Inventory Control

(Production Planning & Control)

IE 2353

Pratya Poeri SuryadhiniQuantity Discount Models

Object is to Minimize total inventory costs; includes material costs

Material costs relevant in total cost: –TC = DC + D/Q(Co) + Q/2(Ch)

where

D = unit annual demand C = unit cost

Co= each order cost

Ch= carrying cost per unit per year

IC must be used in place of Chin decision-making

Steps for Solving Quantity Discount

1.

Compute EOQ for each discount price:

2.

If EOQ < discount minimum level, make Q = minimum.

3.

For each EOQ, compute total cost:

TC = DC + D/Q(Co) + Q/2(Ch)

4.

Choose the lowest cost quantity from all levels.

Q

*2DC

IC

oQuantity Discount Models

Text example:

Quantity Discount Schedule

Material cost:

•Total material cost is affected by the Discount (%)

•Unit cost if first $5.00, then $4.80, and finally $4.75

Quantity Discount Models

Total Cost Curves for each of the 3 discount plans

Figure 6.7

Quantity Discount Steps

–

A Review

1. Calculate Q for each discount.

2. Adjust Q upward if quantity is too low for discount.

3. Compute total cost for each discount.

4. Select Q with the lowest total cost.

Quantity Discount Example

The Smith company purchases 8000 units of a

product each year. The supplier offers the units for

sale at $10.00 per unit for orders up to 500 units and

at $9.00 per unit for orders of 500 units or more.

What is the economic order quantity if the order

cost is $30.00 per order and the holding cost is 30%

of per unit cost per year?

Quantity Discount Example

The EOQ at $9.00 is invalid, since it is not available for quantities less than 500 units. The EOQ at $10.00 is valid. Therefore, the total cost of the valid EOQ is compared with the total cost at the larger price-break quantity:

Economic Production Quantity

The assumptions that the entire orders is received into inventory at one time (instantaneously is often not true.

The EPQ assumes continuous gradual additions to stock (finite replenishment rate) over the production period.

The EPQ formula is obtained:

p= production rate

d = demand rate

Economic Production Quantity

Economic Production Quantity

Optimum length of production run

Production reorder point in units

Total annual cost = production cost + setup cost + holding cost

EPQ Example

EPQ Example

The Use of Safety Stock

Stock-outs occur when there are uncertainties with: - Demand

- Lead time

Safety stock is extra stock on hand to avoid stock-outs

•ROP = d*L + SS

•d = average daily demand

•L = average lead time, time for an order to be delivered

•SS = safety stock

ROP is adjusted to implement safety stock policy:

The Use of Safety Stock

In

Fig. 6.8. The Use of Safety Stock

The Use of Safety Stock and ROP

Known stock-out costs:

•

Given probability of demand, find total cost for each

safety stock alternative

Unknown stock-out costs:

Known Stock-out Costs

• ABCO example:

Table 6.2

Initial calculations: ROP = 50 (d*L) Ch= $5

Css= $40/ unit (stock-out cost) D/Q = 6 times per year

Known Stock-out Costs continued

• ABCO example: Table 6.3

Calculation the EMV (expected monetary value) for each ROP

alternative

Known Stock-out Costs continued

ABCO example:

Calculations for a given ROP, N: 1. Being Short: D(S) = (N-S)* Css*D/Q,

• where S = demand during lead time 2. Being Over: D(O) = (D-O)* Ch

• where O = demand under ROP Calculations for an ROP of 40:

• Being Over

D(30) = (40-30)*$5 = $50 D(40) = $0

• Being Short

D(50) = (50-40)*$40*6 = $2,400 D(60) = (60-40)*$40*6 = $4,800 D(70) = (70-40)*$40*6 = $7,200

Known Stock-out Costs continued

ABCO example:

Last step for ROP = 40 is to calculate the EMV:

EMV = P(D) * Cost of Being Short/Over

EMV(40) =

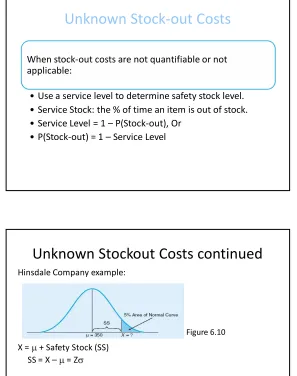

Unknown Stock-out Costs

When stock-out costs are not quantifiable or not

applicable:

•

Use a service level to determine safety stock level.

•

Service Stock: the % of time an item is out of stock.

•

Service Level = 1

–

P(Stock-out), Or

•

P(Stock-out) = 1

–

Service Level

Unknown Stock-out Costs continued

Hinsdale Company example:

1. Lead time demand ~N(350, 10) where = 350, = 10

2. Desired Policy: P(Stock-out) = 5%

Therefore, service level = 95%

Visualization of Desired Inventory Policy:

Figure 6.9

Unknown Stockout Costs continued

Hinsdale Company example:

X = + Safety Stock (SS) SS = X – = Z

Z = =

23

Figure 6.10

X-

SS

Unknown Stock-out Costs continued

Hinsdale Company example:

Find Z using a Normal table, like in Appendix A: Z = 1.65 for a 5% right tail

Rewrite equation: Z = 1.65 = =

Solving for SS yields 16.5, or 17, units. Therefore, ROP = 350 + 17 = 367

24

Service Level versus Carrying Costs

Figure 6.11

The following curve depicts the tradeoff between carrying costs and service level for the previous example

such dramatic tradeoffs exist for all similar problems

ABC Analysis

ABC analysis divides on-hand inventory into three classifications on the basis of dollar (TL) volume.

It is also known as Pareto analysis. (which is named after principles dictated by Pareto).

The idea is to focus resources on the critical few and not on the

trivial many.

(Annual Dollar Volume of an Item) = (Its Annual Demand) x (Its Cost per unit)

ABC Analysis

Class

A

items are those on which the annual

dollar volume is high.

They represent 70-80% of total

inventory costs, but they account

for only 15% of total inventory

items.

ABC Analysis

Class

B

items are those on which

annual dollar volume is medium.

They represent 15-25% of total

dollar value, and they account for

30% of total inventory items on the

ABC Analysis

Class

C

items are low dollar volume

items.

They represent only the 5% of total

dollar volume, but they include as

many as 50-60% of total inventory

items.

ABC Analysis

ABC Analysis

Some of the Inventory Management Policies that may be based on ABC analysis include:

a) Class A items should have tighter inventory control.

b) Class A items may be stored in a more secure area.

c) Forecasting Class A items may warrant more care.

Summary of ABC Analysis

•

Group A Items - Critical

•

Group B Items - Important

•

Group C Items - Not That Important

32

ABC Inventory Analysis

0

Percent of Inventory Items

P

ABC Inventory Policies

34

Greater expenditure on supplier development

for A items than for B items or C items

Tighter physical control on A items than on B

items or on C items

Greater expenditure on forecasting A items

than on B items or on C items

ABC Inventory Example

Item Unit cost Annual Usage

Annual Dollar Usage

Total Annual Persentage Usage

1 0.05 50000 2500 34.3

2 0.11 2000 220 3.0

3 0.16 400 64 0.9

4 0.08 700 56 0.8

5 0.07 4800 336 4.6

6 0.15 1300 195 2.7

7 0.20 17000 3400 46.7

8 0.04 300 12 0.2

9 0.09 5000 450 6.2

10 0.12 400 48 0.6

ABC Inventory Example

Rank by percentage of usageItem Annual Dollar Usage Total Annual Persentage Usage Cumulative Percentage Item Classification

Rank by Classification

Item Classification Items Percentage Percentage Value

A 7, 1 20 81

B 9, 5, 2, 6 40 16.5