No part of this document may be reproduced, stored in an automated retrieval system, or transmitted in any form or by any means, graphic, electronic, mechanical, photocopying, recording, scanning, or otherwise, without the prior permission of the author. Several people have offered their help during this research, which made the completion of this research a lot smoother. Therefore, I take this opportunity to convey my sincere gratitude to everyone who has helped me.

Next, I would like to acknowledge all the respondents who participated in the questionnaires that I distributed. I would like to dedicate this research project to my supervisor, Encik Khairul Anuar bin Rusli, who has been a great help to me throughout the research project's duration. Goh Hong Swee and Ms Tang Sook Heng, who provided me with both mental and physical support throughout the conduct of this research project.

I also want to dedicate this research to them for supporting me both with words of encouragement and acts of service, which gave me the strength to do my best in this research project.

INTRODUCTION

- Introduction

- Research Background

- Problem Statement

- Research Questions

- Research Objectives

- General Objective

- Specific Objectives

- Scope of Study

- Significant of Study

- Chapter Layout

- Summary

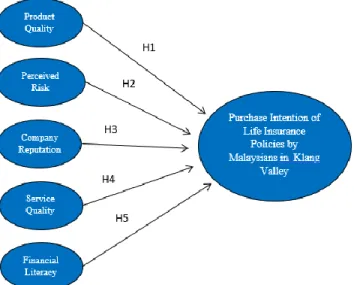

There is still a lack of awareness when it comes to the utility of life insurance. How perceived risk affects the purchase intention of Malaysians when it comes to life insurance products. The main purpose of this research is to investigate the factors that influence the purchase intention of life insurance products by Malaysians in Klang Valley.

To examine how product quality affects Malaysians' purchase intention towards life insurance products. To study how risk affects the purchase intention of Malaysians when it comes to life insurance products. To examine how service quality affects the purchase intention of life insurance products by Malaysians.

To study how financial literacy affects the purchase intention of life insurance products by Malaysians.

LITERATURE REVIEW

- Introduction

- Life Insurance

- Financial Capability

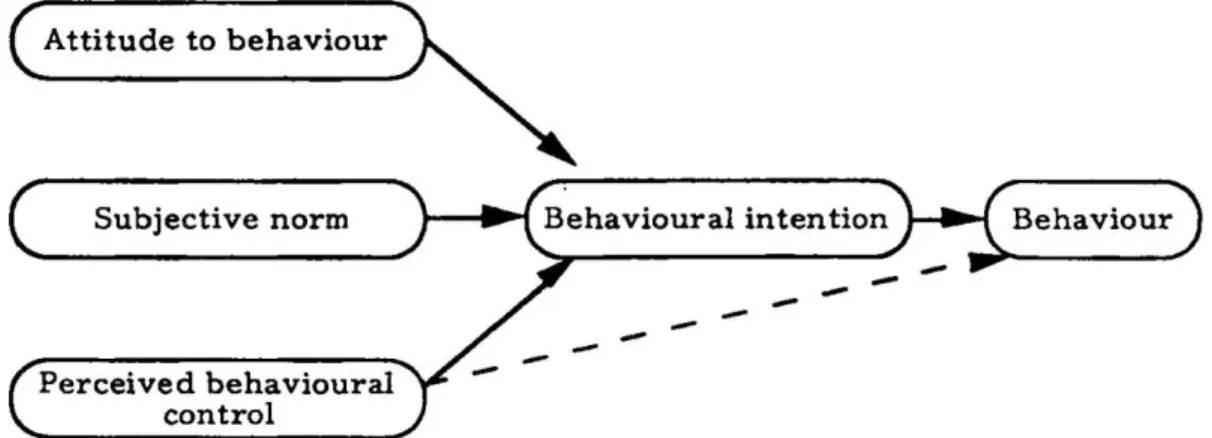

- Theory of Planned Behavior

- Population Density of Klang Valley

- Review of Variables

- Purchase Intention of Life Insurance Policies

- Product Quality

- Perceived Risk

- Company Reputation

- Service Quality

- Financial Literacy

- Hypothesis of Study

- Research Framework

- Summary

The final type of life insurance product is personal accident insurance, which provides a sum of money to the policyholder when they lose their ability to work due to an injury. This theory will be important to predict the future behavioral patterns of Malaysians in the Klang Valley regarding the intention to purchase life insurance policies. Household income, inflation, insurance price, culture, demographic variables and religion are the determinants that influence the consumer's purchase intention towards life insurance.

Life insurance products are considered intangible products because they provide a contract for financial compensation when the expected event occurs. According to Vijaya (2016), intangible products offered by life insurance companies consist of the preservation and accumulation of wealth in the form of investments. If the benefits associated with the product do not match the consumer's wants and needs, the consumer will move to other life insurance companies that can offer better value instead.

Life insurance companies will have a smoother process of acquiring loyal customers by minimizing their promotional cost when they are a reputable company. H1: Product quality has significant influence on Malaysians' purchase intention towards life insurance products. H2: Perceived risk has significant impact on the purchase intention of Malaysians when it comes to life insurance products.

H3: Company reputation has significant influence on the purchase intention of Malaysians regarding life insurance products. H4: Service quality has a significant impact on the purchase intention of life insurance products by Malaysians. According to Mahdzan & Victoria (2013), individuals who are more financially literate tend to be more involved in financial planning which includes getting life insurance to protect themselves financially.

The more financially literate an individual is, the more aware he will be of the financial risks he needs to protect against, which he can do with life insurance. H5: Financial literacy has a significant effect on purchase intentions of life insurance products by Malaysians.

RESEARCH METHODOGY

- Introduction

- Research Design

- Data Collection Method

- Primary Data Collection

- Secondary Data Collection

- Sampling Design

- Target Population

- Sampling Frame and Sampling Location

- Sampling Element

- Sampling Technique

- Sampling Size

- Questionnaire Design

- Pilot Test

- Construct Measurement

- Origin and Measure of the Construct

- Scale of Measurement

- Data Processing

- Proposed Data Analysis Tools

- Descriptive Analysis

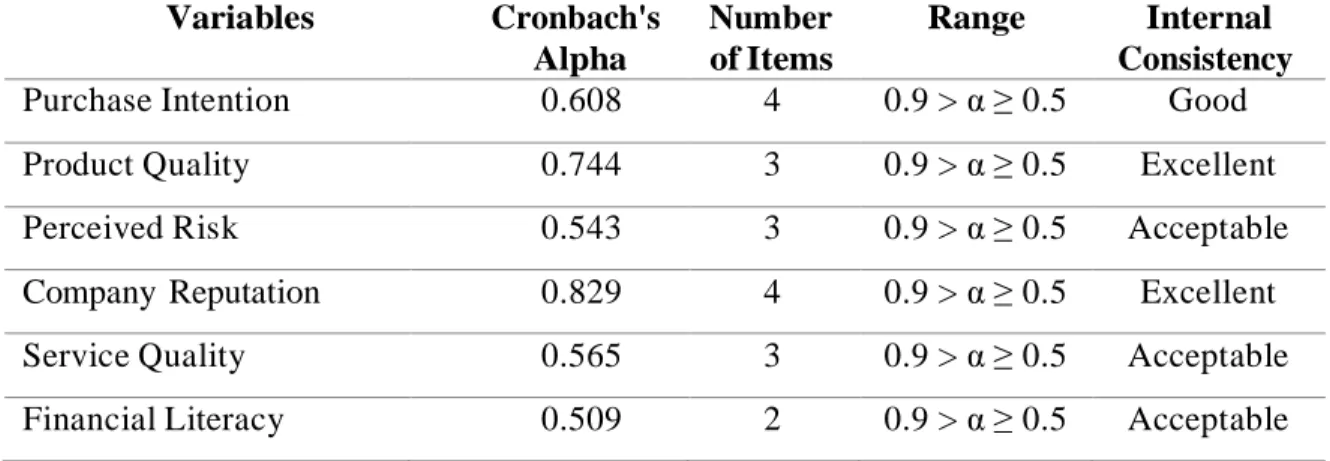

- Reliability Test

- Pearson Correlation Analysis

- Multiple Regression Analysis

- Conclusion

It should be sufficiently exclusive to produce adequate data for the research and to avoid misinterpretation of the study population. For example, the target population of this research would be Malaysians who live in the Klang Valley. In addition to the survey questions, there is a university privacy statement to ensure that respondents know that their privacy is respected and kept confidential.

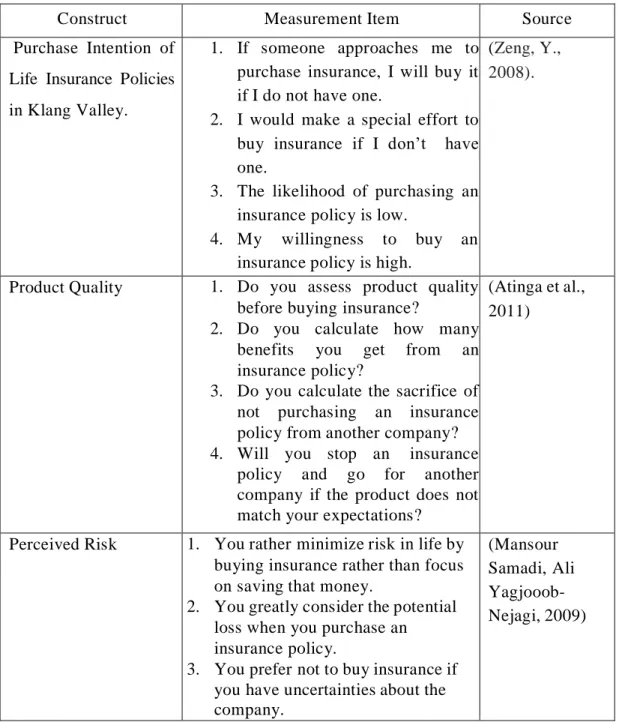

Finally, part C, a measure is constructed that is intended to collect respondents' opinions about the dependent and independent variables of this study. The structure of the questions asked in Part C is based on the 5-point Likert scale. The aim of the pilot test is to test the validity of the questions structured for the respondents.

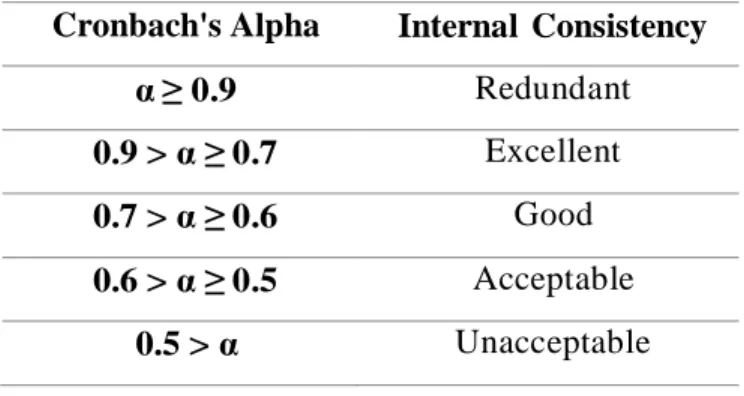

Statistical Package for Social Sciences (SPSS) version 26 was used by the researcher to analyze and interpret the reliability of the questions asked. You would defer your decision to buy life insurance without going through the life insurance agent. The nominal scale can be found in Part A of the online questionnaire as it collects information such as gender, age, marital status, employment status and monthly household income levels.

In this research, all the questions in Section C of the online questionnaire follow the 5-point Likert scale where it measures each variable from 1-5, 1-Strongly agree, 2-Disagree, 3-Neutral, 4-Slightly agree , 5- Totally agree. Finally, the statistical software is used to ensure that the analysis and interpretation of the results produced is done efficiently and accurately. The data collected will first undergo descriptive analysis followed by the reliability test to determine the validity of the information collected and ending with inferential analysis to investigate the hypothesis proposed in this research.

Sections A and B of the distributed questionnaire accept frequency and central tendency in the data interpretation. Applicability to various types of data and issues, ease of understanding, robustness to violations of the underlying assumptions, and broad availability all add to its appeal.

DATA ANALYSIS

- Introduction

- Descriptive Analysis

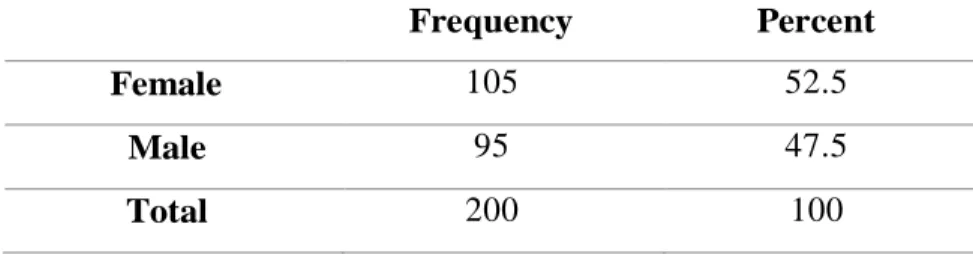

- Respondent Demographic Profile and General Information

- Central Tendencies Measurement of Construct

- Reliability Analysis

- Pearson Correlation Analysis

- Multiple Regression Analysis

- Hypothesis Testing

- Conclusion

The results developed highlight that product quality has the greatest influence on the purchase intention of life insurance policies by Malaysians in Klang Valley, while perceived risks have the lowest impact. This means there is a significant relationship between product quality and purchase intention of life insurance policies. This means there is a significant relationship between perceived risk and purchase intention of life insurance policies.

This means that there is no significant relationship between the company's reputation and purchase intention of life insurance. This means that there is a significant correlation between service quality and purchase intention of life insurance. This means that there is no significant relationship between financial knowledge and purchase intention with life insurance.

Surprisingly, the company's reputation and financial knowledge were not significant in influencing the purchase intention of life insurance. Another notable implication from this research is the untapped potential of the life insurance industry in Malaysia. As cited in the opening chapters of this study, the penetration rate of life insurance policies in Malaysia has only reached 55%, which is below the government's target of 75%.

As mentioned in the implication of the study, future research can narrow the target audience to the untapped potential of the life insurance industry. Retrieved April 29, 2022, from https://www.businesstoday.com.my malaysias-life-insurance-industry-sees-growth-with-rm12-8-billion-in-premiums-bought-for-. Investigating the factors of consumer purchase intention towards Life insurance in Bangladesh: An application of the theory of reason.

I'd rather minimize the risk in life by buying life insurance than focus on saving that money. I will not switch to another life insurance company if the current company has good service quality. I would switch to another life insurance company if your current one has poor service.

I would hesitate in my decision to buy life insurance without the intervention of the life insurance agent.

DISCUSSION AND CONCLUSION

Introduction

In addition, the researcher outlines the implications and limitations of the research, after which a recommendation for further research is made.

Implication of the Study

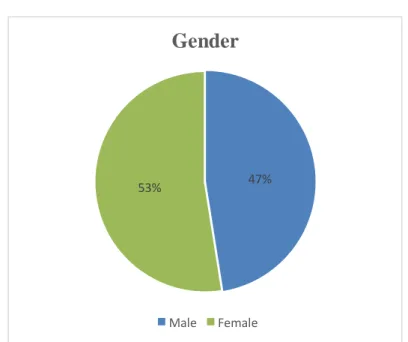

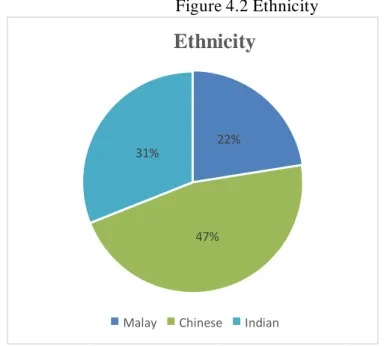

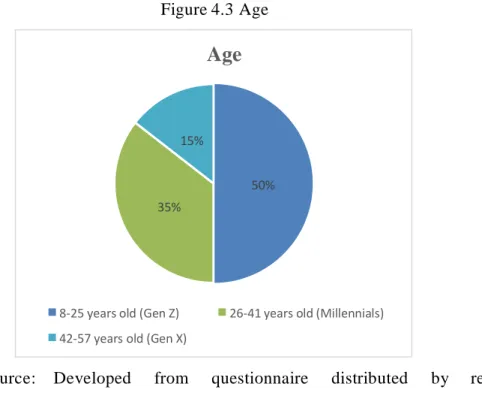

Due to the limited journal articles around the topic of this study, especially in the Malaysian context, it was quite challenging to structure higher reliable questions which will affect the quality of findings among the studied variables, especially the company's reputation and financial knowledge. The majority of respondents who participated in this study were Chinese, single, bachelor degree holders, below M40 (Household monthly income below RM10,000) and below the Generation Z age group. The data collected may not be sufficient to fairly draw conclusions about the respondents of the other demographic factor.

Perhaps further research can be done to understand where this huge market share is located, which will be valuable information for life insurance companies and the government to ensure that Malaysians across the country are protected financially regardless of race, age, gender, education level and income level. One of the reasons why the penetration rate of the life insurance industry is still very low in Malaysia may be due to the lack of awareness of the seriousness of not having enough life insurance cover. In short, the researched managed to achieve most of the research goals set at the start of the research project and found out how to further improve the quality of research in this specific niche.

Retrieved 29 April 2022 from https://www.fenetwork.my/wp-content/uploads/2020/11/RinggitPlus-Financial-Literacy- Survey-Full-Report.pdf. Retrieved 29 April 2022 from https://www.hasil.gov.my/en/individual/individual-life-cycle/how-to-declare-income/tax-reliefs/. Retrieved 29 April 2022 from https://www.freemalaysiatoday.com/category/leisure/money types-of-insurance- for-different-stages-in-life/.

I would cancel my current life insurance policy and switch to another company if the product does not meet my expectations. I buy life insurance from reputable companies because I can anticipate the future of my policies. I am a risk averse individual and you manage your risk by purchasing life insurance to protect yourself.

Limitation of the Study

Recommendation for Future Research

Once prospective researchers have narrowed the scope down to a very niche target population, the ideal would be to get an equal number of respondents around the different demographics to ensure that the data collected is as accurate as possible.

Conclusions