Although many of the constraints to aquaculture development are technical, a large number are actually economic, cultural and institutional. This technical report, published jointly with the SEAFDEC Aquaculture Department, is the first of several to address the economics of various aspects of the milkfish (Chanos chanos) industry. The fry and fingerling industry of the milkfish (Chanos chanos Forskal) in the Philippines is alleged to suffer from certain imperfections.

The alleged lack of fry from the natural fishery provides the justification for various government programs in the Philippines, Taiwan and Indonesia, one of the most ambitious and far-reaching of which is the attempt to induce spawning of the milkfish under controlled conditions. However, policy planning necessarily continues despite insufficient knowledge of the structure and performance of the current brood collection and distribution system. The study on which this report is based was a follow-up to the Socio-Economic Study of the Aquaculture Industry in the Philippines, a joint project for Southeast Asia.

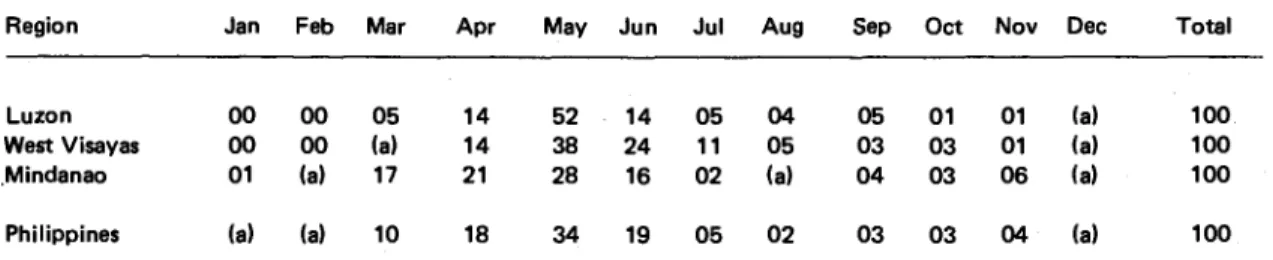

The peak season in the Philippines and Taiwan is from April to June, although barbecue is available year-round in certain regions of the Philippines, especially Southern Mindanao, where a second but less pronounced peak occurs from September to November.

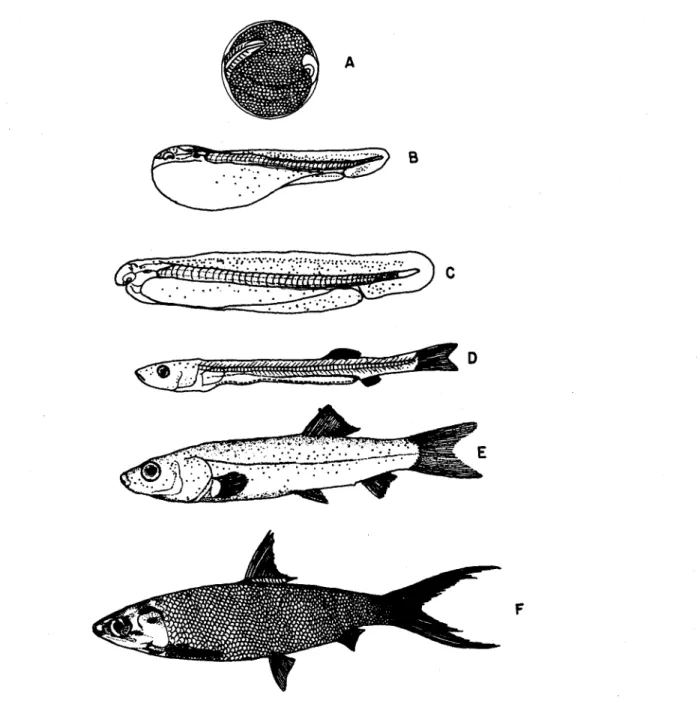

Milkf ish Distribution: Areas of Fry Capture in Coastal Waters: 9

The milkfish is the most important farmed species in brackish water ponds in the Philippines, Taiwan and Indonesia. Milkfish represented 18% of the total fresh and frozen fish consumed in the Philippines during Guerrero and . Darra 1975). This study is a first step in a comparative analysis of the milkfish and fingerling industry in the Philippines, Taiwan and Indonesia.

Added to this is 1) the sufficiency of the annual fry catch to meet the annual stock requirements;. This study indicates that only in certain areas of the country was the year atypical. The barbecue marketing system is a more restrictive term and refers to that sector of the barbecue industry which is responsible for the distribution of barbecue from barbecue grounds to fishponds.

There are certain economic characteristics of piglets that influence the structure, conduct and performance of the piglet industry. About 40% of pickers who are not employed by concessionaires have obtained equipment loans to start picking as soon as the fawn season begins. In fact, this comparative density technique was found to be practiced by only 26% of fry harvesters.

DAYS STORED

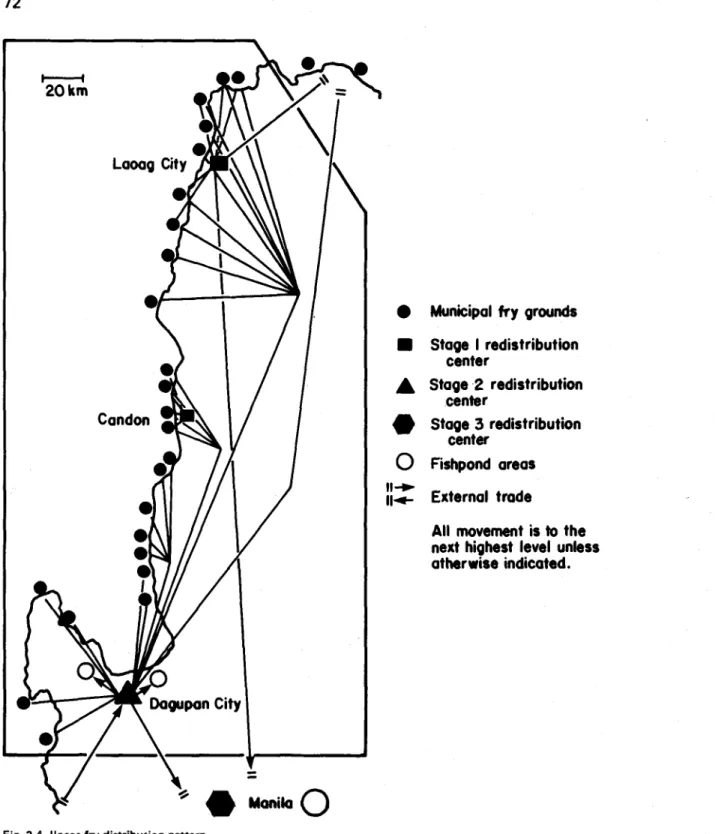

Center System Market Town

Level I Center Level 2 Center

Level 4 Center System Bulking Center

Boundary of major

The two-level and the hierarchical models are presented here as a framework for analyzing the spatial dimensions of the market structure of the fry industry. With significant intra- and inter-regional trade, it would be highly unlikely that the structure of the fry and fingerling industry is of the two-tier type. Some, such as the characteristics of the brood product, especially its seasonality and transience, have already been mentioned.

Finally, government regulations that either restrict or promote free competition will affect interrelationships between components of the industry. Indeed, the study found that the industry is essentially hierarchical, adjusted by the geography of the country. The - increase in the relative proportion of braai involved in interregional trade, benefiting from the directness and reduced costs (due to reduced mortality) of air routes, therefore tended to shorten the marketing chain.

Sections in the previous chapter have alluded to the presence of opportunistic behavior in the brood system. Another important sociological factor in determining the structure of the industry is somewhat related to the issue of opportunism and trust. The flow of capital through an industry is a measure of the interconnectedness of components of the system.

Some traders, especially in the Western Visayas and llocos regions, also doubled as fish brokers and as such, financed 12% of the rearing pond operators by agreeing to accept payment to fry after harvesting marketable milkfish. The extent to which FA0 115 and concession regulations are circumvented by smugglers will drive the structure of the industry in the opposite direction; so towards a redistributive network. The preceding discussion has revealed a complement of interrelated forces affecting the structure of the frying industry.

Vertical and horizontal integration, whether formally through partnerships or through unwritten cash advance and credit agreements, will guide the structure of the industry. Based on the identified determinants, the general trend of the frying industry is towards a shortened marketing chain.

0 Manila a

These second dealers can then sell to third-party dealers who in turn sell to hatchery operators in Manila. Breeder operators can then resell the fry to other smaller nursery operators or nursery operators. In the second phase of the redistribution centers, concessionaires and dealers sell fry to other dealers (2.1%), to nursery operators (1.3%) and to nursery operators (1.7%).

At phase 3, redistribution centres, concessionaires and traders sell 35% and 2% respectively to nursery pond operators. With minor exceptions of physical exchange using commissaries, fingerlings are marketed directly by nursery pond operators (producers) to rearing pond and fish farm operators (consumers) (Fig. 3.7). This was particularly true of traders and nursery pond operators who had the greatest exposure to alternative sources and outlets.

Much of this can be traced to the turnover of concessionaires who are major suppliers to both traders and nursery pond operators. The central role of nursery pond operators is evident in their efforts to ensure provision of fry and outlets for fingerlings. Consequently, no flow of fry is shown in Figure 3.6 directly from fry collectors to nursery pond operators.

Fish hatchery activity led to the development of paddling pool areas and thus increased competition among paddling pool operators for fry supply. The resulting marketing chain involves an average of 2.7 t i t l e exchanges from fry collectors to nursery or rearing pond operators. Add to that the fry required by paddling pool operators to supply catch to fishing grounds and the annual fry requirement will be approximately 2 billion.

Second, nursery pond operators were forced to temporarily stop buying fry in the same month because their nursery ponds were fully stocked. The direct and indirect evidence leads to the conclusion that the fry industry was able to supply sufficient fry to meet hatchery and nursery operators' rearing requirements in and through 1977.

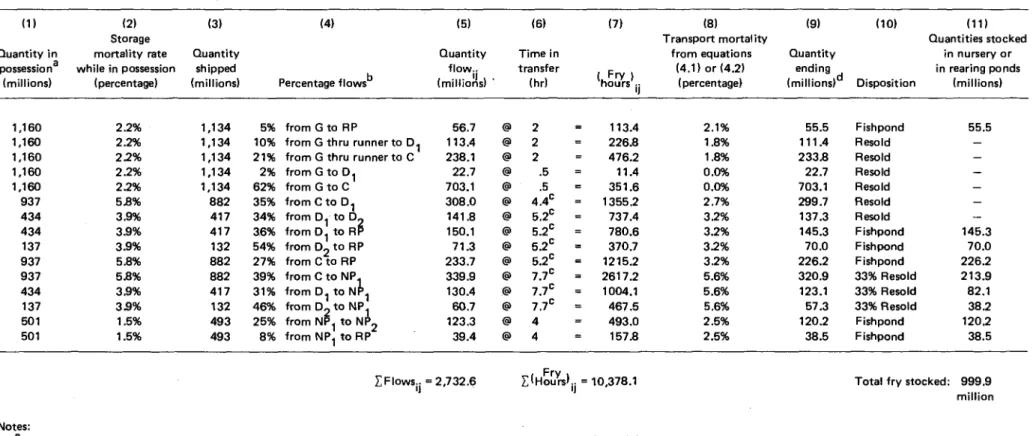

HOURS

2% of fry die during transport from breeding ponds to breeding ponds and fishers. Improvements in the technical efficiency of the industry therefore appear to be the duty of the pond operators who receive shipments of fingerlings. In summary, there is room for improvements in the technical efficiency of the piglet marketing system.

It is reasonable to conclude that the Philippines' fry distribution system exhibits a satisfactory level of efficiency in interregional trade. The fourth criterion by which the performance of the hatchery industry was evaluated was the adequacy of return on capital, labor, management and risk of market intermediaries. In addition to determining the net income for each of the market intermediaries, collection and marketing costs as a percentage of the average price per thousand fry paid by nursery and rearing pond operators also calculated.

These calculations indicate the disposition of the consumer peso and the marketing margin for fry. Total revenue minus total costs provided a net revenue for the collection team's labor and capital. One of the purposes of this presentation of concessionaire costs and returns is to address this issue.

The largest single cost, representing 54% of total non-barbecue costs, is the annual concession fee. The main operating cost apart from the purchase of barbecue was bad debt which represented 25% of the total. The total net return to all entrepreneurs in the fry industry, including collectors, is 828.6 per thousand, or 49.3% of the cost of fry to rearing and nursery pond operators.

Sometimes they also act as brokers, charging those they represent 5% of the fry's selling price. If the largest licensee whose sales were 59% of the total for trial licenses is not included, the remaining licenses received a net income of P178,030.

Further analysis of these costs and returns by nursery pond operators will be reported in the final section of this chapter when pricing efficiency for the fingerling and fingerling industries is examined. The largest five concessionaires in the sample handled just over 7% of the estimated 1976 fry catch of 1.16 billion. fry. The five largest retailers in the sample also handled just over 7% of the total fry trade.

In contrast, the five largest pond operators in the sample purchased 28% of the state catch of fingerlings and sold 64% of the total 1976 fingerling quantity. Correlation coefficients between prices in different trading regions therefore provide a measure of the flow of information between markets. Another explanation lies in the nature of the relationship between pond managers and clients.

First, it led to the establishment of appropriate delayed litter prices against which litter prices could be compared. In 1976, net returns to the industry increased with the degree of concentration in the various sub-sectors of the gilt and gilt industry. On individual lines, there were occasionally differences in prices that significantly exceeded the costs of transmission between markets.

Perceived imperfections in the milkfish and fingerling industry have provided the rationale for a series of government policies designed to improve the operation of the Philippine dairy industry. Due to the more competitive situation facing the product market, the concessionaire cannot pass it on to its buyers as easily. The government's decision regarding a national or regional approach to the fried resource will be decisive in this regard.

Alleged imperfections in the Philippine fry and fingerling industry fall into three main categories: 1) inadequate supply. Although there has been a slight downward trend in the net income of horticulture ponds since early 1976, this aspect of the hatchery and fingerling industry still provides a significant return to the private investor. Preliminary analysis of the performance of the milkfish (Chanos chanos Forskal) hatchery industry in the Philippines.

This index, based on correlation coefficients between prices in different markets, provides a measure of the flow of information between markets.