The University of Manchester

Abstract

DECLARATION

COPYRIGHT

Papers Presented

Acknowledgements

List of Abbreviations

Introduction

- Introduction

- Statement of the problem

- Objectives of the research

- Research design

- Research strategy

- Significance of the study

- Structure of the thesis

It begins by explaining the research background, which briefly discusses performance management as one aspect of public sector reform. This chapter begins with the introduction, which is followed by the background of the research, which briefly describes public sector reform, performance management and the BSC concept. The implementation of the BSC as the PBS in the MoF is part of a reform strategy in the public sector to improve performance, service quality and public trust (three pillars of bureaucratic reform 2007).

Many ministries and government agencies are duplicating the Ministry of Finance's implementation of the BSC system in their own organizations. This is to verify that BSC practice within the organization has followed the principles of the strategy-oriented organization (SFO) as stated by its authors (Kaplan and Norton 2001c). Confirmatory factor analysis (CFA): to evaluate the implementation of the BSC based on the SFO principles;

With regard to the former, this study investigates how implementation of the BSC affects employees' professional behavior in terms of OC and PSM.

Context of the Study

- Introduction

- An overview of the Indonesian context

- Geographical context

- Population

- Economic context

- The implementation of the BSC in the Ministry of Finance

- Context of the study

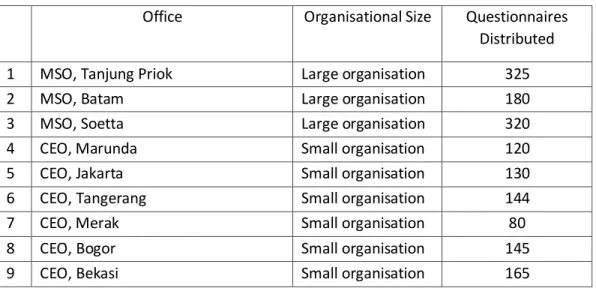

- MSO, Tanjung Priok

- MSO, Batam

- MSO, Soetta

- CEO, Marunda

- CEO, Jakarta

- CEO, Tangerang

- CEO, Bekasi

- CEO, Bogor

- CEO, Purwakarta

- CEO, Bandung

- Chapter summary

Thus, in 2011 Jakarta's CEO implemented BSC at all levels of the organization (to the individual level). In 2011, Merak's managing director thus implemented BSC at all levels in the organization (down to individual level). Thus, in 2011 Tangerang's CEO implemented BSC at all levels of the organization (to the individual level).

Thus, in 2011, Bekasi's CEO implemented BSC at all levels of the organization (down to the individual level). In 2011, the CEO of Bogor implemented BSC at all levels of the organization (down to the individual level). Thus, in 2011 Purwakarta's CEO implemented BSC at all levels of the organization (to individual level).

Thus, in 2011, the CEO of Bandung implemented the BSC within all levels of the organization (at the individual level).

Chapter 3: Exploring the Concept and Practices of the BSC: A Literature Review

- Introduction

- Public-sector reform

- BSC concept

- BSC practices

- The associated effects of using the BSC system

- Effects on organisational performance

- Effects on strategy clarity

- Managerial effects

- Effects on efficiency and effectiveness

- Research gaps

- Previous research settings

- Clarity of the BSC implementation level

- Lack of interest in the properties of the BSC

- The effect of organisational attributes on BSC implementation

- The influence of the BSC as a new management model on employees’

- Associated effect of BSC implementation on organisational performance Perkins et al. (2014) expressed surprise that, considering the large body of

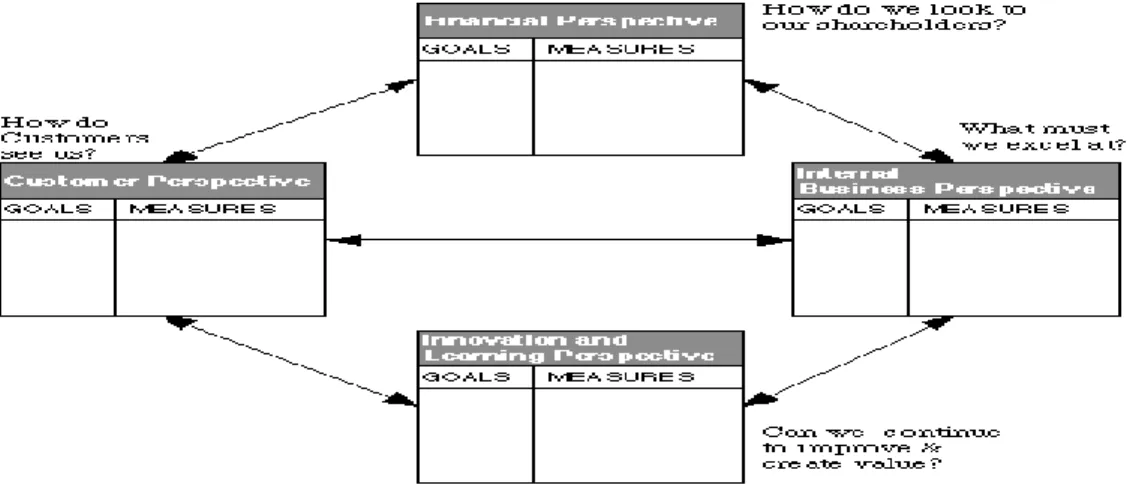

The BSC concept has evolved considerably since its first introduction (Braam and Nijssen 2004; Madsen and Stenheim 2015). Regarding the development process, Kaplan (2009) explained that the development of the BSC can be divided into three phases. Kaplan and Norton (1992) explained that the BSC places strategy and vision at the heart of an organization.

Crabtree and Debusk also found that firms generate higher surpluses after implementing BSC. It is evident that there have been ambiguous definitions of the BSC concept in the theoretical literature (Speckbacher 2003). Research on the benefits of using the BSC concept can substantiate the claims of Niven (2008).

However, undertaking such an exercise is dependent on a specific description of the BSC being implemented. In developed countries with advanced economies, many studies have been conducted on the application of the BSC in the public sector (see Appendix 2). This chapter therefore also discusses some fundamental critiques of the fundamental concepts and theoretical assumptions of the BSC.

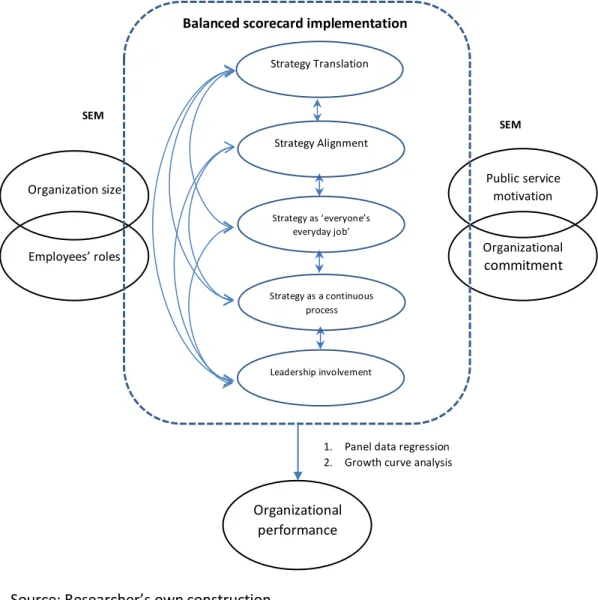

Research Framework

- Introduction

- Research objectives and research questions This study addresses four research objectives: This study addresses four research objectives

- Research gaps and hypothesis construction

- BSC implementation: using the principles of the SFO model

- Organisation size and employees’ roles

- Organisational commitment and public service motivation

- The relationship between public service motivation and organisational commitment

- Demographic correlation between OC and PSM

- Organisational performance and its relevance for the BSC

- Chapter summary

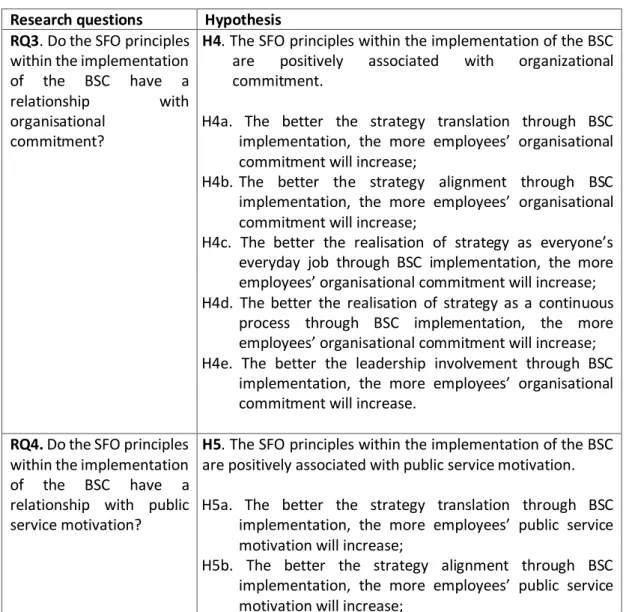

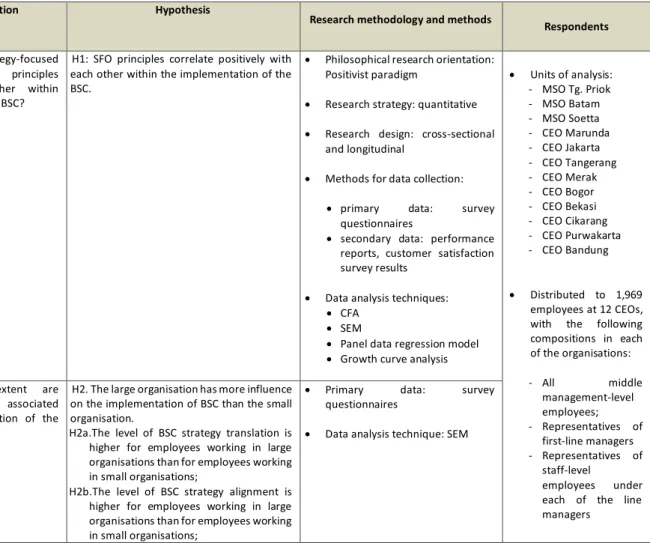

How do strategy-focused organizations (SFO) principles relate to each other within implementation of the BSC. Do the SFO principles within the implementation of the BSC relate to organizational commitment. Do the SFO principles within the implementation of the BSC relate to public service motivation.

In addition to organizational size, this study examines how employee roles affect BSC implementation. Therefore, the current research investigates the potential effects of management practices, in this case BSC implementation, on the level of PSM. They concluded that the three principles of SFO – strategy translation, strategy alignment and strategy process – have a significant impact on OP.

However, this research assumes that all five of the SFO principles represent BSC implementation in public sector organizations. With regard to the use of the BSC as a management system, the researcher is aware of only two studies (Hoque and James 2000 and Speckbacher 2003) that investigated the effect of organizational size on BSC implementation. The level of implementation of the BSC strategy as everyone's everyday work is higher among employees who occupy strategic roles than among other employees;.

The authors concluded that the implementation of BSC in the organization has a positive relationship with employee commitment. According to this finding, the researcher expects that the implementation of BSC will show a positive association with OK. One way to reduce the ambiguity of the actual contribution is to link the BSC to the strategies of the organization.

Using data from a survey of 66 manufacturing firms in Australia, Hoque and James (2000) found that greater use of the BSC was associated with improved OP. Second, this study investigates how organizational factors, particularly organizational size and employee roles, affect BSC implementation.

Research Methodology

- Introduction

- Philosophical research orientation

- Selection of the research strategy

- Research design of the study

- Reasons for cross-sectional research design

- Reasons for longitudinal design

- Justification of the selection of the units of analysis

- Sampling technique

- Sample size

- Research methods for data collection

- Questionnaire rating scale

- Questionnaire refinement

- Questionnaire distribution and collection

- Data analysis techniques

- Ethical considerations

- Pilot study

- Chapter summary

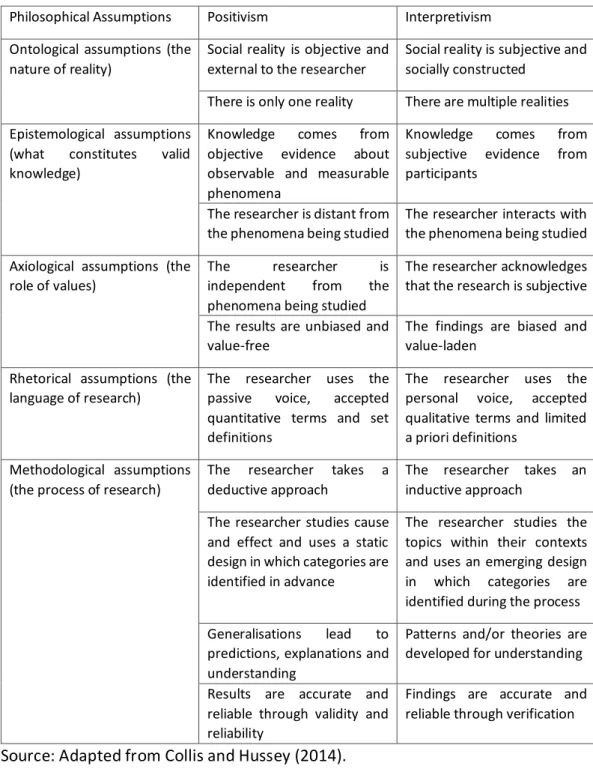

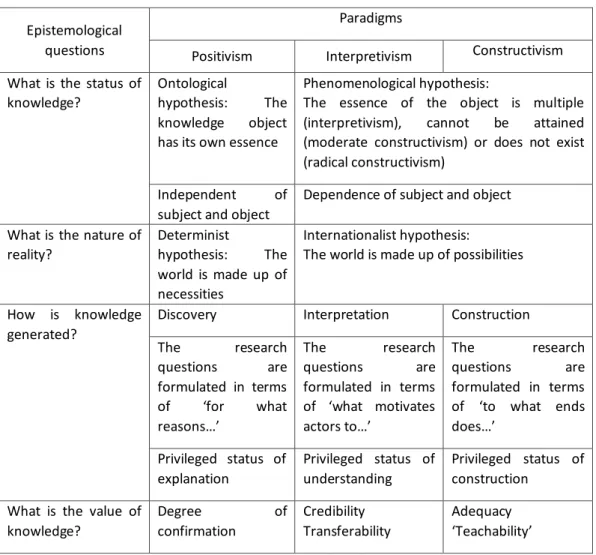

Second, epistemology questions the nature of the relationship between the investigator and the known (Guba, 1990). The essence of the object is multiple (interpretivism), cannot be reached (moderate constructivism) or does not exist (radical constructivism). According to Thietart et al. 2001), qualitative research methods allow for both the researcher's subjectivity and that of the subjects.

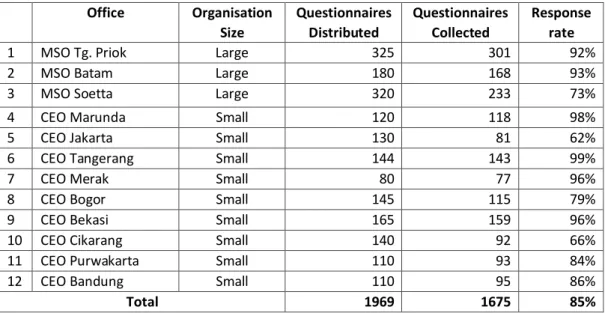

Another consideration was the inclusion of all major DGCE offices in the study. One of the research questions of the present study is: To what extent are organizational factors related to BSC implementation. The BSC implementation statements in the questionnaire were developed by the researcher based on the elements of each SFO principle (see Kaplan and Norton 2001) and the 2012 SFO survey by the Indonesian Ministry of Finance.

CFA was applied to the first research question, How do the principles of strategy-focused organizations (SFO) relate to each other within the implementation of the BSC?. The researcher used SEM to analyze data related to the second research question, To what extent are organizational factors associated with the implementation of BSC?. During the SEAG review process, the risks involved in the research and the research protocol were assessed and approved.

To obtain a representative picture, the researcher also took into account the variance of the respondents in terms of different employees. H2c. The level of the strategy that everyone's everyday work through in large organization is higher than that of small organization;. H2d.The level of the strategy as a continuous process by BSC in large organization is higher than that of small organization;.

H2e. The level of leadership involvement through a BSC in the large organization is higher than that of the small organization. The SFO principles within the implementation of the BSC are positively associated with organizational commitment.

Chapter 6: Findings on the Associations of Organisation Size and Employee Roles with the BSC

- Introduction

- Distribution, collection and response rate of the survey questionnaire The survey questionnaires were distributed by the researcher personally at each The survey questionnaires were distributed by the researcher personally at each

- Research questions, hypotheses and rationale construction

- Individual constructs

- Descriptive statistics

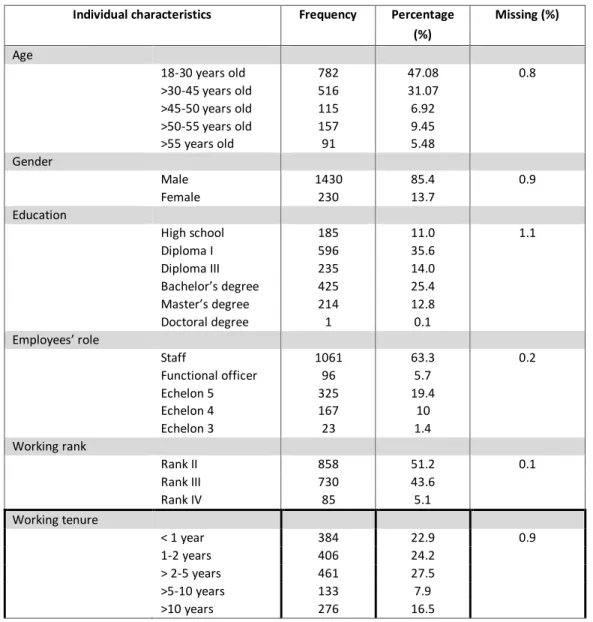

- Descriptive statistics of respondents’ characteristics

- Descriptive statistics of 7-point Likert scale responses

- Descriptive statistics of construct variables

- Data processing analysis techniques

- Analysis of sample size

- Analysis of outliers

- Data analysis

- Assessment of measurement model validity

- Assessment of model reliability

- Assessment of construct validity

- Assessment of convergent validity

- Assessment of nomological validity

- Hypothesis testing

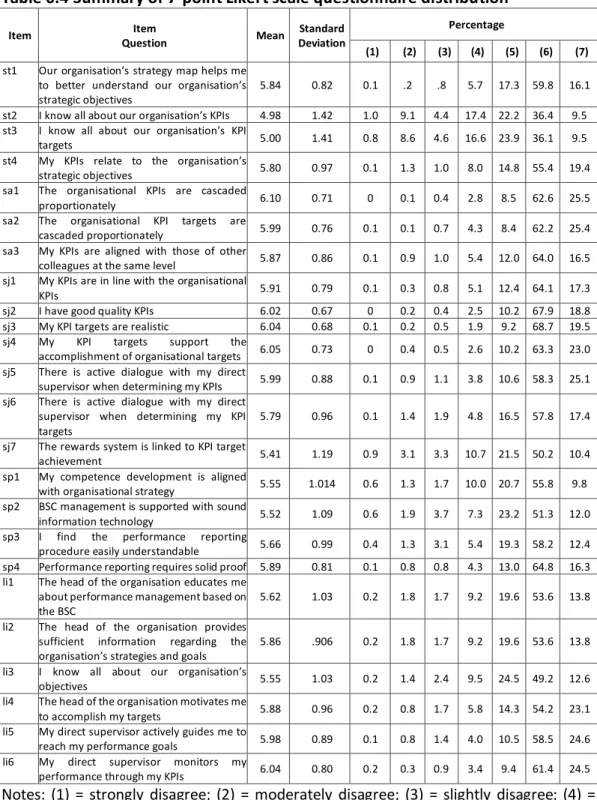

This chapter provides results on the application of the BSC as represented by the principles of SFO initially stated by Kaplan and Norton (2001c). The table shows that the average of the items in the survey varies from 4.98 (item st2, "I know everything about our organization's KPIs") to 6.10 (item sa1, "the organization's KPIs are relatively classified in a cascade "). Item li2 (The head of the organization provides enough information about the organization's strategies and goals) was ranked fourth, followed by item li1 (The head of the organization educates me about BSC-based performance management).

The variables of the first section accept the five SFO principles: strategy translation, strategy alignment, strategy as everyone's everyday work, strategy as an ongoing process and leadership involvement (Kaplan and Norton 2001c). This result therefore supports the nomological validity of the BSC implementation model used in this research. Moreover, this research is intended to investigate whether an organization's size has any influence on the implementation of the BSC.

Employees in strategic roles are those who work one level below the head of the organization. Regarding organizational size, it is reported that organizational size had a significant and negative association with all five latent variables of the BSC implementation. Hypothesis H1 predicted that SFO principles will positively correlate with each other within implementation of the BSC.

The results showed that employees with strategic roles had a significant relationship with four of the five latent variables representing BSC implementation. Large organization has more impact on BSC implementation than small organization. The level of strategy, the daily work of everyone through the BSC of employees who hold strategic roles is higher than the rest of the employees;.

The level of the strategy as a continuous process by BSC of employees who hold strategic roles is higher than the rest of employees;. The level of leadership involvement through a BSC of employees occupying strategic roles is higher than the rest of employees. This chapter provided the empirical evidence from this study of the associations of organizational size and strategic employee roles with the BSC model.

The first aim of this study was to examine how the SFO principles relate to each other within the implementation of the BSC.

Chapter 7: Findings on the Association of BSC with Organisational Commitment and Public Service Motivation

- Introduction

- Research questions, hypotheses and rationale construction

- Individual constructs

- Descriptive statistics of 7-point Likert scale responses

- Means and standard deviations of OC and PSM across offices

- Descriptive statistics of construct variables

- Data processing analysis technique

- Data analysis preparation

- Analysis of missing data

- Analysis of outliers

- Analysis of normality of data distribution

- Assessment of reliability

- Assessment of factor loading

- SEM analysis .1 Tested model

- Chapter summary

In this study, it is hypothesized that the implementation of BSC has a positive impact on OC and PSM. The principles of SFO in the context of BSC implementation are positively related to public service motivation. The second part provides data on the distribution of completed questionnaires with summary answers on a 7-point Likert scale of the observed variables OC and PSM.

The detailed distribution of OC and PSM scores, along with standard deviations, are given in Table 7.6. As can be seen, the contribution of employees' educational level differed between OC and PSM. For PSM, however, high school graduates, Diploma I, Diploma III and bachelor gave relatively similar figures (5.9); The highest level of PSM (6.06) was among employees with a master's degree.

This section provides information on OC and PSM means, standard deviations, and Pearson's correlation coefficients. As shown in Table 7.13, in the item 'My effort at work is greatly appreciated by this organisation'. The results showed that the univariate normality for both OC and PSM is significant at ρ < 0.01 for all 14 observed variables.

Before running the SEM program, reliability tests and factor loadings of the OC and PSM latent constructs were estimated. Therefore, based on the results of the fit index, the model of the links between the implementation of BSC and OC and PSM can be considered to be a good fit. The full results of the examination of the implementation of the BSC and its relation to OC and PSM are as described in Table 7.18.