The completion of this research would not have been successful without the support and assistance of many individuals. We really appreciate his valuable guidance, advice and motivation when we faced difficulties during this research project. Due to his cooperation, understanding and enthusiasm towards this research project, he had led to the completion of this research project.

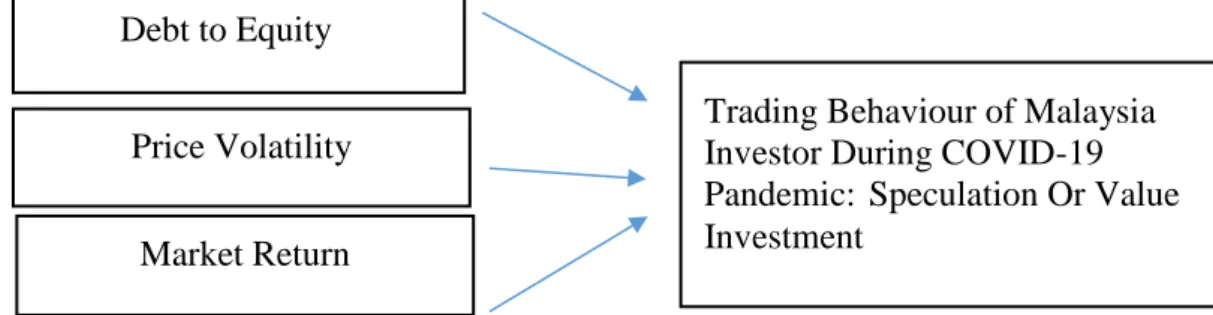

This research can determine the return of the portfolios based on debt to equity, price volatility and market return and how these variables affect the conversion of Malaysian investor trading behavior. This research is to study the performance of portfolios based on debt to equity, price volatility and market return and to identify if there is a switch in investors. This research collected data from KLSE top 100 market capitalization companies during January 1, 2020 to June 30, 2020.

INTRODUCTION

- Research Background ......................................................................... 1-4

- General objectives

- Specific Objectives

- Research Questions

- General of Questions

- Specific of Questions

- Significance of the Study .................................................................... 6-8

- Conclusion

To find out how the coronavirus disease pandemic is affecting the trading behavior of investors in the Malaysian stock market. How the coronavirus disease pandemic is affecting the trading behavior of investors in the Malaysian stock market. The independent variables could help the researcher better analyze the trading behavior of Malaysian investors during the coronavirus disease pandemic.

This chapter introduces the background history of the Malaysian stock market during the coronavirus disease pandemic.

LITERATURE REVIEW

Introduction

Review of Literature

- Review of speculation and value investing ...................... 11-12

The importance of the volatility index is becoming crucial in the financial market as it can be used to predict the future volatility of the underlying index. Realized return is the problem that has happened and it is crucial to measure the expected return and risk in the future and the financial performance of the company. In the study of Christiana, Setiana & Mamduch (2016), interest rates are the most important factor that will affect the market return of the stock market as it controls the purchasing power of investors.

If the company uses one-time debt to invest in a project, it can increase profits for their company shareholders in the future. The uncertainty during the coronavirus disease pandemic has affected the Malaysian investors in decision making for their investment activities and this is due to the higher volatility risk in the stock market. For example, the impact of Covid-19 on share price and the economy's debt-to-equity ratio is used to determine the firm's financial leverage factors in the study.

The weak form of the EMH states that the current price fully integrates information contained only in past price history (Clarke, Jandik, & Mandelker, 2001). When the stocks in the portfolio are highly correlated, the price movement of the stocks in the portfolio will move in the same direction. The EMH stated that no abnormal returns can be found in the market since everyone is given similar publicly available information and a similar level of risk.

Therefore, based on behavioral finance, it is assumed that investors are irrational in the stock market based on various cognitive biases. They are able to calculate market risk by comparing changes in the price of a stock to changes in the overall average price of all stocks.

Hypothesis

- Hypothesis of Market Return ........................................... 21-22

On the other hand, the returns were more positive during the placement of the MCO. The typical investor approach would be to sell the stock before the severity of the decline is apparent. Based on Saad, Edi and Haniff (2020), six restrictions have been imposed which shut down most sectors as Malaysia saw a significant increase in active cases.

With the announcement of various restrictions, especially tourists from other countries are not allowed to enter the country, and the closure of all government and private buildings, except for essential services, most of the participants in the stock exchange quickly respond to their trading progress, which has caused price volatility as they realize that the outbreak of the Covid-19 pandemic could have a major impact on market performance globally. Due to the outbreak of the Covid-19 pandemic, the uncertainties of the pandemic have brought a huge impact on the stock market, causing the Malaysian stock market to fall and fall since the implementation of the MCO. This suggested that the market index is a stable investment option for investors as their trading behavior may change with market returns.

Therefore, investors are most likely to change their investment decisions based on the debt ratio or the company's investment risks. For example, one of the studies that this research uses is conducted in Malaysia, China, and the United States (Lee, Jais, & Chan, 2020). Besides that, there are other factors that usually confound relationships between change in the explanatory variables and the responding variable.

For example, one of the journals reviewed by this research is related to one of the variables which is the price volatility that this research uses. However, some of the studies found by this research only provide the information up to April 2020.

METHODOLOGY

Introduction

Research Design

- Secondary Data ................................................................ 26-27

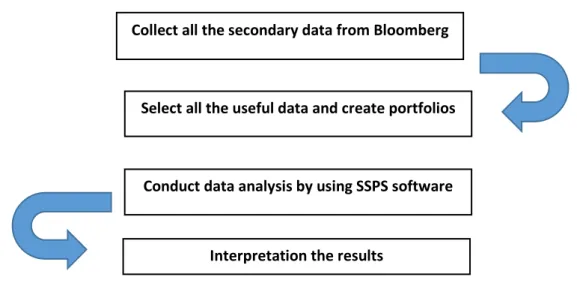

Then the data will be edited and applicable dates selected to create portfolios to conduct hypothesis tests using the SSPS software. Finally, the result will be compared and analyzed to draw conclusions about the research objective.

Data Analysis Tools

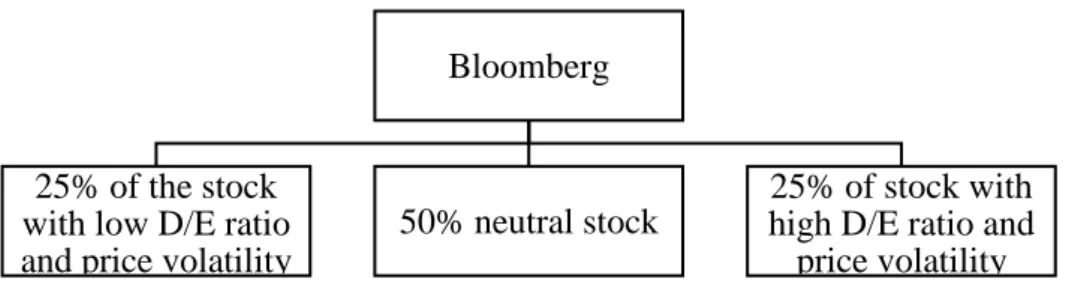

- Creation of Portfolios

- Calculation of Return

- Calculation of Price Volatility

- Calculation of Debt to Equity Ratio

- Descriptive Statistics

- Normality Test

- Shapiro-Wilk ..................................................... 32-33

The share price used to calculate the return is the closing share price of the day, meaning that the impact of dividends has been taken into account. Using the formula above, first calculate the stock return for each company over the period and the average stock return with SPSS for all companies. Then the calculated data will be used in this research for statistical testing purposes.

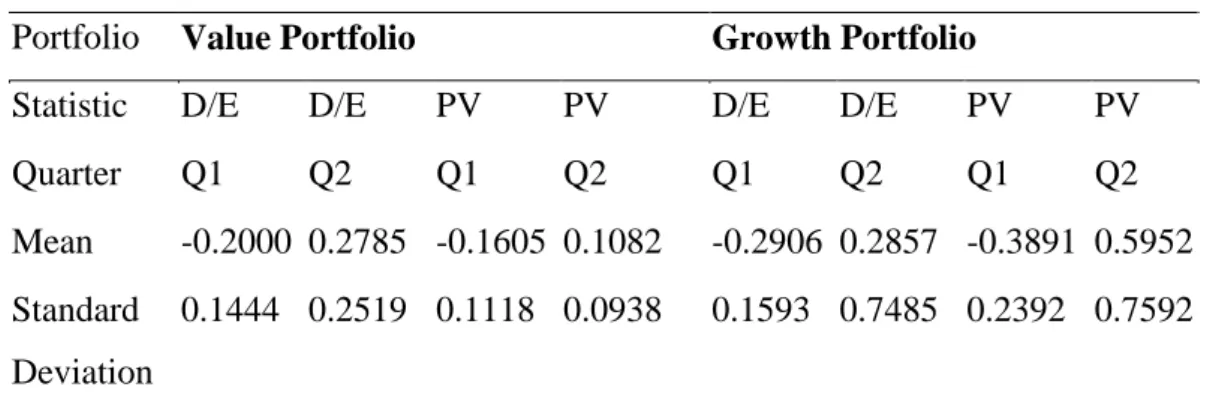

First, find the mean of a data set by adding up each value in the data set and dividing by the number of values. The debt-to-equity ratio (D/E) is used to estimate a company's leverage and by dividing the total liabilities by the company's total equity. In descriptive statistics, this research can determine the mean, standard deviation for each portfolio.

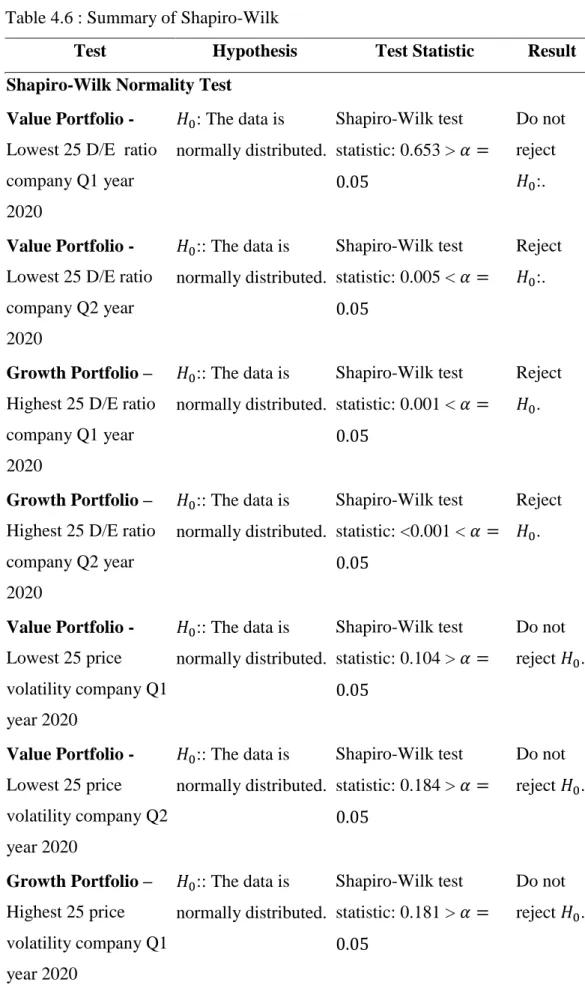

A graphical approach is the most basic and simple graphical approach, such as a histogram. When the Shapiro-Wilk probability value is less than the 0.05 level of significance, it indicates that there is significant evidence to reject the Ho (null hypothesis) and it is not normally distributed. However, the Shapiro-Wilk probability value is greater than the 0.05 level of significance, indicating that there is insufficient evidence to reject the Ho (null hypothesis).

Mann-Whitney-U is a test for comparing 2 independent samples if one of the dependent groups is ordinal. Reject 𝐻0 , if the probability value is less than the 5% significance level besides that, do not reject 𝐻0.

DATA ANALYSIS

Introduction

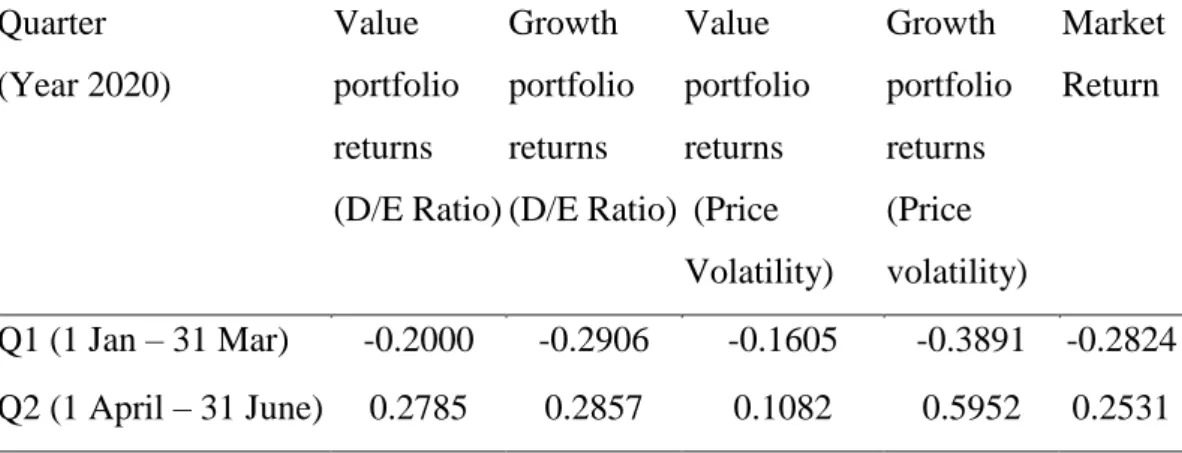

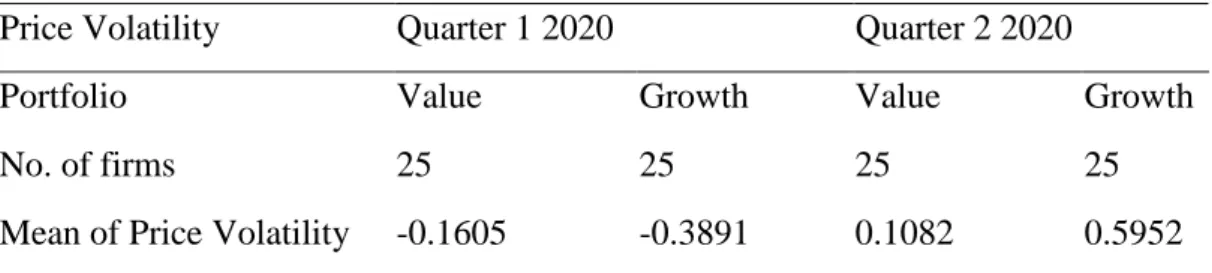

In the first and second quarters of 2020, value portfolios have lower average (mean) price volatility than growth portfolios. It is striking that the value portfolio of price volatility produces the highest returns during the first quarter. Meanwhile, for the price volatility portfolio, the value portfolio also appears to outperform the growth portfolio.

Also, both the debt/equity value portfolio and price volatility have outperformed the market index, with higher returns. Meanwhile, the growth portfolio for the price volatility portfolio is outperforming the value portfolio and the market index. There is a significant relationship between price volatility and the equity trading behavior of Malaysian investors during the Covid-19 pandemic.

The previous studies by Qammar and Abidin (2019), Pati, Rajib and Barai (2019), Ngu, Ziaei and Szulcyyk (2021) have also produced consistent results showing that price volatility has a significant impact on investors' trading. behaviour. The empirical findings showed that investors' portfolio investments would be constructed taking into account the price volatility of the stock. Thus, it is concluded that price volatility is affecting the trading behavior of Malaysian investors during the Covid-19 pandemic.

It has shown that the price volatility value portfolio achieved the best performance during the first quarter, while the price volatility growth portfolio recorded the worst performance during the first quarter. of price volatility recorded the lowest return.

Descriptive Statistic ........................................................................ 35-36

- Shapiro-Wilk Of Normality Test ..................................... 37-38

Conclusion

The hypothesis tests that this research uses are the Mann-Whitney-U Test and the Shapiro-Wilk of Normality Test. First, Shapiro-wilk proved that there are a few of the portfolios that are not normally distributed. Therefore, this research is suitable to use Mann-Whitney-U test to test whether there is a significant difference between each portfolio.

This is because the Mann-Whitney-U test is a parameter-free test that does not need to be distributed. Second, descriptive statistics and portfolio and market returns are used to compare each of the portfolio returns.

CONCLUSION

Summary of the Study

Implications of the Study

- Financial Institutions

- Market Investors ................................................................... 48-49

- Time Period Restriction

- Limited Sample Size

If the market favors a value portfolio, the market investors should be conservative and invest in the value portfolio without the risk of losing capital due to high-risk investments. If both portfolios underperform, investors may choose to invest only in the market index or allocate their capital to other investment options. Thus, the market trading behavior during a pandemic is important for the market investors to provide the investors with a reference or guidance for better investment decisions when there is a major event in the market in the future.

This research is focused on trading behavior of investors during Covid-19, which is in the period of pandemic. Based on 'Testing for Normality with SPSS Statistics' (n.d.), the Shapiro-Wilk test used is more suitable for small sample sizes which are 50 samples. This research contributed to literature as it investigated investor trading behavior in Malaysia's stock market during strong crises such as Covid-19 pandemic, and there are few propositions that can be put forward in this research topic.

Second, it is suggested that more independent variables (parameters) such as P/E ratio and P/B ratio should be included in the research. Therefore, by including more variables in the research, it enables a more concrete and comprehensive result. Third, only a small sample was selected in the research, which could affect the accuracy and cause bias in the result.

The impact of the Covid-19 pandemic on stock market volatility: evidence from Malaysia and Singapore. The impact of covid-19 on the financial performance of companies with PN17 and GN3 status: does it add salt to the wound?