1 rtment of Higher Education as a Private Higher Education Institution under the Higher Education Act,

1997. Registration Certificate No. 2000/HE07/008

AC U L T Y O F B U S I N E S S ,

EC O N O M I C S &

A N A G EM EN T S C IEN C ES

Q U A L I F I C A T I O N T I T L E : B A C H EL O R O F C O M M ER C E

L E A R N E R G U I D E

S : M A R K E T I N G M A N A G E M E N T 5 1 1 ( 1 S T S E M E S T E R )

PREPARED ON BEHALF OF

NI N G & B U S I N E S S C O L L E G E (P T Y ) L T D U TH O R : D r . L a w r e n c e L e k h a n y a

I T O R : Mr . S i m b r a s h e M a g w a g w a

C U L T Y HE A D : P r o f . R o s h M a h a r a j

C o p y r i g h t © 2 0 1 3

T r a i n i n g & B u s i n e s s C o l l e g e (P t y ) L t d e g i s t r a t i o n N u m b e r : 2 0 0 0 / 0 0 0 7 5 7 / 0 7

rved; no part of this publication may be reproduced in r by any means, including photocopying machines, out the written permission of the Institution.

BUSINESS ADMINISTRATION, MANAGEMENT &

COMMERCIAL SCIENCES

ACCOUNTING 511

2

Previously

BUSINESS ADMINISTRATION, MANAGEMENT

& COMMERCIAL SCIENCES

STUDY GUIDE

MODULE: ACCOUNTING 511

(1

stSEMESTER)

Copyright © 2017

Richfield Graduate Institute of Technology (Pty) Ltd Registration Number: 2000/000757/07

3

6. Lectures and Tutorials 8

7. Notices 8

8. Prescribed & Recommended Material 8

9. Assessment & Key Concepts in Assignments and Examinations 10

10.Specimen Assignment Cover Sheet 12

11.Work Readiness Programme 13

12.Work Integrated Learning 14

ACCOUNTING 511 (1ST SEMESTER)

TOPIC 1: THE NATURE AND PURPOSE OF BOOKKEEPING AND ACOUNTING

1.1 Introduction 20

1.2 What Is Bookkeeping And What Is Accounting? 21

1.3 The Purpose of Accounting 22

1.4 Nature of accounting 22

1.5 Why Study Accounting? 23

1.6 The Functions of Accounting 24

1.7 Developments In Accounting 25

1.8 Generally Accepted Accounting Practice (GAAP) 27

1.9 Approach To Setting Accounting Standards 28

1.10 Types of Business Organisations 29

1.11 The Purpose, Status And Scope Of The Accounting Framework

39

1.12 The Nature Of And The Need For Financial Information 40

1.13 The objectives of financial statements 41

1.14 Financial Performance, Changes In Equity, Financial Position And Statement Of Cash Flows

42

1.15 Accounting principles 44

1.16 Accounting policy 52

1.17 Disclosure of Accounting policy 53

1.1.8 Generally accepted accounting practise (GAAP) 53

1.19 Elements of Financial Statements 54

1.20 The accounting equation 55

1.21 Qualitative characteristics of financial statements 57

Assessment Questions 59

TOPIC 2: THE DOUBLE ENTRY SYSTEM

4

2.2 The Accounting Equation 65

2.3 The effect of transactions on the basic accounting equation 65

Assessment Questions 69

TOPIC 3: THE ACCOUNTING CYCLE

3.1 Definition-Accounting Cycle 70

3.2 Source Documents 71

3.3 Books of First Entry(Journals) 72

3.4 Ledgers 75

3.5 Control Accounts 76

3.6 The Trial Balance 77

3.7 Compilation of Financial Statements 109

Assessment Questions 112

TOPIC 4: THE BASIC ASPECTS OF FINANCIAL STATEMENTS

4.1 Accounting Entity 114

4.2 Grouping of items in a business 114

4.3 Financial Position 116

4.4 The Financial Result 122

Assessment Questions 124

TOPIC 5: ADJUSTMENTS

5.1 Introduction 126

5.2 Five Steps Relating to Adjustments 127

5.3 Short-term Adjustments 127

5.4 Long-term Adjustments 134

5.5 Methods of Depreciation 135

5.6 Accounting Entries for Depreciation 137

5.7 The Trial Balance 137

Assessment Questions 138

TOPIC 6:CASH AND CASH EQUIVALENTS

6.1 Introduction 139

6.2 Bank Reconciliation Statement 140

6.3 The Petty Cash Journal 144

Assessment Questions 145

TOPIC 7: TRADE RECEIVABLES

7.1 Introduction 149

7.2 Settlement Discount Granted 149

7.3 Interest Charged 150

7.4 Credit Losses 150

7.5 Allowance for Credit Losses 151

7.6 Recording Allowances For Credit Losses 151

7.7 Recovery of Credit Losses Written Off 155

7.8 Debtors Control Account 155

5

8.1 Introduction 157

8.2 Cost Formulae 157

8.3 The Importance of Correct Inventory Valuation 160

TOPIC 9: NON-CURRENT ASSETS

9.1 Tangible Assets 161

9.2 Scrapping Of Alienation Of Assets 165

9.3 Scrapping An Asset Without Alienation 166

9.4 Sale Of An Asset 166

9.5 Trading In Of Assets 170

9.6 Other Non- Current Assets 171

Assessment Questions 174

TOPIC 10: LIABILITIES

10.1 Trade Creditors 177

10.2 Bills Payable 178

10.3 Other Arrears Or Accumulated Obligations 178

10.4 Creditors Control Account 178

10.5 Non- Current Liabilities 180

Assessment Questions 181

TOPIC 12: SOLE PROPRIETORSHIP

11.1 Introduction 182

11.2 Equity in the Entity 182

11.2 Drawings 183

11.3 Statement of Changes in Equity 183

Assessment Questions 184

TOPIC 12: NON – PROFIT ORGANISATION .

12.1 Introduction 184

12.2 What are the major differences between non-profit and

for-profit accounting?

184

Assessment Questions 194

TOPIC 13:ADDENDUM 511(A) : REVISION QUESTIONS 195

6

PREFACE

1.WELCOME

Welcome to the Faculty of Business, Economics & Management Sciences at Richfield Graduate Institute of Technology (Pty) Ltd. We trust you will find the contents and learning outcomes of this module both interesting and insightful as you begin your academic journey and eventually your career in the business world.

This section of the study guide is intended to orientate you to the module before the commencement of formal lectures.

Please note that this study guide covers the content of various academic programmes at different levels of the NQF. Your lecturers will provide further guidance and additional study materials covering parts of the syllabi that may have been omitted from this study guide. Students who are undertaking this qualification may use the non-compulsory material supplied as additional reading. This will however not be directly examinable.

The following lectures will focus on the common study units described:

WELCOME & ORIENTATION

Study unit 1: Orientation Programme

Introducing academic staff to the students by academic head. Introduction of institution policies.

Lecture 1

Study unit 2: Orientation of Students to Library and Students Facilities

Introducing students to physical structures

Lecture 2

Study unit 3: Distribution and Orientation of Accounting

511Study guide s, Textbooks and Prescribed Materials Lecture 3

Study unit 4: Discussion on the Objectives and Outcomes of

Accounting 511 Lecture 4

Study unit 5: Orientation and guidelines to completing Assignments

Review and Recap of Study units 1-4

7

2.TITLE OF MODULES, COURSE, CODE, NQF LEVEL, CREDITS & MODE OF DELIVERY

3.PURPOSE OF MODULE

3.1 Accounting 511 ( 1st Semester)

The purpose of this module is to equip students with knowledge of accounting and the skills to apply the acquired knowledge. Students will be taught the theoretical and conceptual approaches to accounting as well as the informational and reporting functions of accounting.

4. LEARNING OUTCOMES

On completion of this module, students should have a basic / fundamental practical and theoretical knowledge of:

The Nature and Purpose of Accounting

The Functions of Accounting

The Nature of Accounting Theory

The Financial Position and the Financial Result of an Enterprise

The Double Entry System

The Accounting Cycle

Inventory Systems

Adjustments

The Bank Reconciliation and Petty Cash Journal

5. METHOD OF STUDY

The sections that have to be studied are indicated under each topic. These form the basis for tests, assignments and examination. To be able to do the activities and assignments for this module, and to achieve the learning outcomes and ultimately to be successful in the tests and examination, you will need an in-depth understanding of the content of these sections in the learning guide and prescribed book. In order to master the learning material, you must accept responsibility for your own studies.

8

6. LECTURES AND TUTORIALS

Students must refer to the notice boards on their respective campuses for details of the lecture and tutorial time tables. The lecturer assigned to the module will also inform you of the number of lecture periods and tutorials allocated to a particular module. Prior preparation is required for each lecture and tutorial. Students are encouraged to actively participate in lectures and tutorials in order to ensure success in tests, assignments and examinations.

7. NOTICES

All information pertaining to this module such as tests dates, lecture and tutorial time tables, assignments, examinations etc. will be displayed on the notice board located on your campus. Students must check the notice board on a daily basis. Should you require any clarity, please consult your lecturer, or programme manager, or administrator on your respective campus.

8. PRESCRIBED & RECOMMENDED MATERIAL

8.1 Prescribed material

Berry, P.R., de Klerk, E.S., Doussy, F., Ngcobo, R.N., Rehwinkel, A., Scheepers, D. and Scott, D. 5th ed. Vol. 1. 2014. About Financial Accounting. Durban:

LexisNexis.

8.2 Recommended Material

Myburgh, J.E., Founche, J.P. and Cloete, M. 11th ed. 2013, Accounting: An

Introduction. Durban: LexisNexis.

Kew, J., Mettler, C., Walker, T. and Watson, A. 4th ed. 2013. Accounting: an

Introduction. Cape Town: Oxford.

8.3 Library Infrastructure

The following services are available to you:

8.3.1 Each campus keeps a limited quantity of the recommended reading titles and a larger variety of similar titles which you may borrow. Please note that students are required to purchase the prescribed materials.

9

8.3.3 RGI has also allocated one library period per week as to assist you with your formal research under professional supervision.

8.3.4 RGI has dedicated electronic libraries for use by its students. The computers laboratories, when not in use for academic purposes, may also be used for research purposes. Booking is essential for all electronic library usage.

9 ASSESSMENT

Final Assessment for this module will comprise two Continuous Assessment tests, an assignment and an examination. Your lecturer will inform you of the dates, times and the venues for each of these. You may also refer to the notice board on your campus or the Academic Calendar which is displayed in all lecture rooms.

9.1Continuous Assessment Tests

There are two compulsory tests for each module (in each semester).

9.2. Assignment

There is one compulsory assignment for each module in each semester. Your lecturer will inform you of the Assessment questions at the commencement of this module.

9.3Examination

There is one two hour examination for each module. Make sure that you diarize the correct date, time and venue. The examinations department will notify you of your results once all administrative matters are cleared and fees are paid up.

The examination may consist of multiple choice questions, short questions and essay type questions. This requires you to be thoroughly prepared as all the content matter of lectures, tutorials, all references to the prescribed text and any other additional documentation/reference materials is examinable in both your tests and the examinations.

10

9.4Final Assessment

The final assessment for this module will be weighted as follows:

Continuous Assessment Test 1

Continuous Assessment Test 2 40% Assignment 1

Examination 60%

Total 100%

9.5Key Concepts in Assignments and Examinations

In assignment and examination questions you will notice certain key concepts (i.e. words/verbs) which tell you what is expected of you. For example, you may be asked in a question to list, describe, illustrate, demonstrate, compare, construct, relate, criticize, recommend or design particular information / aspects / factors /situations. To help you to know exactly what these key concepts or verbs mean so that you will know exactly what is expected of you, we present the following taxonomy by Bloom, explaining the concepts and stating the level of cognitive thinking that theses refer to.

Competence Skills Demonstrated

Knowledge

observation and recall of information knowledge of dates, events, places knowledge of major ideas

mastery of subject matter

Question Cues

list, define, tell, describe, identify, show, label, collect, examine, tabulate, quote, name, who, when, where, etc.

Comprehension

understanding information grasp meaning

translate knowledge into new context interpret facts, compare, contrast order, group, infer causes

predict consequences

Question

Cues

11

Application

use information

use methods, concepts, theories in new situations solve problems using required skills or knowledge

Questions

Cues

apply, demonstrate, calculate, complete, illustrate, show, solve, examine, modify, relate, change, classify, experiment, discover

analyze, separate, order, explain, connect, classify, arrange, divide, compare, select, explain, infer

Synthesis

use old ideas to create new ones generalize from given facts

relate knowledge from several areas predict, draw conclusions

Question Cues

combine, integrate, modify, rearrange, substitute, plan, create, design, invent, what if?, compose, formulate, prepare, generalize, rewrite

Evaluation

compare and discriminate between ideas assess value of theories, presentations make choices based on reasoned argument verify value of evidence recognize subjectivity

Question Cues

12

BUSINESS ADMINISTRATION, MANAGEMENT & COMMERCIAL SCIENCES

ACCOUNTING ASSIGNMENT COVER SHEET

1ST SEMESTER ASSIGNMENT

Name & Surname: ____________________________________________ ICAS No: _________________

Qualification: ______________________ Semester: _____ Module Name: __________________________

Specialization: _____________________ Date Submitted: ___________

QUESTION NUMBER MARK ALLOCATION EXAMINER MARKS MODERATOR MARKS

TOTAL

E a i e s Co e ts:

Mode ato s Co e ts:

Signature of Examiner: Signature of Moderator:

The purpose of an assignment is to ensure that the Student is able to:

Demonstrate an understanding of accounting principles.

Systematically record the financial aspects of business transactions.

Prepare financial statements to know the result of business operations for a particular period of time.

To meet the financial information needs of the decision-makers and help them in rational decision-making.

Report the results and position of business to Use s of fi a ial state e ts.

P ese ti g t ue a d fai ie of fi a ial t a sa tio s.

13

End –User Computing (if not included in your curriculum)

The illustration below outlines some of the key concepts for Work Readiness that will be included in your timetable.

It is in your interest to attend these workshops, complete the Work Readiness Log Book and prepare for the Working World.

14

11. WORK INTEGRATED LEARNING (WIL)

Work Integrated Learning forms a core component of the curriculum for the completion of this programme. All modules which form part of this qualification will be assessed in an integrated manner towards the end of the programme or after completion of all other modules. Prerequisites for placement with employers will include:

Completion of all tests & assignment

Success in examination

Payment of all arrear fees

Return of library books, etc.

Completion of the Work Readiness Programme.

Students will be fully inducted on the Work Integrated Learning Module, the Workbooks & assessment requirements before placement with employers.

15

Good luck and success in your studies…

Registered with the Department of Higher Education as a Private Higher Education Institution under the Higher Education Act, 1997. Registration Certificate No. 2000/HE07/008

BUSINESS ADMINISTRATION, MANAGEMENT &

COMMERCIAL SCIENCES

STUDY GUIDE

MODULE: ACCOUNTING 511 (1st SEMESTER)

TOPIC1: THE NATURE, FUNCTIONS AND PURPOSE OF BOOKKEEPING AND ACOUNTING

TOPIC 2: DOUBLE ENTRY SYSTEM TOPIC 3: THE ACCOUNTING CYCLE

TOPIC 4: THE BASIC ASPECTS OF FINANCIAL STATEMENTS TOPIC 5: ADJUSTMENTS

TOPIC 6: CASH AND CASH EQUIVALENTS TOPIC 7: TRADE RECEIVABLES

TOPIC 8: INVENTORY

TOPIC 9: NON-CURRENT ASSETS TOPIC 10: LIABILITIES

TOPIC 11: THE SOLE PROPRIETORSHIP TOPIC 12: NON-PROFIT ORGANISATIONS

TOPIC 13: ADDENDUM 511(A): REVISION QUESTIONS

16

TOPICS

TOPIC 1: THE NATURE AND PURPOSE OF BOOKKEEPING AND ACOUNTING

Introduction

Lecture 6

What Is Bookkeeping And What Is Accounting? Why Study Accounting?

Developments In Accounting

Generally Accepted Accounting Practice (GAAP) Approach To Setting Accounting Standards

The Nature Of And The Need For Financial Information Users Of Financial Information

The objectives of financial statements

Lecture 10-12

Financial Performance, Changes In Equity, Financial Position And Statement Of Cash Flows

The Purpose of Accounting Terminology

The Nature of Accounting 13-16

Accounting principles Accounting Policy

Disclosure Of Accounting Policy

Generally Accepted Accounting Practice (GAAP) Underlying Assumptions

Qualitative Characteristics of Financial Statements The Function of Accounting

Lecture 17

Users of Accounting Information

TOPIC 2: THE DOUBLE ENTRY SYSTEM

The Double Entry System

Lecture 18-22

The Accounting Equation

The Effect of Transactions On The Basic Accounting Equation

TOPIC 3: THE ACCOUNTING CYCLE

Definition – Accounting Cycle

Source Documents Lecture

17

Accounting Entity

Lecture 25-27

Grouping of Items In A Business Financial Position

Allowance for Credit Losses Lecture 33-34

Recording Allowances For Credit Losses Recovery of Credit Losses Written Off Debtors Control Account

TOPIC 8: INVENTORY

Introduction Lecture

35-36

Cost Formulae

The Importance of Correct Inventory Valuation

TOPIC 9: NON-CURRENT ASSETS

Tangible Assets Lecture

37-38

Depreciation

Scrapping Of Alienation Of Assets

Scrapping An Asset Without Alienation Lecture 39

Sale Of An Asset Trading In Of Assets

18

TOPIC 10: LIABILITIES

Trade Creditors Lecture

42 - 43

Bills Payable

Other Arrears Or Accumulated Obligations Creditors Control Account

Non – Current Liabilities

TOPIC 11: THE SOLE PROPRIETORSHIP

Introduction Lecture

44 - 45

Equity in the Entity Drawings

Statement of Changes in Equity

TOPIC 12: NON – PROFIT ORGANISATION .

Introduction Lecture

46 - 47

What are major differences between non-profit and profit organisation

Income and expenditure statement

TOPIC 13: ADDENDUM 511 (A): REVISION QUESTIONS Lecture 48

TOPIC 14: ADDENDUM 511 (B): TYPICAL EXAMINATION

QUESTIONS

19 The following are guide icons that will be used throughout this Study guide :

INTERACTIVE ICONS USED IN STUDY GUIDE S

Learning Outcomes Study Read Writing Activity

Think Point Research Glossary Key Point

Review Questions

Case Study Bright Idea Problem(s)

Multimedia Resource

20

TOPIC 1

_____________________________________________________________ 1. THE NATURE, PURPOSE AND FUNCTIONS OF BOOKKEEPING AND

ACOUNTING

______________________________________________________________

Learning Outcomes:

The purpose of topic one is to explain the nature, objectives and functions of accounting and bookkeeping, the processes by means of which this information is generated and who the users of the financial information are.

After studying this topic, you will know the types of information generated by accounting and how they meet the information needs of the various users of financial information. This knowledge is a prerequisite for studying the theory and practice of accounting, which follows hereafter. You require this knowledge in order to keep your study focused on the objectives of accounting.

1.1 INTRODUCTION

21

Institute of Chartered Accountants (SAICA) after approval by the Accounting Practice Board (APB) and having adopted the framework for the preparation and presentation of financial statements issued by the International Accounting Standards

The purpose of this chapter is to explain the function and objectives of accounting and the need for financial information, which the users of financial information require and how this information is generated and communicated to the users thereof.

1.2 WHAT IS BOOKKEEPING AND WHAT IS ACCOUNTING?

The above definition indicates that accounting must fulfil the following requirements:

the orderly and systematic recording; the monetary value and economic transactions of

economic transaction of

the monetary values of

an individual person or institutions (entity);

the reporting on the results of these transactions; and

the provision of the information in financial statements,

which information is used as a basis for decision-making by the users of the information.

Bookkeeping involves the identification and recording of economics events

only; therefore it is just one part of the accounting process.

Accounting can be defined as the orderly and systematically identification

and recording of the monetary values of the economic transactions of an individual entrepreneur (person) or a business enterprise (entity or

institution), the reporting on the results of these transactions, and the

22

For additional information on definition of Accounting, read pages: 3 – 6 from the prescribed textbook.

1.3 THE PURPOSE OF ACCOUNTING

The primary aim of the accounting process is to give a REPORT of the financial results of a business for a particular period of time and the financial position at a particular point in time. Accounting is the process where transactions are recorded in an Orderly and systematic manner.

A TRANSACTION is the agreement between two parties where the one sells something to another or renders a service that can be expressed in terms of money. The purpose of recording these transactions is to determine the exact financial state of the business at all times.

To do this he will need the following information:

How much does he owe other people;

How much do other people owe him;

The value and nature of his possessions in the business;

The nature and the amount of expenses for a period;

The nature and amount of all income for a period;

The profit/loss of the period;

The amount of his interest in the business (his capital investments);

The actual financial position of the business (possession as opposed to debts of the business)

1.4 THE NATURE OF ACCOUNTING

The main aim of any business today is for the owner to make a profit.

23

Therefore, because the owner wanted to know more it created a need for financial information.

This is the main aim of accounting – to provide the necessary – FINANCIAL INFORMATION

1.5 WHY STUDY ACCOUNTING?

Knowledge of accounting is needed on two levels:

By the users of financial information, and

By the preparers of financial information

All users of financial information need not be trained accountants. Anyone who has to make financial decisions, based on information disclosed by the accounting process should, however, at least have basic knowledge of accounting .The decision-maker must have an understanding of the information disclosed in the financial statement in order to make proper decisions. The more complex the information on which the decision is to be based, the greater the required knowledge of accounting. Knowledge of accounting will also enable any individual to manage his or her personal financial affairs more effectively.

The preparer of financial information, i.e. the accountant who accepts

responsibility for the design of accounting systems, the processing of financial information in the accounting process and the preparation and interpretation of financial reports, requires a profound knowledge of the theory and practice of the subject.

In addition, a wide variety of career opportunities exist for those with

accounting training. The accounting profession enjoys a high level of prestige in society and provides a great deal job satisfaction and security. The accountant, in the performance of normal responsibilities acquires a thorough insight into all the aspects of the activities of a business. An accounting qualification is an excellent entry opportunity into the business world

On obtaining an accounting qualification, the accountant has a variety of career opportunities:

In public practice, which mainly consists of:

Auditing (trainee accountants following the training-in-practice route)

Accounting services

Management consultation services;

24

manager, as well as a trainee accountant following the training-outside-practice route;

In the public sector as a government auditor, financial or management accountant or internal auditor, and

In academic spheres, where a great demand exists for trained accountants with a disposition for education and research.

1.6 THE FUNCTION OF ACCOUNTING

The function of accounting is to provide financial information to all interested parties on the result of the economic activities of a particular individual or institution (entity). Financial information that can be reported on in particular can be expressed in monetary terms (money values).

Economic activities include all activities (transactions) that use or consume resources (assets) to create new value. A person performs economic activities by working and earning a salary. The income from this salary is added to the assets of the person at the moment that person earns the income. The increased assets are now available for use by that person.

A trading entity purchases merchandise which is sold at a price higher than the purchase price plus other related costs. The difference between the purchase price and costs on the one hand, the higher selling price on the other, is called a profit. The proceeds from the profit increase the assets of the entity and are available for use.

The financial results of economic activities therefore have two aspects:

The value added to the net worth of a person or an entity during a particular period, and

The accumulated net worth of that person or entity.

Information about the financial results of an entity is provided in a complete set of financial statements. In terms of paragraph 10 of IAS 1 (AC101), a complete set of financial statements must consist of:

A statement of financial position as at the of period;

A statement of comprehensive income for the period;

A statement of changes in equity for the period;

A statement of cash flows for the period;

25

Paragraphs 20 and 21 of the framework explain the interrelationships between the various statements and the role of the notes and supplementary schedules to the statements. A single statement may not be enough to fulfil all the needs of a user of the information since information about one transaction may be included in different statements. For example, the information disclosed on the statement of comprehensive income may give an incomplete picture of the

e tit s pe fo a e a d the i fo atio i the otes o s hedules a e (Framework .21.). It would be necessary to make a study of the complete set of financial statements before a decision can be made.

1.7 DEVELOPMENTS IN ACCOUNTING

Accounting had been developed over many centuries as a result of the need to account for assets entrusted to people and/or entities who have the responsibility of dealing with these assets in a particular manner. It is expected that the person to whom the assets have been entrusted, i.e. the entrepreneur, will give account of the financial results regarding the economic application of those assets, to the suppliers thereof. In the early days, financial transactions were recorded by hand. In many cases, this still happens. It is only during the last century that technology has improved to such an extent that hand-written records are being replaced by computerised systems.

26

In the rest of Europe, the first works on double-entry bookkeeping appeared towards the middle of the sixteenth century: in Antwerp in 1543, in London in 1547, and in Germany in 1549.The early literature mainly described the technique of bookkeeping, i.e. how transactions could be recorded according to the double-entry system. The development of the theory of accounting that is, the why as to the how, began only in the nineteenth century.

The ea s et ee Pa ioli s su a a d the o e s ie tifi a ou ti g of

the nineteenth century was a period of refinement and elaboration of the procedures described by Pacioli? The summa became the standard reference work for bookkeepers and a model for numerous textbooks that provided a record of bookkeeping innovations between the fifteenth and the nineteenth centuries.

The development of bookkeeping can be divided into three phases:

The 110 years between 1450 and 1560. Business practices were more sophisticated than textbooks and authors tried to promote bookkeeping mechanics as developed by merchants.

The period from1560 to about 1800. Major improvement were made bookkeeping model and theoretical research on bookkeeping began, especially with the emergence of financial statements – and the acknowledgement of the enterprise as being separate and distinct from its owners.

The period after 1800, when manufacturing operations, income tax and the emerging profession acted as major stimulants.

Towards the middle of the nineteenth century, the formation of professional accounting societies began in many countries. The purpose of the various institutes and societies was to make recommendations on accounting practice to their members. This was to improve uniformity in dealing with financial transactions and to formulate basic principles applicable to financial statements.

Today, the issuing of recommendations on accounting practice is one of the most important functions of professional societies of accountants and auditors throughout the world.

27

Republic (the ZAR). Today, the profession in South Africa is organised into various provincial and national accounting institutes and societies, the most prominent being the South Africa Institutes of Chartered Accountants (SAICA).

I , the Pu li A ou ta ts a d Audito s A t, o , hi h o t ols the

practicing section of the accountancy profession in South Africa, was

p o ulgated. This legislatio eated the Pu li A ou ta ts a d Audito s

Board, whose functions include the registration of accountants and auditors who are permitted to practice in public, ensure discipline in the profession, and train accountants.

1.8 GENERALLY ACCEPTED ACCOUNTING PRACTICE (GAAP)

South Africa, like various other countries, developed its own accounting standards in the form of statements, which are the basis on which accounting reporting is done. The development of statements goes through a whole process of drafting and exposure by SAICA.

They must then be approved by the APB (the standard-setting body in South Africa). The principle objective of the APB is the establishment, recognition and acceptance of what the board considers being generally accepted practice (GAAP). The APB consists of representatives from commerce and industry, regulators, professional bodies, academics and user groups.

Since the APB has agreed to issue international financial reporting standard (IFRSs) as statements of GAAP, it has adopted the International Accounting Standards Board (IASB) framework for the preparation of financial statements (hereafter referred to as the frameworks). The purpose of this framework is mainly to assist preparers of financial statements to prepare and present financial statements for external use according to international standards.

In this module, reference will be made to the content of the framework, the preface to GAAP, and to International Accounting Standards (IAS). The

sta da ds set the IA“B a e la elled ith the p efi IA“ a d a u e . The

corresponding statement of GAAP will form part of the reference. For example: IAS 1 (AC 101) deals with the presentation of financial statements. Where reference is made to a paragraph of IAS, for example paragraph 55 of IAS 1, the reference will be stated as IAS 1 (AC 101).55.

28

and set out the objectives of the standard-setting process. All statements of GAAP should be read and applied in the context of the preface.

Since the framework forms the basis of accounting theory, it will be discussed in more detail in the remainder of this chapter and in chapter 2. As you progress with your studies, you might find it necessary to revisit these two chapters to re-acquaint yourself with the framework.

1.9 APPROACH TO SETTING ACCOUNTING STANDARDS

Statements of GAAP have been harmonised with IFRS. The APB has taken a decision to approve the international text of IFRS for issue in South Africa, without amendment (Preface .12).

Application of statements of GAAP

IFRSs apply to all general-purpose financial statements. Such financial statements are directed towards the common information needs of a wide range of users, for example, shareholders, creditors, employees and the public at large. The objective of a financial statement is to provide information about the financial position, performance and cash flows of an entity that is useful to those users in making economic decisions. (Preface, Annexure A .10).

Compliance with Legal Requirements

The requirements of the Companies Act and Schedule 4 thereto are taken into account in the preparation of GAAP (Companies Act, No 61 of 1973 as amended, section 285A (a) and (b). Some entities may be required to prepare financial statements which comply with other statutes. Statements of GAAP are, however, of concern in the preparation of all financial statements that purport to be prepared in accordance with GAAP, including those of business entities incorporated under other legislation, as well as those not incorporated at all.

1.10 TYPES OF BUSINESS ORGANISATIONS WITH PROFIT MOTIVES

In the private sector, there are mainly four types of business organisations with profit motives which can be considered as individual entities:

Soletraders (sole proprietors);

Partnerships;

Close corporations, and

29

There are a wide variety of organisations in the private sector with various objectives without a profit motive that can be regarded as individual entities:

Clubs;

Charitable organisations;

Churches;

Educational institutions;

Associations, and

Trusts.

In the public sector, the state as a whole, or individual government establishments, such as provinces, state departments, municipalities, boards and commissions, are all regarded as accounting entities. All these concepts are discussed extensively in business management modules and handbooks.

Between a public business and private business, which one would you prefer to run?

Types of business activities with profit motives

Business operating with a profit motive can be classified as service, trading and manufacturing business. These types of business can be explained in the following examples.

George is a qualified electrician who runs his business from home. George installs electrical cables and repairs electrical cables. The cabling he is doing must be supplied by the people for whom he is doing the repairs. These people are called clients.

Because George is merely rendering a service; we say that he runs a service organization. His clients buy their cabling from the hardware shop. The hardware shop is therefore a trading organization. The other people and other business entities served by the hardware shop are customers. The hardware shop buys the good from the manufacturer who is in this case the supplier.

The business entities that manufacture and sell the products are called

30

It is important to note that the manufacturer and the wholesaler are not always the same. Sometimes the distribution chain is longer with the manufacturer selling to a wholesaler, the wholesaler selling to retailer and the retailer selling to the customer.

TYPES OF BUSINESS BASED ON ORTGANISATIONAL FORM

Public Private Company Company

Sole trader

A sole trader is sometimes referred to as the sole proprietorship. This is a form of business ownership owned and run by one person usually the owner. The owner is responsible for the day to day running activities of the business. Many small service businesses such as plumbers, hairdressers and lawyers, fall into this category.

This is one the simplest form of business ownership since a limited amount of capital is required to start up the business. However, the owner is liable/ responsible in his/her personal capacity for the debts of the business. The owner is taxed is his own capacity.

The sole proprietorship is not a separate legal entity meaning that the business cannot be summoned to court and it can cease to exist once the owner dies.

Partnership

A partnership is a form of business that is owned by a minimum of two partners and a maximum of twenty (20) partners. Medical doctors, stockbrokers, attorneys and accountants often conduct their business as

partnership. All the partners are the owners of the business. A partnership just a sole proprietorship does not have a separate legal personality.

The individual partners are liable in their personal capacity for the debts of the company. Partnership profits are taxed in the hands of the individual partners.

31

When a partner dies or withdraws from the partnership, the partnership will be dissolved. If the remaining partners want to continue their business a new partnership will be formed.

One of the advantages of a partnership is that it can be set up with relatively little effort a d i i al apital i est e t. I the i di idual pa t e s o interest, it is important to draw up a partnership agreement which will contain information such as:

The profit sharing ratio

Each partners duties

And general code of conduct

Interest on drawings

Interest on capital, and

Salaries.

In order to ensure that the terms of the partnership agreement are complied with, it is important that financial information is provided by an accounting system.

Close corporation

The close corporation as business form has very popular in South Africa since 1985. A close corporation may have a minimum of 1 and a maximum of 10 owners (called members). The close corporation is different from the sole traders and the partnership in the sense that it has its own legal personality, and it exist independently of its members. When certain conditions exist members of the close corporation are personally liable for its debts. The members of the close corporation are usually also actively involved in its daily business activities. The letter CC after the name of the close corporation denotes it as such, for example Industrial Laboratories CC.

When compared with a company, a CC is relatively easy and inexpensive to set up. Presentation of the financial statements of a close corporation is regulated by the Close Corporation Act and Generally Accepted Accounting Practice (GAAP).

When registering a close corporation there are a number of legal requirements and certain paper work needs to be completed and signed.

One of the documents required is called a Founding Statement.

32

The Founding Statement of the CC needs to be completed and signed by every member.

The Founding Statement needs to contain the following information:

Full name of the CC

Letters CC added to the end of the businesses name

Postal address of the registered office

Principal activity of the CC

Details of each members contributions to the CC

Full names and identity numbers of each member

Interest of each member which needs to be expressed in percentage

Date on which the financial year ends

Name and address of the accounting officer of the CC

The Founding Statement is then sent to the Registrar of Close Corporations

An accounting officer must be appointed to the CC as he will draw up the financial statements

The Registrar of Close Corporations will issue a Certificate of Incorporation and a Registration number when the CC is registered. One copy of the Certificate of Incorporation is kept by the Registrar, another copy is sent to the CC and a third copy is sent to SARS (South African Revenue Services) to register the business for tax purposes.

The CC may only commence business after the Certificate of Incorporation has been issued.

When registering a CC you will have to provide your desired name of the CC, it is a good idea to have a few ideas as your first choice might not be available.

Advantages of a Close Corporation

The advantages of a CC are:

Registering a Close Corporation (CC) is a simple and relatively affordable option. It is not expensive and there are only a few regulations.

A CC does not have any legal complications that a company has. For example, a CC is not required to have annual financial statements audited and a CC is not required to hold annual general meetings. This makes running a CC easier than a company.

33

Income distributed to the members of the CC is exempted from normal income tax.

A CC may give financial assistance to a member to acquire an interest in the corporation.

The amount of capital a CC is able to access is normally more than the average sole trader or small business.

Liability of members for debts is limited except under certain exceptional contributes less capital because they have specific skills that are needed in the CC.

Knowing the advantages of a CC and the disadvantages will be useful when deciding if the number of members allowed in a Close Corporation (CC) is this could limit and hamper the growth and expansion of the business.

A member of a CC can be personally held liable for the losses of a CC if the member acts carelessly, or without skill.

Banks or loan establishments might require the financial documents of the CC to be audited when a CC applies for a loan. Funds will not be released until the auditing has been completed.

All e e s ust ag ee to dispose of a e e s i te est. This ould ake

it difficult for members to leave the CC or to pay a member their portion.

Every member acts as an agent of the CC and the CC is bound by the

e e s a tio s.

It is not possible to sell a CC to a company. First the CC needs to be converted into a company, and this can take time.

A CC cannot become part of a group structure, for example: A CC cannot become a subsidiary of a company or another close corporation.

Certain major decisions concerning the CC can be made by member/members who own a membership of at least 75%. These decisions must however, be in compliance with the CC agreement.

34

Company

A company is a business that maybe owned by a few or by thousands of people known as the shareholders. It is often managed by people who are not the owners. There are two types of companies:

Public company, limited by share capital which may be listed on the stock exchange or may not be listed;

Private company, limited by share capital; private companies cannot be listed

Anyone can buy shares for public companies on the stock exchange. The name

of the pu li o pa e ds ith Li ited a d p i ate o pa it s Pt ltd .

Registration requirements

All required registration forms may be purchased from a stationer dealing in statutory forms for approximately R100. To reserve a name, a CM5 application form (duplicate copies are no longer required), stamped with R50 in revenue stamps, must be submitted to the Regist a s offi e.

In order to save time and costs, it is recommended that three to four alternative names be furnished in order of preference. A preliminary search can be done on the Companies and Intellectual Property Registration Office of South Africa (CIPRO) website.

Following approval, the name will be reserved for a period of two months. Within this period, the documents for incorporation should be submitted. An extension of one month may be granted with the submission of the CM6 form, stamped R20 in revenue stamps. The Registrar must receive the application for

e te sio efo e the e d of the fi st t o‐ o th pe iod.

Legal and other professional fees relating to the registration of a company depend on the complexity of the individual application. For ordinary applications, without complications. Legal costs start at about R4 500. Standard versions of a memorandum and articles of association are included in the Companies Act.

A company may choose to submit its own version. However, this may slow down the approval process, as they would require close examination by the

‘egist a s offi e.

A complete application includes:

35

Power of attorney (if an attorney is used or if more than one subscriber exists)

CM22 (notice of postal address and registered office address), in duplicate

Me o a du a d a ti les of asso iatio , i dupli ate • CM e tifi ate of

incorporation

CM44 (signature page for subscribers)

CM46 (certificate to commence business), stamped R60

Close corporation versus companies

Owners Members Shareholders Shareholders Liability Limited Limited Limited Continuity Unlimited Unlimited Unlimited

36

Tax Pays Company Tax Pays Company Tax

Users of accounting information withdrawing the investment would mean that the business would close down. In the case of an investment in a company, the investor would simply sell the shares either to existing shareholders or to new shareholders.

The decision of an investor to continue holding the investment in a business, or the decision of a new investor, who is considering investing in a business, depends largely on the expected future performance of the business.

In order to make some estimates about its future prospects, pas financial performance of the business will provide important information. Investors will therefore the financial information generated by accounting. They will use this information to decide whether they will continue to keep their money in the business.

Management

The people who are responsible for managing a business are not always the same people as those who have invested money in the business. They are often employees of the business who work for a salary. Management objective is to make the business succeed, as they will be judged on how well they have done their job by the performance of the business. In order to monitor the progress of the business, they will be interested in the financial condition of the business, the cash available to run the business and the profitability of the business. All this financial information is supplied by the accounting system. Management are thus also users of accounting information.

Creditors

37

of the profit which is likely to be made. Creditors are most interested in the liquidity of the business. Liquidity is the ability of a business to pay its debts in cash when they fall due. All creditors are taking a risk when they lend money to a business or sell goods without receiving the cash payments immediately. The accounting system the creditors with information that assist them in assessing the extent of the risk and to determine the confidence which can be felt regarding the payment.

Investment analyst

An investment analyst is a person who studies the financial situation of various businesses and advises clients regarding investments. The requirements of the analysts are therefore essentially the same as those of the investors whom they advise.

Analysts spend a great deal of time comparing similar businesses in an attempt to predict which is likely to be most profitable and what risk are attached to each investment. It is obvious that the accounting system which provides financial information will assist in this task.

Government

Government bodies require financial information for two main reasons. The first is in order to develop statistical material which forms the basis on which economic and industrial policies are based. The second is in order the taxation policies of the South African Revenue Services (SARS). Most taxation of businesses in South Africa is based on the profit which the business has made. Quite clearly the accounting system must be designed to provide this information.

Employees

Employees use the accounting information during collective bargaining process. The financial information provided by the accounting system forms the basis for negotiation on wages and salaries. Generally employees will be interested to know the prospects of the future employment, whether they are being rewarded with a reasonable share of the profit which they helped to produce, and the ability of the business to meet its wage bill.

38

It is the primary responsibility of the entity to prepare and present the financial statement. Since the management is also a decision maker, it needs the information disclosed in the financial statement. Management has, in addition, access to other management and financial information that help it carry out its planning, decision-making and control function. For this, it has the ability to determine the format and content of the additional information used by management about the financial position, performance and changes in equity and the cash flow of the entity (framework 11)

1.11THE PURPOSE, STATUS AND SCOPE OF THE ACCOUNTING FRAMEWORK

The framework sets out the directives and concept that underlie the preparation and presentation of financial statements.

The purpose of the framework is to assist (Framework .1)

In the development of future accounting standards and the review of existing accounting standard

In promoting the harmonising of regulations, accounting standards and procedures relating to the presentation of financial statements, by providing a basis for reducing the number of alternative accounting treatments permitted by accounting standards;

National standard-setting bodies in developing national accounting standards;

Auditors in forming an opinion regarding whether financial statements are in line with international accounting standards, and

Users of financial statements in interpreting and valuating the information disclosed in financial statements.

The scope of the accounting framework is dealt with in paragraph 5 to 8 of the Framework, which deals with (Framework.5)

The objectives of financial statements;

The qualitative characteristics that determine the usefulness of information in financial statements;

The definition, recognition and measurement of the elements from which financial statements are constructed, and concept of capital and capital maintenance.

39

the information disclosed in the financial statements which should, therefore, be prepared and presented to fulfil their needs. (Framework 6).

Financial statements form part of the process of financial reporting. A complete set of financial statements (see paragraph 1.6 above) may include schedules and supplementary information. Financial statements do not, however, include such items as reports by directors, statements by chairman, discussions and analyses by management and similar items that may be included in a financial or annual report Framework 7).

The Framework applies to the financial statements of all commercial, industrial and business reporting entities, whether in the public or the private sector. A reporting entity is an entity for which there are users who rely on the financial statements as their major source of financial information about the entity (Framework 8).

1.12 THE NATURE OF AND THE NEED FOR FINANCIAL INFORMATION

Before the nature of the information needs of the various parties interested in an entity can be discussed, the function of information must first be discussed. The main function of information is t support decision-making.

A decision is usually preceded by the consideration of the information relevant to the factors that could affect the decision. Financial information supplied by the accounting process is primarily used for decision directed at planning or at exercising control. For planning decisions, financial information is used in determining future actions to be taken, often based on what happened in the past. The accounting process provides historical information-it records what happened in the past and reports on this. Decision-makers often require information in order to forecast future financial results. The historical information provided by the accounting process serves as a basis for forecasting the future.

Planning decisions are sometimes very simple, for example in the case of routine activities, or are some sometimes very complex, for example, decisions regarding the financial strategy and planning of an entity for the next financial year.

40

The most important control function of financial information is the provision of accountability and stewardship. Financial accountability is the responsibility of a person to whom assets have been entrusted, and entails giving accounts to the provider of the assets regarding the use of the assets. The provider of the assets exercises control over the use of the assets through the enforcement of accountability.

In the preface to the framework, it is stated that the ISAB is of the opinion that nearly all users of financial statements are making economic decision to:

Decide when to buy, hold or sell an equity investment;

Assess the stewardship and accountability of management;

Assess the ability of the entity to pay and provide other benefits to its employees;

Assess the security for amounts lent to the entity;

Determine taxation policies

Determine distributable profits and dividends

Prepare and use national income statistics, or

Regulate the activities of entities.

The different decision-makers have different needs, and use the information disclosed in the financial statements differently.

1.13 THE OBJECTIVES OF FINANCIAL STATEMENTS

According to paragraph 12 of the framework, the objectives of financial statements is to provide useful information about the financial performance, financial position and changes in financial position, which information is useful to a wide range of users in making economic decisions Financial statements prepared for this purpose will meet the common needs of most users. Financial statements do not, however, always provide all the information that users may need to make economic decisions. Statements largely disclose

The financial effects of past events, and do not necessarily provide non- financial information (framework 13)Financial statements also show the results of the stewardship of management, or the accountability of management for the resources entrusted to it.

41

1.14 FINANCIAL PERFORMANCE, CHANGES IN EQUITY, FINANCIAL POSITION AND STATEMENT OF CASH FLOWS

The disclosure of the financial performance, changes in equity and changes in the financial and cash flow positions of the entity are discussed in paragraph 15 to 21 of the framework.

Financial Performance

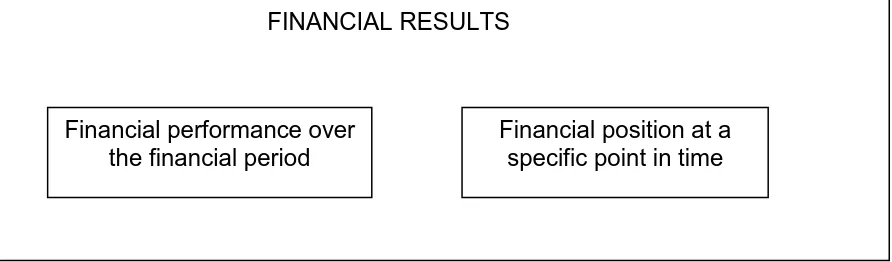

The financial results of an entity consist of economic activities which are measured in two ways: firstly, the financial performance for a particular period and, and secondly, the financial position at a particular point in time. This is illustrated in figure1.1

FIGURE 1.14.1

The financial performance reflects the profit made or the loss incurred by the entity over a specific period of time. The financial performance is reported in a statement of comprehensive income. A statement of comprehensive income reports the two elements of financial performance, i.e. revenue that was earned, and expenses that were incurred to earn the revenue. The difference between revenue and the expenses results in the profit or loss for that specific period. The various types of revenue and expenses are shown as separate items on the statement of comprehensive income.

Paragraph 17 of the framework explains that information about the performance of an entity is required to assess potential changes in the economic resources that the entity may control in the future. This type of information is useful in predicting the capacity of the entity to generate cash flow from its existing resources. This information may also help in assessing the effectiveness of the way in which new resources will be managed. Example 1.1 shows the Statement of Comprehensive Income of Alpha Services.

FINANCIAL RESULTS

Financial performance over the financial period

42

Example

Statement of Comprehensive Income for the year ended 31 March 2010

Revenue R850 000 Income from services rendered R850 000 Distribution, administrative and other expenses (R579 000) Salaries R520 000 Wages R50 000 Telephone expenses R4 000 Stationery R2 000 Insurance R3 000

Profit / Total comprehensive income for the year R271 000

Statement of changes in equity

In terms of paragraph 106 of IAS (Ac 101), information regarding any changes in the equity of an entity must be reported in a statement specially formatted to show the changes in the equity of an entity.

This statement also forms a link between the statement of comprehensive income (reflecting the profit/ total comprehensive income for the year) and the statement of financial position (reflecting the capital or equity) of the entity. In its simplest form, it starts with the balance of the capital at the end of the financial period. Example 1.2 shows the statement of changes in equity of Alpha services.

Example

Alpha Services

Statement of Changes in Equity for the year ended 31 March 2010 Capital

Balance at 1 April 20.1 409 000

Additional capital invested 100 000 Profit/total comprehensive income for the year 271 00

Drawings (90 000)

43

1.15 ACCOUNTING PRINCIPLES

Study the following sections on Accounting Principles

Pages: 14 – 18 from the prescribed textbook.

Prudence Concept

Accounting transactions and other events are sometimes uncertain but in order to be relevant we have to report them in time. We have to make estimates requiring judgment to counter the uncertainty. While making judgment we need to be cautious and prudent. Prudence is a key accounting principle which makes sure that assets and income are not overstated and liabilities and expenses are not understated.

Examples:

1. Bad debts are probable in many businesses, so they create a special

contra-account to accounts receivable called allowance for bad debts which brings the accounts receivable balance to the amount which is expected to be realized and hence prevents overstatement of assets. An expense called bad debts expense is also booked to stop net income from being overstated.

2. Some liabilities are contingent upon future occurrence or non-occurrence of an event such a law suit, etc. We judge the probability of occurrence of that event and if it is more than 50% we record a liability and corresponding expense at the most likely amount. Hence, we stop liability and expense from being understated.

3. Periodic evaluations of assets are made to make sure their carrying value does not exceed the benefits expected to be derived from the asset, and if it does exceed, the impairment of fixed asset is recorded by reducing its carrying amount.

Consistency Concept

The concept of consistency means that accounting methods once adopted must be applied consistently in future. Also same methods and techniques must be used for similar situations.

44

changed, a business must disclose the nature of change, the reasons for the change and its effects on the items of financial statements.

Consistency concept is important because of the need for comparability, that is, it enables investors and other users of financial statements to easily and correctly compare the financial statements of a company.

Examples

1. Company A has been using declining balance depreciation method for its

IT equipment. According to consistency concept it should continue to use declining balance depreciation method in respect of its IT equipment in the following periods. If the company wants to change it to another depreciation method, say for example the straight line method, it must provide in its financial report, the reason(s) for the

change, the nature of the change and the effects of the change on items such as accumulated depreciation.

2. Company B is a retailer dealing in shoes. It used first-in-first-out method of

inventory valuation in respect of shoes at Branch X and weighted average inventory valuation method in respect of similar shoes at Branch Y.

Here, the auditors must investigate whether there are any valid Hence, all such information which has the ability to affect the decisions of the users of financial statements is material and this property of information is called materiality.

In deciding whether a piece of information is material or not requires considerable judgment. Information is material either due to the amount involved or due to the importance of the event.

Examples:

1. The government of the country in which the company operates in working on a new legislation which would seriously impair the company's operations in future. Although there are no figures involved but the impact is so large that disclosure is imminent.

2. The remuneration paid to the executives and the directors is material. 3. The accounting policies are material because they help the users