MACROECONOMIC DETERMINANTS OF STOCK MARKET

DEVELOPMENT, EVIDENCE OF IRAN

Hadi Akbarzade Khorshidi*, Farimah Mokhatab Rafiei and Seyed Mehran Hoseini** *Corresponding Author: Department of Industrial and Systems Engineering, Isfahan University of Technology, Esteghlal Square, Isfahan 84156-83111, Iran, E-mail: [email protected]

**Department of Industrial and Systems Engineering, Isfahan University of Technology, Esteghlal Square, Isfahan 84156-83111, Iran, E-mail: [email protected], [email protected]

Abstract:The goal of our study is evaluation and determination of effective factors on stock market development of Iran. In previous studies, the effectiveness of two groups of factors (macroeconomic and institutional) has been examined by panel data method. However, in this paper the effect of macroeconomic factors are analyzed using time series and traditional econometrics (OLS) models. Income, saving, investment rate, financial intermediary development, stock market liquidity and macroeconomic instability are important factors that are evaluated. In addition, results of this study are compared with a similar study that performed on Middle-Eastern and North Africa (MENA) countries. At the end, some suggestions are proposed to develop the stock market in Iran.

Keywords: Stock market development, Determinants, Macroeconomic factors, Iran, Econometrics.

1. INTRODUCTION

Stock market development is a multi-faceted concept and there are various agents that can affect on, so identifying the effective indices has an especial importance. Dailami and Atkin (1990) tried to reveal key factors that can be substantial in developing countries. In investigation of effective agents on stock market, there are two criterion groups: macroeconomic criteria and institutional criteria. In macroeconomic approach, some criteria such as income growth, saving and investment, financial development and inflation are considered. Also in institutional approach, property laws, clearance and settlement issues, transparency and the inside information problems, taxation issues and accounting standards are evaluated.

showed that real income, saving rate, financial intermediary development and stock market liquidity are important. Ben naceur et al. (2007) used Garcia and Liu model to assess the effect of economic factors in 12 countries of Middle-Eastern and North Africa (MENA).

Pagano (1993) showed effect of institutional and regulatory factors on stock markets. La Porta et al. in duration of their study perceived that rule of law, anti-director rights and one-share = one-vote are the most effective factors on stock market.

Furthermore Calderon-Rossell in 1990 presented a model for elucidation of stock market development. In this model, economic growth and stock market liquidity are considered as main indices. Yartey (2008) extended Calderon-Rossell’s model and examined economical and institutional factors simultaneously. Macroeconomic criteria that were involved in this model, are income level, investment and saving, stock market liquidity, macroeconomic stability and private capital flows. Institutional criteria included political risk, bureaucratic quality, law and order, corruption and democratic accountability.

In this study, we want to determine effect of each macroeconomic factor on stock market development in Iran, so we use Garcia and Liu model as a basic model with marginal difference and apply time series econometric approach on it.

In Section 2, some explanations are brought about Iran’s Stock market, Section 3 describes relationship between financial and economical development. Determination of econometric model and definition of variables are lied in Section 4. Section 5 shows and interprets output of empirical investigation. Conclusion and guidelines for stock market development of Iran are in Section 6.

2. STOCK MARKET DEVELOPMENT TREND IN IRAN

In recent decades, most of the middle-eastern countries tried to implement the economical reforms and structural adjustments. Major part of these plans was involved with financial section, so that many of them were able to establish and resurrect their stock markets. As a result of this progress, stock exchanges in these countries are considered as an important phenomenon and their roles increased in international financial system (Ben naceur et al, 2007). T herefore, Iran was not separated from middle-eastern evolution trend and performed these reforms in its financial structure. Especially, Iran’s financial structure that it could be observed in middle-eastern countries, is Islamic financial market (for more detailed about Islamic financing can refer to Ramady and Kantarelis, 2009).

bond, the volume of transactions in this market increased by a good slope until 1978. Because of strikes and shutting in manufacturing and commercial units during the Islamic Revolution, legislating some laws and occurrence the war between Iraq and Iran, exchanges in stock market were stopped between 1978 and 1983.

In 1984, regarding to government decision on privatization and submission of some factories to workers, stock exchanges promoted a little. However, statistics show that there is no steady trend in stock market activities in 1989 – 1997. Tehran’s stock market began a new period of activities from 1997, so that foundation of many reforms and future evolutions in capital market was created from this year (Sanginian, 2008).

To show the status of Iranian financial markets, annual time series of some important indices are brought in diagrams 1, 2, 3, 4 (data of this diagrams extract from Central Bank of Iran). T hese indices are number of listed companies, market capitalization by GDP, value traded and turnover ratio.

Diagram 1: Changes Trend of Number of Listed Companies in Iran

Diagram 2: Changes of Market Capitalization by GDP Trend in Iran

Diagram 3: Changes of Value Traded Trend in Iran

3. STOCK MARKET DEVELOPMENT AND ECONOMIC GROWTH

T here are many works that implemented on relationships between economy and their factors, they try to interpret the economic system (Cohen, 2010; Evaghorou, 2010). Financial system is necessary for an economy because of responsibility for resource allocation. Financial intermediaries have positive effect on economic growth by decreasing of the cost of information and transactions, improving of resource allocation, promotion of saving rates and enhancement of markets and tools development (Levin, 1997; Ben naceur et al., 2007).

Surveys that done based on empirical investigations admitted that there is a positive relationship between financial development and economic growth. Goldsmith in 1969 for first time used a panel data approach for 35 countries in 1860 – 1963. Some researchers found that financial development cause increasing in economic prosperity and reinforcement in growth trend (King and Levine, 1993; Levine and Zervos, 1998; Rousseau and Sylla, 2001).

Some of other studies discovered that economic growth leads to financial development. In this view, financial markets uphold by economic expansion (Goldsmith, 1969). However, recent researches have shown that there is a bi-directional effect between finance and economy, so that each of them supports together (Shan et al., 2001).

4. RESEARCH MODEL 4.1 Econometric Modeling

T his survey uses time series information of Iran for analysis the model. In previous studies like this model, due to lack of data, panel data often is employed. Whereas using time series data has more flexibility because political and social turns that they have effected on statistical data are not considered in panel data separately (Moinul islam and Salimullah, 2006). T his attitude helps us to apply an appropriate dummy variable for illustration of Iran’s condition.

Basic model that is used in this essay is like below:

Yt=α +βXt +εt t = 1, ...,T ... (1)

WhereYt is as a dependent variable,α is constant,Xt is a vector that involvedK explanatory variables, β is a vector of explanatory variable coefficients and εt is error’s amount of each

of significance. Also, if amount ofP-value be greater than level of significance, the coefficient is not significant.

AnF value is defined to analyze this fact that right hand side variables of Eq. (1) can explain the left hand side variable. Inability of this estimation will be proven, if itsF value be small. In addition, R2 is a measure to compare regressions in explanation of dependant variable (Gujarati, 2004).

4.2 Data and Variables

In this study, the financial data of Iran’s market are extracted from Central Bank of Iran. Furthermore, a M.Sc. thesis that carried out in IUT (Isfahan University of Technology) is employed for finding economical data (Danesh, 2007). T his dissertation carefully exposed some Iran’s economical factors.

We use division of Total Market Value on GDP for dependent variable that is proxy of financial market development. Total Net Capital Stock employs to define the Total Market Value that this parameter took out from Central Bank’s data. Here, we apply this division rather than using the combination of the other development indices, because the other indices have a severe correlation together (Demirguc-Kunt and Levine, 1996).

Principal variables select from Garcia and Liu (1999) but due to better coordination with and explanation of financial development of Iran, some definitions change and some variables add to model. Explanatory variables that are used in our model come as below:

Gross domestic product: In this paper, GDP represents the income of country. However, we use logarithm of GDP for better estimation like Yartey (2008). LogGDP plays more significant role to explain the stock market development than GDP. We expect that income be an important factor in our purpose.

Saving and investment: Since financial intermediaries convert saving to investment, it’s expected that these variables have determined effects. However, due to being severe multicollinearity between these two variables, they are not brought in model together. Saving rate and investment rate were taken from a method similar to Ben naceur et al. (2007). T hese rates are computed as Eqs (3, 4)

Saving rate= Gross national saving

Gross national income ... (3)

Investment rate= Gross national investment

Gross national income ... (4)

To avoid from causality problem, we use last year amount of them.

Miller theory (1958) value of securities that are made by company could be autonomous from their money support resource, if market be perfect with symmetric information. However, in real world, market is imperfect and information is asymmetric. T herefore, being substitute or complement depends on laws, incentives or taxation system of countries. Here, domestic credit to the private sector divided by GDP is used as a proxy of financial intermediary development.

Stock market liquidity: Liquidity defines as a simplicity and velocity in security transactions that is one of functions of stock markets (Miller, 1991). Also, liquidity gives a capability to investors for economical and rapid improvement on their financial portfolios (Bencivenga et al., 1996). In this study, Value traded and Turnover ratio are used for measurement of stock market liquidity using Eqs (5, 6).

Value traded =T otal value traded

GDP ... (5)

Turnover ratio= Total value traded

Market capitalization ... (6)

These two factors are not employed in model simultaneously and last year data are used for them.

Macroeconomic instability: Macroeconomic stability is a positive factor on stock market development. Much variation in national economic could disappoint investors and firms to participate in stock market (Garcia and Liu, 1999). Also, stock return has a negative correlation with inflation rate (Fama, 1981). Floros (2004) used OLS model, Johansen method and Granger-Causuality tests to evaluate relationship between stock return and inflation rate with Greece data, he indicated that these two items are not correlated. T here are several criteria such as inflation rate, inflation change and inflation standard deviation, to compute macroeconomic instability. T herefore, we use last year Consumer Price Index (CPI) change to calculate this factor. (Iran’s inflation data is not available).

Lagged variable of dependent variable: By reason of better estimation of stock market development, amount of last year Total Market Value by GDP add to explanatory variables like Yartey (2008).

Trend variable: Due to increase significance of estimators, this variable insert in model.

Dummy variable: Regarding Iran’s stock market history and Diagram 3, stock market between 1978 and 1983 was inactive. As a result, a dummy variable put in model for covering these changes so that the value of this variable in 1978 – 1983 is zero and in the other years is one.

5. EMPIRICAL RESULTS

Table 1

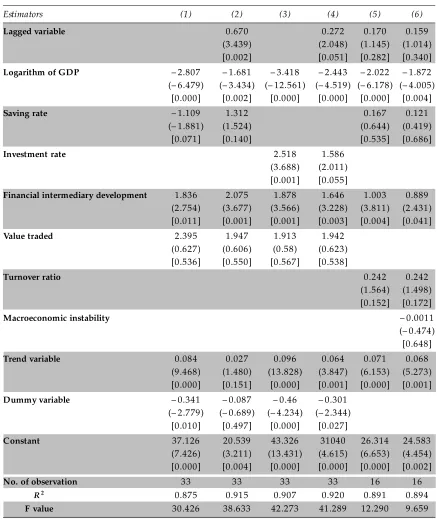

Results of Statistical Estimation Amounts in the Parenthesis aret-value and Values in Bracket areP-value

Saving rate – 1.109 1.312 0.167 0.121

(– 1.881) (1.524) (0.644) (0.419)

[0.071] [0.140] [0.535] [0.686]

Investment rate 2.518 1.586

(3.688) (2.011) [0.001] [0.055]

Financial intermediary development 1.836 2.075 1.878 1.646 1.003 0.889

(2.754) (3.677) (3.566) (3.228) (3.811) (2.431)

Trend variable 0.084 0.027 0.096 0.064 0.071 0.068

(9.468) (1.480) (13.828) (3.847) (6.153) (5.273) [0.000] [0.151] [0.000] [0.001] [0.000] [0.001]

Dummy variable – 0.341 – 0.087 – 0.46 – 0.301

(– 2.779) (– 0.689) (– 4.234) (– 2.344) [0.010] [0.497] [0.000] [0.027]

Constant 37.126 20.539 43.326 31040 26.314 24.583

(7.426) (3.211) (13.431) (4.615) (6.653) (4.454) [0.000] [0.004] [0.000] [0.000] [0.000] [0.002]

No. of observation 33 33 33 33 16 16

R2 0.875 0.915 0.907 0.920 0.891 0.894

Column (1) shows that income, saving rate and financial intermediary development have significant effect on stock market development, but value traded is insignificance. It should be mentioned that income and saving rate have negative sign. In column (2) lagged variable add to the model for evaluation of its effect. As it can obtain from table, only significance of saving rate reduces so that it’s not significant at 10 percent level. However, the other variables improve, especially the coefficient of saving rate becomes positive. As a result of these observations, lagged variable has a good effect on model. Although these improvements occurred, coefficient of income is negative yet. T his event may be interpreted in this way that by income growing money and capital push to other sections such as trading, purchasing real estate, etc. in Iran. Also, stock markets in Iran are small. It must be cited that in study that performed by Ben naceur et al for MENA countries, income had an insignificant outcome.

Saving rate and financial intermediary development have positive and significant effect that these effects are according to Ben naceur et al. However, value traded is insignificant whereas this criterion for MENA countries had significant positive coefficient.

Investment rate enters to model in third column. Coefficient of this factor is positive and significant but this factor in MENA was negative insignificantly. Column (4) has a lagged variable more than column (3) that this variable has the same before influences.

In column (5), turnover ratio substitutes with value traded. T his criterion has not significance effect on stock market development. In general, estimation that created in column (5) is weaker than column (2). Despite this observation, turnover ratio in compare to value traded is more significant. It must be mentioned that data for turnover ratio is available for 1991 – 2007, so this column doesn’t need to participate the dummy variable.

Column (6) evaluates effect of instability using last year CPI change. As we expected the coefficient of this factor is negative but it’s not significant that these results are in accordance with MENA countries.

6. CONCLUSION

We have utilized Garcia and Liu model to analyze the effect of macroeconomic factors on Iran’s stock market development. For adaptation the model with Iran’s data, lagged, trend and dummy variables are inserted to the model so that these variables enhance the impact of the estimation equation. To sum up, income factor has negative coefficient and remains having inappropriate effect on stock market. Saving and investment rates are positive and significant but investment rate is more significant according to columns 1 to 4 of Table 1. Financial intermediary development is positively effective. Although, they are positive, none of the liquidity criteria is significant. Also, the macroeconomic instability is an insignificant negative factor.

market. Second, due to promotion of investment rate, the investment share of national income must be increased. At the end, along with the effect of financial intermediaries, privatization is an accurate policy to expansion.

For the further research, it could be a good suggestion to determine the causality between stock market development and economic growth in Iran. In addition, the relationship between financial intermediaries and stock markets may be evaluated in Iran. If they are complements or substitutes in growth process.

REFERENCES

[1] Bencivenga V.R., Smith B.D. and Starr R.M., (1996). “Equity Markets, Transaction Costs, and Capital Accumulation: An Illustration”,World Bank Economic Review,10, 241 – 265.

[2] Ben naceur S., Ghazouani S. and Omran M., (2007). “T he Determinants of Stock Market Development in the Middle-Eastern and North African Region”, Managerial Finance, 33 (7), 477 – 489.

[3] Calderon-Rossell R. J., (1990). “T he Structure and Evolution of World Stock Markets”, in S. Ghon Rhee and Rosita P. Chang (eds.),Pacific Basin Capital Markets Research Proceeding of the First Annual Pacific Basin Finance Conference, Taipei, China, 13 – 15 March 1989, (Amsterdam: North Holland).

[4] Central Bank of Islamic Republic of Iran, http://tsd.cbi.ir/IntT SD /EnDisplay/Display.aspx. [5] Cohen S.I., (2010). “Behavioural Types Determining Economic Systems”, International Journal

of Society Systems Science,2 (1), 26 – 51.

[6] Dailami M. and Atkin, M. (1990), “Stock Markets in Developing Countries, Key Issues and a Research Agenda”,The World Bank Financial Policy and Systems, WPS 515.

[7] Danesh A., (2007), “Evaluation of R and D Role in Economic Growth of Iran”, Unpublished M.Sc. Thesis, Isfahan University of Technology, Isfahan, Iran.

[8] Demirguc-Kunt A. and Levine R., (1996), “Stock Markets, Corporate Finance, and Economic Growth: An Overview”,World Bank Economic Review,10, 223 – 239.

[9] Evaghorou E.L., (2010). “T he State Strategy in Today’s Global Economy: A Reset Position in the T heory of International Political Economy”,International Journal of Society Systems Science,2 (3), 297 – 311.

[10] Fama E., (1981). “Stock Returns, Real Activity, Inflation and Money”,American Economic Review,

71, 545–565.

[11] Floros C., (2004). “Stock Returns and Inflation in Greece”,Applied Econometrics and International Development,4 (2), 55 – 68.

[12] Garcia F.V. and Liu L., (1999). “Macroeconomic Determinants of Stock Market Development”, Journal of Applied Economic,2 (1), 29 – 59.

[14] Gujarati D ., (2004). “Basic Econometrics”, McGraw Hill, Fourth Edition.

[15] King R.G. and Levine R., (1993). “Finance and Growth: Schumpeter Might be Right”,Quarterly Journal of Economics,108, 717 – 38.

[16] La Porta R., Lopez-de-silanes F. and Shleifer A., (1997). “Legal Determinants of External Finance”, Journal of Finance,52, 113 – 150.

[17] Levine R., (1997). “Financial Development and Economic Growth: Views and Agenda”,Journal of Economic Literature,35, 688 – 726.

[18] Levine R. and Zervos S., (1996). “Stock Markets, Banks, and Economic Growth”, The World Bank Policy Research working paper, 1690.

[19] Miller M., (1991). “Financial Innovations and Market Volatility”, Blackwell, Cambridge. [20] Modigliani F. and Miller M.H., (1958). “T he Cost of Capital, Corruption Finance, and the

T heory of Investment”,American Economic Review,48 (3), 261 – 297.

[21] Moinul Islam A.N.M. and Salimullah A.H.M., (2006). “Effects of Private Investment, Economic Freedom and Openness on Economic Growth: LDC Experience”,Asian Affairs,28 (1), 46 – 68. [22] Pagano M., (1993). “Financial Markets and Growth: An Overview”,European Economic Review,

37, 613 – 622.

[23] Ramady M.A. and Kantarelis D., (2009). “Financial Capital Democratisation: Recipes for Growth and Disaster”,International Journal of Society systems Science,1 (4), 325 – 350.

[24] Rousseau P.L. and Sylla R., (2001). “Financial Systems, Economic Growth and Globalization”, NBER working paper, 8323.

[25] Sanginian A., (2008). “Tehran’s Stock Market History and its Revolution Trend”,The world of economy newspaper,1731, 11.

[26] Shan J.Z., Morris A.G. and Sun F., (2001). “Financial Development and Economic Growth: An Egg and Chicken Problem?”,Review of International Economics,9, 443 – 454.