International Journal of Islamic and Middle Eastern Finance and

Management

Transparency and perf ormance in Islamic banking: Implicat ions on prof it dist ribut ion Nada Lahrech Abdelmounaim Lahrech Youssef Boulaksil

Article information:

To cite this document:Nada Lahrech Abdelmounaim Lahrech Youssef Boulaksil , (2014)," Transparency and performance in Islamic banking Implications on profit distribution ", International Journal of Islamic and Middle Eastern Finance and Management, Vol. 7 Iss 1 pp. 61 - 88

Permanent link t o t his document :

http://dx.doi.org/10.1108/IMEFM-06-2012-0047

Downloaded on: 25 March 2017, At : 18: 59 (PT)

Ref erences: t his document cont ains ref erences t o 41 ot her document s. To copy t his document : permissions@emeraldinsight . com

The f ullt ext of t his document has been downloaded 1158 t imes since 2014*

Users who downloaded this article also downloaded:

(2014),"Ownership structure and financial performance in Islamic banks: Does bank ownership matter?", International Journal of Islamic and Middle Eastern Finance and Management, Vol. 7 Iss 2 pp. 146-160 http://dx.doi.org/10.1108/IMEFM-01-2013-0002

(2014),"Shari’ah compliance in Islamic banking: An empirical study on selected Islamic banks in

Bangladesh", International Journal of Islamic and Middle Eastern Finance and Management, Vol. 7 Iss 2 pp. 182-199 http://dx.doi.org/10.1108/IMEFM-06-2012-0051

Access t o t his document was grant ed t hrough an Emerald subscript ion provided by emerald-srm: 602779 [ ]

For Authors

If you would like t o writ e f or t his, or any ot her Emerald publicat ion, t hen please use our Emerald f or Aut hors service inf ormat ion about how t o choose which publicat ion t o writ e f or and submission guidelines are available f or all. Please visit www. emeraldinsight . com/ aut hors f or more inf ormat ion.

About Emerald www.emeraldinsight.com

Emerald is a global publisher linking research and pract ice t o t he benef it of societ y. The company manages a port f olio of more t han 290 j ournals and over 2, 350 books and book series volumes, as well as providing an ext ensive range of online product s and addit ional cust omer resources and services.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation.

*Relat ed cont ent and download inf ormat ion correct at t ime of download.

Transparency and performance

in Islamic banking

Implications on profit distribution

Nada Lahrech, Abdelmounaim Lahrech and Youssef Boulaksil

School of Business Administration, Al Akhawayn University,Ifrane, Morocco

Abstract

Purpose– The purpose of this paper is to assess whether Islamic banks are transparent regarding profit (and loss) sharing to investment account holders. Another objective is to appraise whether Islamic banks’ performance affects management incentives to distribute profit (and loss) to investment account holders.

Design/methodology/approach– To investigate the research issue, the authors conducted an empirical study. Data of 25 global operating Islamic banks have been collected and analyzed for the period 2006-2010. The authors also developed a mathematical model based on the generalized least-squares principle.

Findings– The research results showed that enhancing transparency will prevent Islamic banks from shadowing their profit allocation practices and place investment account holders in a better position to manage their invested funds. The study also showed that bettering Islamic banks’ performance will induce them to manager profit-sharing investment account holders’ funds under bonafides.

Research limitations/implications– The main limitation is data availability. The maximum number of Islamic banks that disclose financial data covering the period of 2006-2010 limited the scope of the study to 25 banks.

Practical implications– The findings are very valuable for designing policies and standards as well as for the enforcement of these standards to improve transparency in Islamic banking.

Originality/value– The study outcome is vital to many parties involved in the Islamic banking field and can be taken as a strong foundation to make appropriate actions that would help grow and sustain Islamic banking development globally.

Keywords Performance, Profit distribution, Transparency

Paper typeResearch paper

1. Introduction

In the past few years, it has been widely believed that transparency enhances market disciplines. This trend toward transparency has triggered tremendous improvements in accounting rules and capital regulations that serve as a pathway for the establishment of a transparent and a compatible picture that would benefit investors all over the world. The idea of transparency in the banking sector is scarcely new; its importance emerged after the recent credit turmoil, the Asian financial crisis and the US subprime crisis where many banks have been blamed for lacking transparency. In the broad sense, the issue of transparency is of critical importance in the banking sector in general and even more so in the Islamic banking sector. Islamic banking is one of the most important aspects in the global economy nowadays with a rapid expansion over the past five years

in which it had witnessed a growth rate of 15-20 per cent per annum[1]. The Islamic

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1753-8394.htm

Islamic banking

61

International Journal of Islamic and Middle Eastern Finance and Management Vol. 7 No. 1, 2014 pp. 61-88 © Emerald Group Publishing Limited 1753-8394 DOI10.1108/IMEFM-06-2012-0047

banking sector is the most advanced part of the Islamic finance segment, providing a

wide array of financial instruments based on Islamic Shariah laws (Association of

Islamic Banking Institutions Malaysia, 2011). The Islamic Shariah is established on the prohibition of the receipt or payment of an agreed upon rate of return. This closes the door to the conventional interest-based lending system.

In the same optic, Islamic banks operate under the umbrella of profit and loss sharing (PLS) principle in which interest-bearing contracts are swapped by return-bearing contracts. Depositors[2] in such banks can be considered as investors or shareholders who receive dividends in case the bank reports a profit or loss part of their capital in case the bank incurs a loss. The key point in PLS is to avoid debt financing and to use equity

financing by providing financial instruments called Mudaraba and Musharaka.

However, despite the rapid expansion of Islamic banks, many of them fail in adopting

PLS-based finance (Humayon and Presley, 2000).

One of the reasons of such a failure is the agency problem. Under Mudaraba financing, capital owner is not allowed by Shariah law to manage the funds invested. Depositors do not have the right to control or interfere in the management of their funds, which is the sole responsibility of the Islamic bank acting as “Mudarib” (Ghayad, 2008). In such case, there is less monitoring from the depositors’ side, which provides the bank with more incentives to report less profit in a way that a large proportion of the earnings are kept inside the bank.

Under Musharaka, described most essentially as a joint-venture profit-sharing contract, profits are shared among participants on an agreed ratio, while losses are shared in proportion to their capital contribution. A major element in this contract relies on the fact that unlike in the case of Mudaraba, both partners share and control how the investment is managed. However, banks rely on professional managers and partners, namely, external auditors and consultants, to manage and make business decisions. The concern here is the latter aspect, professional managers or partners may have inducement to seek and maximize their own benefits at the expense of business owners (Samadet al., 2005).

Another major reason for PLS adoption failure is the moral hazard problem. As Islamic banks are not exposed to a total risk of loss, they have more inducement to invest in risky projects.Ariffinet al.(2009)point out that the concept of bank transparency is more essential to Islamic banks than conventional banks, as Islamic banks operate under PLS principle. This standpoint lies in the fact that profit-sharing investment account holders (PSIAHs) necessitate higher access to information concerning the level of risk and return associated with their participation, enabling them to scrutinize their investments. Do all Islamic banks really disclose the appropriate information for all the parties involved? Or, in other words, can all Islamic banks be considered transparent?

Based on the theoretical foundation of Islamic banking, this paper argues that Islamic banking transparency constitutes the prime concern for investment account holders (IAHs). PSIAHs try to choose among Islamic banks based on the level of confidence in banking competencies and abilities to realize returns from the invested capital. Lack of such confidence will drive PSIAHs to switch to less-opaque Islamic banks. In addition, as PSIAHs do not meet the basic characteristics of depositors, i.e. neither a certain capital nor a return on investment, this can give incentives to Islamic banks to be less transparent, which facilitates the manipulation of profit distributed to this type of depositors.

IMEFM

7,1

62

The attractiveness of transparency avoidance that may benefit Islamic banks seems to be one of the factors that influence profit sharing to the PSIAHs. On the other hand, banks’ performance is predicted to have a strong correlation with the latter. Strictly speaking, in case Islamic banks’ performance is flourishing, there is no room for profit manipulation. However, in case of low performance, Islamic banks tend to shadow the estimation of profit sharing to sustain their profit share as Mudarib.

In this paper, an empirical study will be conducted to investigate the impact of transparency on profit-sharing ratio and to find evidence of a linkage between performance and profit distribution. The result of this research can be valuable for many parties involved in the Islamic banking industry: Islamic institutions, investors and Islamic policymakers will have a clear idea about the general tendency used by global Islamic banks in terms of profit distribution and take the appropriate actions to avoid any anomaly that could be detected by the study.

The remainder of the paper is structured as follows: Section 2 presents a literature review related to the issue. Section 3 deals with the empirical approach. Section 4 explains the data collection approach used to study the problem. Finally, Sections 5 and 6 present the results with the appropriate conclusions and recommendations, respectively.

2. Literature review and hypotheses

TheBasel Committee on Banking Supervision (1998)defined in 1998 transparency as:

[…] public timely disclosure of reliable information that enables users of that information to make a precise appraisal of a bank’s financial health and performance, business activities, risk profile and risk management practices.

Based on this definition, for an Islamic bank to be transparent, it should disclose adequate and reliable information which enables the assessment of its financial performance, profitability and risk exposure.

This definition leads us to raise the question of when are practices applied for profit distribution transparent and consistent? General theories about profit distribution argue that the profit belongs to the owner of the business. In the schools of the classical

and neo-classical economic theories (Dobb, 1973), it is assumed that the profit was

closely associated to the entrepreneur, as they have in mind that the owner is the one who seeks profit maximization, which is not the case of workers. However, labor is the main profit driver for the company, which may call for investigating this theory. Hence, labor is not remunerated to its contribution to the added value, making the distribution process less optimal. As a result, what model can be considered as an efficient profit distribution?

The answer to this question needs an analysis of the economic efficiency principle which states that “ends and means should be related to each other as optimal as possible” (Diefenbach, 2003). Diefenbach explains the principle by the fact that means contribute to the ends so it is essential that the former should receive a return in a way that compensate their contribution to the ends and increase their willingness to attain the ends for the next period. If the economic efficiency principle was applied in the Islamic banking context, the means represent the agent who has expertise in developing capital (Mudarib) and profit represents the ends; in that case, the agent must be remunerated in proportion to his/her contribution to the added value (Haller, 1998).

63

Islamic banking

By extrapolating the aforestated principles to the banking sector in particular, we can notice different practices applied. In the case of conventional banking, the sector is dominated by the interest-based credit contract system. The purpose of the conventional

bank is to capitalize on shareholders’ value by maximizing their wealth.Awan (2009)

explains profit maximization by the fact that conventional banks raise funds by borrowing money from depositors under a variety of deposit schemes. The main source of profit for these types of banks is generated from charging high interest rates on loans outstanding and low interest rates on deposits.

As opposed to conventional banks which stipulate returns based on the capital extended, when Islamic banks operate funds through their PLS facilities, they are required to agree on a profit-sharing ratio so as to comply with Shariah guidelines. One of the major Shariah principles is that the profit and loss should be shared equitably

among the parties involved in the transaction.Khaldi and Hamdouni (2011)stated that

Shariah equity law expresses the need for a fair and equitable sharing of profit and loss between depositors and banks, whatever the form of financing used. To do so, Islamic banks determine the profit distribution ratio by taking into account the envisaged rate of return on capital, the size of the investment and the period of exposure such as the duration taken for realization of profits. To decide on the profit-sharing ratio, banks start by multiplying the amount of capital sought to be invested by the appropriate rate of return and by the expected period, arriving at the net return the bank wishes to realize. The rate of return can be negotiated especially in case of high exposure.

AlthoughEl Tegani (1996)argues that the main issue of the methodology undertaken by Islamic banks relies on the fact that when investment holders place their money with such banks, the deposit is held in one single investment pool containing all other types of deposits, namely, saving, current and investment deposits. Consequently, two major concerns rely behind the latter mode of operation. The primary concern is to breakdown the actual amount invested into the proportion of funds belonging to the IAHs and those belonging to the bank. Generally, banks are not allowed to invest all the money deposited; they are required by law to keep a portion of the money as a legal reserve to meet unexpected withdrawals. Also, beside government regulations, sometimes, bank projects included in its investment portfolio necessitate less capital than the total funds available for investment. Thereby, the participation ratio of each party involved cannot be easily ascertained. The second concern encountered is the allocation of the actual return to IAHs and other types of depositors. To make it clear, Islamic banks invest their pool of funds in several projects; on one hand, only a portion of each depositor’s funds is invested, and on the other hand, the projects may be completed in different time horizons, making it difficult for the bank to determine the appropriate profit allocated to investment holders, especially if the latter withdraws his or her money before the completion of the project.

In the same perspective, a number of standards and best practices established by the Islamic Financial Services Board (IFSB) are useful and provide a valuable reference in enhancing the transparency among Islamic institutions. The standards were settled to allow financial market participants, namely, investors, financial institutions and IAHs, to evaluate major operating activities undertaken by Islamic financial institutions. IFSB standards gauge capital structure as assessment of the financial health of the entity, assess the overall risk profile by reviewing capital adequacy levels, appraise the Islamic financial institutions in terms of risk and return treatment toward IAHs and determine

IMEFM

7,1

64

the exposure level to different types of risk (IFSB, 2007). IFSB ensures that Islamic banks incorporate all best practices as a mean to reinforce transparency in Islamic banking, and provide clarity regarding profit allocation basis applicable to various PSIAHs. Disclosure on rate of return calculation and profit allocation is essential to prevent banks from unduly manipulating share of profit distributed to IAHs.

Moreover,Farooket al.(2012)find that Islamic banks do engage in profit distribution management. It is important to recognize the impact of PLS mode of financing on depositors. When Islamic banks provide PLS facilities, they are able to manage the amount of profit allocated to their investment depositors mainly resulting from the profit-sharing relationship that banks have with their depositors. As a result, it may prove useful to consider that information disclosure will reduce information asymmetry and reduce Islamic banks’ willingness to manipulate profit distribution ratio.

In line with the aforementioned literature and analysis, this study hypothesizes the existence of a significant relationship between transparency in Islamic banks and their profit distribution.

H1. Ceteris paribus, there is a significant relationship between the disclosure level of quantitative and qualitative information in Islamic banking financials and the profit allocation ratio.

The second part of the research will assess the relationship between the Islamic banks’ performance and the distribution of profit to IAHs.

Prior studies discussed and tested the indirect relationship between the performance and profit allocation. In other words, researchers argued that corporate governance mechanisms affect the performance of a firm, which in turn has an effect on the profit distribution mainly in form of dividends.Myers and Majluf (1999)argue that in presence of asymmetric information, firms tend to overlook good investments due to lack of capital reserve, leading to minimizing the transaction costs or the cost of issuing new stock to raise capital in the market, restricting paying dividends to those resources that will not be used for investment. While part of the literature highlights information asymmetry impact on dividends policy, another part cites agency conflict as a factor influencing dividends payout. Agency theory deals with conflicts of interest between corporate insiders, such as managers and controlling shareholders, on one hand, and outside investors, such as minority shareholders, on the other hand. One of the principal remedies to the agency problems is the alignment of interests of both parties (principle

and agent), which can be done in the form of dividends payment.Jensen and Meckling

(1976) as well asFama and French (2001)stated that shareholders are interested in reducing the discretionary funds for a better alignment between the interests of managers and those of the shareholders, to minimize the agency cost.Coreet al.(1999)

demonstrated that low agency problem can improve the firm value and performance. In that way, good corporate governance mechanisms will lead to better performance.

Archer and Abdel Karim (2009)argue that Islamic banks keep savings from profit generated to smooth returns or cover periodic losses to compete with interest rates

offered by non-Islamic banks. This argument is in line with a study byFarooket al.

(2012)that brought evidence of Islamic banking profit distribution management. The latter phenomenon is triggered by the profit-sharing relationship with their investment depositors; Islamic banks are able to manage the extent of profit allocated to IAHs based on market circumstances. Under bad economic conditions, Islamic banks may perform

65

Islamic banking

poorly and incur losses which stipulate sacrificing their shareholders’ profit to offset such losses and remain competitive in the banking market. To our knowledge, none of the previous research works examine the direct relationship between performance and profit distribution. Therefore, this study will investigate the simultaneous relationship between the two by indentifying performance indicator for banks’ financial performance. One may assume that in periods of financial strengths, the Islamic banks may distribute higher profits to their depositors than in periods with an adverse financial position.

H2. Ceteris paribus, there is a significant relationship between better bank performance and the level of profit distribution ratio.

3. Methodology and model formulation

The purpose of this paper is twofold:

(1) evaluate the transparency and consistency of methods applied by Islamic banks

for profit distribution to depositors; and

(2) identify the impact of Islamic banks’ performance on profit distribution to

depositors.

3.1 Evaluation of transparency of methods applied by Islamic banks for profit distribution

For attaining transparency, Islamic banks need to place greater emphasis on the disclosure of sufficient, accurate and relevant information on a timely basis. The disclosure should be in the form of quantitative as well as qualitative information that will permit parties involved to make appropriate assessment of the bank’s operations and also to be able to evaluate the level of risk inherent in its operations. That is why a transparency audit checklist is used to determine the level of transparency among Islamic banks. The list includes the main standards established by the IFSB with regard to transparency in general and profit distribution disclosures in particular (Appendix 2). The score of each bank in terms of transparency was used as a measurement to conduct further quantitative tests to assess the correlation between transparency and profit distribution to depositors.

The methodology of transparency estimation was provided from a study undertaken by Standard & Poor’s (S&P) to assess the transparency of the Russian banking sector (Standard & Poor’s, 2010). In line with S&P’s methodology, the transparency ratios will be calculated based on annual reports and publicly disclosed information released for

bank i in year T until the new publication of year T⫹ 1. The study will use three

transparency ratios; the first one named general transparency ratio (GEN) that will assess compliance with IFSB general information disclosure practices either on annual

reports or Web sites (Appendix 2). The second one named unrestricted investment

account (UIA) rates banks in terms of their transparency toward unrestricted IAHs (Appendix 2). In other words, the variable will assess published information concerning profit allocated to this type of depositors, the profit rate calculations, the amount of funds invested and the invested funds. The third determinant of transparency, called restricted investment account ratio (RIA), will appraise transparency about restricted IAHs, representing another type of depositors in Islamic banks (Appendix 2).

This study considers the fact that the impact of transparency on profit distribution may differ from one type of account to another. To the extent that under RIAs, banks

IMEFM

7,1

66

tend to be transparent because they are subject to restrictions on one hand and investors have full control of their money on the other hand. Whereas under UIAs, banks follow an aggressive approach under which all the deposits are put together regardless of their sources. In this case, banks are prone to invest these funds into risky portfolios, as unrestricted IAHs will share any unexpected loss from these investments. This latter argument is in line withCihak and Hesse (2008), as they argue that when banks have full access to deposits, moral hazard increases because of the fact that the risk uncounted or loss incurred would be absorbed by the IAHs, inducing banks to go for riskier projects. Additionally, unrestricted IAHs have more incentives to monitor banks’ operations, considering the fact that neither their initial capital deposited nor the return on that capital is fixed or guaranteed (Errico and Farahbaksh, 1998). The study provides also a practical example of Iranian banks, where restricted Mudarabah is well common under which restricted depositors invest their funds in specific types of projects. This setting provides a basis to investigate whether an adequate information disclosure can have a significant impact on profit distribution to IAHs.

In addition to the aforestated ratios, a global transparency ratio is added in the model to assess the impact of transparency in general on the profit distributed to depositors. The ratio will be calculated as an average of all the three ratios of transparency. This regression approach was used by a prior paper that studies the relationship between transparency and efficiency in the Russian banking sector (Farvaqueet al., 2011). The empirical model specification is as follows:

Profit distributionit⫽␣ ⫹ 1(GENit)⫹2(UIAit)⫹3(RIAit)⫹4(GTRit)

⫹ 5(CDUM)⫹6(ODUM)⫹

(1)

Where:

Profit distribution ratioit⫽profit distribution ratio at the level of bankiat yeart

␣ ⫽Constant

1…6 ⫽Coefficient regression

GENit ⫽Ratio of general transparency at the level of bankiat

yeart

UIAit ⫽Ratio of unrestricted investment account transparency at

the level of bankiat yeart

RIAit ⫽ Ratio of restricted investment account transparency at

the level of bankiat yeart

GTRit ⫽Ratio of global transparency at the level of bankiat

yeart

CDUM ⫽Country dummy

ODUM ⫽Ownership dummy

The calculation of profit distribution ratio differs from one country to another. Banks allocated profit in accordance with central banks’ instructions. Under the study coverage, two major methods have been identified when allocating profit to IAHs. The first one corresponds to the attribution of the net profit realized from all income and expenses at the end of the financial year (for instance, banks located in Qatar and United Arab Emirates). In this case, after deducting all the expenses, the net income is divided among shareholders of the bank and the IAHs. The second method considers

67

Islamic banking

the allocation of profit on the basis of the income generated from financing and investing activities before the deduction of the bank’s operating expenses (for instance, banks located in Jordan and Bahrain). To be consistent, the calculation of profit distribution ratio is adapted to the accounting policies of each bank by dividing the total amount of profit distributed over the basis of the allocation.

Concerning the control variables, we will use a country variable, as banks’ attitude

toward transparency may differ from one country to another.Dincer and Eichengreen

(2007)demonstrate that banks in developed countries are more transparent than banks in developing countries. The country control variable is a dummy variable with 1 corresponding to developed countries and 0 to otherwise. Beside the country dummy, an ownership dummy is also added to the model to control for the ownership structure of each bank in the sample. ODUM has a value of 1 for publicly listed banks and 0 for privately owned banks. In principle, higher level of transparency seems to be evident in publicly listed banks, as they are subject to close monitoring and restrictions by regulators (Table I).

3.2 Assessment of the performance impact on the profit distribution

With Islamic banking on the rise in Muslim as well as non-Muslim countries, it is vital to give due attention to the impact of banks’ performancevis-a`-visprofit distribution. The most popular model when assessing bank’s financial health called CAMEL will be

used in this research (Manoj, 2010). Most financial experts, particularly banks

supervisors, are adopting this method in a way to evaluate bank performance. This approach endeavors to evaluate how different ratios have been used and interpreted to reveal a bank’s performance. Using the CAMEL framework, an analysis of five groups of indicators will be undertaken to reflect the financial health of Islamic banks. The indicators are as presented inTable II(seeAppendix 3for ratios detailed components).

Table I.

Descriptive statistics for transparency and profit sharing

Variables

Number of observations

Mean (per cent)

Standard deviation (per cent)

Minimum (per cent)

Maximum (per cent) CV

PDR 123 43.43 21.50 ⫺70.00 99.68 0.495

GEN 123 45.84 15.00 5.56 77.78 0.327

UIA 123 40.40 15.20 0.00 84.62 0.376

RIA 123 7.43 13.30 0.00 57.14 1.790

GTR 123 31.22 10.80 1.85 71.33 0.346

Notes: All variables used have moderate standard deviation. From major Islamic banks located globally, profit distribution ratio is ranged between⫺70 and 99.68 per cent. The mean of PDR is equal to 43.43 per cent, meaning that on average, Islamic banks tend to distribute 43 per cent of their profits to depositors. Concerning general transparency ratio (GEN), it ranges from 5.5 to 77.77 per cent, with a mean of 46 per cent. The restricted investment account transparency ratio (RIA) varies from 0 to 57 per cent, with a mean of 7 per cent, implying that Islamic banks are very opaque with regard to restricted investment account holders. Moreover, the transparency ratio regarding unrestricted investment account holders (UIA) shows a discrepancy from 0 to 85 per cent, with an average of 40 per cent. Still, the average rate is below 50 per cent, implying that Islamic banks are making inadequate disclosure also less transparent with regard to unrestricted investment account holders. As to general transparency ratio, which measures the average transparency of each bank included in the sample, it shows that, on average, Islamic banks are 31 per cent transparentvis-a`-visinvestment account holders

IMEFM

7,1

68

Table

II.

CAMEL

framework

Category Ratio Interpretation and citation

Capital adequacy (Tier 1⫹Tier 2)/risk-weighted assets

The ability of banks offset a decline in assets due to losses on bank assets using its own capital.

The most widely used indicator of capital adequacy (Hasbi and Haruman, 2011). Assets quality Non-performing loans/gross

loans

Cash recovery/loan default Loan loss reserve/impaired loans

The NPL ratio is often used as a proxy for asset quality and is intended to identify problems with asset quality in the loan portfolio (IMF, 2006).

The most important indicator used to identify problems with asset quality in loan portfolio is the percentage of gross and net non-performing loans to total advances (Sarker, 2006;Hasbi and Haruman, 2011).

Kabir and Bashir (2003) argued that the loan loss reserve to impaired loans ratio relate provisions to non-performing or impaired loans. The higher this ratio the better quality is.

The quality is measured in relation to the level of: Non-performing assets Recoveries

Provisions

Management soundness Total cost/income Administrative expense/T. expenditure

This component is mainly used to assess the working efficiency of the bank’s management.

Both ratios’ expense helps in gauging the management quality of the banking institutions (Hasbi and Haruman, 2011).

Earnings and profitability Return on equity (net income/T. equity) Return on assets (net income/T. assets)

Non-interest margin (non-interest income/avg loans)

This component indicates how profitable a bank is, which gives an idea as to how efficient the bank is at using its assets to generate earnings.

ROE: prior literature found that return to equity was a significant proxy in the level of profitability generated by the bank using its shareholders’ funds. The higher this ratio, the better performance of the bank (Hasbi and Haruman, 2011;

Routledge and Gadenne, 2000).

ROA (net income/T. assets): ROA was used by prior researchers as an indicator that measures the ability to generate profits and found to be significant (Demirguc-Kunt and Huizinga, 2000).

NIM (non-interest income/avg loans): this ratio was adjusted to the Islamic banking principles, as the interest income is prohibited by the Shariah.Goldberg and Rai (1996)used the net non-interest return as a rough proxy of bank efficiency.

Liquidity Loans/deposits

Liquid assets/T. assets

The first ratio measures the ability to repay the bank withdrawals by customers with relying on loans as a source of liquidity (Routledge and Gadenne, 2000). The second ratio looks at what percentage of customer and short-term funds could be met if they were withdrawn suddenly (Kabir and Bashir, 2003).

69

Islamic

banking

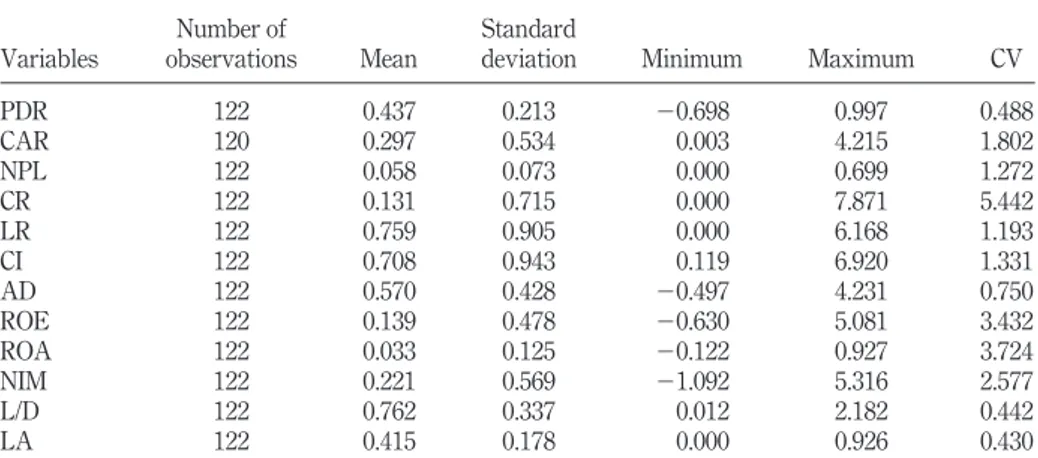

Inputs to the CAMEL model are obtained from balance sheets and income statements of the 25 banks included in the sample, as well as other financial reports that the Basel Committee required banks to publish. The results of the ratios calculation are used in a regression model to assess the correlation between the Islamic banking performance and the profit distribution. The multiple regression model would be expressed as follows (Table III):

PDRit⫽␣ ⫹ 1(CARit)⫹2(NPLit)⫹3(CRit)⫹ 4(LRit)⫹5(CIit)⫹6(ADit)

⫹ 7(ROEit)⫹8(ROAit)⫹9(NIMit)⫹ 10(L/Dit)⫹11(LAit)

⫹

兺

12(CDUM)⫹兺

13(ODUM)⫹ (2)

Where:

PDRit ⫽profit distribution ratio at the level of bankiat yeart

␣ ⫽Constant

1…13⫽Coefficient regression

CARit ⫽Capital adequacy ratio at the level of bankiat yeart

NPLit ⫽Non performing loans ratio at the level of bankiat yeart

Table III.

Descriptive statistics for profit sharing and banks’ performance: CAMEL approach

Variables

Number of

observations Mean

Standard

deviation Minimum Maximum CV

PDR 122 0.437 0.213 ⫺0.698 0.997 0.488

CAR 120 0.297 0.534 0.003 4.215 1.802

NPL 122 0.058 0.073 0.000 0.699 1.272

CR 122 0.131 0.715 0.000 7.871 5.442

LR 122 0.759 0.905 0.000 6.168 1.193

CI 122 0.708 0.943 0.119 6.920 1.331

AD 122 0.570 0.428 ⫺0.497 4.231 0.750

ROE 122 0.139 0.478 ⫺0.630 5.081 3.432

ROA 122 0.033 0.125 ⫺0.122 0.927 3.724

NIM 122 0.221 0.569 ⫺1.092 5.316 2.577

L/D 122 0.762 0.337 0.012 2.182 0.442

LA 122 0.415 0.178 0.000 0.926 0.430

Notes: On the subject of performance indicators in Islamic banks, the average capital adequacy is around 30 per cent. However, some banks covered in the sample have a very high CAR due to the fact that their risk-weighted assets are minimal compared to their Tier 1 and 2 capital. Regarding the assets quality dimension, Islamic banks have a varying range of non-performing loans ratio from 0 to 70 per cent, with a mean of 6 per cent. However, Islamic banks are taking actions to avoid potential loan default, as they are enlarging their loan loss reserve, which accounts for 75 per cent from their non-performing loans and they are recovering cash amounted to 13 per cent from loans classified as defaulted. Concerning management soundness, on average, Islamic banks’ cost of income ratio is around 70 per cent, from which 57 per cent of the cost is paid as administrative expenses. With regard to the profitability level, the average return on equity is 14 per cent and return on assets of 3 per cent with 22 per cent of the return generated is coming from loans. Additionally, 76 per cent of the funds deposited in Islamic banks are given as loans with a liquidity rate ranging from 0 to 92 per cent and an average liquidity rate of 41 per cent

IMEFM

7,1

70

CRit ⫽Cash recovery ratio at the level of bankiat yeart

LRit ⫽Loan loss reserve ratio at the level of bankiat yeart

CIit ⫽Cost to income ratio at the level of bankiat yeart

ADit ⫽Administrative expense ratio at the level of bankiat yeart

ROEit ⫽Return on equity ratio at the level of bankiat yeart

ROAit ⫽Return on assets ratio at the level of bankiat yeart

NIMit ⫽non interest margin ratio at the level of bankiat yeart

L/Dit ⫽Loans over deposits ratio at the level of bankiat yeart

LAit ⫽Liquid assets ratio at the level of bankiat yeart

CDUM ⫽Country dummy

ODUM ⫽Ownership dummy

Furthermore, a sixth component, sensitivity to the market, was added by federal banking supervisors to the CAMEL framework as a measurement method that provides adequate information to evaluate bank’s condition and risks regarding the market. The sensitivity can be estimated by calculating the price to earnings ratio. This ratio was used byNurazi and Evans (2005)as a proxy of the sensitivity to the market risk. Prior literature concerning the assessment of the financial performance of Islamic banking through CAMELS framework demonstrated that the method is one of the most

efficient techniques in evaluating the performance of banks (Mubarak, 2004;Sari,

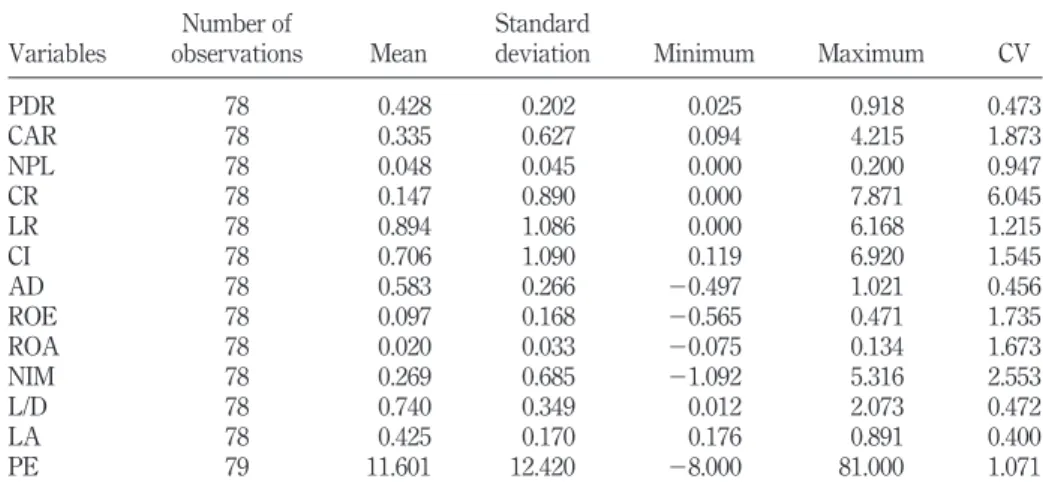

2007andWijaya, 2008). The research uses also the CAMELS approach to determine the impact of price to earnings ratio, as a sensitivity measure, on profit distribution. However, as not all the banks included in the sample are listed; the analysis will be limited to the number of publicly traded banks. The new empirical model specification is as follows (Table IV):

PDRit⫽ ␣ ⫹ 1(CARit)⫹ 2(NPLit)⫹ 3(CRit)⫹ 4(LRit)⫹ 5(CIit)⫹ 6(ADit)

⫹ 7(ROEit)⫹ 8(ROAit)⫹ 9(NIMit)⫹10(L/Dit)⫹ 11(LAit)

⫹ 12(PEit)⫹

兺

13(CDUM)⫹兺

14(ODUM)⫹ (3)

Where:

PDRit ⫽profit distribution ratio of at the level of bankiat yeart

␣ ⫽Constant

1…14⫽Coefficient regression

CARit ⫽Capital adequacy ratio at the level of bankiat yeart

NPLit ⫽Non performing loans ratio at the level of bankiat yeart

CRit ⫽Cash recovery ratio at the level of bankiat yeart

LRit ⫽Loan loss reserve ratio at the level of bankiat yeart

CIit ⫽Cost to income ratio at the level of bankiat yeart

ADit ⫽Administrative expense ratio at the level of bankiat yeart

ROEit ⫽Return on equity ratio at the level of bankiat yeart

ROAit ⫽Return on assets ratio at the level of bankiat yeart

NIMit ⫽non interest margin ratio at the level of bankiat yeart

L/Dit ⫽Loans over deposits ratio at the level of bankiat yeart

LAit ⫽Liquid assets ratio at the level of bankiat yeart

PEit ⫽Price per earnings ratio at the level of bankiat yeart

71

Islamic banking

CDUM ⫽Country dummy

ODUM ⫽Ownership dummy

Additionally, in this research we use a panel data set, as each bank covered has repeated measurements at a specific point in time. An analysis of the data set was required to decide on the type of the regression model to use in the study. The first stage in the data analysis is to clarify the appropriate model that would fit the data. The two main approaches that will fit panel data are acknowledged as fixed- and random-effects regression models. This study tests the data under fixed- and random-effects models, and then selects the most appropriate one based on the Hausman test (Hausman, 1978). Hausman’s specification test evaluates the significance of an estimator versus an alternative one. The results of Hausman’s test point toward the use of random-effects regression in all parts of the study.

4. Data collection

Due to the global expansion of Islamic banking, this research will undertake a global coverage based on the geographical distribution of Islamic banking by region. The sample consists of 25 Islamic banks in 18 different countries all over the world. The

Table IV.

Descriptive statistics for profit sharing and banks’ performance: CAMELS approach

Variables

Number of

observations Mean

Standard

deviation Minimum Maximum CV

PDR 78 0.428 0.202 0.025 0.918 0.473

CAR 78 0.335 0.627 0.094 4.215 1.873

NPL 78 0.048 0.045 0.000 0.200 0.947

CR 78 0.147 0.890 0.000 7.871 6.045

LR 78 0.894 1.086 0.000 6.168 1.215

CI 78 0.706 1.090 0.119 6.920 1.545

AD 78 0.583 0.266 ⫺0.497 1.021 0.456

ROE 78 0.097 0.168 ⫺0.565 0.471 1.735

ROA 78 0.020 0.033 ⫺0.075 0.134 1.673

NIM 78 0.269 0.685 ⫺1.092 5.316 2.553

L/D 78 0.740 0.349 0.012 2.073 0.472

LA 78 0.425 0.170 0.176 0.891 0.400

PE 79 11.601 12.420 ⫺8.000 81.000 1.071

Notes: Speaking of publicly listed Islamic banks. The average profit distribution ratio is around 42 per cent, ranging from 2 to 91 per cent. Islamic banks have a high capital adequacy ratio amounted to 35 per cent when comparing their equity capital to their assets weighted by risk. Besides, Islamic banks have moderate non-performing loans ratio equal to 4.7 per cent and which can increase up to 19 per cent. Yet, from their default loans, listed Islamic banks succeed in collecting14 per cent as cash recovery. Also, one way to cope with loan default is to keep some reserves to cover potential losses. The average loan loss reserve is 90 per cent from the total loans that are expected to default. Thereby, keeping a high reserve allows Islamic banks to minimize their exposure to default. On the other hand, the cost of running a listed Islamic bank is quite high, as, on average, the cost to income ratio is amounted to 70 per cent, from which 58 per cent is paid as administrative expenses. On the topic of profitability, a listed Islamic bank can make, on average, a 9 per cent return on equity and 2 per cent return on assets, which can grow up to 47 and 13 per cent, respectively. Also, listed Islamic banks are able to generate 70 per cent of their deposits as loans while keeping a relatively high liquidity ratio of 47 per cent

IMEFM

7,1

72

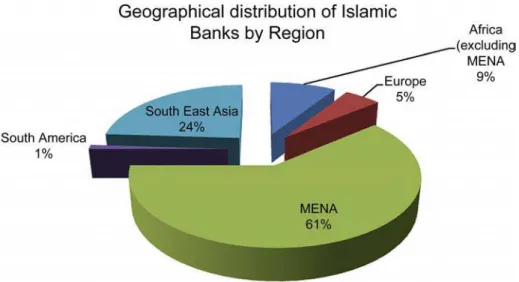

minimum required sample size is five cases for every independent variable in the model; the sample contains 125 observations which exceed the minimal number of data needed. Due to the fact that data on Islamic banking are limitedly accessible, the sample is representative to the extent that it covers all the banks that publish annual reports and for which data are publicly available. The fact that data about some Islamic banks are not accessible can provide on one hand an idea about its low transparency and on the other hand that there is no basis for the assessment concerning its profit distribution practices. In addition, some studies used well-established banks to assess the transparency in Islamic banking due to the fact that they have a higher proportion of PLS contracts in their assets. That is why within each country, well-established Islamic banks[3] would be included in the sample. The research will use yearly data over five financial periods per bank between 2006 and 2010. Due to lack of available data, a five-year data collection period is assumed to detect and capture any variation in the financial reports for all the banks in all the countries through time. The main regions included in the sample are Africa (excluding Middle East and North Africa, MENA),

Europe, MENA and Asia (seeAppendix 1for sample details).

5. Results

5.1 Impact of transparency on profit distribution

The research once predicted that enhancing quantitative as well as qualitative disclosure will induce banks to distribute more profit to their IAHs; precisely the same has been proven true. The overall model significance has confirmed that transparency in Islamic banks is of vital importance due to the existence of profit-sharing arrangements (Table V).

Outcomes from equation (1) show that the GEN is highly significant at less than 1 per cent level of significance. GEN has a positive impact on the share of profit distributed to IAHs. This can be related to the fact that this GEN includes all necessary information for all types of depositors. As a result, relevant disclosure about governance arrangement for IAHs’ funds, strategy of assets trading, management duties toward IAHs’ funds and methodology for profit distribution will help market participants in general and IAHs in

Table V.

Relationship between profit distribution ratio and transparency ratios

Equation (1) Coefficient p-value

GEN 0.8391413*** 0.000

UIA 0.2759487** 0.026

RIA 0.2352547** 0.014

GTR – –

ODUM ⫺0.0608641** 0.021

CDUM 0.1435167*** 0.003

Cons ⫺0.0466303 0.279

Wald chi2(5) 213.24 0.0000

Number of observations 123.00

Number of groups 25.00

Notes: The table shows the relationship between profit-sharing ratio allocated to investment holders and the level of transparency in Islamic banks using a generalized least-squares regression; * represents coefficient significant at the level of 10 per cent, ** for those significant at 5 per cent, *** for those significant at 1 per cent; (–) omitted because of collinearity

73

Islamic banking

particular assessing the Islamic banks’ ethical responsibility and credibility as well as interpreting and understanding Islamic banks’ operational and risk profile.

The UIA ratio is significant at 5 per cent significance level; the more quality and quantity information disclosed about UIA, the greater the proportion of profit allocated to depositors. Strictly speaking, some Islamic banks tempt to invest in risky portfolios to take advantage of the fact that UIA holders can absorb potential losses. Lowering transparency and benefiting from moral hazard induce Islamic banks to manipulate

profit distribution ratio as a result of high information asymmetry (Hyytinnen and

Takalo, 2002). Obviously, transparency is asymmetrical, as some parties involved can have access to more information than others. For instance, Islamic banks’ shareholders can have private signals from insiders about a negative outcome, so that they can withdraw their money early. In this case, UIA holders will incur losses that will be generated by the bank. Thereby, enhancing transparency by disclosing essential information regarding unrestricted IAHs such as the percentage of funds invested taken form UIA, types of assets in which those funds have been invested and average quoted rate of return will make it easier to detect if the bank is passing on risk to their UIA holders.

At a 5 per cent significance level, RIA transparency ratio is found to be significantly positively related to share of profit allocated to depositors. Even if RIAs are classified as off balance sheet items and they do have the right to decide where to invest their money, with more disclosure they can control Islamic banks more efficiently and make the timely switch to a better fund manager if they notice a mismanagement undertaken by the current bank.

Additionally, ownership dummy was found to be significant at 5 per cent level. The study predicted that listed Islamic banks will distribute more profit to depositors compared to unlisted Islamic banks. Precisely the opposite has proven to be true. One possible explanation is the fact that publicly listed Islamic banks will be prone to external scrutiny by bank supervisors, auditors and financial analysts who continuously watch the banks’ actions. The latter makes listed Islamic banks more transparent relative to unlisted ones. Thereby, unlisted Islamic banks tend to distribute more profit compared to Islamic banks as a symbol of transparency enhancement. In the same context, country dummy is significant at the level of 1 per cent. This implies that Islamic banks located in developed markets will tend to distribute more profit to depositors relative to developing countries. These results are aligned with the regulations of such countries. For instance, some country regulators such as central banks require Islamic banks to avoid charging losses to IAHs and to smooth periodic returns to them.

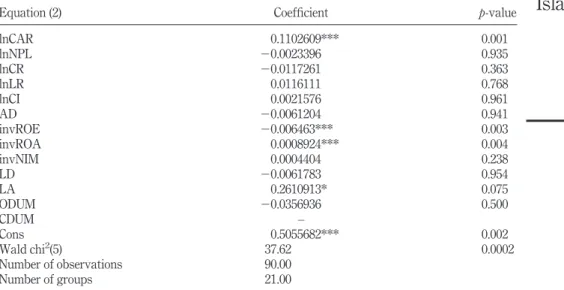

5.2 Impact of Islamic banks’ performance on profit distribution: CAMEL approach The relationship between profit sharing and Islamic banks’ performance is statistically significant at the level of 1 per cent. The study hypothesized that higher banks’ performance will induce them to distribute more profit to depositors, and the result of

equation (2) has proven evidence that performance is associated with profit-sharing

level significantly (Table VI).

The first dimension of performance is capital adequacy ratio, the latter is found to be positive and significant at 1 per cent level. This outcome is explained by the principle that banks need to raise adequate capital in a way to absorb losses. Yet, as Islamic banks

IMEFM

7,1

74

operate under PLS arrangement, they do not raise capital and transfer the loss to PSIAHs. Under this case, profit shared will be lowered due to the transferability of the loss account to IAHs. As a result, a higher capital adequacy ratio entails that Islamic banks have sufficient capital that can keep them out of difficulty, which make them less prone to profit distribution management.

The profitability and earnings dimension in CAMEL framework is also highly significant at a level of 1 per cent. Return on equity has a positive impact on profit distribution ratio. The relationship between return on equity and profit distribution appears to be straightforward. The higher return generated signaling good performance, the higher value created to shareholders, the more willingness to share part of this value to depositors. On the other hand, return on asset impacts negatively the profit-sharing ratio to the depositors. The latter result is significant at the level of 1 per cent. The ROA upshot can be explained by the simple reason that Islamic banks rely heavily on the funding base whose cost depends on the return of its assets as opposed to conventional banks that make profit from the difference of interest rate charged to loans and deposits. As a matter of fact, Islamic banks are not in a position to share their profits with their IAHs, as return generated from assets is defined as the final wealth generated by the bank and attributed to its owners (Hassoune, 2002).

Another notable significance is the impact of liquidity on profit distribution. This proxy of performance is statistically significant at 10 per cent level. The research predicted that higher liquidity will drive Islamic banks to manage less profit-sharing ratio and allocate more profit to IAHs. This prediction has been proven by results of equation (2). The result sheds light on the major concern of any bank, which is liquidity. All banks are working toward the avoidance of mismatching assets and liabilities by

Table VI.

Banks’ performance impact on profit distribution: CAMEL approach

Equation (2) Coefficient p-value

lnCAR 0.1102609*** 0.001

lnNPL ⫺0.0023396 0.935

lnCR ⫺0.0117261 0.363

lnLR 0.0116111 0.768

lnCI 0.0021576 0.961

AD ⫺0.0061204 0.941

invROE ⫺0.006463*** 0.003

invROA 0.0008924*** 0.004

invNIM 0.0004404 0.238

LD ⫺0.0061783 0.954

LA 0.2610913* 0.075

ODUM ⫺0.0356936 0.500

CDUM –

Cons 0.5055682*** 0.002

Wald chi2(5) 37.62 0.0002

Number of observations 90.00

Number of groups 21.00

Notes: The table illustrates the relationship between profit-sharing ratio allocated to investment holders and the performance level of Islamic banks using generalized least-squares regression; * represents coefficient significant at the level of 10 per cent, ** for those significant at 5 per cent, *** for those significant at 1 per cent; (–) omitted because of collinearity

75

Islamic banking

maturity. The study considered liquid assets as those with maturity up to three months. This means that if an Islamic bank places its funds in assets with maturity more than three months, it will restrict its profitability and will be less willing to distribute profit to depositors (Archer and Abdel Karim, 2009). The other way around, higher liquidity ratio will help Islamic banks generate substantial profit and improve its performance, driving them to distribute more profit to depositors.

This justification rests, asIFSB (2011)notes, a major concern for IAHs. For one

reason, Islamic banks have full discretion to make use of deposits when managing unrestricted IAHs’ funds without denoting where, how and for which purpose those funds are to be invested. For another, restricted IAHs make agreement with Islamic banks on how their deposits will be utilized and for what purpose. Exposition of restricted IAHs to rate of return risk in view of the fact that any loss incurred from assets funded by their deposits will be born solely by them may push unrestricted IAHs to withdraw their money from Islamic banking, leading to a liquidity crisis. IFSB’s study establishes a clear idea about the existing relationship between liquidity levels and profit rates, where Islamic banks tend to attract and maintain deposits by providing higher returns.

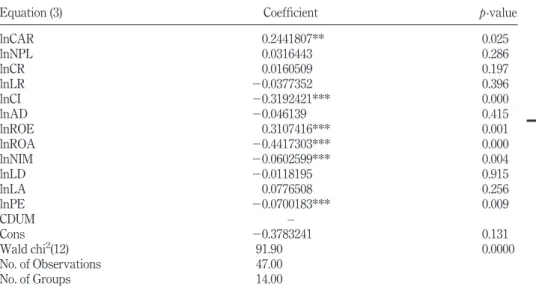

5.3 Impact of Islamic banks’ performance on profit distribution: CAMELS approach CAMELS approach results revealed that Islamic banks’ performance is definitely affecting banks’ intention regarding profit distribution. The overall model of equation (3) is significant at 1 per cent level. The findings indicate that a good performance in all the five aspects of the operations of Islamic banks will promote IAHs’ share of profit. The sensitivity to market risk variable added to this model is also significant, providing evidence that in addition to banks’ operations, IAHs are also affected by the external market risk (Table VII).

If we further analyze the general results, we find that capital adequacy ratio measures respond positively to the profit-sharing ratio at 5 per cent significance level. This result supports the previous findings in equation (2). This implies that a high capital adequacy ratio indicates a good financial health of Islamic banks, which reduces their incentives to manage the profit distribution ratio.

The outcome of equation (3) indicates that the cost to income ratio has a strong role in explaining the distribution of profit to IAHs. The results show that poor performance indicated by a mismanagement of costs incurred relative to income generated will push managers to distribute less profit to depositors. The proxy of management soundness is found to be significant at 1 per cent level. The same conclusion was noticed concerning administrative expenses ratio, meaning that the more a bank is incurring administrative expenses, the less willingness to distribute profit to depositors. The rationale behind it is that the profit margin tends to shrink when cost levels rise, inducing banks to manage profit distribution regarding IAHs in a way to smooth earnings allocated to banks’ shareholders. The latter sheds light on corporate governance issues in Islamic banking. To make it clearer, equity investors, namely, PSIAHs, need to have a corporate governance structure that offers them the required and efficient monitoring of their funds. Unlike shareholders who have the board of directors designed to protect their rights, PSIAHs do not have such mechanism of governance established in Islamic banks. However, some Islamic banks have established governance committees to deal with this issue, but the effectiveness of this mechanism is questionable.

IMEFM

7,1

76

Profitability level as a proxy of good performance is found to affect positively profit-sharing ratio. ROE, ROA as well as NIM are significant at 1 per cent level. The

results of ROE and ROA impact on profit distribution are in line with equation (2)

findings, which give more strength to the outcome. However, NIM turned to be significant in this model at 1 per cent level. Yet, the study predicted that all profitability measures including NIM will impact positively profit distribution ratio, but precisely the opposite has proven true regarding NIM. The counterintuitive finding that higher NIM will make Islamic banks distribute less profit to depositors may be appropriate in terms of assets composition. Basically, Islamic banks rely on contractual structure for fund management activities, namely, Mudarabah. These structures differ from one type of investment account to another. For instance, UIAs appear in Islamic banks’ balance sheet, whereas RIAs are treated as off balance sheet items. The latter creates complication in the supervision of Islamic banks as well as corporate governance problems as described earlier. These complications facilitate the task for Islamic banks to manipulate profit distribution to depositors.

The sixth dimension added to the CAMEL, sensitivity to the market risk, is found to be significant at the level of 1 per cent. Higher price to earnings ratio may raise the concern that the stock market may be headed for a downturn, because Islamic banks’ share prices have become very high relative to their earnings. Some financial analysts who hold this outlook point out that in the past, high price-earnings ratios have usually been followed by slow growth in stock prices (Shen, 2000). Thereby, to be in a position

Table VII.

Banks’ performance impact on profit distribution: CAMELS approach

Equation (3) Coefficient p-value

lnCAR 0.2441807** 0.025

lnNPL 0.0316443 0.286

lnCR 0.0160509 0.197

lnLR ⫺0.0377352 0.396

lnCI ⫺0.3192421*** 0.000

lnAD ⫺0.046139 0.415

lnROE 0.3107416*** 0.001

lnROA ⫺0.4417303*** 0.000

lnNIM ⫺0.0602599*** 0.004

lnLD ⫺0.0118195 0.915

lnLA 0.0776508 0.256

lnPE ⫺0.0700183*** 0.009

CDUM –

Cons ⫺0.3783241 0.131

Wald chi2(12) 91.90 0.0000

No. of Observations 47.00

No. of Groups 14.00

Notes: The table shows regression results using generalized least-squares model. The dependent variable is the profit distribution ratio and the IVs are CAMELS ratios. Also country dummy is added to the model as a control variable. This idea behind adding this model is to assess the effect of sensitivity to market on the profit-sharing issues; * represents coefficient significant at the level of 10 per cent, ** for those significant at 5 per cent, *** for those significant at 1 per cent; (–) omitted because of collinearity

77

Islamic banking

to face a potential risk from the external market, Islamic banks may be tempted to allocate part of their profit as a reserve on the expense of distributing less to their depositors. This evidence reveals that higher sensitivity to the market risk will affect negatively Islamic banks’ performance, which in turn drives profit-sharing ratio downturn.

6. Conclusions and recommendations

This paper has exposed the key issues regarding transparency in Islamic banks. It has identified that general disclosure of qualitative and quantitative information will enhance the transparency of Islamic banks. The latter will serve as a foundation for depositors’ confidence by giving them better ability to monitor and investigate management of their investments. It is worth stressing that beside general disclosure, disseminating information about specific types of depositors will improve banks’ transparency. As such, Islamic banks will be more willing to distribute profit to depositors because transparency prevents banks from withholding information, thereby the incentive to cheat is reduced.

Interestingly, this research reveals that banks’ performance is significantly and positively related to profit-sharing ratio. This outcome is intuitive and consistent with prior literature. It points out that adequate capital plays strong empirical evidence toward profit sharing. This means that Islamic banks are more eager to distribute profit when they have enough capital to cover probable losses, created high value to shareholders as well as high liquidity levels.

All the conclusions drawn from the results of this study provide new insights into the Islamic banking field. Although prior literature provides qualitative analysis of the issue of transparency in Islamic banking, this research strengthens prior arguments by providing empirical evidence regarding the impact of transparency and performance on profit distribution. Previous studies have been limited on the subject of the impact of performance of profit allocation, while this study provides insights concerning the existence of a direct positive relationship between the two.

The study outcome is vital to many parties involved in the Islamic banking field and can be taken as a strong foundation to make appropriate actions that would help grow and sustain Islamic banking development globally. Room for improvement still exists. Islamic banking regulators should impose on Islamic banks to adopt strict rules and policies regarding the management of PSIAHs’ funds such as a mandatory establishment of a corporate governance committee that will endeavor to protect PSIAHs’ rights from any potential mismanagement of their funds as well as profit. Regulatory authorities must examine and scrutinize Islamic banks’ appliance to IFSB disclosure, making the latter a necessary component of a sound regulatory framework governing the Islamic banking industry. An effective enforcement of transparency policies such as the standards issued by the IFSB will reduce Islamic banks’ opaqueness and eliminate potential incentives of profit manipulation. Hence, this research generated important quantitative findings in the field of Islamic banking.

The main limitation of this study is data availability. Even with this moderate sample size, we tried to ensure a representative distribution of the population. Another limitation that needs to be pointed concerns the sensitivity to the market factors included in the CAMELS framework. Future research can consider increasing the

IMEFM

7,1

78

sample size even further, as well as adding more market sensitivity variables to assess their significance and impact on profit distribution.

Notes

1. Islamic Finance Magazine, November 2011. 2. Also referred to as IAHs.

3. Well-established Islamic banks listed by the Global Finance magazine.

References

Archer, S. and Abdel Karim, R. (2009), “Profit-sharing investment accounts in Islamic banks: regulatory problems and possible solutions”, Journal of Banking Regulation, Vol. 10, pp. 300-306.

Ariffin, N., Archer, S. and Abdel Karim, R. (2009), “Issues of transparency in Islamic banks”,

Review of Islamic Economics, Vol. 13 No. 1, pp. 89-104.

Association of Islamic Banking Institutions Malaysia (2011), “Islamic finance”, available at:http:// aibim.com/content/view/17/34/(accessed 10 July 2011).

Awan, A. (2009), “Comparison of Islamic and conventional banking in Pakistan”, Working Paper, Department of Economics, Islamia University, Bahawalpur.

Basel Committee on Banking Supervision (1998), “Enhancing banking transparency”, No. 41, available at:www.bis.org/publ/bcbs41.pdf(accessed 2 September 2011).

Cihak, M. and Hesse, H. (2008), “Islamic banks and financial stability: an empirical analysis”, Working Paper No. 8/16, Monetary and Capital Markets Department, International Monetary Fund, Washington, DC.

Core, J., Holthausen, R. and Larcker, D. (1999), “Corporate governance, chief executive officer compensation, and firm performance”,Journal of Financial Economics, Vol. 51, pp. 371-406. Diefenbach, T. (2003),Internal Value Added and Profit Distribution: A Contribution-Orientated Model of Internal Remuneration of the Factors of Production and Proportional Profit-Sharing, Chemnitz University of Technology, Chemnitz, available at:

www.econ.cam.ac.uk/cjeconf/delegates/diefenbach.pdf(accessed 15 July 2011).

Dincer, N. and Eichengreen, B. (2007), “Central bank transparency: where, why, and with what effects?”, Working Paper No. 13003, National Bureau of Economic Research, Cambridge, MA.

Dobb, M. (1973),Theories of Value and Distribution since Adam Smith: Ideology and Economic Theory, Cambridge University Press, Cambridge.

El Tegani, A. (1996), “Distribution of profits in Islamic banking: a case study of Faysal Islamic Bank of Sudan (FIBS)”,Islamic Economics, Vol. 8, pp. 15-32.

Emirguc-Kunt, A. and Huizinga, H. (2000), “Financial structure and bank profitability”, Policy Research Working Paper no. 2430.

Errico, L. and Farahbaksh, M. (1998), “Islamic banking: issues in prudential regulations and supervision”, available at: www.imf.org/external/pubs/ft/wp/wp9830.pdf (accessed 30 October 2012).

Fama, E. and French, K. (2001), “Disappearing dividends: changing firm characteristics or lower propensity to pay”,Journal of Financial Economics, Vol. 60, pp. 3-43.

Farook, S., Hassan, M. and Clinch, G. (2012), “Profit distribution management by Islamic banks: an empirical investigation”, The Quarterly Review of Economics and Finance, Vol. 52, pp. 333-347.

79

Islamic banking

Farvaque, E., Refait-Alexandre, C. and Weill, L. (2011), “Are transparent banks more efficient? Evidence from Russia”,Eastern European Economics, Vol. 50, pp. 63-81.

Ghayad, R. (2008), “Corporate governance and the global performance of Islamic banks”,

Humanomics, Vol. 24 No. 3, pp. 207-216.

Goldberg, L. and Rai, A. (1996), “The structure-performance relationship for European banking”,

Journal of Banking and Finance, Vol. 20, pp. 745-771.

Haller, A. (1998), “Value added in financial accounting”,Advances in International Accounting, Vol. 58 No. 2, pp. 261-265.

Hasbi, H. and Haruman, T. (2011), “Banking: according to Islamic Shariah concepts and its performance in Indonesia”,International Review of Business Research Papers, Vol. 7 No. 1, pp. 60-76.

Hassan, M.K. and Bashir, A.M. (2003), “Determinants of Islamic banking profitability”, ERF paper.

Hassoune, A. (2002), “Islamic banks’ profitability in an interest rate cycle”,International Journal of Islamic Financial Services, Vol. 4 No. 2, pp. 54-58.

Hausman, J. (1978), “Specification tests in econometrics”, Econometrica, Vol. 46 No. 6, pp. 1251-1271.

Humayon, A. and Presley, R. (2000), “Lack of profit loss sharing in Islamic banking: management and control imbalances”,International Journal of Islamic Financial Services, Vol. 2 No. 2, pp. 1-16.

Hyytinnen, A. and Takalo, T. (2002), “Enhancing bank transparency: a reassessment”,European Finance Review, Vol. 6, pp. 429-445.

International Monetary Fund (2006), “Financial soundness indicators”, available at:www.imf.org/ external/pubs/ft/fsi/guide/2006/index.htm(accessed 10 July 2011).

Islamic Financial Services Board (2007), “Disclosures to promote transparency and market discipline for institutions offering Islamic financial services (Excluding Islamic Insurance (Takaful) Institutions And Islamic Mutual Funds)”, available at:www.ifsb.org/standard/ ifsb4.pdf?&lang⫽en_us&output⫽json http://sbp.gov.pk/ibd/2007/ifsbsurvey-05-Apr-07. pdf?&lang⫽en_us&output⫽json(accessed 5 September 2011).

Islamic Financial Services Board (2011), “Guiding principles on liquidity risk management for institutions offering Islamic financial services”, available at: www.cbb.gov.bh/assets/ Consultations/ED-12%20Liquidity%20Risk%20Mgmt%20for%20IIFS%20(2011-10-12).pdf(accessed 1 November 2012).

Jensen, M. and Meckling, W. (1986), “Agency costs of free cash flow, corporate finance, and takeovers”,American Economic Review, Vol. 76, pp. 323-329.

Khaldi, K. and Hamdouni, A. (2011), “Islamic financial intermediation: equity, efficiency and risk”,

International Research Journal of Finance and Economics, Vol. 65, pp. 145-160.

Manoj, K. (2010), “Financial soundness of old private sector banks (OPBs) in India and benchmarking the Kerala based OPBs: a ‘CAMEL’ approach”, American Journal of Scientific Research, Vol. 11, pp. 132-149.

Mubarak, M. (2004), “The financial performance analysis using CAMEL approach at bank Shariah Mandiri”, Working Paper, University of Muhammadyah Malang, Malang, Indonesia.

Myers, S. and Majluf, N. (1999), “Corporate financing and investment decisions when firms have information that investors do not have”,Journal of Financial Economics, Vol. 13, pp. 187-221.

IMEFM

7,1

80

Nurazi, R. and Evans, M. (2005), “An Indonesian study of the use of CAMEL(S) ratios as predictors of bank failure”,Journal of Economic and Social Policy, Vol. 10 No. 1, article 6, available at:

http://epubs.scu.edu.au/jesp/vol10/iss1/6, pp. 1-23.

Routledge, J. and Gadenne, D. (2000), “Financial distress, reorganisation and corporate performance”,Accounting and Finance, Vol. 40, pp. 233-260.

Samad, A., Gardner, N.D. and Cook, B.J. (2005), “Islamic banking and finance in theory and practice: the experience of Malaysia and Bahrain”,The American Journal of Islamic Social Sciences, Vol. 22 No. 2, pp. 69-86.

Sari, D. (2007), “The implementing of CAMEL method as a tool for assessing financial performance at Islamic commercial bank”, Working Paper, University of Muhammadyah Malang, Malang, Indonesia.

Sarker, A. (2006), “CAMELS rating system in the context of Islamic Banking: a proposed ‘S’ for Shariah framework”,Journal of Islamic Economics, Banking and Finance, Vol. 2 No. 2, pp. 78-84.

Shen, P. (2000), “The P/E ratio and stock market performance”,Economic Review of the Federal Reserve Bank of Kansas City, pp. 23-36.

Standard and Poor’s, (2010), “Transparency and disclosure by Russian Banks 2010”, available at:

www.vedomosti.ru/research/getfile/429/613_T%26D_Russia_2010_ENG.pdf(accessed 25 September 2011).

Wijaya, A. (2008), “Islamic banking at 2008: evaluation, trend, and projection”,Journal of Karim Review, Special Edition, Vol. 1, pp.1-15.

Appendix 1. Data collection

Figure A1presents Islamic banking distribution by region.

Figure A1.

Islamic banking distribution by region

81

Islamic banking

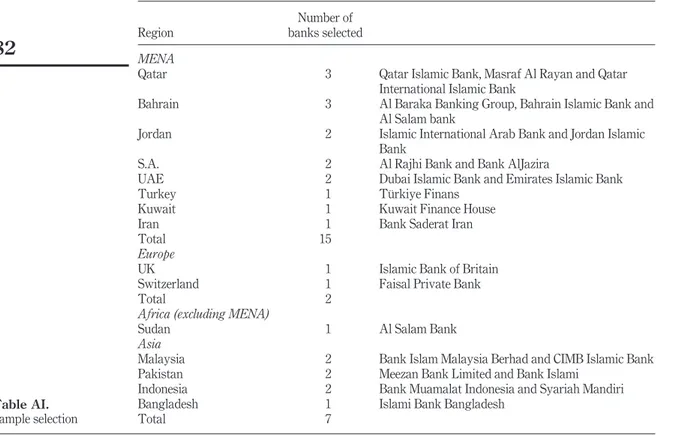

Table AIandTable AIIprovide sample details.

Table AI.

Sample selection

Region

Number of banks selected

MENA

Qatar 3 Qatar Islamic Bank, Masraf Al Rayan and Qatar International Islamic Bank

Bahrain 3 Al Baraka Banking Group, Bahrain Islamic Bank and Al Salam bank

Jordan 2 Islamic International Arab Bank and Jordan Islamic Bank

S.A. 2 Al Rajhi Bank and Bank AlJazira

UAE 2 Dubai Islamic Bank and Emirates Islamic Bank

Turkey 1 Türkiye Finans

Kuwait 1 Kuwait Finance House

Iran 1 Bank Saderat Iran

Total 15

Europe

UK 1 Islamic Bank of Britain

Switzerland 1 Faisal Private Bank

Total 2

Africa (excluding MENA)

Sudan 1 Al Salam Bank

Asia

Malaysia 2 Bank Islam Malaysia Berhad and CIMB Islamic Bank

Pakistan 2 Meezan Bank Limited and Bank Islami

Indonesia 2 Bank Muamalat Indonesia and Syariah Mandiri

Bangladesh 1 Islami Bank Bangladesh

Total 7

IMEFM

7,1

82

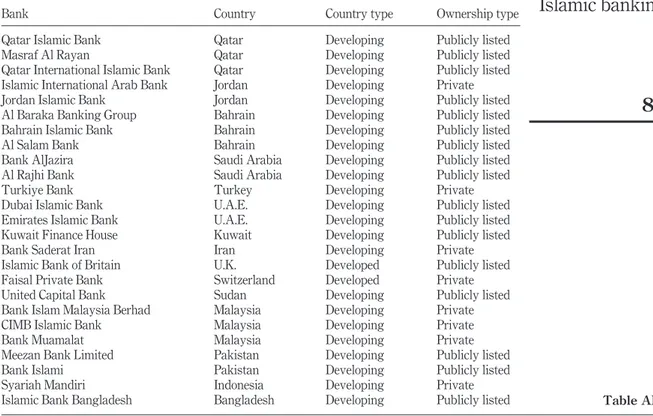

Table AII.

Bank Country Country type Ownership type

Qatar Islamic Bank Qatar Developing Publicly listed

Masraf Al Rayan Qatar Developing Publicly listed

Qatar International Islamic Bank Qatar Developing Publicly listed Islamic International Arab Bank Jordan Developing Private

Jordan Islamic Bank Jordan Developing Publicly listed

Al Baraka Banking Group Bahrain Developing Publicly listed Bahrain Islamic Bank Bahrain Developing Publicly listed

Al Salam Bank Bahrain Developing Publicly listed

Bank AlJazira Saudi Arabia Developing Publicly listed

Al Rajhi Bank Saudi Arabia Developing Publicly listed

Turkiye Bank Turkey Developing Private

Dubai Islamic Bank U.A.E. D