iv

FACTORS INFLUENCING THE FINANCIAL PERFORMANCE IN

INDONESIAN LOCAL GOVERNMENTS

THESIS

A thesis submitted in partial fulfillment of the

requirement for the degree of Magister Sains

By

OKI KUNTARYANTO

NIM: S4307088

FAKULTAS EKONOMI

UNIVERSITAS SEBELAS MARET

SURAKARTA

v

FACTORS INFLUENCING THE FINANCIAL PERFORMANCE IN INDONESIAN

LOCAL GOVERNMENT

By:

OKI KUNTARYANTO

NIM: S4307088

Has been approved by supervisors

On:

Supervisor Co supervisor

Prof. Dr. Bambang Sutopo, M.Com. Ak Doddy Setiawan, S.E. M.Si., IMRI., Ak

NIP. 19520610 198803 1 002 NIP. 19750218 20012 1 001

Acknowledged by

Head of Master of Accounting Program

vi

FACTORS INFLUENCING THE FINANCIAL PERFORMANCE IN INDONESIAN

LOCAL GOVERNMENT

By:

OKI KUNTARYANTO

NIM: S4307088

Has been approved by examiners

On,

Chairman

: Drs. Djoko Suhardjanto, M.Com (Hons), Ph.D, Ak

Vice

: Dra. Y. Anni Aryani, M.Proff.Acc, Ph.D., Ak

Member

: Prof. Dr. Bambang Sutopo, M.Com., Ak

vii

STATEMENT

Name

: Oki Kuntaryanto

NIM

: S4307088

I declared truthfully that this thesis entitled Factors Influencing Financial

Performance in Indonesian Local Government is originally made by the researcher. It is

not plagiarism nor made by others. This things related to other people’s works are written

in quotation and included in the bibliography.

If it is later discovered and proven that this statement is not true, the researcher

willingly accept any penalty from the Master of Accounting Program, Fakultas Ekonomi,

Universitas Sebelas Maret.

Surakarta, January 2010

viii

ACKNOWLEDGEMENT

Assalamu’alaikum Wr. Wb.

Alhamdulilah, researcher thanks to the presence of Allah SWT for the overflows of

blesses, grants, and guides so that Researcher able to accomplish this thesis well. This

thesis is compiled to equip the duties and fulfill the preconditions to achieve the Magister

Sains Degree in Faculty of Economics, Universitas Sebelas Maret.

Researcher realizes that during the thesis accomplishment process, there are many

helps from other parties. Herewith, Researcher says many thanks to various following

parties:

1.

Minister of Education of Indonesian Republic, for the willingness to give grants in

form of scholarship “Beasiswa Unggulan Diknas”, in order to complete the study in

Master of Accounting Study Program, Faculty of Economics, Universitas Sebelas

Maret.

2.

Prof. Dr. Bambang Sutopo, M.Com. Ak, as The Dean of Economics Faculty,

Universitas Sebelas Maret and as the thesis supervisor for helps and guidance.

3.

Dr. Bandi, M.Si. Ak, as The Head of Master of Accounting Program Economics

Faculty, Universitas Sebelas Maret.

4.

Mr. Doddy Setiawan as the co-supervisor for helps and guidance.

5.

Mr. Djoko Suhardjanto, M.Com (Hons), Ph.D for your kindness

6.

All lecturers in MAKSI, for their kindness.

ix

Researcher realizes that this works is a long way off from perfection. Hence,

researcher expects the constructive suggestions and criticism. Finally, researcher feels very

sorry if there are mistakes and drawbacks in this thesis.

Wassalamu’alaikum Wr. Wb

Surakarta, January 2010

x

TABLE OF CONTENT

Page

APPROVAL ………

ii

DEDICATION ……… iv

MOTTO ……… v

STATEMENT………..………. vi

ACKNOWLEDGEMENT……….. vii

TABLE OF CONTENT……… ix

LIST OF TABLE………..

xii

LIST OF FIGURE……… . xiii

LIST OF APPENDIX……… xiv

ABSTRACT……….. xv

CHAPTER I. INTRODUCTION………. 1

A.

Research background………. 1

B.

Problem statement……….. 8

C.

Research objective……….. 9

D.

Research importance………... 9

E.

Expected benefits……… 9

F.

Chapter Organization……….. 10

CHAPTER II. LITERATURE REVIEW AND HYPOTHESIS

DEVELOPMENT……… 12

A.

The public sector accounting reform in Indonesia……….. 12

xi

1.

Financial ratio selection………. 17

C.

Exogenous factor selection……… 21

1.

Macroeconomic factor………. 22

2.

Size……….. 31

3.

Geographical factor………. 35

D.

Theoretical framework……….. 42

CHAPTER III. RESEARCH METHOD……… 43

A.

Data collection……….. 43

B.

Population and sample……….. 43

C.

Analysis technique……… 44

D.

Variable identification……….. 46

E.

Operational definition………... 46

CHAPTER IV. DATA ANALYSIS AND DISCUSSION………... 43

A.

Data description……… 49

B.

Data analysis………. 56

1.

Year 2006……… 56

2.

Year 2007……… 60

3.

Two-year analysis……… 64

C.

Discussion………. 68

CHAPTER V. CONCLUSION AND SUGGESTION

A.

Conclusion………. 76

xii

xiii

LIST OF TABLE

Page

Table 1

Ratio calculation………..

47

Table 2

Data description for 2006………

49

Table 3

Data description for 2007……… 50

Table 4

Descriptive statistics for 2006………. 51

Table 5

Descriptive statistics for 2007……….

54

Table 6

OLS assumption for 2006………...

56

Table 7

Collinearity test for 2006……….

57

Table 8

Hypothesis test result for 2006………

58

Table 9

OLS assumption for 2007………...

61

Table 10

Collinearity test for 2007……….

62

Table 11

Hypothesis test result for 2007………

63

Table 12

Panel analysis assumption……… 65

xiv

LIST OF FIGURE

xv

LIST OF APPENDIX

Page

Appendix I.

Sample of local government for 2006……… 79

Appendix II. Sample of local government for 2007……… 80

Appendix III. Data Analysis for 2006………... 81

Appendix IV. Data Analysis for 2007……… 90

xvi

ABSTRACT

Oki Kuntaryanto

NIM: S4307088

FACTORS INFLUENCING FINANCIAL PERFORMANCE IN INDONESIAN

LOCAL GOVERNMENTS

The use of financial ratios to measure financial performance is a common practice in

private sector. However, this research uses those ratios and applies them in public sector.

This research is a modified replication from Cohen (2008) which investigates factors

influencing financial performance in Indonesian local governments. Financial

performance is represented by financial ratios comprising profitability ratios, short term

solvency ratio, capital structure ratios and performance ratios. The conjectured factors

which influence financial performance are macroeconomic factors represented by GRDP

and inflation, size represented by population, and geographical factors represented by

administrative status of local governments and island-based location of local governments.

This research employs audited financial reports from 281 local governments for

2006 and 255 local governments for 2007. The financial reports included in data analysis

are those which do not have adverse and disclaimer opinions. Ordinary least squares

regression technique is employed for testing the hypothesis for cross-sectional data. In

addition, panel analysis is employed to test the time change effect.

This research finds that macroeconomic factors represented by GRDP and inflation

influence all financial ratios except capital structure ratio. Size represented by population

influences all financial ratios except performance ratios. Geographical factors represented

by administrative status of local government influence all financial ratios. However,

geographical factors represented by island-based location of local government does not

influence debt related ratios.

Keywords: Financial performance, Financial ratios, Local governments, Indonesia,

Macroeconomic factors, Size, Geographical factors

xvii

Oki Kuntaryanto

NIM: S4307088

FAKTOR-FAKTOR YANG MEMPENGARUHI KINERJA KEUANGAN

PEMERINTAH DAERAH DI INDONESIA

Penggunaan rasio keuangan untuk mengukur kinerja keuangan umum digunakan

oleh sektor privat. Namun, penelitian ini menerapkan rasio keuangan tersebut pada sektor

publik. Penelitian ini merupakan replikasi dari Cohen (2008) yang meneliti faktor-faktor

yang mempengaruhi kinerja keuangan pemerintah daerah di Indonesia. Kinerja keuangan

direpresentasikan oleh rasio-rasio keuangan yang terdiri atas rasio profitabilitas, rasio

solvensi jangka pendek, rasio struktur modal, dan rasio kinerja. Faktor-faktor yang diduga

berpengaruh terhadap kinerja keuangan meliputi faktor makroekonomi yang

direpresentasikan oleh PDRB dan inflasi, faktor ukuran yang direpresentasikan oleh

jumlah penduduk, serta faktor geografis yang direpresentasikan oleh status administratif

pemerintah daerah dan lokasi pemerintah daerah berdasarkan pulau.

Penelitian ini menggunakan laporan keuangan pemerintah daerah auditan yang

terdiri atas 281 pemerintah daerah pada tahun 2006 dan 255 pemerintah daerah pada

tahun 2007. Laporan keuangan yang dianggap memenuhi kriteria sampel adalah laporan

keuangan yang tidak diberi opini tidak wajar dan disclaimer oleh auditor. Pengujian

hipotesis menggunakan teknik statistik ordinary least squares (OLS) untuk data

cross-sectional. Sebagai tambahan, analisis panel digunakan untuk menguji model yang

melibatkan pengaruh waktu (time-series effect).

Penelitian ini menemukan bahwa variabel makroekonomi berpengaruh terhadap

semua rasio keuangan kecuali rasio struktur modal. Faktor ukuran yang direpresentasikan

oleh jumlah penduduk berpengaruh terhadap semua rasio keuangan kecuali rasio kinerja.

Faktor geografis yang direpresentasikan oleh status administrative pemerintah daerah

berpengaruh terhadap semua rasio keuangan. Akan tetapi, faktor geografis yang

direpresentasikan oleh lokasi pemerintah daerah berbasis pulau tidak berpengaruh

terhadap rasio keuangan terkait hutang.

Kata Kunci: Kinerja keuangan, Rasio keuangan, Pemerintah daerah, Indonesia, Faktor

makroekonomi, Ukuran, Faktor geografis.

xviii

CHAPTER I

INTRODUCTION

A. Research Background

The Governm ent Rul e Number 24 Year 2005 r equir es t he government ent it ies pr epar e audit able financial st at em ent s in order t o increase t ransparency and account abilit y. The rule also

requires t hat t he f inancial st at ement s must implement t he cash t ow ard accrual basis w hich means t hat revenue, expendit ur e and f inancing must be recognized using cash basis and asset , liabilit y, and equit y must be recognized using accrual basis.

The implem ent at ion of accrual basis in public sect or ent it ies in Indonesia is not a revolut ion. It t akes a long t im e span for t his count r y t o implem ent it . The eff or t on r eforming public sect or account ing had been begun in 1980 conduct ed by M inist ry of Finance from init iat ing a modernizat ion of governm ent account ing syst em st udy unt il t he issuance of Gover nm ent Rule Number 24 Year 2005 about Governm ent al Account ing St andard (Soegijant o and Hoesada, 2005).

The decent ralizat ion era enabl es t he local gover nment s t o w iden t heir aut horit ies in est ablishing t he governm ent al af fairs. Aut horit ies t o est ablish t he governm ent al affairs are expanded t o all aut horit ies except for five aut horit ies t hat r emain t o be t he aut horit ies of cent ral governm ent . The five aut horit ies ar e def ense affair, t he securit y affair, t he monet ar y affair t hat belongs t o cent ral bank, t he religion af fair and int ernat ional affair.

xix

revenue it self does not st and alone in composing t he w hole local government r evenue. According t o The Law , local government r evenue is composed f rom t hr ee main sources; local governm ent

original revenue, count er balance fund and ot her legal revenues. In financial t erms, decent ralizat ion concept s r equire t he local gover nment be more independent from t he dependence on cent ral government subsidies. M ardiasmo (2002) st at es t hat befor e t he implement at ion of regional aut onomy, t her e w as a big expect at ion from local government s t o develop t heir ow n r egion based on t he original capabilit ies and w ills, but in f act , t he local governm ent s ar e t rapped in bigger dependence on cent ral governm ent s subsidies. Set iaji and Adi (2007) find t hat t he share of local government original revenue t o r egional expendit ur e during aut onom y era show s no improvement because t he local governm ent s st ill have st r ong dependence on cent ral government subsidy.

The t ranspar ency and account abilit y mat t ers also becom e int er est ing t opic as t he pow ers of local government t o manage t heir fund are bigger t han t he era befor e aut onomy. M ardiasmo (2003) st at es t hat account abilit y pat t ern befor e t he issuance of St at e Finance Law package w as a horizont al pat t ern in nat ur e. It means t hat t he local governm ent execut ive is responsible for bot h local parliament and t he w hole soci et y. How ever, M ardiasmo (2003) finds t hat t he execut ive is mor e r esponsible f or local parliament rat her t han t he societ y as a w hole. The absent of f inancial report ing st andards make t he problem on t ranspar ency aspect . This happens because it limit s t he independent t hird part y t o conduct audit .

xx

t he predet ermined obj ect ives periodically. The Rule also r equires all local governm ent s be t ransparent by r eleasing open and honest financial informat ion t o t he soci et y based on a

judgm ent t hat t he societ y has a right t o know compr ehensively about governm ent ’ s responsibilit y in managing resources and t he obedi ence t o t he posit ive law .

How ever, t her e ar e ot her pr oblems besides t he t ransparency and account abilit y problem. One of t hem is t he perfor mance aspect . The perfor m ance aspect is m ent ioned in Act Number 15 Year 2004 about St at e Finance Audit . The dimensions of performance measur ement s ar e econom y, effect iveness, and efficiency.

Int ernat ional experiences show t hat t he perfor mance measur em ent is an import ant t hing t o do along w it h t he implem ent at ion of accrual basis account ing. Gr eece, for example, in t he M unicipal and Communal Code of 2006 in several inst ances ment ioned t hat t he f inancial perfor mance assessm ent of local government s w ould be mat erialized via financial rat io analysis t hat is expect ed t o be used for benchmarking, t arget set t ing, ident ificat ion of best pract ices and ult imat ely direct ion of subsidies and grant s on t he basis of rat ional and just if ied argum ent s (Cohen, 2008).

xxi

Adi (2007) f inds t hat f inancial performance index during regional aut onomy is posit ively different from pr e aut onomy era. Adi (2007) also f inds t hat t he economic grow t h has st rong

influence t o t he financial perfor mance. Set iaji and Adi (2007) f ind t hat t he port ion of Local governm ent original revenue t o regional expendit ur e during aut onom y era has no diff erence f rom pre aut onom y era but t he grow t h of local governm ent original revenue during aut onom y has posit ive differ ence from pr e aut onomy era. Set yaw an and Adi (2008) find t hat f iscal st ress posit ively influences t he grow t h of capit al expendit ure and fiscal st r ess during t he aut onom y er a has st ronger ef f ect on t he gr ow t h of local gover nm ent original revenue and capit al expendit ur e rat her t han t he impact of fiscal st ress before aut onom y era.

xxii

This research is also a modified replicat ion f rom Cohen (2008). The r eason t o r eplicat e Cohen (2008) is t o invest igat e fact ors influencing financial perf ormance in Indonesian cont ext in a

mor e compr ehensive manner compar ed t o pr evious researches in Indonesia w hich only invest igat e t he financial performance by emphasizing on t he local governm ent original revenue and relat ed variables influencing it (for example; Adi 2006; Adi 2007; Set iaji and Adi 2007; Ndadar i and Adi 2007; Set yaw an and Adi 2008; and Abdullah and Halim 2003). The pr evious researches also use local governm ent s in Java and Bali as t heir samples. Thus, t his r esear ch uses not only local governm ent original relat ed rat ios but also ot her financial rat ios such as profit abil it y rat ios, short -t erm solvency rat io, capit al st ruct ure rat io and performance rat ios t o measur e financial performance. This research also uses mor e samples t hat not only cover Java and Bali but also all local governm ent s in Indonesia. Thus, t his research invest igat es fact ors influencing financial performance in nat ional cont ext .

xxiii

This research t hen incorporat es several new exogenous variables t hat are suit able w it h t he circumst ances w hich exist in Indonesia. Those variables consist of inf lat ion, island-based locat ion

of local governm ent s and administ rat ive st at us of local government s. Inflat ion is a new proxy for macroeconomic fact ors. Island-based locat ion of local governm ent and administ rat ive st at us of local governm ent are t he proxies for geographical fact ors.

xxiv

B. Problem Statement

Financial perf ormance measur ement is st ill a rare t opic in public sect or account ing ar ea, especially in Indonesia. Several previous r esear ches (for exampl e; Adi 2006; Adi 2007; Set iaji and Adi 2007; Ndadari and Adi 2007; Set yaw an and Adi 2008; and Abdullah and Halim 2003) only

invest igat ed t he financial perf or mance by incorporat ing local governm ent original revenue r elat ed rat ios and used sam ples limit ed t o only Java and Bali Island. Thus, it is necessary t o ext end t he financial performance measur ement by adding not only local governm ent original revenue relat ed rat ios but also ot her financial rat ios com monly used in privat e sect or t o get w ider insight s on measur ing financial performance. It is also necessar y t o ext end t he sample t hat not only cover s Java and Bali Island but also all local governm ent s in Indonesia t o get w ider insight s in det er mining f act ors influencing financial perf ormance in nat ional cont ext .

Cohen (2008) has developed t he model in invest igat ing fact ors influencing t he f inancial perfor mance in Greek cont ext . This research t ries t o generalize t he findings from Cohen (2008) in Indonesian cont ext . Thus, t he problem st at em ent s in t his research are as follow:

1. Is financial performance influenced by macroeconomic fact ors? 2. Is financial performance influenced by size?

3. Is financial performance influenced by geographical fact ors?

C. Research Objective

The purpose of this research is to test the factors which influence the financial performance

in Indonesian local governments. The proposed factors will be macroeconomic factors, size, and

xxv

(GRDP) and inflation. Size is represented by the number of population. Geographical factors are

represented by island-based location of local governments and administrative status of local

governments. Thus, this research will provide empirical evidence on factors which influence

financial performances of local governments in Indonesian context.

D. Research Importance

This research is import ant for several reasons. First , it analyses t he financial st at em ent s of a large number of local governm ent s w hich is st ill rare for public sect or sur veys. Second, it analyses t he cont ent of financial st at em ent t hr oughout t im e (i.e. for t w o financial st at em ent years). Thus, t he conclusions ar e not rest rict ed t o one-year dat a. Finally, t he result s may assist policy makers in designing bet t er perf ormance m easur em ent f or t heir supervised organizat ions t hat not only borrow but also ext end and adapt privat e sect or pract i ces t o t he public sect or cont ext .

E. Expected Benefit

This research is expect ed t o be useful in t hree w ays. First , it is expect ed t o gi ve t he cont ribut ion t o t he em er ging st udy of public sect or in Indonesia as t he researches concerning t he public sect or account ing ar e st ill rare. Second, it is expect ed t o gi ve t he pract ice guidance t o t he policy makers (especially for t he cent ral government as t he donat or of f und) in assessing t he perfor mance using t he r esult s of t his research. The t hird benefit expect ed from t his research is t o give t he enrichment t ool for local governm ent s in planning and assessing t heir f inancial perfor mance using not only local governm ent original revenue r elat ed rat ios but also ot her financial rat ios adapt ed from privat e sect or.

F. Chapter Organization

xxvi

Chapter II : LITERATURE REVIEW AND HYPOTHESIS FORM ULATION

This chapt er discusses about account ing ref orm in Indonesia, financial rat io analysis, exogenous fact or select ion, hypot hesis for mulat ions and t heor et ical framew orks.

Chapter III : RESEARCH M ETHOD

This chapt er discusses about r esear ch met hods comprising dat a collect ions, populat ion and sample, operat ional definit ion and variable measur em ent , and analysis t echnique

Chapter IV : DATA ANALYSIS

This chapt er discusses about dat a analysis comprising dat a descript ion, descript ive st at ist ics, result s of hypot hesis t est ing, and discussion

Chapter V : CONCLUSIONS AND SUGGESTIONS

This chapt er discusses about conclusions of t he r esearch, limit at ions, and suggest ions for fut ure researches.

CHAPTER II

LITERATURE REVIEW AND HYPOTHESIS DEVELOPM ENT

xxvii

The public sect or account ing refor m in Indonesia is not a revolut ion. It passes a long journey t hrough phase t o phase. For t he t ime being, t he last phase of t he r eform is signed by t he issuance

of law about st at e finance w hich consist s of Law Num ber 17 Year 2003 about St at e, Act Number 1 Year 2004 About St at e Tr easury and Law Number 15 Year 2004 about St at e Finance Audit . Art icle 32 (1) Act Number 17 Year 2003 about St at e Finance st at es t hat t he r esponsibilit y of budget implement at ion (bot h st at e budget and local gover nment budget ) has t o be report ed in form of financial st at em ent s t hat comply w it h governm ent account ing st andard.

The st ruggle t o r ef orm governm ent al account ing w as st art ed by M inist r y of Finance in 1979-1980 by t he planning of government al account ing syst em modernizat ion st udy but t he realizat ion of t he st udy w as st art ed in 1982 and w as financially sponsored by World Bank (Soegijant o and Hoesada, 2005). Unfort unat ely, t he next phases of account ing ref orm had not t ouched t he int roduct ion of accrual account ing. The refor m process st ill used cash basis account ing unt il t he issuance of st at e finance law packages in 2003 and t hen follow ed by t he issuance of Government Rule No. 24 Year 2005 about Governm ent al Account ing St andard.

The Government al account ing st andard consist s of Concept ual Framew or ks and eleven Government al Account ing St andard St at em ent s (GASS). The eleven of GASS are as f ollow s:

1. GASS 01 Financial St at ement s Pr esent at ion 2. GASS 02 Budget Realizat ion Report

xxviii 8. GASS 08 Const ruct ion in Progress Account ing 9. GASS 09 Liabilit y Account ing

10. GASS 10 Error Correct ion, Change on Account ing Policy and Ext raordinary Event 11. GASS 11 Consolidat ed Financial St at ement s

One of t he import ant point s from t he St andard is t he int roduct ion of accrual basis account ing in report ed financial st at ement s. The Concept ual Framew ork st at es t hat account ing basis used in t he f inancial st at em ent s is cash basis t o acknow ledge r evenues, expendit ur es and financing in budget r ealizat ion repor t . On t he ot her hand, accrual basis is used t o acknow ledge asset s, liabilities and equit ies in balance sheet . The combinat ion of accrual and cash basis account ing is know n as cash t ow ard accrual basis account ing. Indonesia uses t his account ing basis because budget r ealizat ion report adopt s cash account ing basis (M ust ofa, 2008). M ust ofa (2008) also st at es t hat full accrual basis account ing can be applied if Indonesia uses accrual-based budget ing in it s budget ing syst em.

xxix

account ing must be applied t o all t ypes of financial st at em ent s including budget realizat ion report .

Account abilit y is one of rol e expect ed f rom t he public sect or r efor m in Indonesia as st at ed in Governm ent al Account ing St andard. Account abilit y is a disclosure of act ivit ies and f inancial

perfor mance t o t he st akeholders (Schiavo-Campo and Tomasi, 1999). Gillibrand and Hilt on (1998) advocat es t hat t he use of accrual account ing could impr ove account abilit y. In a w ell funct ioning local governm ent budget and managerial st ruct ure, a local government is subject t o account abilit y t o it s cit izens, account abilit y t o public agencies and account abilit y t o higher l evel governm ent s (Schaeffer and Yilmaz, 2008).

Aust ralia is one role model in applying t he accr ual basis account ing in it s local government s. Local government financial report ing r efor ms in Aust ralia in t he lat e 1980s and early 1990s w er e promot ed on t he basis of usefulness for decision making and for enhanced account abilit y purposes. How ever, persist ent crit icism of t he ref or ms cont inue t o be made, including t hose made by councilors and ot her rat epayers w ho oft en appear t o find such informat ion t o be t oo narrow , t oo complex, and oft en bew ildering (Carnegie, 2005).

The availabilit y of f inancial st at ement s in government ent it ies is a for m of t ransparency needs over t he managem ent of public resources. Tr ansparency of infor mat ion especially f inancial and fiscal informat ion should be implem ent ed in a relevant and underst andable for m (Schiavo-Campo and Tomasi, 1999). This not ion aligns w it h the exist ence of Government al Account ing St andard in Indonesia.

xxx

has a right t o know t he governm ent ’s responsibilities in managing ent rust ed r esour ces and governm ent ’s obedience t o t he posit ive law s. The audit able financial st at em ent s by t he supr eme

audit inst it ut ion enable t he local governm ent s t o disclose t he infor mat ion about t he managed resources (SAP, 2005). The t ranspar ency of infor mat ion, especially financial and fiscal informat ion should be r ealized in t he r elevant f or m and easy t o underst and (Schiavo-Campo, 1999). The not ion of t ransparency is also advocat ed by van der Hoek (2005).

B. Financial Ratio Analysis

Financial rat ios are used for all kinds of purposes. Barnes (1987) st at ed t hat t he uses of financial r at ios include t he assessm ent of t he abilit y of a f irm t o pay it s debt s, t he evaluat ion of business and managerial success and even t he st at ut ory r egulat ion of a firm’s perf ormance. Whit t ingt on (1980) ident if ied t w o principles uses of financial rat ios. The t radit ional, normat ive use of t he measur em ent of a firms’ rat io compared w it h a st andard, and t he posit ive use in est imat ing empirical relat ionships, usually for predict ive purposes.

The use of financial rat ios and t heir analysis becom es m ore challenging if t he analysis is ext ended int o t he public sect or, especially in local government s because financial rat ios ar e com monly used in privat e cont ext and researches r elat ed t o financial rat io analysis in public sect or cont ext ar e st ill rare. The analysis of Alijarde (1997) revealed t hat local ent it ies mainly use t he f inancial rat ios t hat exist in t he business ent it ies and adapt t hem t o t heir needs. Cohen (2008) found t hat t he assessment of financial performance t hrough t radit ional financial rat ios is influenced by macr oeconomic fact ors.

xxxi

barriers in successfully analyzing t he financial st at ement s of local governm ent s. The first barrier is t he lack of w idely accept ed financial rat ios and t he second barrier is t he fact t hat since such rat ios

do not exist neit her are t her e nat ionw ide nor ms against w hich t o com pare t he rat ios for a part icular local governm ent s.

The obst acles of conduct ing financial rat io analysis in public sect or can be solved by underst anding t he nat ur e of financial rat ios implement at ion in local government s as indicat ed by Cohen (2008) w ho st at ed t hat financial rat ios implement at ion in local governm ent s ar e not as st raight f orw ard as t he privat e sect or. The evaluat ion of public sect or ent it ies’ financial condit ion involves judgm ent s about t he int erplay of complex social, organizat ional and financial fact ors. In general t er ms, economy, geography and demographi cs const it ut e major component s of a local governm ent f inancial condit ion as t hey ar e det er mining fact ors of a government s’ abilit y t o m eet it s f inancial and service obligat ion.

Thus, as t he charact erist ics of t he com munit y ar e expect ed t o have an impact on t he act ivit y of local government s, t he use of macroeconomics t ype paramet ers as moderat ors w hen assessing t he perfor mance of public sect or ent it ies is a com monly employed f eat ur e in public sect or ef ficiency st udies as conduct ed by At hanassopulos and Triant is (1998) and Cohen (2008). At hanassopulos and Triant is (1998) have analyzed t he efficiency of 172 large Gr eek local governm ent s for t he year 1996 on t he basis of cash-basis account ing dat a. They concluded t hat t he most efficient local governm ent s w ere t hose t hat had higher t ax bases, incom e levels and

public invest m ent share on t ot al expendit ure.

1. Financial ratio selection

xxxii

profit abilit y rat ios, liquidit y rat ios, capit al st ruct ur e rat ios, and perfor mance rat ios. Cohen (2008) st at ed t hat t he f inancial rat ios select ion is based on privat e sect or and public sect or lit erat ur e

such as ICM A (2003), Berne (1992), Ant hony and Young (2003), and Finkler (2005). M oreover, t he select ed rat ios aim at achieving balanced r epr esent at i on of t he four broad cat egori es of f inancial rat ios w it hin t he analysis f ramew ork (Cohen, 2008).

a. Profit abilit y rat ios

In privat e sect or, one of t he most difficult at t ribut e of a fir m t o concept ualize and t o measur e is profit abilit y. Ross et al. (2005) st at ed t hat t he pr ofit abilit y rat ios cont ain t w o draw backs. The first draw back is t hat many business opport unit ies involve sacrificing curr ent profit for fut ure profit s and possibly t he business w ill produce low init ial profit s. Thus, current profit s can be a poor r ef lect ion of t rue f ut ur e profit abilit y. The second draw back is t hat t hey ignore risk.

Profit abilit y in public sect or is measured by comparing surplus or deficit on local governm ent ’s budget w it h equit y, t ot al asset s and local government original r evenue. Thus, prof it like usually know n in privat e sect or is replaced by budget surplus or deficit . Even t hough profit abilit y is not a primary goal in t he public sect or, t he exist ence of a r easonable surplus is necessar y in or der f or a municipalit y t o have enough funds t o finance it s long-t erm invest m ent (Cohen, 2008).

xxxiii

governm ent can use surplus t o pay debt s, est ablish reser ve fund and finance social securit y program. On t he cont rar y, deficit is less favorable because local governm ent has t o r eimburse t he

deficit w it h several resources as st at ed by Governm ent Rule Number 58 Year 2005 w hich consist of posit ive value of budget calculat ion dif fer ence from previous year, reimbursed reser ved fund, asset auct ion and debt .

The pr ofit abilit y rat ios used in t his research consist of ret urn on equit y rat io (ROE), r et urn on asset s rat io (ROA) and profit margin rat io (PM ). The profit abilit y rat ios ar e included in t his research because t hey provide a reflect ion of eff iciency in t he use of resources (Cohen, 2008).

b. Short -t er m solvency

Rat ios of shor t -t erm solvency measur e t he abilit y of t he fir m t o m eet r ecurring f inancial obligat ions (Ross et al. 2005). The ent it y should have a good rat io in t his t erm t o avoid f inancial

dist ress. In cont ext of local governm ent , t he short -t erm solvency indicat or show s local governm ent abilit y t o sust ain a st rong financial posit ion (Cohen, 2008).

The financial obligat ion of local governm ent s in Indonesia is ruled under Government Rule Number 54 Year 2005 about Local Government Debt . The Rule enables local governm ent s t o issue bonds in order t o cope w it h financial difficulties. How ever, The Rule rest rict s local govern ment s t o involve in debt by r equiring ever y local governm ent meet several crit eria as st at ed by Sect ion 11 and 12 successively.

xxxiv

municipalit ies and f ound t hat f inancial perf or mance t hat elaborat ed w it h several financial rat ios including current rat io is influenced by macroeconomic fact ors.

The m ost w idely used m easur es of account ing liquidit y are current rat io and quick rat io (Ross et al, 2005). How ever, t he short t er m solvency used her e is only t he curr ent rat io since t he

quick rat io is not applicable because t he pr esence of invent or ies t hat only suit able for privat e sect or.

c. Capit al st ruct ure rat io

Capit al st ruct ur e rat ios show how t he ent it y is being f inanced. The f inancing sour ce comes from t w o sources; liabilit y and equit y. The t w o common rat ios for capit al st ruct ur e rat ios ar e debt t o equit y rat ios and debt t o t ot al asset r at io.

This resear ch w ill incorporat e t he debt t o equit y rat io and t he long t erm deb t o t ot al asset s

rat io. The higher t he value of debt t o equit y r at io, t he gr eat er t he local governm ent s’ leverage and t hus t he great er t he ext ent t o w hich it ut ilizes debt funds t o supplem ent int ernal equit y funds (Cohen, 2008).

d. Perf ormance rat io

xxxv

operat ing expense. Based on t he law , operat ing revenue is represent ed by local governm ent original revenue.

The asset s t urnover rat io repr esent s t he efficiency use of asset s in generat ing t he municipal original revenue. The operat ing r evenue t o t ot al revenues show s t he degr ee independency of

local governm ent s from t he cent ral governm ent subsidies. Operat ing revenue t o operat ing expenses rat io show s t he abilit y of Local governm ent original revenue in f inancing t he operat ing expenses.

C. Exogenous Fact or Select ion

This resear ch proposes macroeconomic variables, size, and geographical fact ors t hat are conject ur ed t o influence t he behavior of f inancial rat ios. M acroeconomic fact ors ar e repr esent ed by gross dom est ic regional product (GRDP). The var iables proposed by pr evious research (Cohen,

2008) w ill be modified in t his research by adding and omit t ing several variables. The geographical fact ors r epr esent ed by w het her a local government is a capit al of a province or not w ill be omit t ed from t his research since it w ill generat e dat a singularit y in dat a analysis.

xxxvi

The modificat ion is also made in macroeconomic f act or by adding t he inflat ion as a new exogenous var iable because sever al resear ches (for example; Hut agaol, 2002 and Nugroho, 2007)

show t hat inf lat ion has effect s on local government original revenue. Local governm ent original revenue is one of import ant component t hat composes financial per formance.

1. M acroeconomic factor

a. GRDP

GRDP m easur es t he w ealt h of local governm ent s. St at ist ics Bur eau of t he Republic of Indonesia or Badan Pusat St at ist ik (BPS) uses t hr ee approaches in m easuring GRDP, namely, product ion approach, expendit ur e approach and income approach.

Product ion approach expresses GRDP as t he t ot al value of final goods and ser vices produced by all product ion unit s in a region w it hin a cer t ain period (usually one year period). Product ion unit s are gr ouped as in t he Int ernat ional St andard Indust rial Classificat ion of All Economic Act ivit ies (ISIC), w hich are: Agr icult ure; M ining and Quarrying; M anufact uring Indust ries; Elect ricit y, Gas and Wat er Supply; Const ruct ion; Trade, Hot el and Rest aurant ; Tr ansport and Comm unicat ion; Financial, Ow nership and Business Services; Ser vices including governm ent ser vices.

Expendit ur e approach expr esses GRDP as t he t ot al of final demand component s, covering t he consumpt ion expendit ur e of households and privat e nonprofit inst it ut ions, government consumpt ion, gross dom est ic f ixed capit al format ion, increase in st ock and net export w it hin a cer t ain period. Net export is t he export minus import .

xxxvii

form of w ages or salar ies, land r ent , capit al int erest and profit margin. The profit s include income t ax and ot her direct t axes. In t his definit ion, t he GRDP also cont ains depr eciat ion and net direct

t axes.

In relat ion t o profit abilit y rat io, a local governm ent w it h high GRDP t ends t o enhance t he

value of local government r evenue t hrough local governm ent original revenue and r evenue sharing. This sit uat ion will enhance t he f iscal capacit y of local gover nment . The rise of fiscal capacit y w ill enhance t he possibilit y t o enhance budget surplus, cet eris paribus. The rise of local governm ent revenue w ill also raise t he possibilit y t o enhance t he value of asset and equit y. Cohen (2008) f inds t hat profit abilit y rat io is influenced by GRDP. Thus, it is expect ed t hat GRDP w ill influence t he profit abilit y rat io.

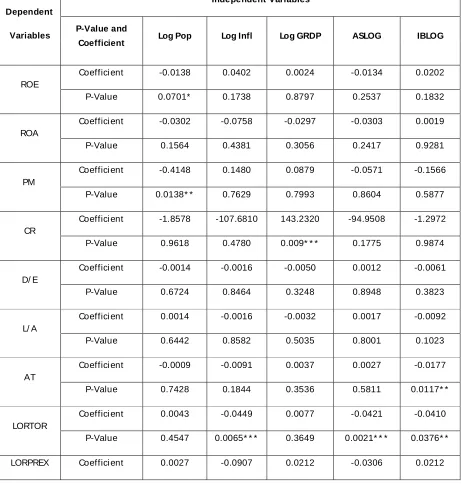

Based on t he above discussion, t his research proposes t he f ollow ing hypot heses:

H1a: Ret urn on equit y (ROE) w ill be influenced by GRDP

H1b: Ret urn on asset s (ROA) w ill be influenced by GRDP

H1c: Profit margin (PM ) will be influenced by GRDP

xxxviii

Based on t he above discussion, t his research proposes t he f ollow ing hypot heses:

H1d: Current rat io (CR) w ill be influenced by GRDP

In relat ion t o capit al st ruct ure rat io, t he r ise of local governm ent revenue t ends t o enhance t he value of asset and equit y, cet eris paribus. If t he value of debt is const ant , GRDP w ill affect t he capit al st ruct ur e rat io negat ively. How ever, Cohen (2008) found t hat GRDP influences capit al st ruct ur e rat io negat ively. This indicat es t hat local government s t hat have higher r evenue t ends t o use debt as t he financing inst rument .

Based on t he above discussion, t his research proposes t he f ollow ing hypot hesis:

H1e: Debt t o equit y rat io (D/ E) will be influenced by GRDP

H1f: Long t erm debt t o t ot al asset s rat io (L/ A) will be influenced by GRDP

In relat ion t o perfor mance rat io, GRDP t ends t o enhance t he value of local government original revenue. The rise of local governm ent original revenue t ends t o enhance t he value of of perfor mance rat io, cet er is paribus. Cohen (2008) found t hat GRDP influences t he perfor mance rat io. Thus, it is expect ed t hat GRDP w ill influence t he perf or mance rat io.

Based on t he above discussion, t his research proposes t he f ollow ing hypot hesis:

H1g: Asset s t urnover rat io (AT) w ill be influenced by GRDP

H1h: Local government original revenue t o t ot al r evenue rat io (LORTOR) w ill be influenced by GRDP

xxxix b. Inflat ion

Usually, inflat ion relat es t o a rise in t he general level of prices of goods and ser vices in an

econom y over a period of t ime. Inflat ion consist s of demand side inflat ion and cost pull inflat ion. Demand side inflat ion is usually follow ed by t he rise of GDP. Cost pull inflat ion is t he t ype of inflat ion caused by t he rise of cost of product ion. Cost pull inflat ion is usually follow ed by t he decline of purchasing pow er.

In cont ext of local governm ent , Hut agaol (2003) conduct s t he research invest igat ing about fact ors influencing t he ent ert ainm ent t ax in DKI Jakart a and finds t hat inflat ion has effect on ent ert ainment t ax revenue. Nugr oho (2007) invest igat es f act ors influencing pr opert y t ax r evenue in Klat en Regency and finds t hat inflat ion has negat ive impact on land propert y t ax revenue.

The influence of inflat ion on prof it abilit y rat io depends on t he t ype of inf lat ion. Demand side inflat ion is expect ed t o influence prof it abilit y rat i o posit ively because it is usually follow ed by t he rise of GDP. As discussed in pr evious discussion, t he rise of GDP is expect ed t o influence profit abilit y rat io positively. On t he ot her hands, cost pull inflat ion is expect ed t o influence profit abilit y rat io negat ively because it is usually follow ed by t he decline of purchasing pow er . The decline of purchasing pow er t ends t o decline t he local governm ent ’ s economic act ivit y. The decline of economic act ivit y t ends t o reduce t he value of local governm ent r evenue. The decline of local governm ent revenue t ends t o decline t he budget surplus, equit y, and asset .

Based on t he above discussion, t his research proposes t he f ollow ing hypot heses:

H2a: Ret ur n on equit y (ROE) w ill be influenced by inflat ion

H2b: Ret urn on asset s (ROA) w ill be influenced by inflat ion

xl

The influence of inf lat ion on current rat io also depends on t he t ypes of inflat ion. Demand side inf lat ion is expect ed t o have similar influence on current rat io as GDP. On t he ot her hands,

t he cost pull inflat ion is expect ed t o have influence on current r at io negat ively because it t ends t o reduce t he value of local governm ent r evenue. The decline of local governm ent r evenue t ends t o lead t he cash shor t age problem. The decline of local government r evenue also t ends t o r educe t he value of current asset , cet eris paribus. Thus, cost pull inflat ion t ends t o influence t he curr en t rat io negat ively.

Based on t he above discussion, t his research proposes t he follow ing hypot heses:

H2d: Current Rat io (CR) w ill be influenced by inf lat ion

In accordance w it h capit al st ruct ure rat io, t he demand side inflat ion is expect ed t o have influence similar t o GRDP. On t he ot her hands, t he cost pull inflat ion is expect ed t o negat ively

influence t he capit al st ruct ur e. The cost pull inflat ion t ends t o reduce local government r evenue. The decline of local governm ent r evenue t ends t o r educe t he value of asset and equit y. This sit uat ion t ends t o push local governm ent t o choose debt as t he financing inst rument .

Based on t he above discussion, t his research proposes t he follow ing hypot heses:

H2e: Debt t o equit y rat io (D/ E) w ill be influenced by inflat ion

H2f: Long t erm debt t o t ot al asset s rat io (L/ A) will be influenced by inflat ion

xli

Furt her , t he decline of local governm ent r evenue t ends t o aff ect t he value of t ot al revenue, asset and operat ing expense.

Based on t he above discussion, t his research proposes t he follow ing hypot heses:

H2g: Asset s t urnover rat io (AT) w ill be inf luenced by inflat ion

H2h: Local government original revenue t o t ot al r evenue rat io (LORTOR) w ill be influenced by inflat ion

H2i: Local governm ent original revenue t o operat ing expense r at io (LORPREX) w ill be influenced by inflat ion

2. Size

xlii

Berne (1992) in Cohen (2008) st at ed t hat many social, polit ical, economic, and polit ical feat ur es of gover nment appear t o be r elat ed w it h usually m easured in t erms of populat ion.

Number of municipal off icers and employees, volume if service offer ed are t he examples of impact influenced by t he size of populat ion (Coh en, 2008). Cohen (2008) also found t hat populat ion as a proxy for size influences t he financial perfor mance.

In accordance w it h profit abilit y rat io, populat ion w ill enhance t he fiscal needs of local governm ent . The rise of fiscal needs t ends t o r educe t he value of budget surplus, cet eris paribus. The rise of fiscal needs also t ends t o r educe t he value of asset and equit y, cet eris paribus. This ar gum ent aligns w it h Cohen (2008) w ho found t hat populat ion has negat ive influence on profit abilit y rat io. Thus, it is expect ed t hat populat ion w ill have influence on profit abilit y rat io.

Based on t he discussion above, t his research proposes t he f ollow ing hypot hesis:

H3a: Ret urn on equit y (ROE) w ill be influenced by populat ion

H3b: Ret urn on asset s (ROA) w ill be influenced by populat ion

H3c: Profit margin (PM ) w ill be influenced by populat ion

The bigger populat ion t ends t o r educe t he value of cur rent asset , cet eris paribus. The bigger populat ion also t ends t o enhance t he possibilit y of local governm ent t o suffer cash short age problem, cet eris paribus. The cash short age probl em w ill push t he local government t o employ current debt . This argum ent aligns w it h Cohen (2008) w ho found t hat populat ion has negat ive influence on current rat io. Thus, it is expect ed t hat populat ion will influence t he curr ent rat io.

Based on t he above discussion, t his research proposes t he follow ing hypot hesis:

xliii

The bigger number of populat ion t ends t o enhance t he possibilit y of local governm ent in using debt as t he f inancing inst rument , cet eris paribus. The bigger number of populat ion also

t ends t o r educe t he value of asset and equit y, cet eris paribus. This argument aligns w it h Cohen (2008) w ho found t hat populat ion influences capit al st ruct ur e rat io posit ively. Thus, it is expect ed t hat t he populat ion w ill influence t he capit al st ruct ur e rat io.

Based on t he above discussion, t his research proposes t he follow ing hypot heses:

H3e: Debt t o equit y rat io (D/ E) w ill be influenced by populat ion

H3f: Long t erm debt t o t ot al asset s rat io (L/ A) will be influenced by populat ion

In accordance w it h performance rat io, bigger populat ion t ends t o enhance local governm ent original r evenue, local governm ent t ot al revenue and operat ing expense. On t he cont rar y, bigger populat ion t ends t o r educe t he value of asset if t her e is no rise on local governm ent r evenue. Cohen (2008) found t hat populat ion influences perfor mance rat io posit ively. Thus, populat ion is expect ed t o influence per formance rat io.

Based on t he above discussion, t his research proposes t he follow ing hypot heses:

H3g: Asset s Turnover Rat io (AT)) w ill be influenced by populat ion

H3h: Local gover nm ent original revenue t ot al revenue r at io (LORTOR) w ill be influenced by populat ion

H3i: Local government original revenue t o operat ing expense Rat io (LORPREX) w ill be influenced by populat ion

3. Geographical factor

xliv

The dif f erent charact erist ics in local governm ent s i n Indonesia could also com e f rom administ rat ive st at us differ ence of local governm ent s w hich divides local government s int o t w o

administ rat ive st at uses; municipalit y and regency. According t o w w w .w ikipedia.com (2009), t he differences bet w een municipalit y and r egency in Indonesia r eside on t hree point s; demographic charact erist ics, area size, and economic charact erist ics. Dat a r eleased by Indonesian St at ist ics Bur eau (BPS) implies t hat municipalit y has larger populat ion densit y t han r egency in t er ms of dem ographic charact erist ic. M oreover, municipalit y has smaller area t han t he regency in t erms of ar ea size. From t he economic charact erist ics, municipalit y t ends t o be t he cent er of indust r y and service provider, on t he ot her hand, regency t ends t o be provider in agricult ural sect or. The differences bet w een municipalit y and regency, t hus, are similar t o differences bet w een rural and urban.

When discussing about t he relat ion bet w een rural and urban in Indonesian cont ext , t he discourse of disparit y also em er ges. Daryant o (2003) st at es t hat unsolved development problem in Indonesia includes int err egional disparit y, t he high level of urban primacy, t he syner gy linkage bet w een rural and urban, underdeveloped r egions, and pover t y. It implies t hat several developm ent problems in Indonesia involve t he disparit y bet w een rural and urban. The M inist ry of Underdeveloped Regions and The Accelerat ion of Indonesian East Region Developm ent in 2008 st at es t hat t here ar e 199 r egencies in Indonesia t hat classified as underdeveloped r egions. It means t hat none of t he municipalit y is classif ied as underdeveloped r egion.

xlv

revenue t ends t o enhance t he value of asset and equi t y, cet eris paribus. Thus, it is expect ed t hat administ rat ive st at us of local governm ent w ill have influence on profit abilit y rat io.

Based on t he discussion above, t his research proposes t he follow ing hypot hesis:

H4a: Ret urn on equit y (ROE) w ill be influenced by administ r at ive st at us of local governm ent

H4b: Ret urn on asset s (ROA) w ill be influenced by administ rat ive st at us of local governm ent

H4c: Profit margin (PM ) w ill be influenced by administ rat ive st at us of local government

In accordance w it h curr ent rat io, municipalit y t ends t o have mor e opport unit ies t o generat e r evenue compar ed t o regency. The rise of local government revenue t ends t o enhance t he value of curr ent asset , cet eris paribus. By assuming t hat t he value of curr ent asset is const ant , t he r ise of current asset is expect ed t o influence t he value of current rat io.

Based on t he above discussion, t his research proposes t he foll ow ing hypot hesis:

H4d: Current rat io (CR) w ill be influenced by administ rat ive st at us of local government

In accordance w it h capit al st ruct ure rat io, municipalit ies t end t o have m ore oppor t unit ies t o enhance local gover nm ent revenue com pared t o regencies due t o t heir st at uses as indust r y and service providers. How ever, t heir st at uses as providers of indust ry and ser vice might push t hem t o make mor e invest ment compar ed t o r egencies. This sit uat ion might urge t he local governm ent t o finance it using debt . Thus, it is expect ed t hat administ r at ive st at us of local governm ent w ill have influence on capit al st r uct ure rat io.

Based on t he above discussion, t his research proposes t he follow ing hypot heses:

xlvi

H4f: Long t er m debt t o t ot al asset s rat io (L/ A) w ill be influenced by administ rat ive st at us of local governm ent

In accordance w it h perfor mance rat io, municipalit y as t he cent er of indust ry and ser vice t ends t o have mor e opport unit ies t o earn local government original revenue and local

governm ent t ot al revenue. The rise of local governm ent r evenue t ends t o enhance t he value of asset , cet eris paribus. Thus, it is expect ed t hat adm inist rat ive st at us of local governm ent w ill influence t he perfor mance rat io.

Based on t he above discussion, t his research proposes t he follow ing hypot heses:

H4g: Asset s t urnover rat io (AT) w ill be influenced by administ rat ive st at us of local gover nment

H4h: Local gover nm ent original revenue t o t ot al r evenue r at io (LORTOR) w ill be inf luenced by administ rat ive st at us of local governm ent

H4i: Local governm ent original revenue t o operat ing expense rat io (LORPREX) w ill be influenced by administ rat ive st at us of local governm ent

b. Island-based locat ion of local governm ent

xlvii

and Levine (2000) f ound t hat physical fact ors fail in explaining cross-count r y and cross t ime grow t h difference.

When discussing about diff erences bet w een Java and Bali versus local governm ent s locat ed out side t hose islands, t he frequent ly discussed t opic is about disparit y, especially in economic

disparit y. Bhinadi (2003) st at ed t hat t her e ar e t w o issues w hen discussing about regional economic disparit y. The first issue r elat es t o r esour ces of regional grow t h. The second issue relat es t o t he r egional disparit y it self. Bhinadi (2003) analyzes t he r egional disparit y bet w een Java and out side Java and finds t hat t her e is no regional grow t h disparit y bet w een t hem. On t he cont rar y, t he official release from The M inist ry of Underdeveloped Regions and The Accelerat ion of Indonesian East Region Development in 2008 st at es t hat f rom all local governm ent s classified as underdeveloped region, 91 per cent ar e cont ribut ed by t he local governm ent out side Java-Bali, w hereas Java and Bali only cont ribut e t he rest of t he per cent age. Edy (2009) st at ed t hat f rom 2001 unt il 2007, Java and Bali cont r ibut e sixt y percent t o nat ional gr oss dom est ic product s (GDP) and all areas locat ed out side t hose islands cont ribut e t he r est (i.e. fort y percent ). Thus, t he influence of island-based local government on financial per for mance is expect ed t o be similar t o t he inf luence of GRDP on financial performance.

From t he discussion above, t his research proposes t he follow ing hypot hesis:

H5a: Ret urn on equit y (ROE) w ill be influenced by island-based locat ion of local gover nment

H5b: Ret urn on asset s (ROA) w ill be influenced by island-based locat ion of local governm ent

H5c: Profit margin (PM ) w ill be influenced by island-based locat ion of local governm ent

xlviii

H5e: Debt t o equit y rat io (D/ E) w ill be influenced by island-based locat ion of local government

H5f: Long t er m debt t o t ot al asset s rat io (L/ A) w ill be influenced by island-based locat ion of local governm ent

H5g: Asset s t urnover rat io (AT) w ill be influenced by island-based locat ion of local governm ent

H5h: Local gover nm ent original revenue t o t ot al r evenue r at io (LORTOR) w ill be inf luenced by island-based locat ion of local governm ent

H5i: Local governm ent original revenue t o operat ing expense rat io (LORPREX) w ill be influenced by island-based locat ion of local governm ent

xlix

The t heor et ical f ramew ork for t his research is graphed below ;

ROE ROA D/ E CR PR L/ A AT LORTOR LORPREX F i n a n c i a l P e r f o r m a

Financial Perfor mances are hypot hesized t o be influenced by

M acroeconomic Fact ors, Size, and Geographical Fact ors

Regr ession Analysis Using Ordinary Least

Squares and Panel

Local governm ent

l

Figure 1

Theoretical Framew orks

CHAPTER III

RESEARCH M ETHOD

A. Data Collection

Dat a is collect ed f rom t he published audit ed financial st at ement s from t he official w ebsit e of BPK f rom year 2006 t o 2007. The published financial st at ement s from local government s w ill include several t ypes of audit opinion excluding adver se and disclaimer. Dat a for macroeconomic fact ors ar e collect ed f rom various sources especially dat a available in w ebsit es provided by Indonesia St at ist ics Agency or BPS , Bank of Indonesia (BI) and many ot her support ive w ebsit es.

li

1. Population

Populat ion ref ers t o t he ent ire group of people, event s, or t hings of int er est t hat t he researcher w ishes t o invest igat e (Sekaran, 2003). The populat ion of t his research is all published audit ed financial st at em ent s of Indonesian local governm ent s f or t w o years successively (f rom

2006 t o 2007).

2. Sample

A sample is a subset of populat ion and it comprises some mem bers select ed fr om t he populat ion (Sekaran, 2003). This research uses judgment al sampling t o draw t he samples fr om financial st at ement s. The use of judgment al sampling aimed t o achieve t he samples by choosing subject s t hat are in t he most suit able place t o give specif ied informat ion (Sekaran, 2003). All published financial st at em ent s cont aining any t ypes of opinion except adverse and disclaimer w ill be included in dat a calculation.

C. Analysis Technique

This research w ill use mult ivariat e r egr ession analysis t hat is done by using ordinary least squares (OLS). Ordinary least squar es (OLS) is a t echnique for est imat ing t he unknow n paramet ers in a linear regr ession model w hich minimizes t he sum of squared dist ances bet w een t he obser ved responses in a set of dat a, and t he fit t ed responses from t he r egr ession model (w w w .w ikipedia.org).

lii The model w ill be proposed as follow s:

Financial Rat ios= a0 + b1 Log GRDP + b2 Log Pop + b3 Log Infl + b4 M undic + b5 Cireg

Where;

Log GRDP = Logarit hmic f orm of Gross Regional Dom est ic Product

Log Pop = Logarit hmic f orm of Populat ion

Log Infl = Logarit hmic f orm of Inflat ion

IBLOG = Island-based Locat ion of Local Governm ent s

ASLOG = Administ rat ive St at us of Local Governm ent s

To comput e t he regression model, t his research w ill use GRETL Version 1.1 Soft w are.

The assumpt ion of t he models are as following:

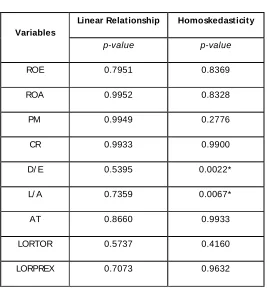

Nonlinearit y t est : This kind of t est is used t o check t he linearit y of t he r egression model. Themodel of linear regression must be linear.

Het eroskedast icit y: Her oskedast icit y happens w hen random variables have differ entvariances. Het eroskedast icit y problem of t en occurr ed in OLS t echnique. The assumpt ion of homoskedast icit y has t o be maint ained. How ever, if het eroskedast icit y is occurr ed or t he

liii

The w eight ed least squar es t echnique in Gret l is conduct ed using het er oskedast icit y correct ed t est .

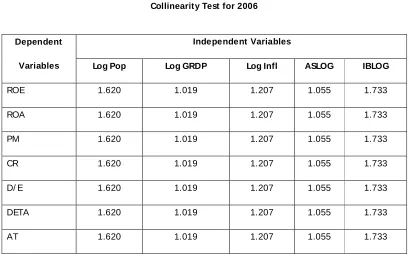

Collinearit y: This t est is aim ed t o indicat e t he degr ee t o w hich each of t he explanat or yvariables is collinear w it h t he ot her explanat or y var iables. When t his sit uat ion exist s, t he model suf fer s mult icollinearit y problems. The good regr ession model must f r ee from t his problem. In Gret l, t his assumpt ion is checked by indicat ing variance inf lat ion fact ors (VIF) value. When t he VIF is higher t han 10, t hen t he model suffers mult icollinearit y problem.

Normalit y: Nonnormalit y of errors oft en r equir ed by r egr ession model. In t he cont rary,ordinary least squar es (OLS) t echnique does not require t his assumpt ion (Ramanat han, 1993). As st at ed by Ramanat han (1993), t he most impor t ant t hing in OLS is t hat t he dat a is nonsingular t ype free of het eroskedast icit y and mult icollinearit y problems.

D. Variable Identification

This research is a replicat ion f rom Cohen (2008) w it h several modif icat ions. The main modificat ion in t his research is caused by t he dat a availabilit y. The price and t ourist as invest igat ed by Cohen (2008) ar e unavailable. This research also modifies t he pr evious r esear ch by adding inflat ion t hat is expect ed t o have influence on f inancial rat ios.

island-liv

based locat ion of local governm ent s (IBLOG) and administ rat ive st at us of local governm ent (ASLOG).

E. Operational Definition

The dependent variables are classified int o four groups t hat consist of profit abilit y rat io, liquidit y rat io, capit al st ruct ure rat io and perfor mance rat io. Profit abilit y rat io consist s of ret ur n on equit y, ret urn on asset s and pr ofit margin. Liquidit y rat io consist s of only current rat io. Capit al st ruct ur e rat io consist s of debt t o equit y rat io, and long-t er m liabilit ies t o t ot al asset s. Perf ormance rat io consist s of asset s t urnover, operat i ng revenues t o t ot al r evenues and operat ing revenues t o t ot al expenses.

[image:51.612.147.526.422.699.2]The operat ional definit ions for each dependent variable are summarized in f ollow ing t able:

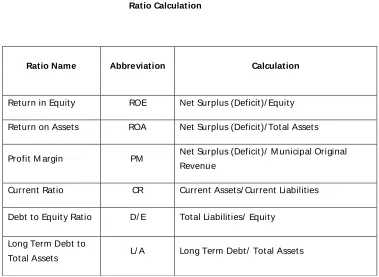

Table 1

Ratio Calculation

Ratio Name Abbreviation Calculation

Ret urn in Equit y ROE Net Surplus (Deficit )/ Equit y Ret urn on Asset s ROA Net Surplus (Deficit )/ Tot al Asset s

Profit M argin PM Net Surplus (Deficit )/ M unicipal Original Revenue

Current Rat io CR Current Asset s/ Current Liabilities

Debt t o Equit y Rat io D/ E Tot al Liabilit ies/ Equit y

Long Term Debt t o

lv

Asset s Turnover AT Local Government Original Revenue/ Tot al Asset s

Local government original

revenue/ Tot al Revenue

LORTOR Local Government Original Revenue/ Tot al Revenue

Local government original

revenue/ Operat ing Expense

LORPREX Local Government Original Revenue/ Operat ing Expenses

lvi

CHAPTER IV

lvii

A. Data Description

The local government dat a collect ion goes along t he sampling guidelines. The disclaimer and adverse opinion are excluded from dat a analysis in order t o keep t he dat a validit y. The exclusion also equally t r eat ed t o dat a t hat encount er t echnological difficult ies such as t he excessiveness in comput er m emory consumpt ion t hat makes t he comput er encount ers dist ort ion.

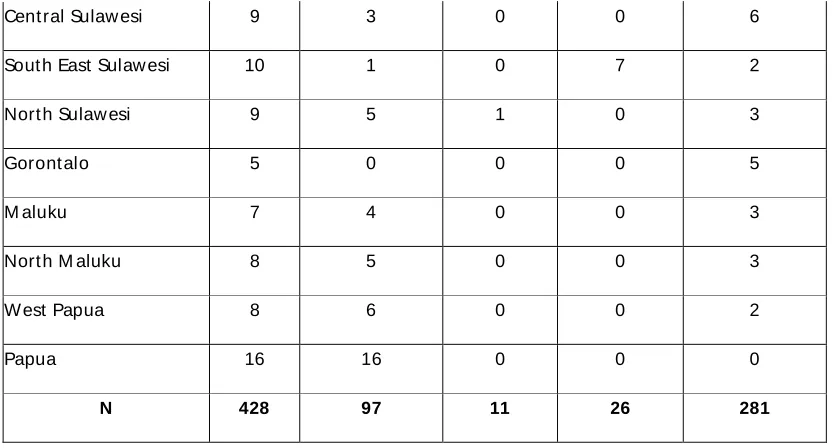

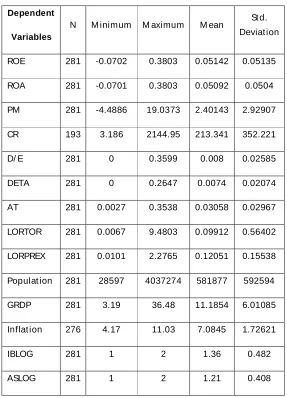

The t abulat ed dat a in Table 2 present s t he dat a descript ion for 2006. Dat a descript ion elaborat es t he dat a aligned w it h sampling crit eria. The num ber of local government s for 2006 is 428. The number of disclaim er opinion is 97. The number of adverse opinion is eleven. The number of incomplet e dat a caused by t echnological handicap is 26. Thus, t he number of f inancial st at em ent s t o be incor porat ed in dat a analysis comes f rom 281 local gover nm ent s.

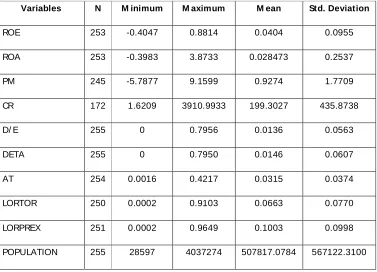

The t abulat ed dat a in Table 3 pr esent s t he dat a descr ipt ion for 2007. Dat a descript ion also elaborat es t he dat a aligned w it h sampling crit eria. The num ber of local gover nment s for 2007 is 432. The number of local governm ent s for 2007 is differ ent fr om pr evious year (2006) because t he exist ence of new local government s. The number of disclaimer opinion is 74. The number of adverse opinion for 2007 is 62. The number of incomplet e dat a caused by t echnological handicap is 14. Thus, t he number of f inancial st at em ent s t o be incorporat ed in dat a analysis com es f rom 255 local governm ent s.

Table 2

Data Description for 2006

lviii

NAD 21 5 0 2 14

Nort h Sumat era 26 17 1 0 8

Riau 11 2 0 1 8

Kepulauan Riau 6 1 0 2 3

Bengkulu 8 3 0 0 5

Jambi 10 2 0 0 8

W est Sumat era 20 5 0 0 15

Sout h Sumat era 14 1 0 0 13

Bangka Belit ung 7 0 0 0 7

Lampung 10 0 0 0 10

Bant en 6 0 0 2 4

W est Java 25 0 0 2 23

Cent ral Java 35 1 0 1 33

DIY 5 1 1 0 3

East Java 38 5 0 2 31

Bali 9 0 0 1 8

Nusa Tenggara Bar at 9 2 0 0 7

Nusa Tenggara Timur 17 4 1 1 11

W est Kalimant an 12 3 1 0 8

Sout h Kalimant an 13 0 3 1 9

Cent ral Kalimant an 14 2 3 1 8

East Kalimant an 13 0 0 0 0

W est Sulaw esi 4 0 0 0 4

lix

Cent ral Sulaw esi 9 3 0 0 6

Sout h East Sulaw esi 10 1 0 7 2

Nort h Sulaw esi 9 5 1 0 3

Goront alo 5 0 0 0 5

M aluku 7 4 0 0 3

Nort h M aluku 8 5 0 0 3

W est Papua 8 6 0 0 2

Papua 16 16 0 0 0

[image:56.612.105.522.106.330.2]N 428 97 11 26 281

Table 3

Data Description for 2007

Province Tot al LG Disclaimer Adverse Incomplete

Tot al Incorporated

Data

NAD 21 2 0 0 19

Nort h Sumat era 26 13 0 0 13

Riau 11 2 0 0 9

Kepulauan Riau 6 0 0 0 6

Bengkulu 9 0 0 3 6

Jambi 10 0 0 0 9

W est Sumat er a 20 5 0 0 15

Sout h Sumat era 14 0 0 0 14

lx

Lampung 10 0 0 0 10

Bant en 6 1 0 0 5

W est Java 25 6 0 0 19

Cent ral Java 35 4 0 1 30

DIY 5 0 1 0 4

East Java 38 0 36 0 2

Bali 9 0 0 0 9

Nusa Tenggara Barat 9 3 0 1 5

Nusa Tenggara Timur 17 1 0 4 12

W est Kalimant an 12 3 3 0 6

Sout h Kalimant an 13 1 4 1 7

Cent ral Kalimant an 14 4