5TH ASEAN’S

INTERNATIONAL CONFERENCE ON ISLAMIC FINANCE

(AICIF)

VOLUME 2

5TH ASEAN’S

INTERNATIONAL CONFERENCE ON ISLAMIC FINANCE

(AICIF) VOLUME 2

EDITED BY

ABDUL GHAFAR ISMAIL

ROSE ABDULLAH

Published by:

UNISSA Press

Centre for Research and Publication Sultan Sharif Ali Islamic University Simpang 347, Jalan Pasar Baharu BE 1310, Gadong

Brunei Darussalam

© UNISSA Press First Published 2017

All right reserved. No part of this book may be reprinted or reproduced or utilized in any form or by any electronic, mechanical or other means, now known or hereafter invented, including photocopying and recording, or in any information storage or retrieval system, without permission in writing from the copyright owner.

Perpustakaan Dewan Bahasa dan Pustaka Brunei

Pengkatalogan Data-dalam-Penerbitan (Cataloguing-in-Publication)

ASEAN International Conference on Islamic Finance (5th : 2017 : Bandar Seri Begawan) Proceedings 5th ASEAN’S InternationalConference on Islamic Finance (AICIF) (Vol. 2). -- Bandar Seri Begawan : UNISSA Press , 2017.

414 p. 21.59 cm x 27.94 cm.

E-ISBN 978-99917-82-79-9 (Ebook)

1. Finance--Islamic countries--Congresses 2. Bank and banking--Islamic

countries--Congresses 3. Finance--Religious aspects--Islam--Congresses 4. Islamic countries--Economic conditions--Congresses 5. Globalization--Economic aspects-- Congresses I. Title

332.091767 ASE (DDC 23)

i CONTENTS

LIST OF CONTENTS i-iii

1. Sharia Marketing Innovativeness on Marketing Performance Model

Hendar & Mutamimah

1-16

2. Maqashid Al-Sharia Approach in Human Development Index: Case Study at Six Provinces in Java Island Dr. Muhammad Zilal Hamzah & Dr. Eleonora Sofilda

17-30

3.

ةيداصتقلاا تلاماعملا ىف ةعيرشلا دصاقم قيبطت

Mulyono Jamal

31-39

4. The Financial Stability of Islamic Financial Institutions in Malaysia

Nur Lalua Rashidah Mohd Rahsiad & Nur Hidayah Mohd Nor

40-46

5. Grievances on Islamic Banking Issues: Causes and Remedies Ahmad Shaharudin Abdul Latiff, Haryani Haron &

Muthukkaruppan Annamalai

47-57

6. The Contribution of Islamic Social Reporting to The Financial Performance of Sharia Banking in Indonesia Provita Wijayanti & Mutoharoh

58-67

7. Towards Transforming The Cooperative to a Bank: An Analysis

Selamah Maamor, Husin Abdullah, Fauzi Hussin, Norehan Abdullah * Mohd Saifoul Zamzuri Noor

68-83

8. Privatization Predicament and Shari’ah Compliant Alternate Solutions

Malik Shahzad Shabbir

84-89

9. A Study of Factors Influencing The Choice Of Islamic Banking Among Non-Muslim Customers in Nigeria Buerhan Saiti & Abubakar Aliyu Ardo

90-99

10. Islamic Banking Dispute: Critical Analysis on The Contract Structuring and Recovery Practices

Dr Hakimah Yaacob, Dr Kamaru Salam bin Yusof & Hajah Nurliza binti Dato Mahalle

100-110

11. Examining The Shariah Non-Compliance Events in The Malaysian Islamic Financial Institutions: Post Shariah Governance Framework Implementation

Prof. Dr. Rusni Hasan, Muhammad Issyam bin Itam@Ismail &

Associate Prof. Dr Adnan Yusoff

111-123

ii 12. The Impact Of Sharia Principle Adherence and Islamic

Corporate Governance on Trust in Islamic Financial Institutions

Lisa Kartikasari

124-129

13. Islamic Corporate Governance and Islamic Reporting in Sharia Banks: The Case Of Indonesia

Luluk Muhimatul Ifada

130-136

14. Equal Employment Opportunity in Leadership of Islamic Universities

Tri Wikaningrum, Ahyar Yuniawan & Udin

137-153

15. Antecedents of Enterpreneurship’s Motivation Among Young Muslim Students

Nurhidayati

154-158

16. The Impact of Knowledge Sharing and Islamic Ethic Works on Innovation Capability and Competitive Advantage of Small and Medium Enterprises

Mulyana & Sutapa

159-169

17. Developing Framework for Improving Indonesian Islamic Banking Performance Through The Construct of Service Innovation, Human Capital Drivers, and Knowledge Management Capability

Ruspita Rani Pertiwi, Jann Hidajat Tjakratmadja & Hary Febriansyah

170-186

18. The Effects of Enterprise Risk Management on Bank Performance: Evidence from Indonesian Public Listed Companies

Hamdi Agustin, Azwirman & Siska

187-194

19. Analysis of Effect of Intellectual Capital and Good Corporate Governance to Bank in Indonesia Sri Indrastuti, Amris Tanjung & Hamdi Agustin

195-200

20. The Effect of Institutional Ownership, Profitability and Company Size on Islamic Social Reporting

Sutapa

201-210

21. Faktor Determinan Rendahnya Likuiditas Project Based Sukuk di Pasar Sekunder

Wafi Azkia Zahidah & Rizal Nazarudin Firli

211-224

22. Implications of Islamic Corporate Social Responsibility (Icsr) and Corporate Social Responsibility (Csr) on Firm Value: A Conceptual Model (Comparative Study of Islamic Banking Versus Conventional Banking)

Muhammad Ja’far Shodiq

225-233

iii 23. Earning Management of Indonesian Islamic Banks

Saiful

234-243

24. Legal Documentation in Islamic Home Financing in Malaysia: Concepts, Conundrums, and Contextualization Syarah Syahira Mohd Yusoff

244-256

25. Determining The Causes of Bank Runs in Sharia Banking in Indonesia

Sunaryati

257-277

26. Service Quality from Customer Perception: Evidence from Carter Model on Bank Islam Brunei Darussalam (Bibd) Qaisar Ali

278-293

27. Sharia Financing Analysis on The Financial Performance Sharia Banking in The Moderation of The Syariah

Supervisory Board (Dps)

Osmad Muthaher & Edy Suprianto

294-306

28. Bounded-Mosharaka A Unifying Islamic Banking and Finance Contract

Dr Fawzi Gherfal

307-332

29. Determinants of Corporate Governance Disclosure in Indonesian Islamic Banks

Hendri Setyawan & Devi Permatasari

333-346

30. Analysis of Good Corporate Governance (Gcg)

Implementation Effect on The Achievement of Maqashid Sharia of The Indonesian Islamic Banking for The Period of 2012 – 2015

Rifaldi Majid & Moh. Hamilunni’am

347-369

31. Corporate Governance and Islamic Social Reporting in The Indonesia Sharia Banking Companies

Indri Kartika

370-386

32. Shariah Governance in Islamic Wealth Management: A Learning Lesson from Securities Commission Malaysia Nor Razinah Mohd Zain, Prof. Dr. Rusni Hasan & Assoc. Prof.

Dr. Salina Kassim

387-396

33. Islamic Microfinance in The Light of Maqasid Shariah from Experts’ Perspective

Hartomi Maulana & Khoirul Umam

397-414

THE DISCLOSURE OF CORPORATE SOCIAL RESPONSIBILITY IN THE SHARIA PERSPECTIVE: THE EFFECT OF SHARIA SUPERVISORY BOARD

AND FINANCIAL PERFORMANCE AS A MEDIATING VARIABLE (AN EMPIRICAL STUDY ON SHARIA BANKING IN INDONESIA)

Winarsih

Department of Accounting, Faculty of Economics, UNISSULA, Semarang, Indonesia Email: [email protected]

Abstract

The measurements of CSR disclosure in Sharia perspective using the ISR index (Sharia Social Reporting) are listing the reported accounts of CSR activities in accordance with Sharia principles. This research aims to examine the relationship of Sharia Supervisory Board against disclosure of Corporate Social Responsibility with the financial performance as Mediating Variable. This research was conducted on Sharia banking registered in Sharia Banking Statistics of the financial services authority (OJK-RI) during 2010-2011. The sample of this study amounted to 6 pieces of Sharia banks which were selected through purposive sampling technique. Data analysis technique used in this study was the Structural Equation Modeling (SEM) with AMOS Version 16. The results showed that the Sharia supervisory board was associated positive against disclosure of CSR. However, based on the financial performance of variable role as a mediation variable, it is indicated that financial performance is not able to mediate the relationship between the DPS with CSR disclosure of sharia bank in Indonesia.

Keywords: Corporate Social Responsibility Disclosure, ISR Index, Sharia Supervisory Board, Intellectual Capital, Financial Performance

INTRODUCTION

The Sharia based business entities such as sharia banking have a foothold in implementing and disclosing CSR activities, as regulated in Law no. 21 of 2008 concerning Sharia Banking. The regulation states that Sharia Bank and Sharia Business Unit (UUS) can perform social functions in the form of zakat, infaq, alms or other social funds and deliver to the organizations of zakat management. It also can raise endowments (money) and distribute it to the management (Nazhir) in accordance with the will of the waki). Sharia banking in carrying out operational activities will be formed the Baitul Maal to manage CSR and charity, alms, and qard hassan (loans without profit).

The CSR in Sharia perspective is a consequence of Islam, and the objective of Sharia law (Maqasid al shariah) is maslahah so the business is an effort to create maslahah and has a position of great depth, and one way to reduce problems in society. Islam requires the circulation of wealth to occur in all members of society and prevent the occurrence of circulation of wealth only in some people (Yusanto and Yunus, 2009: 165-169). Allah says: ".... so that it may not move around the rich among you ..." (Surah Al Hasyr: 7).

The practice of CSR in Islam emphasizes the ethics of Sharia business. The operational companies must be free from various modes of corruption (fight agains corruption) and provide maximum service guarantee throughout its operational place, including trusted services for each products (provision and development of safe and reliable products). This is explicitly stated in the Qur'an. Allah SWT says: "....

Then the full measure and weight and do not subtract for humans goods of dosing and weighing ...." (Qur'an, al-A’raf: 85).

In addition to emphasizing social activities in the society, Islam also orders CSR practices on the environment. The environment and preservation are one of the main teachings of Islam. The fundamental principles shaped the philosophy of environmental virtue performed holistically by the Prophet Muhammad are the belief in the existence of interdependence among God's creatures. Allah SWT creates this universe measurably, both quantitative and qualitative (QS. Al Qamar: 49) and in balanced condition (Surah Al Hadid: 7). From this principle, the consequence is if humans corrupt or neglect one part of Allah's creation, then nature as a whole will experience suffering which in the end will also harm human (Sharing, 2010). Allah SWT says: "It appears that the destruction on the land and at the sea is caused by the deeds of human hands, Allah may feel to them a part of their (consequence) deeds that they may return (to the right way)." (QS. Ar Rum:

41).

It explains that Islam has been set up with very clear about the basic principles contained in the CSR, even though the new CSR issues began in the 20th century.

According to the Sharia perspective, the obligation carried out CSR is not only about fulfilling legal and moral obligation, but also a strategy in order to companies and people still survive in the long term. If CSR is not implemented, there will be more costs to be borne by the company then. Conversely, if the company carries out CSR with good and hard-working actively compensate for the rights of all stakeholders based on fairness, dignity, and justice, and ensure the fair distribution of wealth, it would be really beneficial for the company in the long term. In contrast to conventional banks cannot be dichotomized separately between business orientation and social orientation. The social activities of Sharia banks are an additional value implicated in increasing long-term profitability and good will acquired in a positive image of the business works and

increase confidence of stakeholders on the performance of Sharia banks. If CSR is not implemented then, there will be more costs to be borne by the company. Conversely, if a company executes CSR well and actively works hard to balance the rights of all stakeholders based on fairness, dignity, and fairness, and ensuring a fair distribution of wealth, it will actually benefit the company in the long term.

The measurement used by the Sharia banking to express its social responsibility using indexes Sharia Social Reporting (ISR), which is the standard reporting of social performance of companies based on sharia emphasis on social justice related to the environment, the rights of minorities, and employees (Fitria and Hartanti, 2010). There are five themes disclosing ISR index, namely financing and investment themes, themes of the products and services, employees theme, the theme of community and environmental themes. Five themes such disclosure developed by Othman et al (2009) by adding a disclosure theme is the theme of corporate governance.

Sharia banking as well as conventional banks is required to have a good performance, where performance level is a commonly used measure of financial

performance using several aspects, namely capital,

quality of assets, management, earnings and liquidity. The Sharia Supervisory Board Effectiveness will effect financial performance and corporate social responsibility. This matter shows that GCG practice will produce the financial performance higher and also corporate social responsibility.

The previous studies related to the implementation of the Sharia Supervisory Board (SSB) on the disclosure of CSR in Sharia banks including this research have been done by Haniffa (2007), Chariri (2012), Rizkiningsih (2012), Khoirudin (2013), Rahman and Abdullah (2013), as well as Musibah and Wan (2014). Chariri (2012) used the Sharia corporate governance variables as dependent variable with proxy characteristics such as the presence of DPS and DPS Composition Skills. Chariri (2012) stated the existence of the Sharia Supervisory Board and the composition of the membership of the DPS effected on the level of CSR disclosure. Rahman and Abdullah (2013) also examined the relationship of SSBSCORE (Sharia Supervisory Board-SCORE), the number of board members, cross membership, secular education qualifications, reputation and expertise of scholars SSB against CSR disclosed using ISR indexes in an annual report on the State Sharia banks incorporated in the GCC (Gulf Council Countries) with the control variables of bank size, financial performance using ROD (Return on Debt), and economic performance using GDP. Based on the research of Rahman and Abdullah (2013) SSBSCORE has a significant effect on CSR disclosure.

Musibah and Wan (2014) conducted a study to determine the effect of Sharia Supervisory Board Effectiveness (SSBE) and Intellectual Capital (IC) on Corporate Social Responsibility (CSR) among 36 Sharia Banks in GCC countries during 2007-2011 with financial performance as a mediation variable. They found a positive effect relationship between SSBE and CSR.

In contrast to the research of Chariri (2012), Rahman and Abdullah (2013), and Musibah and Wan (2014), Khoirudin (2013) in their research showed the sharia supervisory board size variables did not affect CSR disclosure using ISR index of sharia banking in Indonesia. Khoirudin (2013) explained the average of ISR disclosure conducted by Sharia banks was 55.20% with the population of the study were all Sharia banks in Indonesia. He got same results (2013) according to the research was conducted by Rizkiningsih (2012) claimed Sharia governance scores did not significantly affect the ISR disclosure, the research concluded there was still a lack of attention to the Sharia Supervisory Board for the ISR disclosure.

Reminding the importance of the responsibilities of the Sharia Supervisory Board in the continuity of Sharia Banks, it is necessary to re-examine them. The researcher intends to prove empirically the relationship between the Sharia Supervisory Board (SSB) on the CSR disclosure of Sharia Banking in Indonesia with the Bank Syariah financial performance as its mediation variable.

REVIEW OF RELATED LITERATURE 1. Stakeholder Theory

Stakeholder theory is a theory describes to any parties of responsible company (Freeman, 2001). Stakeholder theory said the company is not only the entity operates for its own sake, but also to be able to provide benefits to stakeholders. The companies must maintain a relationship with his stakeholders to accommodate the desires and needs of its stakeholders, especially the stakeholders who have the power to availability of resources used for the company's operational activities, e.g. the labor market on the company's products and others. When stakeholders control the important economic resources to the company, it will react in satisfaction ways to the stakeholders’ desire (Chariri and Ghozali, 2007).

Deegan (2004) stated the stakeholder theory emphasizes the accountability of the organization exceeds the financial performance or simple economic. This theory stated that the organization will voluntarily disclosed information about the company's environmental, social and intellectual performance, beyond mandatory requested such as financial statements to meet actual or recognized expectations by stakeholders. Thus, stakeholders’ theory considers powerful stakeholders in positions. This stakeholder group is the main consideration for the company in disclosing and/ or not disclosing any information in the financial statements. Groups of "stake", according to (Riahi- Belkaoui, 2003) including shareholders, employees, customers, suppliers, creditors, government, and society. The whole potential of the company, both employees (human capital), physical capital, as well as structural capital must be used optimally in order to create value added for companies that can drive a company's financial performance and CSR for the benefit of stakeholders.

2. Agency Theory

Agency theory is a concept described the relationship between principal and agent. The principal party is the party which mandates the other party, the agent, to perform all activities on behalf of the principle in its capacity as a decision maker (Sinkey, 1992 in Prajitno, 2009). The agency theory assumes that the CEO (agent) has more information than the principal because the principal cannot observe the activities carried out agents continuously and periodically, resulting asymmetry of information. The emergence of agency problems, make the company should tighten supervision of Sharia banking by applying the good corporate governance. Sharia banks implement their corporate governance by setting up a regulatory body known as the Sharia Supervisory Board who served as Sharia Compliance Bank as a manifestation of the principles of sharia compliance.

3. Disclosure of CSR in Sharia Perspective

Social disclosure in Sharia perspective consists of full disclosure and social accountability (Hannifa, 2002). The concept of accountability is related to the principle of full disclosure aimed at serving the public interest. In Islam, the public has the right to know the operational effects of an organization on prosperity and advisable in Sharia requirements whether the established goals have been achieved (Baydoun and Willet, 1997 in Othman et al., 2009).

The goal of Sharia Social Reporting by Hannifa (2002) consists of two things. First, ISR is a way to show corporate accountability not only to God, but also to society. Second, ISRs are used to improve the transparency of business activities by providing relevant information in the formation of conformity to the spiritual needs of decision makers.

Othman et al. (2009) explained that the ISR contains items of social reporting standards set by AAOFI (Accounting and Auditing Organization for Sharia Institutions) which is then developed by the researchers regarding ISR items that should be disclosed by an Sharia entity. The themes in the ISR is similar to the theme in a conventional social disclosure, the difference of ISR aims to serve the principles of business ethics Islam and the items to be reported ISR emphasized different. Hannifa (2002) proposed five themes of disclosure: finance and investment, products, employees, and the environment. The scope of the disclosure of the ISR on the five themes,

namely a) Financial and investment, b) products

and services, c) Employees, d) Society and e) Environment.

4. Sharia Supervisory Board (DPS)

The application of shariah compliance was realized by the Shariah Supervisory Board. The important role of the Sharia Supervisory Board (DPS) in maintaining a sharia compliance is responsible for overseeing services, and products offered by banks and bank operations has implemented and adheres to Sharia principles.

Sharia Supervisory Board is an element that creates a sharia compliance assurance and the one of the main pillars in the implementation of Good Corporate Governance (GCG) of Sharia banks. The more experienced DPS members will be able to improve business skills through collective decision-making and strategic decision action. The previous studies (John & Senbet, 1998; Sharma, 2011; Accidents and Wan, 2014) have been used DPS effectiveness as measure corporate governance.

In Indonesia, DPS is responsible to the National Sharia Board-Majelis Ulama Indonesia (DSN-MUI) and Bank of Indonesia. The provisions on membership numbers vary for each country, but on the same functions and duties (Akbar, 2008). The membership of the Sharia Supervisory Board has been regulated in DSN-MUI Decree no. 30 of 2000 (Sutedi, 2009: 143).

5. Financial Performance

The measurements of bank's financial performance can be seen from the soundness of the bank. Based on Bank of Indonesia Regulation No.9/ 1/ PBI/ 2007 was concerning Rating System of Commercial Banks based on Sharia Principles and Circular Letter of Bank Indonesia No.9/ 24/ DPbS in October 30, 2007 concerning Rating System of Commercial Banks based on Sharia Principles. The measurement and assessment of bank performance could use some aspects, namely Capital, Asset Quality, aspect Management, earnings and liquidit)

a. Capital

The quantitative and qualitative assessment of capital factor is performed by appraising the components, i.e.: Adequacy of Minimum Capital Supplier Liability (KPMM) to the prevailing provisions; Composition of capital; Future trend of KPMM:

Productive assets classified as compared to bank capital; The ability of banks to maintain the need for additional capital derived from profits (retained earnings); Bank capital plan to support business growth; Access to sources of capital; Financial performance of shareholders to increase bank capital.

b. Management

Evaluation on management factor, among others carried out through an assessment of these components includes: Calculating used Net Operational

Margin (NOM); General management; Implementation of risk management system; Bank compliance with prevailing regulations and commitments to Bank of Indonesia and/ or other parties.

c. Profitability Aspect (earnings)

Assessment of quantitative and qualitative approaches earnings factor among others is to do with an assessment of the components, such as: Return on Assets (ROA); Return on Equity (ROE); Net Interest Margin (NIM); Operating costs compared to operating income (BOPO); Development of operating profit; The portfolio composition of earning assets and income diversification; the implementation of accounting principles in revenue and expense recognition; and prospect of operating profit.

d. Aspects of liquidity

Assessment of quantitative and qualitative approaches to liquidity factors, among others, is done through the assessment of the components, including: Liquid assets less than one month compared with liquid assets less than one month; I-month maturity mismatch ratio; Loan to deposit ratio (LDR); Projected cash flow coming three months; Dependence on interbank funds and core depositors; Policy and liquidity management (asset and liabilities management or ALMA); The ability of banks to gain access to money markets, capital markets or other sources of funding; and Stability of third party funds (DPK).

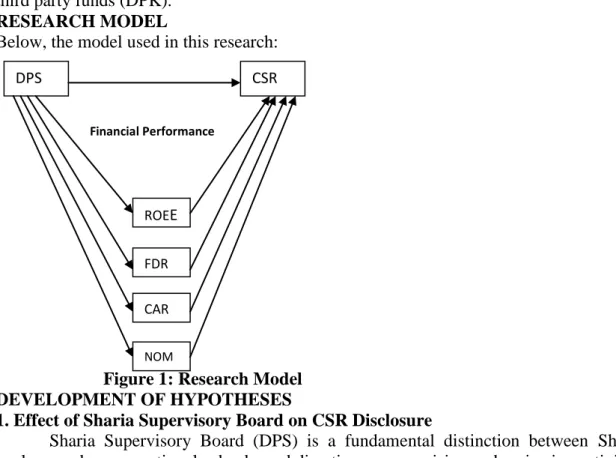

RESEARCH MODEL

Below, the model used in this research:

Figure 1: Research Model DEVELOPMENT OF HYPOTHESES

1. Effect of Sharia Supervisory Board on CSR Disclosure

Sharia Supervisory Board (DPS) is a fundamental distinction between Sharia banks and conventional banks and directing, supervising and reviewing activities of Sharia Bank for ensuring the activities of sharia banks in accordance with rules and principles Sharia expected by society.

Sharia Supervisory Board who served on several Sharia banks to increase disclosure of information because it can do a comparison on several reporting companies to determine which one best reporting is (Hannifa and Cooke, 2000), Abdullah et.al, (2011). If Sharia banks have a strong DPS disclose consider to follow up more CSR information in the annual report of The Sharia banks. (Grais and Pellegrini,

Financial Performance

DPS CSR

ROEE

FDR CAR

NOM MM M

2006; Haniffa and Cooke, 2005; Nathan and Pierce, 2009). Based on these descriptions can be formulated the following hypotheses:

H1: The Sharia Supervisory Board has positive effect on CSR Disclosure of Sharia Banks in Indonesia.

2. Effect of Sharia Supervisory Board on Financial Performance

The existence of the Sharia Supervisory Board helps companies to minimize arised agency problems due to the divergence of interests between the principal and the agent, so the financial performance of Sharia banks would be better.

DPS is formed to charge and responsible for monitoring and ensuring Sharia banks activities in accordance to Sharia principles and have implemented corporate governance in accordance to the applicable rules. The function of DPS monitor is to supervise the policies or decisions of Management in running and advising to the management. A large number of members with diverse expertise of DPS and make the supervision of cross positions against any decision of the management to be better so the performance management also becomes better, the impact will improve the financial performance of Sharia banks. The financial performance of Sharia banks consist of

several aspects, namely capital, asset

quality, Liquidity, Management, profitability (earnings). The approach used financial ratios among which, the Capital Adequacy Ratio (CAR), ROE, Net Operational Margin (NOM), and Financing Deposit Ratio (FDR). The previous research was

conducted by (Rajan &

Zingale, 1998; Brickly et al, 1994; . Williams, 2000; Drobetz et al, 2003; Byrd & Hickma n, 1992; Hossain et a l., 2000; Rosenstein & Wyatt, 1990; Gemmill & Thomas, 2004:Wei sbach, 1988) indicated that there was a positive relationship between the good practice corporate governance with the company performance (Musibah and Wan, 2014).

Based on the description of the hypothesis as follows:

H 2: Sharia Supervisory Board has positive effect on financial performance of sharia Bank

3. The Effect of Financial Performance on CSR Disclosure

Based on Sharia perspectives described by Hannifa (2002) in Othman et al. (2009), companies must be willing to give full disclosure regardless of the company makes a profit or not. However, Janggu (2004) in Othman et al. (2009) argued that firms with higher profitability will disclose information more widely than firms with low profitability. Like the obligation to deliver zakat in Islam, someone with more income is obliged to do zakat for social activities.

The companies with good financial performance will conduct a broader CSR. This is consistent with the stakeholder theory which stated the company is not the only entity that operates for its own sake, but to be able to provide benefits to its stakeholders, the more powerful stakeholders, the greater the company's efforts to adapt (Gray, Kouhy and Adams, 1994 in Chariri, 2008, p. 159). Furthermore, based on through Home Visits legitimacy focuses on the interaction between companies and communities (Ulman, 1982; in Ghozali and Chariri, 2007). As an agent of the owner of the funds, the company produced high profitability; it would reveal information more widely because the company wants to make the good image against the owner of the funds (Othman et al., 2009).

Based on these descriptions can be formulated the following hypotheses:

H 3: Financial Performance has positive effect on CSR disclosure

4. Financial performance mediates the relationship in the effect of the Sharia Supervisory Board on CSR Disclosure

Sharia Supervisory Board (DPS) as a form of the corporate governance implementation in sharia banks are able to effect management decisions and it will also be an impact on the bank's financial performance. Based on resource dependency theory, the SSB will affect performance finance and corporate social responsibility. This matter shows that practice of the corporate governance represented by DPS will show the financial performance higher and also the corporate

social responsibility. The previous

research conductedby (Rajan & Zingale, 1998; Brickly et al,1994; . Williams, 2000;Drob etz et al, 2003; Byrd & Hickman, 1992; Hossain et al., 2000; Rosenstein & Wyatt, 1990;

Gemmill & Thomas, 2004; Weisbach, 1988) have shown a positive link between the good corporate governance and company performance (Musibah and Wan, 2014).

The presence of the Sharia Supervisory Board helps companies to minimize the aroused agency problems due to the divergence of interests between the principal to the agent, so that the financial performance of Sharia banks would be better with improving the financial performance of sharia banks.

The DPS was formed to charge and responsible for monitoring and evaluating the activities of sharia banks in accordance to principles and have implemented corporate governance in accordance to the applicable rules. The DPS function is to supervise the policies or decisions of Management in running and give advice to the management. A large number of members of DPS with diverse expertise and cross positions existed in Sharia banks, it will create an oversight of every management decision better. The management decisions of the DPS members shows better, so it will be able to improve the financial performance of sharia banks and will further effect corporate social responsibility.

Based on these descriptions can be formulated the following hypotheses:

H 4: The Financial Performance mediates the relationship in the effect of the Sharia Supervisory Board on CSR Disclosure

RESEARCH METHODS

The subjects of this study were all Sharia banks in Indonesia contained in Statistics Sharia Banking in the Financial Services Authority of RI in 2010-201 6. The samples in this study used purposive sampling technique. As for the use of purposive sampling method in this research is Sharia banking has the following criteria:

1. Types of unconventional sharia banking.

2. Sharia banking discloses the CSR activities in its annual report.

3. Sharia banking publishes the financial statements consistently and completely in an annual report (2010 – 2016)

TECHNIQUES OF DATA ANALYSIS

The data were analyzed by using Structural Equation Modeling (SEM) with AMOS version 16.

DISCUSSION AND FINDINGS

Based on the research model, the flowchart of research as follows:

Figure 2: Flowchart

Direct Effect

To find out whether the DPS effect on CSR disclosure, a direct test was conducted. The direct test result as follows:

Table 1. Direct Testing

Estimate S.E. C.R. P Label ROE <--- DPS 2,897 1,142 2,538 ,011

FDR <--- DPS -16,500 12,895 -1,280 ,201 CAR <--- DPS -,301 ,434 -,693 ,489 NOM <--- DPS 1,042 ,415 2,514 ,012 CSR <--- DPS ,029 ,014 2,087 ,037 CSR <--- ROE -,001 ,002 -,408 ,683 CSR <--- FDR ,000 ,000 2,801 ,005 CSR <--- CAR -,008 ,004 -1,915 ,056 CSR <--- NOM -,010 ,005 -2,215 ,027

Source: Analysis Data, 2017

The Effect of DPS on CSR

Based on Table 1 above shows the DPS has a positive effect and significant impact on CSR. This is indicated by p-value of 0.037, which is smaller than 0.05. The first hypothesis, (the Sharia Supervisory Board Disclosure has positive effect to CSR of the Sharia Bank in Indonesia) is accepted. Thus, the direct effect of DPS on CSR disclosure show positive and significant impact on CSR

The effect of DPS on Financial Performance

The effect of DPS on Financial Performance consists of ROE, FDR, CAR and NOM.

The direct effect of DPS on ROE is indicated by p-value of 0.011, and less than 0.05. This means that the effect of DPS on financial performance derived from ROE has a positive and significant effect. Thus, the effect of the Sharia Supervisory Board positively to the financial performance of Bank Sharia in Indonesia from the ROE is accepted.

The direct effect of DPS on FDR is shown by p-value of 0.201, and greater than 0.05. This means that the effect of DPS on financial performance derived from FDR is not significant. Thus, the Sharia Supervisory Board positively to the financial performance of Bank sharia in Indonesia coming from FDR is rejected.

The direct effect of DPS on CAR is shown by p-value of 0.489, and greater than 0.05. This means that the effect of DPS on financial performance derived from CAR is not significant. Thus, the Sharia Supervisory Board positively to the financial performance of Bank sharia in Indonesia coming from CAR is rejected

The direct effect of DPS on the NOM is shown by the p-value of 0.012 second, and less than 0.05. This means that the effect of DPS on the financial performance derived from NOM positive effect and significant, thus, the Sharia Supervisory Board positively to the financial performance of Bank sharia in Indonesia coming from NOM is received.

The Effect of Financial Performance on the CSR disclosure

The direct effect of the financial performance consists of ROE, FDR, CAR and NOM on the CSR disclosure.

ROE direct effect on the disclosure of CSR was indicated by the p-value of 0.683 and greater than 0.05. This means that the effect ROE against disclosure CSR is not significant. Thus, the financial performance derived from influential ROE positively to CSR disclosure is rejected.

The direct effect of FDR on CSR is shown by the p-value of 0.005 and less than 0.05. This means that the effect of FDR on significant CSR disclosure. Thus, the financial performance came from FDR influential positive on the CSR disclosure is accepted.

The direct effect of CAR on the disclosure of CSR is indicated by the p-value of 0.056 and greater than 0.05. This means that the effect of CAR on CSR is not significant. Thus, the financial performance derived from influential CAR positively to CSR is rejected.

The NOM direct effect on the disclosure of CSR is indicated by p-value equal to 0.027 and less than 0.05. it means the effect of NOM on significant CSR disclosure. Thus, the financial performance derived from NOM influential is received positively towards CSR disclosure.

Indirect Effect

To find out whether the financial performance mediates the effect of DPS on the CSR disclosure then it is tested indirectly. The financial performance consists of ROE, FDR, CAR and NOM

The indirect testing of the variables

Table 2. Indirect Testing

Relation Estimation SE CR Conclusion

DPS →

KK →

CSR

-0,017 0,013 -1,308 Not significant

source: Data are processed, 2017

Based on the table 2, it shows the Critical Ratio (CR) of -1, meaning 308 less than 1.96. The magnitude of = 5%, which was significant relationship if Critical Ratio (CR)

> 1.96. Therefore, the test results showed that the financial performance consists of ROE, FDR, CAR and NOM does not mediate the DPS relationship with CSR, so that it can be concluded that DPS through financial performance does not have a significant indirect effect on CSR.

The following is a recapitulation of hypothesis testing to direct and indirect effect Table 3: Summary of the results of hypothesis testing to directly effect

p - value Description ROE <--

- DPS ,011 significant FDR <--

- DPS ,201 not significant CAR <--

- DPS ,489 not significant NO

M

<--

- DPS ,012 significant CSR <--

- DPS ,037 significant CSR <--

- ROE ,683 not significant CSR <--

- FDR ,005 significant CSR <--

- CAR ,056 not significant CSR <--

- NOM ,027 significant

Based on these tables, it shows that the DPS has positive and significant impact on the CSR disclosure, as for the financial performance did not prove to mediate the association DPS towards CSR.

CONCLUSION

1. S

haria Supervisory Board (DPS) has a positive effect on CSR disclosure of Sharia bank in Indonesia. This indicates that the main task of DPS to oversee the daily operational activities of Sharia banks is appropriate to Sharia principles.

2. T

he effect of the Sharia Supervisory Board (DPS) to the financial performance of Sharia banks in Indonesia consisted of ROE, FDR, CAR and NOM shows DPS does not affect the FDR and CAR, while DPS affected ROE and NOM positively. These results showed the Good Corporate Governance of sharia is implemented in the form of DPS in giving a positive response to the stakeholders.

3. T

he financial performance of Sharia bank in Indonesia consisted of ROE, FDR, CAR and NOM on the disclosure of CSR indicated ROE and CAR does not affect CSR, while FDR and NOM effect on CSR disclosure. These results suggest that the Sharia banks need recognition from the public or the legitimacy of the community and maximize their financial capabilities through the implementation of CSR activities.

4. T

he financial performance of the proxy formed ROE, FDR, CAR and NOM are not able to mediate the relationship between DPS with CSR closure of Sharia bank in Indonesia. Due to the CSR does not look good or poor financial performance of Sharia banks, so that the financial performance does not give effect to CSR.

Research Limitation

The proxy used in financial performance has not incorporate aspects of asset quality, so cannot determine the level of financing issues faced by banks.

Suggestion

1. F

or future studies, it can add quality assets as a proxy for the financial performance and other variables in order to better results.

2. G CG in Sharia banking in the form of the Sharia Supervisory Board in its oversight tightened further in order to attract the interest of stakeholders, especially the public and investors to consider the belief in using the services of Sharia banking.

REFERENCES

Agustina, Wahyuni, dkk. 2015. “Pengaruh Intellectual Capital, Corporate Social Responsibility Dan Good Corporate Governance Terhadap Kinerja Keuangan (Studi Kasus pada Perusahaan BUMN yang Terdaftar di BEI tahun 2011-2013)”, (Jurnal Akuntansi, Universitas Pendidikan Ganesha) Vol. 3 No. 1 Tahun 2015

Charles, Chariri. 2012. “Analisis Pengaruh Corporate Governance terhadap Pengungkapan Corporate Social Responsibility (Studi Kasus pada Bank Syariah di Asia)”. (Diponegoro Journal of Accounting) -Tahun 2012.

Ekayani, Fitria dan Anton Rahmadi. 2010. “Rangkuman Prinsip Syariah dalam Tata Kelola Perusahaan yang Baik”, Artikel Fakultas Ekonomi Universitas Mulawarman, Samarinda.

El Junusi, Rahman. 2012. “Implementasi Shariah Governance serta Implikasinya Terhadap Reputasi dan Kepercayaan Bank Syariah” (Jurnal Al-Tahrir, IAIN Walisongo Semarang) Vol. 12, No.1 Mei 2012: 87-111

Fauziah, Khusnul dan Prabowo Yudho J. 2013. “Analisis Pengungkapan Tanggung Jawab Sosial Perbankan Syariah di Indonesia Berdasarkan Sharia Social Reporting Indeks”, (Jurnal Dinamika Akuntansi)Vol. 5 No. 1- Maret 2013: 12-20.

Fitria, Soraya dan Dwi Hartanti. 2010. “ Islam dan Tanggung Jawab Sosial : Studi Perbandingan Pengungkapan Berdasarkan Global Reporting Initiative Indeks dan Sharia Social Reporting Indeks” (Jurnal SNA XIII).

Ghozali, Imam dan Hengky Latan. 2012. Partial Least Square Konsep, Teknik dan Aplikasi Menggunakan Program SmartPLS2.0 M3. Badan Penerbit UNDIP:

Semarang.

Hadiwijaya, Rendy Cahyo dan Abdul Rohman. 2013. “Pengaruh Intellectual Capital Terhadap Nilai Perusahaan Dengan Kinerja Keuangan Sebagai Variabel Mediasi,”

(Diponegoro Journal of Accounting) Vol. 2 No. 3 – Tahun 2009: 1 – 7.

Ibrahim, Zuraeda dkk. 2013. “Sharia Social Disclosure (ISCR) of Malaysian Public Listed Companies: Empirical Findings.” (British Journal of Economics, Finance and Management Sciences) Vol.7 9 No. 1 – Januari 2013).

Khoirudin, Amirul. 2013. “Corporate Governance dan Pengungkapan Sharia Social Reporting pada Perbankan Syariah di Indonesia.” (Acounting Analysis Journal UNNES) ISSN 2252-6765 Acoounting analysis Journal 2(2)(2013)

Lestari, Puji. 2013. “Determinants Of Sharia Social Reporting In Syariah Banks: Case of Indonesia.”(International Journal Business and Management Invention) Vol. 2 No. 10- Oktober 2013.

Maulida, Aldehita Purnasanti dkk. 2012. “Analisis Faktor-Faktor yang Mempengaruhi Pengungkapan Sharia Social Reporting (ISR)”, Artikel Fakultas Ekonomi, Universitas Negeri Semarang.

Musibah, Anwar Salem dan Wan Sulaiman Bin Wan Yusoff Alfattani. 2014. “The Mediating Effect of Financial Performance on the Relationship between Shariah Supervisory Board Effectiveness, Intellectual Capital and Corporate Social Responsibility, of Sharia Banks in Gulf Cooperation Council Countries” (Asian Social Sciences) Vol.10 No. 17 – Tahun 2013).

Othman, Rohana dan Azlan Md Thani. 2010. “Sharia Social Reporting Of Listed Companies In Malaysia,” (International Business & Economics Research Journal) Vol. 9 No. 4 – April 2010).

Peraturan Bank Indonesia No. 11/33/PBI/2009 tentang Pelaksanaan GCG bagi Bank Umum Syariah dan Unit Usaha Syariah

Rahman, Azhar Abdul dan Abdullah Awadh Bukair. 2013. “The Effect of the Shariah Supervision Board on Corporate Social Responsibility Disclosure by Sharia Bank of Gulf Co-Operation Council Countries”(Asian Journal of Business and Accounting) Vol. 6 No. 2- Tahun 2013 (ISSN 1985-4064).

Rustriani, Ni Wayan dan Agus Wahyudi S.G. 2012. “Modal Intelektual dan Kinerja Perusahaan: Strategi Menghadapi ASEAN ECONOMIC COMMUNITY”, (Jurnal Fakultas Ekonomi, Universitas Mahasarasawati), Denpasar.

Sofyani, Hafiez dkk. 2012. “Sharia Social Reporting Index sebagai Model Pengukuran Kinerja Sosial Perbankan Syariah (Studi Komparasi Indonesia dan Malaysia).”

(Jurnal Dinamika Akuntansi) Vol. 4 No. 1- Maret 2012: 36-46

Statistik Perbankan Syariah per Bulan September 2014 yang dipublikasikan oleh OJK RI diakses tanggal 22 Januari 2015 pukul 10.11 WIB

Sutedi, Adrian. 2009. Perbankan Syariah, Tinjauan dan Beberapa Segi Hukum. Ghalia Indonesia: Jakarta.

Ulum, Ihyaul. 2013. “iB-VAIC: Model Pengukuran Kinerja Intellectual Capital Perbankan Syariah di Indonesia”(Jurnal Inferensi) Vol. 7 No. 1, hlm 183-204.

ISSN:1978-7332

UU No. 21 tahun 2008 tentang perbankan syariah diakses tanggal 22 Januari 2015 pukul 09.21 WIB

Wardayanti, Siti Maria. 2011. “ Implikasi Shariah Governance Terhadap Reputasi dan Kepercayaan Bank Syariah” (Jurnal Walisongo, Universitas Jember) Vol. 19, No.

1 Mei 2011