Full Terms & Conditions of access and use can be found at

http://www.tandfonline.com/action/journalInformation?journalCode=vjeb20

Download by: [Universitas Maritim Raja Ali Haji] Date: 11 January 2016, At: 22:38

Journal of Education for Business

ISSN: 0883-2323 (Print) 1940-3356 (Online) Journal homepage: http://www.tandfonline.com/loi/vjeb20

Student Academic Performance in Undergraduate

Managerial-Accounting Courses

Abdulrahman Ali Al-Twaijry

To cite this article: Abdulrahman Ali Al-Twaijry (2010) Student Academic Performance in Undergraduate Managerial-Accounting Courses, Journal of Education for Business, 85:6, 311-322

To link to this article: http://dx.doi.org/10.1080/08832320903449584

Published online: 13 Feb 2011.

Submit your article to this journal

Article views: 652

View related articles

ISSN: 0833-2323

DOI: 10.1080/08832320903449584

Student Academic Performance in Undergraduate

Managerial-Accounting Courses

Abdulrahman Ali Al-Twaijry

Qassim University, Qassim, Al-Melaida, Saudi Arabia

The author’s purpose was to identify potential factors possibly affecting student performance in three sequential management-accounting courses: Managerial Accounting (MA), Cost Ac-counting (CA), and Advanced Managerial AcAc-counting (AMA) within the Saudi Arabian con-text. The sample, which was used to test the developed hypotheses, included 312 students whose performance was followed throughout 3 semesters (4, 6, and 8) out of 8. Techniques of mean comparison and correlation were employed. The results suggest that the preuniversity accounting background was only found to have significant impact on the AMA course whereas skill in mathematics was found to affect student performance significantly in the MA course. It was evidenced that student performance in the MA course and overall was significantly affected by preuniversity ability, general undergraduate academic capability, and matriculation year. Student performance in the Financial Accounting course significantly correlated with performance in the subsequent MA and AMA courses. There is also evidence of a significant relationship between MA student performance and that of both CA and AMA. The findings of this study confirmed that the load of weekly registered hours has no negative impact on the stu-dent performance. It also suggested that accounting stustu-dents had outperformed nonaccounting students in accounting and nonaccounting courses.

Keywords: accounting, student performance, undergraduate

Accounting education has received much attention from re-searchers in developed nations. A great many studies have been directed towards accounting education and how it might be enhanced. However, the research on accounting education in developing countries is still far behind. Their education systems are affected by various factors (i.e., culture, politics, and social factors) and this means that results from account-ing education studies can not be always applied to different nations because each has unique features. The education sys-tem in Saudi Arabia differs widely from western education systems in terms of teaching styles and program types, vol-umes, and content.

As is the case with many accounting and business depart-ments and schools worldwide facing the problem of weak student academic performance (cf. Gayle & Michael, 1999; Lane & Porch, 2002; Shotweel, 1999), the Accounting De-partment at Qassim University in Saudi Arabia has encoun-tered a severe challenge with its students. During the 15-year

Correspondence should be addressed to Abdulrahman Ali Al-Twaijry, Qassim University, Accounting Department, Qassim, Al-Melaida 6633, Saudi Arabia. E-mail: aaltwaijry@gmail.com

period from 1990 to 2005, the number of accounting stu-dents whose overall GPA was 4.00 or more out of 5.00 was fewer than 100 students (less than 10%). A great majority of accounting students find it rather difficult to understand managerial accounting courses, and a high percentage (av-erage 35–50%) of students fail in management accounting courses. As noted by Gracia and Jenkins (2002), academic failures have huge consequences, both emotionally and finan-cially. The reasons for these failures need to be understood and appropriate remedies applied.

One possible reason that makes failures in managerial ac-counting courses different from those in financial acac-counting and other business courses is that the managerial courses are not straightforward. They need critical thinking and a good background, especially in mathematics, and this war-rants further research to suggest ways for improving the stu-dent performance in these courses in particular, and account-ing programs more generally. Therefore, the question beg-ging an answer is which factors affect student performance in Managerial Accounting (MA) courses and whether they are different from those affecting performance in Financial Accounting (FA) courses as suggested by previous studies. Because no research was found to tackle this issue within

the Arabian environment, a gap exists in the literature. This study, however, endeavors to identify the potential factors that may have some effect on student performance generally, and particularly in three sequential management-accounting courses. These undergraduate courses are: MA in the second year (fourth semester), Cost Accounting (CA) in the third year (sixth semester), and Advanced Managerial Accounting (AMA) in the fourth year (eighth and final semester). The outcomes of this study have field implications and applica-tions to help enhance student performance generally and for these courses specifically.

Background of Saudi Arabia Business Educational System

The Saudi Arabian business educational system, although originally imported from the United States, is somewhat dif-ferent from those in the West. Public business education in Saudi Arabia, which represents about 80% of the industry and is only available for Saudis, is free with the government paying each student up to 1000 SR per month. Even though business education is available for both men and women, they are separated from each other. Students admitted to the business schools must have a high school degree with an acceptable GPA (normally above 70%).

The average undergraduate student stay at university is 4 years, in which an average of 140 hr (about 40–45% of them within the student major) must be studied and passed. Both Arabic and English are used as a medium of instruction. As for textbooks, they are mainly published in the West, with most of them having been translated into Arabic. Teach-ing styles are mostly a one-way street, which means that the instructor does almost all the talking, and students are the audience. Government regulations do not allow female instructors to teach male students whereas the opposite is possible but only through video conferencing.

A high percentage (an average of 85%) of the course assessment is based on the examinations, and the rest (15%) is based on homework, attendance, and projects. The passing level is 60%, and when the student cannot get a total of 60 out of 100 points for a course, he or she must restudy the course; there is no limit for retaking the same course as long as the GPA is at the required level (2.00 or above out of 5.00). When the GPA goes below 2.00, the student loses his or her stipend. When the GPA stays below 2.00 for three (and sometimes five) sequential semesters, the student must leave the university. In general, business students can find jobs easily, especially those majoring in accounting.

Literature Review and Hypothesis Development

Accounting education is one of the chief subjects that has been receiving and continues to receive great attention from accounting researchers. Many studies have focused on how to improve the quality of accounting education (i.e., Jackling, 2005; Kramer, Johnson, Crain, & Miller, 2005; Mustafa &

Chiang, 2006). Some research has been directed toward iden-tifying and suggesting solutions to problems and difficulties confronting accounting students (Booth, Luckett, & Mladen-ovic, 1999; Davidson, Slotnick, & Waldman, 2000; Gracia & Jenkins 2002; Lane & Porch 2002). More narrowly, several studies concentrated on one or more undergraduate or grad-uate accounting courses. Based on research carried out 18 years ago, Doran, Bouillon, and Smith (1991) found that the preuniversity accounting knowledge of students negatively affected their performance in the basic managerial account-ing course. Although this was a surprisaccount-ing result, it may not still be the case nowadays because both accounting academic programs and preuniversity education systems have changed. Auyeung (1991), Keef (1992), Rohde and Kavanagh (1996a), and Lee (1999) searched for possible variables affecting stu-dent performance in the Principles of Financial Accounting (PFA) course. One important finding of these studies was that the prior university accounting background and the general academic ability had a significant impact on performance in PFA.

The impact on student performance and of various en-try paths to tertiary education in a second-year accounting management course was assessed by Jackling and Anderson (1998). They examined the effect of background features of some students on their performance in the course. Jackling and Anderson’s results revealed that part-time students out-performed full-time students, and that both entry qualifica-tions and a student’s general ability together can predict per-formance in the management course. However, there was no evidence of any significant effect of preuniversity account-ing study, gender, or language background on the course performance of students. On the other hand, Lane and Porch (2002) endeavored to investigate the possible impact of back-ground factors of nonspecialist accounting students on their performance on the UK Level One and Level Two accounting modules. Multiple regression analysis was employed to eval-uate the effect of various explanatory variables. The analysis outcomes suggest that a student’s accounting background does not have a significant effect on Level One and Level Two accounting modules. More recently, Al-Twaijry (2005) studied the potential effects of various factors on student performance in the PFA course. The analysis of his sample (379 students) provided evidence that the significant vari-ables that affect the student performance in the PFA course are: (a) the preuniversity academic achievement, (b) the pre-university accounting background, and (c) the prepre-university mathematics attainment.

These studies have contradictory results regarding the po-tential effect of the student accounting and general back-ground on the introduction to accounting courses. The pos-sible reasons for that are either the time elapsed between the studies (some of them older than 15 years) or the cultural and educational system differences. Because the results of the majority of these studies supported the thesis that preuni-versity academic ability in accounting generally has a strong

effect on accounting courses, the potential impact of the stu-dent preuniversity accounting and their general background and performance on managerial accounting courses can be hypothesized as follows:

Hypothesis 1 (H1): The performance of Saudi Arabian

students with a preuniversity accounting acquaintance would be significantly higher in the university manage-ment accounting courses than those without such expe-rience.

H2: The performance of Saudi Arabian students with a higher

secondary school GPA would be significantly better in the university management accounting courses than those with a lower GPA.

Some research has been concerned with the students’ gen-eral performance in business and management schools. For example, Marcal and Roberts (2000), Brasfield, Harrison, and McCoy (1993), and Allmen (1996) found that past per-formance (i.e., at high school) was a good predictor of future (i.e., university) performance in the fields of management, business, and economic studies. Similarly, Duff (2004) used linear regression analyses to test the explanatory power of students’ approaches to learning, their gender and age, and their prior academic performance on the subsequent aca-demic achievement. The analysis outcome suggested that prior academic attainment was the strongest predicting vari-able of accounting and business economics students’ first-year academic performance. Based on these findings, the extent of the impact of student preuniversity performance and experience on performance at undergraduate business schools can be tested through the following hypotheses:

H3: The performance of Saudi Arabian undergraduate

busi-ness students with a higher secondary school GPA would be significantly better than those with a lower GPA.

H4: The performance of Saudi Arabian undergraduate

busi-ness students who graduated from scientific high schools would be significantly higher than those who graduated from nonscientific high schools.

Fewer studies (i.e., Drennan & Rohde, 2002; Jackling, Russell, & Anderson, 1994; Rohde & Kavanogh, 1996b) have focused on managerial accounting courses. Jackling et al. examined the influence of relaxing the condition of the prerequisite of basic managerial accounting (basic fi-nancial accounting) on the performance on the managerial accounting course and the influence of a student’s level of understanding English language on his or her performance in the basic accounting courses. Their results suggest that, under certain circumstances, waiving the prerequisite has a negative impact on student performance. This result, how-ever, could not be generalized. The level of understanding English was not found to have a significant effect on the student performance in the basic accounting courses. On the other hand, Rohde and Kavanagh searched for the factors

affecting student performance in a course on the principles of management accounting. The most important variable to help predict student performance was the course grade in the prerequisite course (Introduction to Financial Accounting). Considering that financial accounting courses differ in many aspects from managerial accounting courses, the effect of one on the other is questionable. To discover if the results reached can be confirmed or contradicted, the following hypothesis was tested:

H5: The Saudi Arabian undergraduate students who perform

better in the financial accounting course would also per-form significantly better in the management accounting courses.

Drennan and Rohde (2002) studied the factors expected to have an effect on student performance in AMA in an Australian university. They found that the performance of students whose mother tongue was not English in Introduc-tion to Managerial Accounting was relatively poor whereas their performance was good in AMA. Also, they found that the student performance in AMA was better for those who studied its prerequisite at the same university than for those who had taken the prerequisite somewhere else. The admis-sion procedure, which was not specifically addressed in this study, but which can be inferred from its findings, may cor-relate with the student performance in managerial courses and overall. In the year 2000, the acceptance procedure and criteria changed at the School of Business to which the Ac-counting Department belongs. To test the possible effect of such changes on academic performance, the following hy-pothesis was developed:

H6: The performance of Saudi Arabian business students

entering the University after the year 2000 would be significantly higher than those who entered before the year 2000.

Although accounting courses share some similarities, they sometimes differ widely from each other. The relationship between student performance in the first year accounting courses and the following year accounting courses was in-vestigated by Augeung (1991). The results confirm a strong relationship between student performance in the Introduction to Accounting course and in the advanced financial account-ing course. To extend their analysis to examine if the re-lation among introduction to management accounting, cost accounting, and advanced management accounting is also strong, the following hypothesis was set forth:

H7: The Saudi Arabian undergraduate students who

per-form better in a managerial accounting course would also significantly perform better in the other managerial accounting courses.

Other researchers endeavored to identify different fac-tors that may affect student performance in nonaccounting courses. For example, Anderson, Benjamin, and Fuss (1994)

examined the possible impact of the student’s ability in math-ematics in high school on his or her performance in the basic economics course. They found a significant positive corre-lation. On the other hand, in an earlier study, Ely and Hittle (1990) could not find such an effect of student ability in math-ematics on the performance in the business finance course. Because managerial accounting uses mathematics in a deeper manner than the other accounting courses, it was expected that students with good understanding of mathematics would perform better in management accounting courses, and so the following hypothesis was set forth:

H8: The Saudi Arabian undergraduate students achieving

bet-ter in preuniversity mathematics would perform signif-icantly better in the university management accounting courses than those whose achievement in mathematics is poorer.

Mathematical ability can significantly affect graduate and undergraduate business studies given that many of the courses at business schools rely on mathematics. Based on that, the following hypothesis was developed:

H9: The performance of Saudi Arabian undergraduate

busi-ness students who have done well in preuniversity math-ematics would be significantly higher than those whose achievement in preuniversity mathematics is poor.

Course scheduling and load could have an effect on the student performance. The likely influence of course schedul-ing durschedul-ing the week was investigated by Henebry (1997), who focused on the financial management course. Henebry’s results show that the likelihood of passing the course when it is scheduled for more than one meeting during the week is higher than when if there is only one long meeting during the week. The probability of the load effect was examined in a recent study by Mustafa and Chiang (2006), who suggested that course materials and course content do affect the quality of higher education. Because the time and load of the course are expected to affect performance in the course, also time and load of all other courses, which can be measured by the number of registered hours, are expected to negatively affect the individual courses and overall performance. That is be-cause a high load means less time available for homework and examination preparation for individual courses and vice versa. Based on this, the following hypotheses were devel-oped:

H10: Saudi Arabian undergraduate students with a small load

would perform significantly better in the university man-agement accounting courses as compared to those with a large load.

H11: The performance of Saudi Arabian undergraduate

busi-ness students with a small load would be significantly higher as compared to those with a large load.

Other factors, such as class size, course problems, atten-dance, student personality, and instructor’s attributes, could

have an effect on a university student’s academic perfor-mance. Naser and Peel (1998) found out that the class size, the instructor’s character and personality, the students’ effort, and the course problems are the factors most influencing stu-dent performance in the Introduction to Accounting course. Paisey and Paisey (2004) identified potential causes behind student absences from classes and found a strong positive relationship between student attendance and performance in an accounting module. The possible effect of a student’s personality was studied by Nguyen, Allen, and Fraccastoro (2005). They used data of 368 undergraduate and graduate students of a university business course. Anxiety was found to be positively and significantly predicting overall GPA, whereas the other personality characteristics such as agree-ableness, extroversion, emotionality, and intellect had some impact on the final course grade and overall GPA. The influ-ence of emotionality and intellect, however, depended on the student’s gender. Mustafa and Chiang (2006) endeavored to identify the quality dimensions in higher education and how they were related to instructor ability and attitudes, course material, and load and the amount of knowledge provided. The results, which were based on analyzing 485 question-naires, suggest that the key factors affecting the quality of higher education are teacher ability and attitude. The mean comparison analysis showed that students with a high GPA perceive course content to be more important for enhancing education quality, whereas the students with low GPAs per-ceived that a teacher’s superior performance enhanced course content.

Although the literature on this subject has highlighted various factors affecting student performance either in a par-ticular course or in general, other factors that may affect performance in accounting studies were not discussed. The term load, the type of high school, the term length and the student major are further factors that have the potential to have an impact on accounting student performance, and they need to be investigated. These variables are addressed and discussed in this study.

DATA COLLECTION AND DESCRIPTIVE ANALYSIS

The sample used in this study (312 students) was randomly selected from students registering during the academic years 2000, 2001, and 2002. These particular years were chosen because, as the normal stay at the university is 4 years, those students should have graduated, and they would have studied all three courses. The data sample was collected from the students’ present and permanent files kept in the university registration system, to which I was given access, through two steps. First, the data regarding the university academic performance was gathered from the students’ present files, files which contain information about the students’ academic transcripts, all semesters’ details, such as registered hours,

TABLE 1

Number of Students Who Either Received or Did Not Receive a Grade in the Course

Status MA CA AMA

Received a grade 219 187 90

Did not receive a grade 93 125 222

Total sample 312 312 312

Note. Students who did not receive a grade either dropped the course or had chosen different major (other than accounting) or left the university.

passed hours, term GPA, overall GPA, and specialization. Second, the other data were collected from the students’ permanent files, files that contain preuniversity information such as high school transcripts, date of birth, addresses, and special needs. Table 1 shows the number of students in the sample who received a grade in the management accounting courses.

The MA course is in Level 4 (second year), and all students in the college must take and pass it. A high percentage (30%

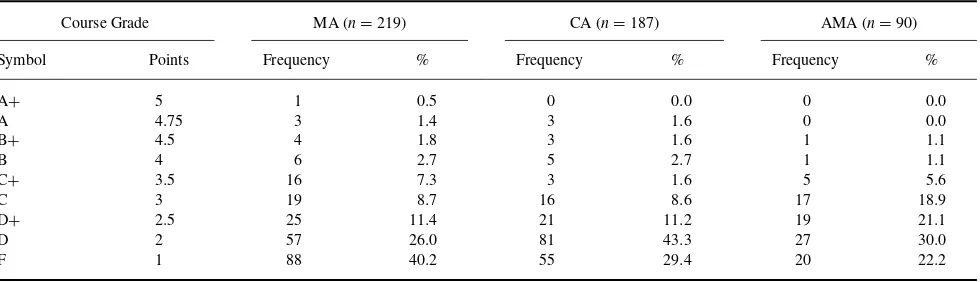

=93 students) did not receive a grade in that course, which means that nearly one third of the students in Level 4 had left the university (withdrawal or dismissal). The CA course is in Level 6 (third year) and must be taken by business students in addition to accounting students. The number of students who received a grade in the CA course was 187 whereas 125 (40%) did not get a grade in the course, which means that 30 (125—93) students (10%) had left the college during their third year. The AMA course is in Level 8, the last semester (in the fourth year) and taken only by accounting students. The total number of students in the sample who graduated in accounting was only ninety students. Table 2 represents the number and percentage of the sample students in each grade. Very few students (<2%) received an A+or A in the MA course, and even fewer (1.6%) in the CA course. Nobody received an A+or A in the AMA course. The number of students who got a B (4 points) or more is 6 (6.4%) in the MA course, 5 (5.9%) in the CA course, and 2 (2.2%) in the

AMA course. The vast majority of the students who passed the courses (MA, CA, AMA) received between a D and C+. On the other hand, 88 students (40%) failed the MA course, 55 students (29%) failed the CA course, and fewer (22%) failed the AMA course. This data may suggest that the performance of students in the management courses did not follow a normal distribution.

By looking at the term GPA and the overall GPA of the sample, which is illustrated in Table 3, it is noticeable that very few students got a GPA of 4.0 or over (between 1% and 3% in all cases). The great majority of the students (between 35% and 72%) had a GPA lower than 2.5. According to the university rules, a student with an overall GPA lower than 2.00 gets a warning and if the student could not improve his or her overall GPA to 2.00 or more for a number of terms (normally three), the student would be asked to leave the university. The percentage of those students who were at risk of being dismissed was 18% in Year 2, 5% in Year 3, and 1% in Year 4. Looking at the term performance, I noticed substantial development because in Term 4 more than 60% of the sample students had an overall GPA lower than 2.5, but in Term 8 more than 60% of the sample students had an overall GPA higher than 2.5. One possible reason of this is that the more time (terms) a student spends at university, the better the student understands and the better the student performs because, with time, the student gets used to the culture, system, and teaching style of the university, and he or she also is more mature.

Statistical Analysis and Hypothesis Testing

The hypotheses used in this research were of the alternative hypothesis format, which suggest an existence of an effect or relationship between variables. Such an effect or relationship was examined, and, if the hypothesis is proven, it would be possible to improve the academic performance by the affecting variables. The most widely used measurement of the student’s future academic performance was his or her past accomplishment. Normally, students with backgrounds in a subject are expected to do better than others with no

TABLE 2

Number and Percentage of Students in Each Grade

Course Grade MA (n=219) CA (n=187) AMA (n=90)

Symbol Points Frequency % Frequency % Frequency %

A+ 5 1 0.5 0 0.0 0 0.0

A 4.75 3 1.4 3 1.6 0 0.0

B+ 4.5 4 1.8 3 1.6 1 1.1

B 4 6 2.7 5 2.7 1 1.1

C+ 3.5 16 7.3 3 1.6 5 5.6

C 3 19 8.7 16 8.6 17 18.9

D+ 2.5 25 11.4 21 11.2 19 21.1

D 2 57 26.0 81 43.3 27 30.0

F 1 88 40.2 55 29.4 20 22.2

TABLE 3

Student Term and Overall Performance During the Three Academic Terms

MA (n=219) CA (n=187) AMA (n=90)

Term GPA Overall GPA Term GPA Overall GPA Term GPA Overall GPA

n % n % n % n % n % n % Grade

4 2 3 1 6 3 1 1 2 2 1 1 ≥4.0

41 19 14 6 33 18 17 9 27 30 15 17 3.0–3.99

40 18 43 20 60 32 48 26 29 32 30 33 2.5–2.99

66 30 119 54 40 21 111 59 19 21 43 48 2.0–2.49

68 31 40 19 48 26 10 5 13 14 1 1 <2.00

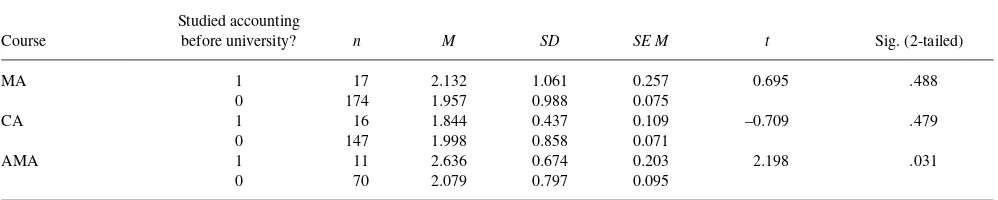

background. To examine this case in managerial accounting, I divided the sample into students who had studied at least one accounting course at high school and those who had not. The mean comparison results are disclosed in Table 4.

Students with preuniversity accounting backgrounds per-formed slightly better (not significantly) in the MA course, and this, to some extent, contradicts the findings of Doran et al. (1991) and those of Al-Twaijry (2005), but they are consis-tent with those of Jackling and Anderson (1998). However, in the CA course, students without such backgrounds per-formed slightly better (not significantly). On the other hand, students who had some experience in accounting before uni-versity did significantly (p<.05) better in the AMA course. These results lead us to acceptH1only for the AMA course.

There is no evidence of any significant (p >.20) effect of the preuniversity accounting background on term and over-all GPA. It seems that, although preuniversity accounting backgrounds may help students understand some topics in accounting, it is not very helpful, and so it may not be con-sidered as an influencing factor on overall performance in undergraduate accounting.

On the other hand, students who do well at high school are also expected to do well at university. To find out to what extent this was true, I compared the performance of students with a high school grade of 77.5 or higher to those with a grade lower than 77.5. This specific point was chosen be-cause, normally, the high school grades of students admitted to the business school at Qassim University range between 70

and 85, with an average of 77.5. Table 5 reveals the statistical analysis.

Students who performed better before university did sig-nificantly better (p<.05) in the MA course, and they also did better in the CA course but with less significance (p=.11). This result agrees with the findings of Jackling and Anderson (1998). However, the difference in means between the two groups in the AMA course is not significant. As a result, we acceptH2for the MA course only. I extended the analysis to

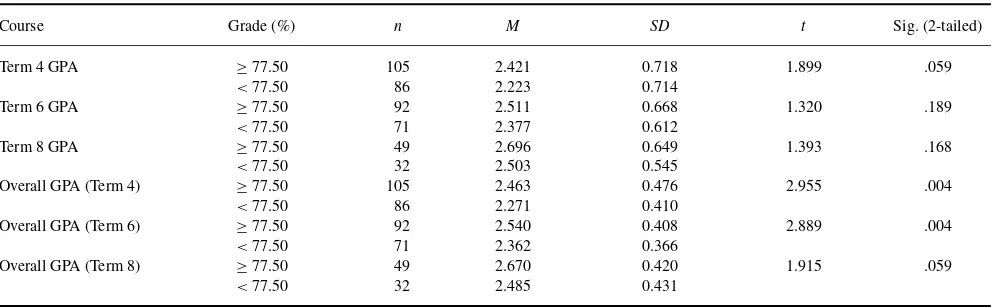

include the performance in the other term courses (measured by the term GPA) and in all university courses (measured by the overall GPA), and results are shown in Table 6.

Students with a higher preuniversity academic perfor-mance do significantly better at the university level, espe-cially in the first term. The difference between term GPA means is significant (p =.059) only in Term 4 and is not significant in Terms 6 and 8, and thus I only acceptH3for

Term 4. However, the difference between overall GPA means is significant in all cases, and soH3for overall performance

must not be rejected. These results confirm the findings of previous studies (i.e., Brasfield et al. 1993; Duff, 2004; Mar-cal & Roberts, 2000; Von Allmen, 1996). As a result, and in order to enhance the undergraduate accounting student suc-cess, more emphasis should be given to the level of student performance at high school.

There are several different types of high schools in Saudi Arabia with only one concerned more with scientific sub-jects (mathematics, physics, and chemistry) and the English

TABLE 4

Mean Comparison Between Students With and Without a Preuniversity Accounting Background

Course

Studied accounting

before university? n M SD SE M t Sig. (2-tailed)

MA 1 17 2.132 1.061 0.257 0.695 .488

0 174 1.957 0.988 0.075

CA 1 16 1.844 0.437 0.109 –0.709 .479

0 147 1.998 0.858 0.071

AMA 1 11 2.636 0.674 0.203 2.198 .031

0 70 2.079 0.797 0.095

Note.1=had accounting background before university, 0=otherwise.

TABLE 5

Course Mean Comparison Using a 77.5 High School Grade Cut-Off Point

Course Grade (%) n M SD t Sig. (2-tailed)

MA ≥77.50 105 2.138 1.052 2.585 .011

<77.50 86 1.770 0.880

CA ≥77.50 92 2.073 0.816 1.594 .113

<77.50 71 1.866 0.832

AMA ≥77.50 49 2.194 0.783 0.548 .586

<77.50 32 2.094 0.837

language. To examine to what extent the type of high school may affect undergraduate business student performance, we usedttest, the results of which shows that there were no sig-nificant differences (p>.25 in terms and overall) in the GPAs between students from scientific high schools and those from other high schools. ThusH4must be rejected. At present, the

Business College at Qassim University prefers students form scientific high schools to others, but as these findings sug-gest, the school type should not be considered as a dominant factor influencing the admission decision. On the other hand, the admission minimum acceptance level of high school GPA should be increased.

Probably, management accounting courses use mathemat-ics more than financial accounting, and so students with a bet-ter understanding (i.e., higher grades) of mathematics were expected to do better in these three management courses (MA, CA, and AMA). Using the mean comparison of grade in the course between students with a grade in mathematics equal to 65 (the average grade of the sample students) or more and others with less than 65 in mathematics, the only significant (p=.07) difference in means was found in the MA course, and so we do not rejectH8 for the MA course.

This result is consistent with Al-Twaijry’s (2005) findings regarding the effect of mathematics achievement on the stu-dent performance in financial accounting. In the other two courses (CA and AMA), and also in the term and overall GPA, student mathematics skill had no significant effect on

his performance. As a result,H8for CA and AMA and also

H9 cannot be accepted. A possible reason behind the

non-significant effect of the preuniversity mathematics capabil-ity on the school of business student performance, although mathematics is used in most of the courses, is either that mathematics content or teaching technique is different.

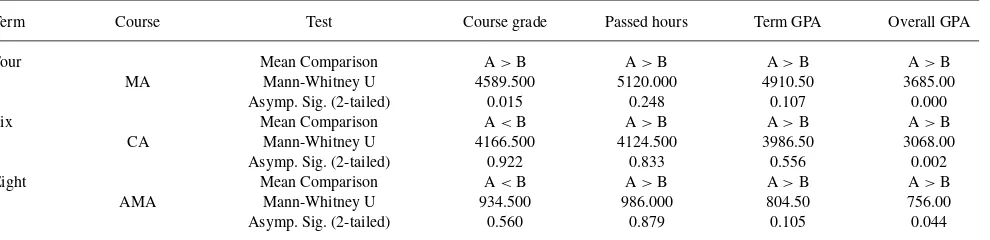

Development in higher education is dynamic. Admission procedures, course contents, and syllabi change over time. To examine whether the changes introduced in the year 2000 helped students in their academic performance and achieve better grades, we compared the performance (measured by course grade, passed hours, and GPA) for students enrolled at the college before the academic year 2000 and those who enrolled either in year 2000 or after. Table 7 shows the Mann-Whitney U results.

Students entering the university in the year 2000 or later performed significantly better (p <.05) in the MA course than students enrolled before the year 2000. However, there were no significant differences between the performances of these groups in CA and AMA courses. Thus,H6can be only

accepted for the MA course. The differences between the means of hours passed by these two groups were not signifi-cant (p>.20) in all three terms (4, 6, 8). The term GPA was better for those matriculating in the year 2000 or later, but the mean differences were not significant except at the 15% level for Terms 4 and 8 and not significant at all for Term 6. Therefore,H6must be rejected for term performance. On the

TABLE 6

Term and Overall GPAs Means Comparison Using a 77.5 High School Grade Cutoff Point

Course Grade (%) n M SD t Sig. (2-tailed)

Term 4 GPA ≥77.50 105 2.421 0.718 1.899 .059

<77.50 86 2.223 0.714

Term 6 GPA ≥77.50 92 2.511 0.668 1.320 .189

<77.50 71 2.377 0.612

Term 8 GPA ≥77.50 49 2.696 0.649 1.393 .168

<77.50 32 2.503 0.545

Overall GPA (Term 4) ≥77.50 105 2.463 0.476 2.955 .004

<77.50 86 2.271 0.410

Overall GPA (Term 6) ≥77.50 92 2.540 0.408 2.889 .004

<77.50 71 2.362 0.366

Overall GPA (Term 8) ≥77.50 49 2.670 0.420 1.915 .059

<77.50 32 2.485 0.431

TABLE 7

Course, Passed Hours, and GPA Means Comparison Using an Academic Year 2000 Cutoff Point

Term Course Test Course grade Passed hours Term GPA Overall GPA

Four Mean Comparison A>B A>B A>B A>B

MA Mann-Whitney U 4589.500 5120.000 4910.50 3685.00

Asymp. Sig. (2-tailed) 0.015 0.248 0.107 0.000

Six Mean Comparison A<B A>B A>B A>B

CA Mann-Whitney U 4166.500 4124.500 3986.50 3068.00

Asymp. Sig. (2-tailed) 0.922 0.833 0.556 0.002

Eight Mean Comparison A<B A>B A>B A>B

AMA Mann-Whitney U 934.500 986.000 804.50 756.00

Asymp. Sig. (2-tailed) 0.560 0.879 0.105 0.044

A=entered the college on or after the year 2000, B=entered college before year 2000.

other hand, students enrolled in the year 2000 or later gen-erally (overall GPA) performed significantly better (p<.05) than those enrolled before than the year 200. Therefore, we do not rejectH6for overall performance. These findings

con-firm that better admission procedures and more strict criteria could very well screen out students who were likely to fail or withdraw from the university, resulting in more successful higher education. On the other hand, it is very important to keep developing the education system to help the students perform better and encourage them to work harder.

Correlation Analysis

Sometimes students who are good in financial accounting are also good in managerial accounting. Nevertheless, this is not always the case. Many students performed much better in either financial or managerial accounting. We examined this case by correlating the students’ performance in financial accounting to their performance in management accounting. Table 8 provides the correlation data.

The previous correlation coefficients suggest that a sig-nificant (p=.000) positive correlation (.39) existed between FA and MA, agreeing with result of Rohde and Kavanagh (1996b). FA is also correlated significantly (p<.01) but with less strength (.30) with AMA. However, the correlation be-tween FA and CA was weak and insignificant. Therefore, al-ternativeH5should not be rejected except for the CA course

and so it is good that the FA course remains a prerequisite of the MA course.

MA is a prerequisite of CA and CA is a prerequisite of AMA. This means that a student cannot register in CA

with-TABLE 8

Correlation (Spearman’s Rho) of the Student Performance in FA, by MA, CA, and AMA

Variable FA MA CA AMA

Correlation coefficient 1 .389 .112 .295

Sig. (2-tailed) — .000 .142 .007

n 253 204 174 83

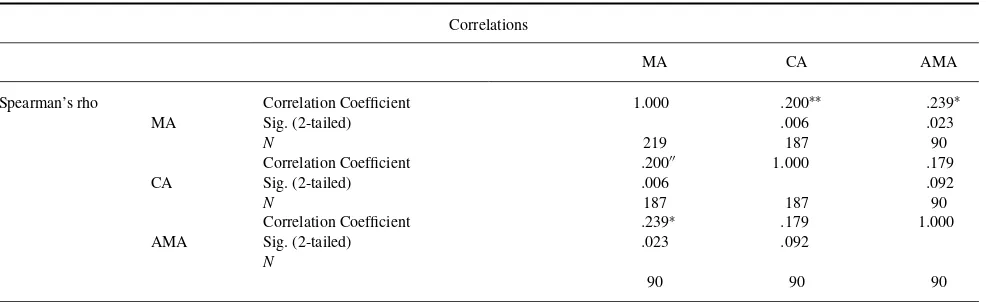

out passing MA and cannot register in AMA without passing CA, logically passing MA as well. Table 9 shows to what extent these three courses were correlated. The correlation matrix suggests that MA is significantly, but not strongly, correlated with CA and with AMA. So we should acceptH7

for the relationship between MA and CA and also between MA and AMA. This may mean that students who understand MA better perform better in both CA and AMA, and so it is important for MA to remain a prerequisite for both CA and AMA. However, there is no significant correlation between CA and AMA at the 5% level and soH7cannot be accepted

for the relationship between the CA and AMA courses. This is probably because the students in these courses vary. Al-though the CA course is considered as a MA course, its content mostly deals with costs, and so it is doubtful that CA should remain a prerequisite of AMA. It may be the time for the accounting curriculum to be reviewed because course prerequisites in many cases contribute to the delay in student graduation.

Load Analysis

The minimum number of hours a normal student must register in a normal academic term is 12 hr per week, the maximum being 20 hr and the normal average being 15 hr. In the summer term, however, a student can register for any number up to 9 hr (in some exceptional cases 12). Table 10 shows a comparison of the number of registered hours with hours passed.

The students tend to take more hours as they proceed in their studies. The percentage of average failing hours de-creases as the student advances to higher levels (26% in Term 4, 20% in Term 6, and 10% in Term 8).

It is rational that, when the load of hours on a student is high, the performance is low and vice versa. This is because if the student has a lighter load (fewer courses), he or she has more time to spend in these courses, but if the load is high (many courses), less time can be spent on each course. For this purpose, the registration system at the university restricts the number of weekly hours that can be registered by students

TABLE 9

Correlation Between Performance of MA, CA, and AMA

Correlations

MA CA AMA

Spearman’s rho Correlation Coefficient 1.000 .200∗∗ .239∗

MA Sig. (2-tailed) .006 .023

N 219 187 90

Correlation Coefficient .200′′ 1.000 .179

CA Sig. (2-tailed) .006 .092

N 187 187 90

Correlation Coefficient .239∗ .179 1.000

AMA Sig. (2-tailed) .023 .092

N

90 90 90

∗∗Correlation is significant at the .01 level (2-tailed)

∗Correlation is significant at the .05 level (2-tailed).

TABLE 10

Comparison Between Registered and Term Hours Passed

Term Description Min Max M SD

4 (MA;n=219) # of hours registered in the term 5 17 13.94 3.13

# of hours passed 0 17 10.25 4.69

6 (CA;n=187) # of hours registered in the term 5 18 15.24 2.35

# of hours passed 0 18 12.19 4.14

8 (AMA;n=90) # of hours registered in the term 5 20 15.54 2.83

# of hours passed 0 20 13.91 4.04

with low overall GPA in order for them to do better. To test the effect of the number of term hours on student performance on the three courses and whether lighter loads result in better performance, we ran a t test, and the results are shown in Table 11.

For the MA course, which is given in the second year, there was a significant difference (p<.05) between the means. But, the students with a load of more than 15 hr achieved better results than those with a lighter load. However, in the CA and AMA courses, there were no significant differences (p>.10) between the means, and so we must rejectH10. These results,

however, contrast with what is expected from the students. We may thus infer that students with more hours are more conscientious than others and work harder, whereas students with fewer hours do not care as much because they think they

can pass a few courses without having to worry too much and subsequently they neglect their studies. Table 12 compares the term GPA means between students with more than 15 hr and those with equal to or fewer than 15 registered hours per week.

From the previous mean comparison statistical analysis, in all three terms (4, 6 8), the term GPA means of students taking more than 15 hr were significantly better than were those of students with fewer hours per week. In Terms 4 and 6, the difference is significant at the 1% level, but the means differences in Term 8 are only significant at the 10% level. These results lead us to reject H11, thus restricting

the students with a low GPA to fewer weekly registered hours, which may not be an encouraging decision and a better alternative should be sought.

TABLE 11

Course Mean Comparison Using a 15-hr Cutoff Point

Course Registered hours n M SD t Sig. (2-tailed)

MA >15 69 2.370 1.100 3.680 .000

≤15 150 1.840 0.949

CA >15 61 2.120 0.937 1.228 .221

≤15 126 1.950 0.851

AMA >15 41 2.200 0.765 –0.110 .913

≤15 49 2.210 0.866

TABLE 12

Term GPA Mean Comparison Using a 15-hr Cutoff Point

Variable Registered hours n M SD t Sig. (2-tailed)

Term 4 GPA >15 69 2.637 0.799 4.079 .000

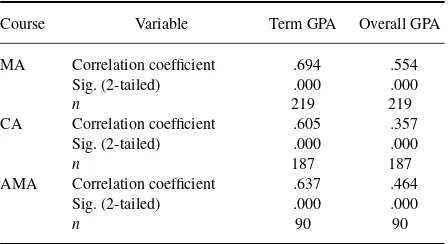

In this section more findings are presented and discussed. The relationship between management accounting courses and the other undergraduate courses reflects the level of con-sistency between them. The extent of relationship between the student’s performance in each of the three management accounting courses and his general (term and all) perfor-mance are measured by the Spearman test, the results of which are shown in Table 13.

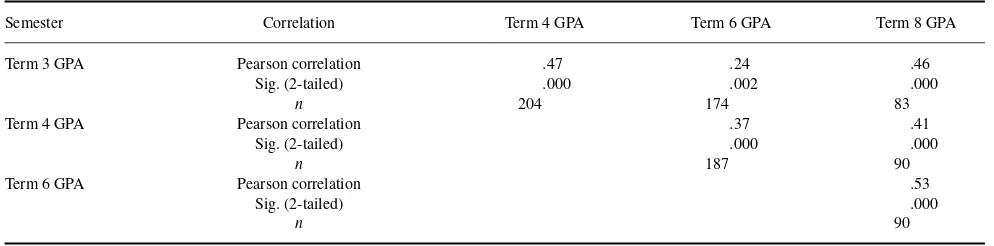

Spearman’s results confirm the strong, significant corre-lations between student performance in the courses (MA, CA, and AMA) and student performance in the other courses (term GPA). Also, there are significant (but weaker) corre-lations between the performance in these individual courses and the students’ general performance at a university level (overall GPA). Table 14 shows the correlation results between four semesters. Term 3 was included because it contains FA, and the others are Terms 4, 6, and 8.

The strongest relationships were found between student performance in Term 6 and in Term 8 (Pearson correlation=

. 53). There were also strong relationships between the per-formance in Terms 3 and 4 (Pearson correlation=.47) and between performance in Terms 3 and 8 (Person correlation

=.46). However, the correlation between Terms 4 and 6 was weaker (Pearson correlation =.37). The weakest relation-ship was between Terms 3 and 6. All these correlations are significant at the 1% level.

TABLE 13

Correlation (Spearman’s Rho) Between Course Performance (MA, CA, and AMA)and General

Performance (Term and Overall GPA)

Course Variable Term GPA Overall GPA

MA Correlation coefficient .694 .554

Sig. (2-tailed) .000 .000

n 219 219

CA Correlation coefficient .605 .357

Sig. (2-tailed) .000 .000

n 187 187

AMA Correlation coefficient .637 .464

Sig. (2-tailed) .000 .000

n 90 90

Two of three management accounting courses (MA and CA) are required to be taken nonaccounting students. By comparing the performance of accounting students to nonac-counting students in these courses, we found that the mean performance (grade) of accounting students in the MA course (2.34) was significantly (p = .000) better than that of the nonaccounting students (1.77). Also the accounting student performance in the CA course (2.16) was significantly (p

<.05) higher than the nonaccounting performance (1.87). It should be noticed, however, that until Term 4, both account-ing and nonaccountaccount-ing students take the same accountaccount-ing courses, and so the difference in means should not be at-tributed to the fact that accounting students have had more accounting courses and experience. The proper explanation of this is that those students with a better understanding of (and performance in) accounting elementary courses are more likely to major in accounting. By comparing the perfor-mance between accounting and nonaccounting students in all term courses, we found that accounting students did signifi-cantly (p=.000) better in the other (nonaccounting) courses as well (2.56) compared to nonaccounting students (2.20) in Term 4. However, in Term 6, although accounting student mean performance (2.44) was higher than for nonaccounting students (2.21), the difference was not significant (p=.66). If we went further and examined the differences between ac-counting and nonacac-counting students in all courses (overall GPA) from the beginning, we would find that accounting stu-dents would outperform nonaccounting stustu-dents. The means of accounting students’ overall GPA were significantly (p=

.000) higher than the means of other students’ overall GPA. This probably means that accounting students are, in gen-eral, better, in terms of ability. Also it can be inferred from these results that students of accounting are competent in courses unrelated to accounting, whereas the competence of nonaccounting students in accounting courses is pathetic.

Many management and business schools offer summer terms to help students complete their degrees faster. But the question that should be raised is whether significant differ-ences exist in the performance in summer terms as com-pared to normal terms. The study’s sample statistical results show no significant difference in the performance in the MA course between normal terms and summer terms (p=.63). However, using the 10% level of significance, the mean of normal terms GPA (2.38) is higher than it is in the summer

TABLE 14

Correlations Between Four Semesters: Term 2 (with FA) and Terms 4, 6, and 8

Semester Correlation Term 4 GPA Term 6 GPA Term 8 GPA

Term 3 GPA Pearson correlation .47 .24 .46

Sig. (2-tailed) .000 .002 .000

n 204 174 83

Term 4 GPA Pearson correlation .37 .41

Sig. (2-tailed) .000 .000

n 187 90

Term 6 GPA Pearson correlation .53

Sig. (2-tailed) .000

n 90

terms (2.11). In the CA course, there were no significant (p>.30) differences, either in the course performance or in the term GPA. Nevertheless, a significant difference exists when examining the results for the AMA course. Students who studied AMA in normal terms performed better (2.27) than those who had taken the course in summer term (1.20). In fact, 4 out of 5 (80%) students who studied AMA in the summer term failed in the course. The general performance in all term courses (Term GPA) was significantly (p=.086) higher in the normal terms. One probable reason of the weak performance in the summer term is the level of absence, and this, as reported by Paisey and Paisey (2004), has a negative influence on academic performance. From these results, we conclude that it would be better not to offer AMA in the summer term. Otherwise, the absenteeism problem must be resolved. The case is, however, more flexible in the MA and CA courses. In other words, there must be a careful selection of the courses that can be offered during summer semester, course with which the students can cope.

SUMMARY AND CONCLUSION

Many problems are associated with weak student perfor-mance at the university level. To eliminate such problems, a sufficient amount of research must be undertaken to uncover ways to enhance student academic performance. However, in the present study, we have attempted to identify factors which may affect accounting student performance in Saudi Arabia, mainly in the management accounting courses as well as more generally. Student performance in management accounting courses was very weak. The failing percentage goes up to 50%, and the great majority of students (up to 80%) who passed the course(s), got low marks (D to C). In terms of general performance (term and overall GPA), over 60% of the sampled students had a GPA lower than 2.50 in Term 4. Although this percentage has improved when going to the higher level (Terms 6 and 8), it is still high (45–50%). There was evidence of a significant effect of preuniversity academic ability on the MA course and on overall perfor-mance. The preuniversity accounting background was only

found to have significant impact on the AMA course, whereas the preuniversity mathematics ability was found to signifi-cantly affect student performance in the MA course. How-ever, no effects related to the type of high school were de-tected on the student undergraduate performance. Student performance in the Financial Accounting course did signif-icantly correlate to the performance in the subsequent MA and AMA courses, but its correlation to the CA was weak. There is also evidence of a significant relationship between the student performance in the MA course and performance in both CM and AMA, but the correlation between CA and AMA was weaker. On the other hand, it was evidenced that students with a better performance in the MA, CA, and AMA also performed significantly better in the other term courses and in the university courses more generally. Moreover, the analysis of the research shows that student performances in Terms 3, 4, 6, and 8 are significantly correlated, emphasizing that the strongest correlation coefficient is between Terms 6 and 8 whereas the weakest coefficient exists between Terms 3 and 6.

The number of weekly registered hours was expected to have a negative impact on the student performance, but, in fact, it did not. The results of the MA course and Term 4 GPA were amazing because a significant positive relation existed between performance and the number of registered hours. On the other hand, it was evident that students who entered the university in the year 2000 or later performed significantly better in the MA course and overall. The comparison between accounting and nonaccounting student performance proved that accounting students had outperformed nonaccounting students even in the nonaccounting courses. Moreover, the performance comparison between normal terms and summer terms confirmed that, in general, students perform better in normal terms.

Based on these findings, we suggest that high school student selection criteria should concentrate more on high school performance, and more attention should be placed on the undergraduate new students and introductory courses. Relaxing the restriction on the number of weekly hours for which students with lower GPA can register might enhance term performance. The accounting curriculum and course

prerequisite in particular and undergraduate accounting pro-gram in general need more meditation.

There is a strong need for qualitative and quantitative research to determine the major problems encountered by accounting students, problems impeding their better aca-demic achievement in general and in management accounting courses in particular. Future researchers should investigate the possible effect of other variables on academic perfor-mance. For example, the effects of teaching styles, course content, evaluation and examination structure, scheduling system, the absenteeism problem, and student capability are factors that should be investigated.

REFERENCES

Allmen, V. P. (1996). The effect of quantitative prerequisites on performance

in intermediate microeconomics.Journal of Education for Business,72,

18–22.

Al-Twaijry, A. A. (2005).Evaluation of student performance in the

Prin-cipals of Financial Accounting course. Research Centre and Human Re-source Development, No 67. Al-Melaida, Saudia Arabia: College of Eco-nomics and Business, Qassim University.

Anderson, G., Benjamin, D., & Fuss, M. (1994). The determinants of

suc-cess in university introductory economics courses.Journal of Economic

Education,25, 99–119.

Auyeung, P. K. (1991, March).Secondary school accounting and student

subsequent performance in the initial university accounting course: An Australian study. Paper presented at Third Annual Conference of Ac-counting Academics, Hong Kong.

Booth, P., Luckett, P., & Mladenovic, R. (1999). The quality of learning in accounting education: the impact of approaches to learning on academic

performance.Accounting Education,8, 277–300.

Brasfield, D., Harrison, D., & McCoy, J. (1993). The impact of high school

economics on the college principles of economics course. Journal of

Economic Education,24, 99–111.

Davidson, R. A., Slotnick, S. A., & Waldman, D. A. (2000). Using

linguis-tic performance to measure problem-solving.Accounting Education,9,

53–66.

Doran, B. M., Bouillon, M. L., & Smith, C. G. (1991). Determinants of

stu-dent performance in Accounting Principles I and II.Issues in Accounting

Education,6, 74–48.

Drennan, L. G., & Rohde, F. H. (2002). Determinants of performance in advanced undergraduate management accounting: An empirical

investi-gation.Accounting and Finance,42, 27–40.

Duff, A. (2004). Understanding academic performance and progression of first-year accounting and business economics undergraduates: the role of

approaches to learning and prior academic achievement.Approaches to

Learning in Accounting Education,13, 409–430.

Ely, D., & Hittle, L. (1990). The impact of mathematics background on

performance in managerial economics and basic finance courses.Journal

of Financial Education,19, 59–61.

Gayle, R. L., & Michael, R. J. (1999). Impact of course length and homework

assignments on student performance.Journal of Education for Business,

74, 325–331.

Gracia L., & Jenkins, E. (2002). An exploration of student failure on an

undergraduate accounting programme of study.Accounting Education,

11, 93–107.

Henebry, K. (1997). The impact of class schedule on student performance

in a financial management course.Journal of Education for Business,73,

114–120.

Jackling, B. (2005). Perceptions of the learning context and learning

ap-proaches: Implications for quality learning outcomes in accounting.

Ac-counting Education,14, 271–291.

Jackling, B., & Anderson, A. (1998). Study mode, general ability and

performance in accounting: a research note.Accounting Education,7,

65–73.

Jackling, B., Russell, G., & Anderson, A. (1994, July).Student background

and performance in management accounting. Paper presented at Account-ing Association of Australia and New Zealand Conference. Wollongong, New Zealand.

Keef, S. P. (1992). The effect of prior accounting education: Some evidence

from New Zealand.Accounting Education,1, 63–68.

Kramer, B., Johnson, C., Crain, G., & Miller, S. (2005). The

practitioner-professor link.Journal of Accountancy,199, 77–80.

Lane, A., & Porch, M. (2002). The impact of background factors on the performance of nonspecialist undergraduate students on accounting

modules—A longitudinal study: A research note.Accounting Education,

11, 109–118.

Lee, D. S. (1999). Strength of high school accounting qualification and student performance in performance in university-level introductory

ac-counting courses in Hong Kong.Journal of Education and Business,74,

301–306.

Marcal, L., & Roberts, W. W. (2000). Computer literacy requirements and

student performance in business communications.Journal of Education

for Business,75, 253–257.

Mustafa, S., & Chiang, D. (2006). Dimensions of quality in higher edu-cation: How academic performance affects university students’ teacher

evaluations.Journal of American Academy of Business, Cambridge,8,

294–303.

Naser, K., & Peel, M. (1998). An exploratory study of the impact of inter-vening variables on student performance in a Principles of Accounting

course.Accounting Education,7, 209–223.

Nguyen, N., Allen, L., & Fraccastoro, K. (2005). Personality predicts

aca-demic performance: Exploring the moderating role of gender.Journal of

Higher Education Policy & Management,27, 105–116.

Paisey C., & Paisey, N. (2004). Student attendance in an account-ing module—reasons for non-attendance and the effect on academic

performance at a Scottish University. Accounting Education, 13,

39–53.

Rohde, F. H., & Kavanagh, M. (1996a). Performance in first year university accounting: quantifying the advantage of secondary school accounting. Accounting and Finance,36, 275–285.

Rohde, F. H., & Kavanagh, M. (1996b). Academic determinants of

perfor-mance in first year management accounting.Accounting Research

Jour-nal,9, 63–69.

Shotweel, T. A. (1999). Comparative analysis of business and non-business student performance in financial accounting: Passing rates, interest and motivation in accounting, and attitudes toward reading and mathematics. College Student Journal,33, 1–13.

Von Allmen, P. (1996). The effect of quantitative prerequisites on

perfor-mance in intermediate microeconomics.Journal of Education for

Busi-ness,72, 18–22.