Buying decision in the marketing of Sharia life insurance - UDiNus Repository

Teks penuh

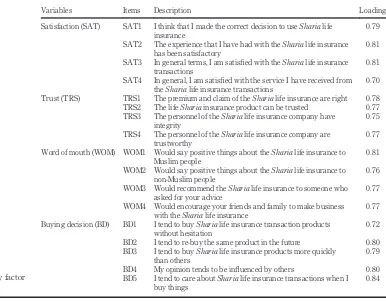

Gambar

Dokumen terkait

The result shows that, consumers buying decision have been influence by green marketing element which is green consumer perception and green promotion activities..

Penelitian ini bertujuan untuk mengetahui apakah: 1) internet marketing mempengaruhi brand awareness secara positif, 2) intention to buy mempengaruhi buying

Variabel yang digunakan dalam penelitian ini adalah E-Marketing Mix, Word of Mouth, dan Buying Decision dengan jenis penelitian konklusif untuk dapat menjabarkan

To find out the impact of claims, investment returns, underwriting results, and operational costs on the profit growth of sharia life insurance companies in the 2016-2021 period, the

Conclusion Based on the results of the research and discussion above, it can be concluded that Attitude has a significant positive effect on the decision to buy sharia insurance

Factors Influencing Buying Behavior Social Factor Marketing Factor Situational Factor Psychological Factor Buying Decision Process Need/Problem recognition Information search

The exploration role of Sharia compliance in technology acceptance model for e-banking case: Islamic bank in Indonesia Hardius Usman and Nucke Widowati Kusumo Projo Department of

Based on the data analysis results, this study found that the digital marketing, brand preference, and product quality variables have a significant influence on the buying decision of