I am very thankful to my parents, both father and mother who pick me up every midnight during the time I was doing the thematic paper and I would also like to thank my brother who cherishes me and supports me every time my heart is overcome by fear is. The purpose of thematic paper is to value the share price of Oishi Group Public Company Limited based on discounted cash flow valuation method which represents the concept of comparing a company's value with that of its competitors or industry peers to determine the firm's financial value. Increasing health awareness, levying of sugar tax and rapid expansion of competitors among the industry has stagnated the growth of OISHI both food and beverage business.

Thus, the valuation value only provides guidance based on past performance of OISHI which investors should carefully take their own consideration to make further investment decisions.

HIGHLIGHT

Macroeconomic Analysis

- Healthy trend is shaping the future consumer demands

- Convenience store chain is driving change in consumers’ behavior

- Gross Domestic Product (GDP) in Thailand has impressively been increased

They also prefer to spend the same amount of spending in convenience stores as their spending in hyper and supermarkets. Although the grocery stores do not provide all range of goods, but it has become the most preferred channel for today's consumers. One of the most successful convenience store chains in Thailand is 7-Eleven, which has expanded across the region with more than 11,000 stores.

The value of Thailand's gross domestic product (GDP) was reported at US$455.22 billion in 2017, accounting for 0.73 percent of the world economy.

SWOT Analysis

- Strengths

- Weaknesses

- Opportunities

- Threats

Oishi operates in the food and beverage industry, where more than 50% of raw materials and products have a short life cycle. The trend of Japanese food and drinks has continuously expanded in all dimensions, which still have opportunities for expansion. People are more aware of their health, especially on food and beverage intake, as Japanese food and beverage are considered healthy for Thai consumers' perception.

Some of them are moving away from high sugar or fatty food and drink as they prefer to see cleaner and healthier food and drink.

INDUSTRY ANALYSIS

- Restaurant Industry

- Japanese restaurant trend in Thailand has increased by 8.3% from 2017 with the market value of 20 billion baht

- Restaurant’s atmosphere draws consumer’s attention

- Healthy food grows on Thai consumers

- Increasing number of Japanese restaurants is accordingly to the number of Japanese residents in Thailand

- Beverage Industry

- The ready-to-drink tea industry in Thailand has been declined during the past years both in term of volume and value

- Consumers tend to aware more on their health which significantly impacts Ready-to-drink tea market

- The new sugar tax impacts on performance of the beverage industry

- The price war in the Ready-to-drink tea market is still intensive

- Restaurant Business

- Oishi has been developing to be a strong restaurant brand and gained market shares among chained full-service restaurants in Thailand

- Oishi has created variety of Japanese restaurants in order to diversify its brands to cover all target groups of customers

- Direct competitors of Oishi restaurants are Hot Pot Restaurant and Hachiban Ramen

- Beverage Business

- Oishi is a leader of ready-to-drink green tea company in the industry both in term of share of the brand and the company

- Oishi focuses heavily on product innovation along with marketing strategy that captures both existing and new customers

- Direct Competitor of Oishi group is Ichitan Group

- Investment Summary

- Saturation of domestic green tea market due to increase in health awareness and aging population

- Increasing price of green tea beverage due to new sugar tax policy The new sugar tax policy will increase the tax expenses of the company which

- Enhance in substitute beverage products

- Slightly growth of Oishi restaurants

- Potential international expansion from strong distribution channels of parent company

The number of Japanese residents in Thailand has reached 60,000 people, which is also one of the factors driving the expansion of Japanese restaurants in the region. So this has a direct impact on the lower amount of profit which has led to poorer performance of the company. At the same time, Oishi Ramen also gained 1.3% of market share in the value of food service industry and ranked in the 14th position of the market.

However, the company's main revenue came from its ready-to-drink tea beverage, which accounted for 96% of its total revenue in 2017.

VALUATION

- Discounted Free Cash Flow to Firm (DCF)

- Overall Sales of Oishi

- Overall Sales for Food Business

- Sales of Domestic Restaurant Branches

- Sales of Oversea Restaurant Branches

- Number of Domestic Restaurant Branches

- Number of Overseas Restaurant Branches

- Overall Sales for Beverage Business

- Number of Bottles of Domestic Beverage Sales

- Price of Domestic Beverage Sales

- Oversea Beverage Sales

- Cost of Goods Sold

- Capital Expenditure

- Net Operating Working Capital

- Weighted Average Cost of Capital

- Terminal Value

- Risk of Terminal Value

- Rating Criteria

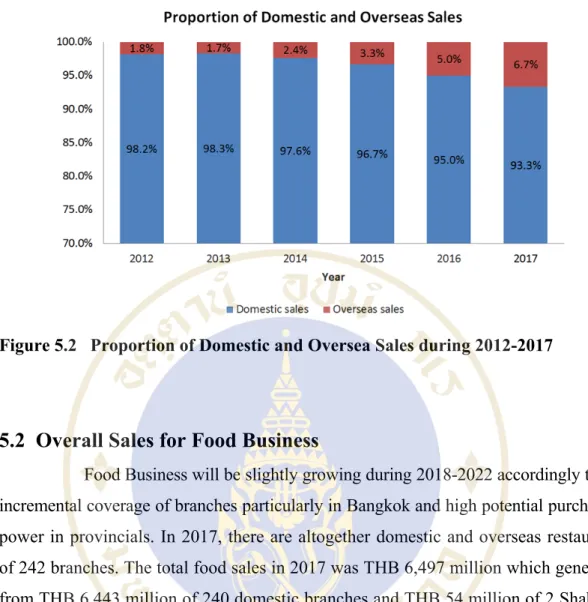

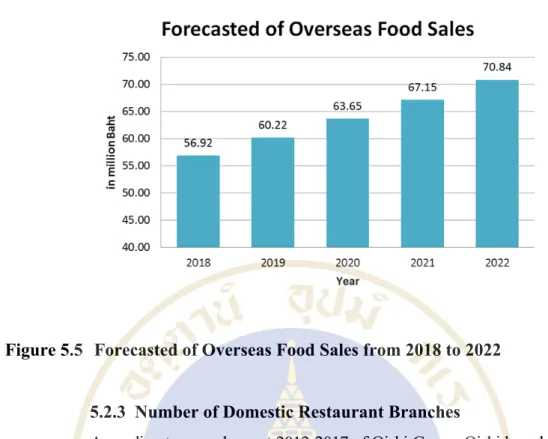

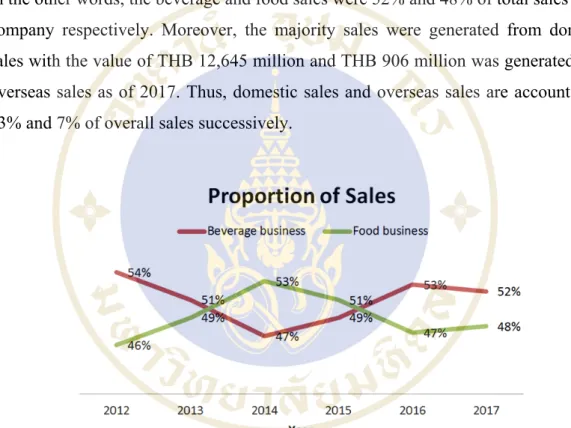

In other words, the sale of beverages and food accounted for 52% and 48% of the company's total sales, respectively. For the international market, there are only 2 Shabushi branches in Myanmar out of 242 branches of the total restaurant branches in 2017. The expected sales of overseas food businesses will be increased in line with the higher inflation in Myanmar, which ranges from.

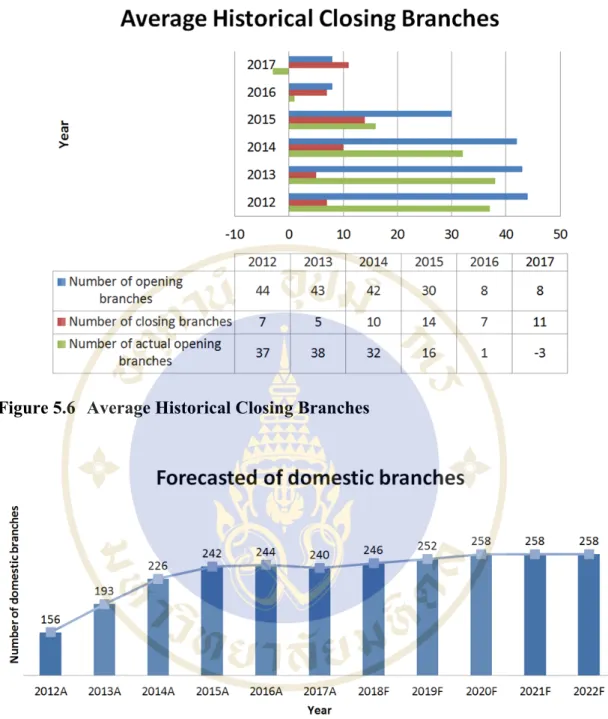

However, the number of restaurant branches will remain constant in 2021 and 2022 due to the historical trend of opening new branches. Therefore, the future trend of the number of sales bottles to be sold in Thailand in the next 5 years will also continue to decline according to the stagnation of the industry market. Therefore, the forecast sales of beverages in the international market from 2018 to 2022 will correspond to the historical compound annual growth rate of 26.16%.

As the company plans to expand 6 restaurant branches per year for the next 3 years from 2018 to 2020. Moreover, the company still does not have certain investment projects to expand its business due to the saturation of the current market. Regarding other receivables, we have estimated using the calculation from the historical average of other receivables to the total assets of the company during the years 2012-2017 of 1.05%.

We calculated the terminal value using the Dividend Discount Model, where the company's constant growth rate is expected to be 2.5% from 2020. We expected Oishi's constant growth rate to be equal to the expected inflation rate, as the company's long-term performance will vary depending on the increase in prices of both goods and services.

CONCLUSION

Summary of Discounted Free Cash Flow to Firm Valuation

Sensitivity Analysis

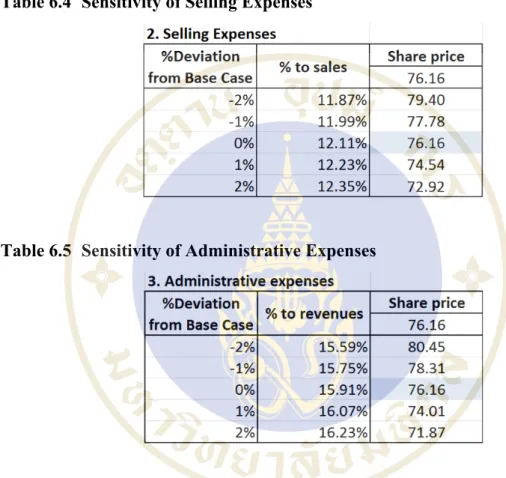

According to the sensitivity analysis in the table above, cost of goods sold varies greatly depending on the company's sales. It has an obvious impact on Oishi's price target, as if COGS declines by more than just 2%, the rating criteria would change from a sell recommendation to a hold recommendation. At the same time, the company's target price is also influenced by sales and administrative costs.

If both expenses decrease by just 1%, then the price target will change, leading to a hold rather than a sell recommendation. For other income, the company's target price has insignificant influence from other income. Since the other income also increases or decreases by 20%, the target price is still in the range of the sell recommendation.

For the sensitivity analysis of the closing restaurant branches of the company, if Oishi closes the branches less than 9 branches for each year, it will have an impact on the target price of the company which will lead to a hold recommendation rather than sell. If the negative trend outperforms by more than 10%, the recommendation will change from sell to hold due to the higher target price of the company. If Oishi decided to open one more branch in Myanmar, it will have an impact on the target price of the company leading to a recommendation to hold rather than sell.

The terminal value influences the target price, if the constant growth rate increases by more than 10%, then the recommendation will change from sell to hold. On the other hand, for WACC, it has a significant impact on the target price, since if WACC decreases by more than 10%, the recommendation rating will be maintained, and if WACC decreases by more than 20%, the rating will be buy instead of sell recommendation.

Scenario Analysis

- Scenario Analysis of Revenues Table 6.12 Scenario Summary of Revenue

- Scenario Analysis of Expenses Table 6.13 Scenario Summary of Expenses

For the WACC and Terminal growth rate, the growth rate is assumed to be a constant 2.5% over the period. In terms of cost scenario analysis, if cost of goods sold and selling and administrative expenses increase by more than 1% as shown in the table above as the worst case. Furthermore, if cost of goods sold and selling and administrative expenses decrease by more than 1%, the target price will be 88.42 THB.

Finally, if the total cost falls by more than 2%, the target share price will be THB 100.76. Therefore, it means that the target price and business operations of Oishi are highly influenced by the incremental expenses of the company.

Investment Risks and Downside Possibilities

- Change in Government Laws

- The Limitation and Fluctuation of Raw Materials

- Intensive Competition in the Industry

- Limitation of Distribution Channels and Logistics

- Natural Disasters Risks

Additionally, the company may experience a lower profit margin due to the differentiation of operations to meet the new policies. The company does not rely on just one supplier for the raw materials of its products. Moreover, the company also has low bargaining power with its suppliers, which leads to disadvantage in price negotiation.

In addition, the company's performance is also significantly affected by fluctuations in the cost of raw materials. Therefore, the company must secure its raw materials by executing contracts to avoid raw material shortages and maintain its production costs. The company must ensure that the selling prices in the market are reasonable and can compete with other competitors.

So the company has to manage negotiation well to take advantage and maintain relationship with the stores. In addition, the company may require higher expenses to place its products and locate restaurants in the good locations. In addition, the company also involves uncertainty risk of the restaurants in each specific area.

In terms of distribution channels, the company distributes both food and beverage products to international markets. The company will directly affect production processes if unexpected natural disasters occur. The company is continuously developing its green tea products under the brands "Oishi", "Chakulza", "Fruito" and "Kabusecha".

They must be aware of raw material shortages that will directly affect the sales activities of the company.

WACC and constant growth rate sensitivity analysis

We provided the analysis by comparing information from Oishi Group with its main competitor Ichitan Grou. When comparing the profit and loss statement between two companies, it is obvious that Oishi Group has double total sales more than Ichitan Group. In addition, Oishi has emphasized lowering the cost of goods sold to increase the company's profit margin.

Oishi's total assets as of 2017 are THB 9,706 million, consisting of THB 2,640 million of total current assets and THB 7,065 million of total non-current assets. For Ichitan Group, total assets are THB 8626 million, consisting of THB 1573 million of total current assets and THB 7053 million of non-current assets. In addition, Oishi has THB 4,116 million in total liabilities for 2017, while Ichitan has THB 2,570 million in total liabilities.

Furthermore, Oishi has shareholders' equity of THB 5,590 million while Ichitan has shareholders' equity of THB 6,056 million as of 2017. Ichitan has the largest paid-up shareholders' equity of THB 1,300 million with smaller retained earnings of only 1,077 million THB. In contrast, Oishi has unadjusted profits of THB 4,393 million and paid-up share capital of THB 375 million.

In contrast, Ichitan appears to be less efficient in OTO green tea business with higher cost of goods sold increasing every year. Furthermore, considering the net profit, Oishi has a higher net profit margin to sales of 10.65%, while the competitor has only 5.54% margin.