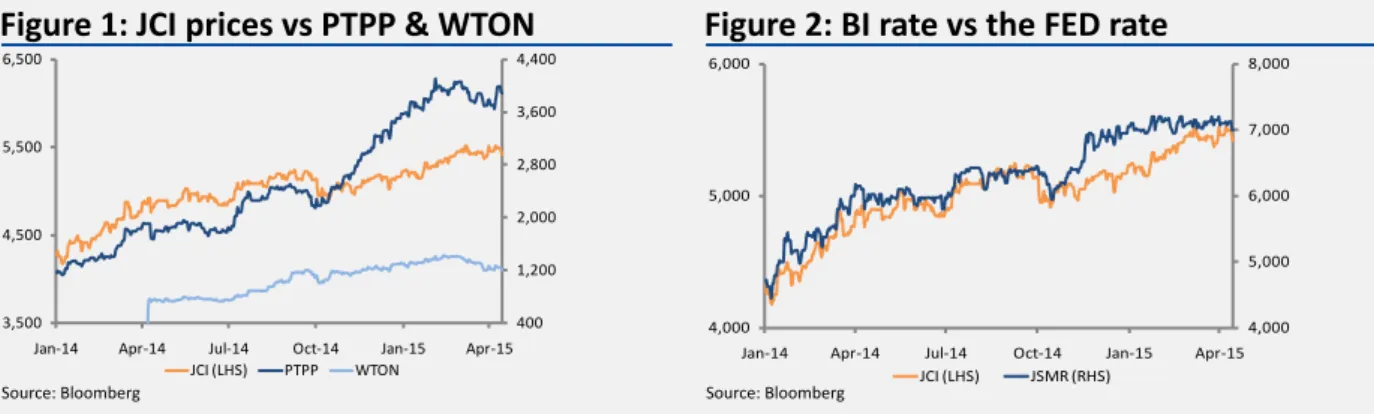

We favor some sectors which are resilient or not negatively impacted by the explained situation above. The sectors are construction (PTPP, WTON) and infrastructure (JSMR). Those three companies do not have USD debt. Pay atten-tion to those companies which large debt exposure in USD, i.e. ISAT, ASRI, MSKY and EXCL. We do not favor sectors with much USD exposure in their costs, i.e. consumer, poultry, media and retailer.

Source: Bloomberg

Figure 3: IDr vs regional currencies

Source: Bloomberg 50.0 250.0 450.0 650.0 850.0 1,050.0 1,250.0 1,450.0 1,000.0 3,000.0 5,000.0 7,000.0 9,000.0 11,000.0 13,000.0 15,000.0 4/ 8/ 20 05 4/ 8/ 20 06 4/ 8/ 20 07 4/ 8/ 20 08 4/ 8/ 20 09 4/ 8/ 20 10 4/ 8/ 20 11 4/ 8/ 20 12 4/ 8/ 20 13 4/ 8/ 20 14 IDR/USD IDR/USD CDS -10% -5% 0% 5% 10% 15% 20%Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 IDR Yen RMB Sing Dollar Ringgit Mly Thai bath

Figure 4: IDr vs CDs

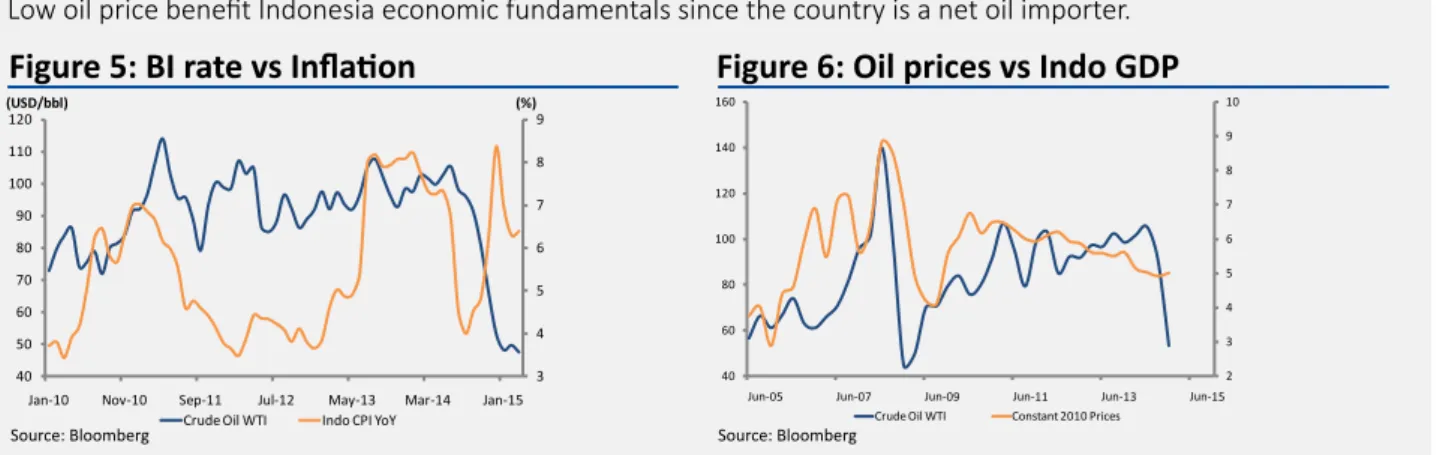

Source: BloombergFigure 5: BI rate vs Inflation

3 4 5 6 7 8 9 5.5 6.5 7.5 8.5Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 BI Rate Inflation Rate

Source: Bloomberg

Figure 6: BI rate vs the FED rate

0 2 4 6 8 10 12 14 0 1 2 3 4 5 6Fed rate (LHS) BI rate (RHS)

IDr movement compared to other currencies

We see that IDR depreciation against USD is in the middle among regional currencies. IDR depreciation is not fol-lowed by CDS hike in 2015, unlike the currency’s depreciation in 2008.

Source: Bloomberg

Figure 1: jCI prices vs ptpp & wton

Source: BloombergFigure 2: BI rate vs the FED rate

400 1,200 2,000 2,800 3,600 4,400 3,500 4,500 5,500 6,500Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 JCI (LHS) PTPP WTON 4,000 5,000 6,000 7,000 8,000 4,000 5,000 6,000

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 JCI (LHS) JSMR (RHS)

Indonesia economic indicators

With manageable inflation of between 4.5-5.0% in 2015, we expect Indonesia will reach economic growth of 5.3% in the same period, higher than 5.02% in 2014.

BI rate compared to Fed rate

We expect there will be no change both in the Fed rate and BI rate in 2Q15.

Low oil price benefit Indonesia economic fundamentals since the country is a net oil importer.

Source: Bloomberg

Figure 5: BI rate vs Inflation

Source: BloombergFigure 6: oil prices vs Indo GDp

3 4 5 6 7 8 9 40 50 60 70 80 90 100 110 120Jan-10 Nov-10 Sep-11 Jul-12 May-13 Mar-14 Jan-15 (%) (USD/bbl)

Crude Oil WTI Indo CPI YoY

2 3 4 5 6 7 8 9 10 40 60 80 100 120 140 160

Crude Oil WTI Constant 2010 Prices

Source: Bloomberg, Sucorinvest

Figure 7: macro economic assumptions

Source: BloombergFigure 8: jCI pBV band for the last five years

-1 ST.Dev Mean +1 ST.Dev -2 ST. Dev +2 ST. Dev 1.5 2.0 2.5 3.0Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Desc (%) 2012 2013 2014 2015F

Inflation 4.30 8.38 8.36 5.00

GDP growth 6.26 5.78 5.02 5.30

BI rate 5.75 7.50 7.75 7.50

Improving income

There is increasing portion of Indonesia’s disposable income of more than USD5,000 per year as a result of continu-ing domestic economic growth.

Consumer confidence index (CCI)

CCI shows tendency to increase since 1Q14 supported by potential economic growth in years ahead.

Figure 9: Indonesian income class

Figure 10: Indonesia CCI

31 41 51 61 90 100 110 120 130Source: Company

Figure 11: net foreign flow

-10 0 10 20 30 40 50 60 70Jan-14 Apr-14 Jul-14 Oct-14 Jan-15

(I D R tn ) net foreign inflow

Since the beginning of 2015, net foreign has increasing tendency on the back of their trust in Indonesian economic growth.

Conclusions

From explained situation above, we believe that defensive stocks with minimum cost or debt exposure in USD will be our top picks. We select construction sector (PTPP, WTON) and infrastructure (JSMR) as our selected picks. Those three companies do not have USD debt. Pay attention to those companies which large debt exposure in USD, i.e. ISAT, ASRI, MSKY and EXCL. We do not favor sectors with much USD exposure in their costs, i.e. consumer, poultry, media and retailer.

sucorinvest, rating definition, analysts certification, and important disclosure ratings for sectors

Overweight : We expect the industry to perform better than the primary market index (JCI) over the next 12 months. Neutral : We expect the industry to perform in line with the primary market index (JCI) over the next 12 months.

Underweight : We expect the industry to underperform the primary market index (JCI) over the next 12 months.

ratings for stocks

Buy : We expect this stock to give return (excluding dividend) of above 10% over the next 12 months.

Hold : We expect this stock to give return of between -10% and 10% over the next 12 months.

Sell : We expect this stock to give return of -10% or lower over the next 12 months.

Analyst Certification

The research analyst(s) primarily responsible for the preparation of this research report hereby certify that all of the views expressed in this research report accurately reflect their personal views about any and all of the subject securities or issuers. The research analyst(s) also certify that no part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this research report.

Disclaimers

This document has been prepared for general circulation based on information obtained from sources be-lieved to be reliable but we do not make any representations as to its accuracy or completeness. PT Sucor-invest Central Gani accepts no liability whatsoever for any direct or consequential loss arising from any use of this document or any solicitations of an offer to buy or sell any securities. PT Sucorinvest Central Gani and its directors, officials and/or employees may have positions in, and may effect transactions in securi-ties mentioned herein from time to time in the open market or otherwise, and may receive brokerage fees or act as principal or agent in dealings with respect to these companies. PT Sucorinvest Central Gani may also seek investment banking business with companies covered in its research reports. As a result inves-tors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Sales office & research

PT Sucorinvest Central Gani

HEAD oFFICE

PT. Sucorinvest Central Gani Equity Tower, 31st Floor Jl. Jend Sudirman Kav. 52-53 Jakarta 12190 – Indonesia Ph : (+62-21) 2996 0999 Fax : (+62-21) 5797 3938

jAKArtA

Equity Tower, 31st Floor Jl. Jend Sudirman Kav. 52-53 Jakarta 12190 – Indonesia Ph : (+62-21) 2996 0999 Fax : (+62-21) 5797 3938 Ruko Pluit Village (Mega Mall Pluit) no. 30

Jl. Pluit Indah Raya, Jakarta Utara 14450

Ph: (+62-21) 6660 7599 (+62-21) 6660 7607 Fax: (+62-21) 6660 7610 Ruko Mangga Dua Square Blok F no. 39

Jl. Gunung Sahari Raya, Jakarta Utara 14420 Ph: (+62-21) 2961 8899 Fax: (+62-21) 2938 3525 Wisma 77 Lt.17 Jl. Letjend S. Parman Jakarta Barat 11410 Ph: (+62-21) 536 3033 Fax: (+62-21) 5366 2966 Ruko Inkopal Block A No. 23 A Jl. Boulevard Barat Raya Jakarta Utara 14240 Ph: (+62-21) 4585 9114 Fax: (+62-21) 4585 9227 Ruko Puri Niaga 1 Blok K7 / 3T Jl. Puri Kencana Jakarta Barat 14240 Ph: (+62-21) 582 3117 Fax: (+62-21) 582 3118 GALERI INVESTASI Universitas PANCASILA Jl. Srengseng Sawah, Lenteng Agung, Jakarta Selatan 12640 Ph: (+62-21) 787 3711 GALERI INVESTASI Universitas Krisnadwipayana Jl. Raya Jatiwaringin, Pondok Gede Jakarta Timur 13620 Kiosk Mall Ambassador Lantai Dasar Blok H No.3A Jl. Professor Doktor Satrio Jakar-ta SelaJakar-tan 12940

GALERI INVESTASI Univesitas Islam 45 Bekasi Jl. Cut Meutia NO.83, Bekasi 17113

tAnGErAnG

Ruko PDA No.9

Jl.Raya Boulevard Gading Serpong

Tangerang 15810. Ph : (+62-21) 54210990 GALERI INVESTASI Surya University

Gedung 01 Scientia Business Park

Jl. Boulevard Gading Serpong Blok O/1 Summarecon Serpong Tangerang 15810

BoGor

Komplek Ruko V Point Jl. Pajajaran Blok ZG, Bogor 16144

Ph: (+62-251) 835 8036 Fax: (+62-251) 835 8037

GALERI INVESTASI STIE Kesatuan Bogor Jl. Ranggagading No.1 Bogor 16123

Ph : (+62-251) 835 8036

BAnDUnG

Ruko Paskal Hyper Square Blok B No.47

Jl. Pasir Kaliki No. 25 - 27 Bandung 40181 Ph: (+62-22) 8778 6206 Fax: (+62-22) 8606 0653 JL.Hegarmanah No.57 Bandung 40141 Ph: (+62-22)-203 3065 Fax: (+62-22) 203 2809 YoGYAKArtA Jl. Poncowinatan No. 94 Yogyakarta 55231 Ph: (+62-274) 580 111 Fax: (+62-274) 580 111 GALERY INVESTASI Universitas Ahmad Dahlan Lab kompt FE Lt-2 kampus 1 Universitas Ahmad Dahlan Jl. Kapas no 9, Semaki, Umbul-hardjo, Yogyakarta 55166 Ph: (+62-274) 71 700 48

mALAnG

Jl. Jaksa Agung Suprapto No.40 Kav. B4, Malang 68416 Ph: (+62-341) 346 900 Fax: (+62-341) 346 928 GALERI INVESTASI UNIVERSITAS MERDEKA Jl. Terusan Dieng No.59, Malang 65146

Ph: (+62-341) 580 900

KEDIrI

GALERI INVESTASI

UNIVERSITAS NUSANTARA PGRI Jl. KH Ahmad Dahlan 76, Kediri 64112 Ph : (+62-354) 7417352 suraBaya Jl. Trunojoyo no.67 Surabaya 60264 Ph: (+62-31) 563 3720 Fax: (+62-31) 563 3710 Jl. Slamet no. 37 Surabaya 60272 Ph : (+62-31) 547 9252 Fax : (+62-31) 547 0598 Ruko Pakuwon Town Square AA2-50

Jl. Kejawen Putih Mutiara, Surabaya 60112

Ph: (+62-31) 5825 3448 Fax: (+62-31) 5825 3449 GALERI INVESTASI Universitas Negeri Surabaya PIC : Wahyudi Maksum Kampus ketintang

Gedung bisnis centre fakultas ekonomi Jl. Ketintang, Surabaya 60231 Ph: (+62-31) 8297123 GALERI INVESTASI Universitas 17 Agustus 1945 Jl. Semolowaru 45 Surabaya 60118 Bali

Jl. Raya Puputan Renon No.60C, Denpasar 80226

Ph : (+62-361) 261 131 Fax: (+62-361) 261 132

research Email

1. Maxi Liesyaputra Head of Research [email protected]

2. Andy Wibowo Gunawan Equity Analyst [email protected]

3. Vasthi Juwita Permata E Equity Analyst [email protected]

4. Inav Haria Chandra Equity Analyst [email protected]