INTRODUCTION

DEAL UNIVERSE

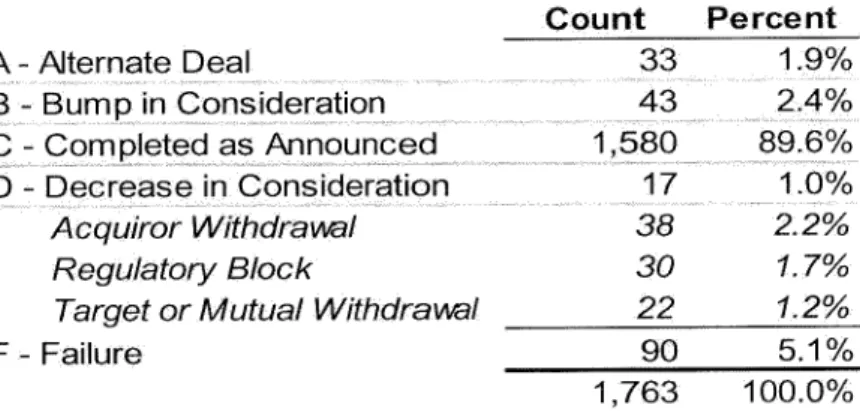

DEAL OUTCOMES

SDC Platinum also has a "Changed Value" field intended to indicate when there has been an increase or decrease in the amount paid to shareholders (categories "B" and "D" in the typology described above). DEP'T OF THE TREASURY, https://home.treasury.gov/policy-issues/international/the- Committee-on-foreign-investment-in-the-united-states-cfius (last visited 16 March 2020).

MARKET EXPECTATION OF DEAL BREAKAGE

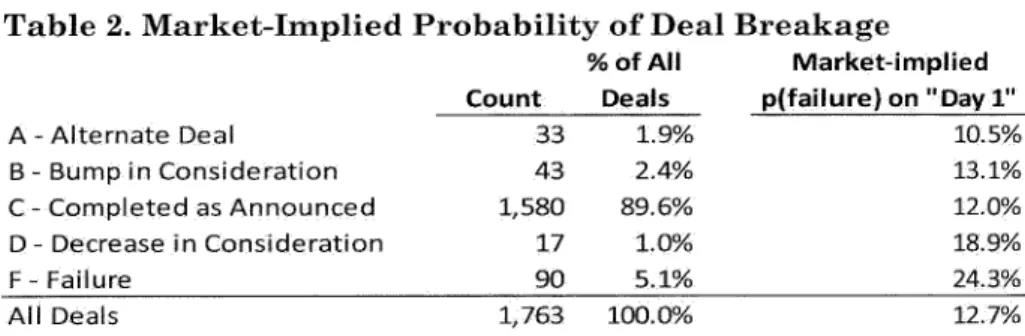

For each trade, company press releases between the signing date and the expiration date were reviewed for each transaction to determine the trade's outcome. The biggest risk is the possibility that the trade breaks down, causing the target's share price to fall back to "unaffected". The trading spread thus conveys information about the market's estimate of the probability of a trade going bust.

The probability can be calculated as the spread of a trade of $2 (that is, $30 of compensation per share minus the market price of $28) divided by the premium of $10 (that is, $30 of compensation per share minus $20 of the flat price). ), or 20 percent. In traders' terminology, this is the "market-implied probability" of a trade being broken.3 5 In the simplified setup described here, the market-implied probability of breaking is the trade's spread divided by the trade's premium. In practice, merger arbitrators must adjust this calculation for the appropriate risk-free interest rate (which in the example above is assumed to be zero) as well as for the expected target dividends per share between the signing date and the anticipated closing date.36 Even in deals that involve stock consideration, the merger arbitrator must short the acquiring company's stock to "lock in" the spread,3 7 which requires additional adjustments to the market-implied probability calculation.

The difference between the target's stock price and the offer price is known as the arbitrage spread. Specifically, the default probability implied by the market is calculated based on the contract spread observed at the close of trading on the trading day following the announcement of the contract.

TIME TRENDS

Broken down by deal outcome, the market on "Day 1" assigns a higher probability of failure to deals that continue to fail (24.3 percent on average) than to deals that close on announced terms (12.0 percent). In other words, the market seems to successfully identify ex ante which deals are most likely to break. For deals that continued to break down, the market on day one assigned a 75.7 percent chance of final completion—in other words, the arbitrageurs believed that the deal was more likely than not.

Notably, the market-implied probability of failure exceeds realized adverse outcomes every year. In other words, the difference between market expectations and realized outcomes appears to have narrowed somewhat after 2000. One possibility is that market participants have learned over time to assess deal risk more accurately.4 1 Another related possibility is that merger arbitrage may have been an undercapitalized form of merger arbitrage. investment strategy in those earlier years.4 2 Several years of high returns may have attracted more capital to the strategy, lowering spreads and bringing the market-implied probabilities of failure slightly closer to reality.4 3.

John Coates has noted that M&A contracts more than doubled in size and in terms of linguistic complexity between 1996 and 2015.44 Impressionistically, this is not the case with contractual growth. The extent to which specific contractual features are associated with a greater likelihood of deal completion is an important topic for further research.

TARGET COMPANY CHARACTERISTICS

Target Industry

Neither financial services transactions nor media and telecommunications transactions show a high incidence of regulatory blockages, despite the power of sectoral regulators to block many of these transactions. Indeed, apart from public utilities, consumer/retail transactions have the highest rate of regulatory blocks, despite the fact that few consumer/retail transactions are subject to sectoral regulatory approval; almost all of these regulatory blocks were on antitrust grounds. However, actions with public utility targets are consistent with the prediction of a high incidence of regulatory blocks.

Public utility contracts are uniquely exposed to regulatory risks in the form of state public utility commissions. Even more surprising is the incidence of withdrawals from acquirers and declines in industry consideration. Deals with tech company targets, far from having a high incidence of these negative outcomes, have the lowest, with only 1.6 percent of tech company deals failing due to acquirer withdrawals, and zero of those deals involving a contractual drop in consideration .

Likewise, deals with utility targets, far from having a low incidence of buyer withdrawals and consideration reductions, have the highest, at 8.1 percent and 3.5 percent, respectively. In any case, acquirer withdrawals and downgrades do not appear to be driven much by the volatility of the target company's industry.

Target Size (Deal Value)

ACQUIRING COMPANY CHARACTERISTICS

The data set therefore includes transactions involving not only US but also foreign acquirers, and not only public but also private acquirers.

Acquiror Nationality

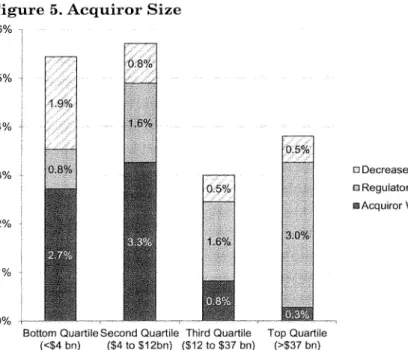

Acquiror Size

One hypothesis is that they sign "better" deals by, for example, doing more thorough due diligence and thereby avoid signing buyer's remorse. Another hypothesis, in tension with the first, is that larger acquirers are poor negotiators and fail to include provisions in their agreements that allow them to withdraw from a deal that turns out to be bad. A third possibility is that larger acquirers give up this option, not because they are bad negotiators, but because they systematically trade optionality for other contract terms.

Fourth, because (holding everything else constant) any given purchase is "lower stake" for a larger buyer than for a smaller buyer, larger buyers can more easily decide to bite. point and conclude a deal whose foundations have gone south.

Strategic versus Financial

TRANSACTION CHARACTERISTICS

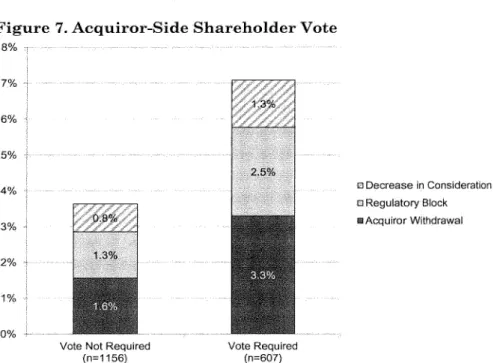

Acquiror Shareholder Vote

It would be reasonable to hypothesize that transactions conditioned on an acquirer-side shareholder vote, all else being equal, would experience a higher rate of adverse outcomes given the additional veto point at the center of the transaction. In compiling the data set, merger agreements for each transaction were reviewed to determine whether the transaction was conditioned on a shareholder vote on the acquirer side. As shown in Figure 7, these deals had an unfavorable outcome probability almost twice that of deals where no shareholder vote was required on the acquirer side.

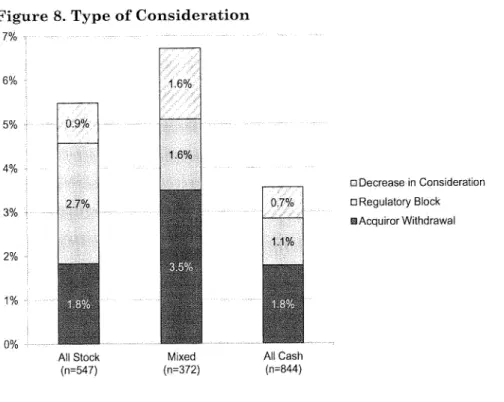

Type of Consideration

All-cash and all-stock deals have an equal incidence of acquirer withdrawals, but all-stock deals were more than twice as likely as all-cash deals to be blocked for regulatory reasons. This is reasonable: Very large trades, which are associated with elevated antitrust risk, are disproportionately all stocks. An interesting finding is that negative outcomes other than regulatory blocking (ie, withdrawals from acquirers and declines in consideration) are elevated in mixed considerations (cash and stock).

Indeed, these (non-regulatory) adverse outcomes are more than twice as common in mixed-stakes deals as in all-stock, all-cash deals.

Premium

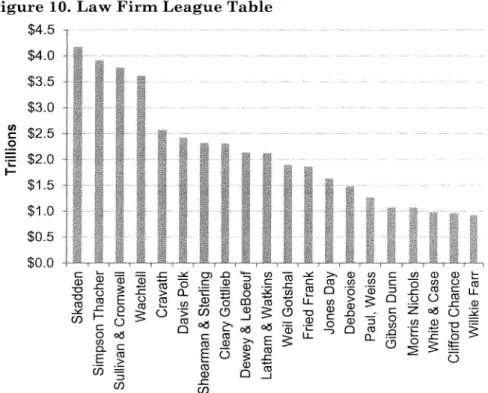

LEGAL ADVISoRs

In theory, more competent and experienced M&A advisors will deliver better deal terms for their clients. As noted in Part I, target firms prefer contracts that limit the acquirer's ability to withdraw from the deal, while maintaining maximum freedom of choice for the target to accept a third-party offer if one arises.66 Acquiring firms prefer the opposite: contracts that preserve their ability to withdraw from the deal while limiting the target company's. Deals in which a bulge bracket firm represents the target but not the acquirer experience a significantly lower rate of acquirer withdrawals than those in which a bulge bracket firm represents the acquirer but not the target.

This finding is consistent with the hypothesis that the most experienced M&A advisors (measured at the law firm level) succeed in negotiating better deals for their clients, at least when compared to less experienced M&A advisors.6 7. Instead of would show negative results, it shows premium results: deals where the target later received a more favorable deal (from an economic point of view) than the one originally signed. Here again, the target firms outperformed at higher frequencies when they retained the bulge bracket advisor, but the acquirer did not.

Acquirers have done better, largely because they have avoided the need to pay extra attention if they have only used a company with bulging brackets. . equity law firms are associated with a number of important bidding outcomes and characteristics.") The use of bulge bracket counsel by one party or the other may correlate in a systematic manner with business or deal characteristics relevant to deal outcomes.

POSTSIGNING MARKET DEVELOPMENTS

As with the other statistics reported in this article, these correlations should be interpreted with caution. The influence of legal advisors on transaction outcomes has previously been examined in various contexts;6 8 extending these studies to the outcomes of mergers and acquisitions may be a fruitful area for future research. Of the twenty-one deals with a financing contingency, four were buyer withdrawals and no other adverse effects.

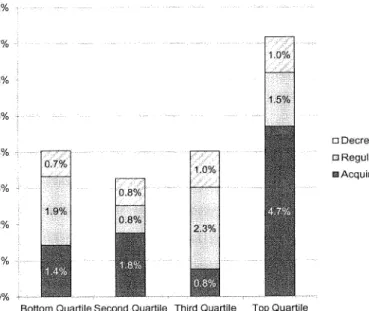

Given the lack of funding contingencies in the deal universe, it can be hypothesized that post-signature developments in financial markets would have little impact on deal outcomes. The BBB bond spread, downloaded from the Federal Reserve's Economic Database,6 9 measures the difference between yields on a basket of BBB-rated corporate bonds and the risk-free rate. The figure shows that transactions in the highest quartile (ie, those that coincided with the largest increase in the BBB bond spread between the underwriting date and the outcome date) experienced negative outcomes with significantly greater frequency than those in the lowest. .

Bernanke, The Nonmonetary Effects of the Financial Crisis in the Spread of the Great Depression, 73 AM. explains that the banking problems of the Great Depression "disrupted the credit allocation process by creating large, unplanned changes in the channels of credit flow.").

CONCLUSION