This thematic paper is a production of the study of valuation and application in the practical stock of The Erawan Group Public Company Limited (ERW) that I decided to apply the concept of discounted cash flow valuation (DCF valuation). EBITDA Earnings before interest, tax, depreciation and amortization ERW The Erawan Group Public Company Limited.

LIST OF ABBREVIATIONS (cont.)

VALUATION

Highlights

- BUY Recommendation, 2017 Expected the Growth as ERW Strategy

- With Fundamental, Operating Figures are Strong

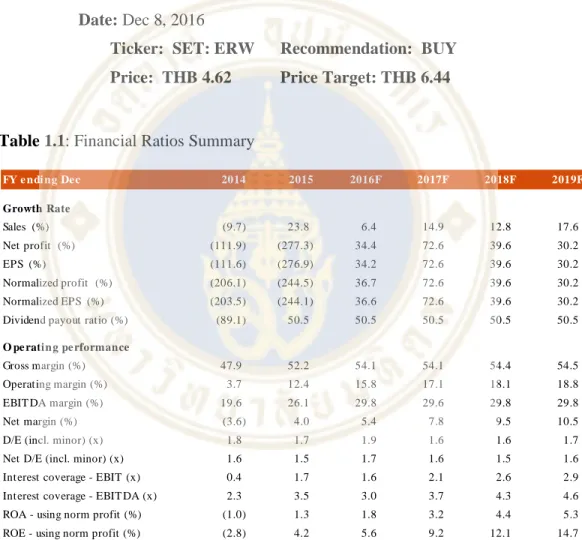

In 2017 hotel in pipeline like 7 HOP Inn hotels in Thailand and 1 HOP Inn hotel in Philippines, I predict the earnings growth in 2017 at 73%, in 2018 at 40%, and in 2019 at 30% The main drivers are the revenue expansion as its hotels continue to build, strong growth momentum from global travel trends and continued growth in international tourist arrivals to Thailand. The growth will be driven by: 1) Continued RevPAR growth in all segments, 2) Rising profit contribution from HOP Inn, 3) Upcountry hotels recovery, 4) Margin expansion and 5) Lower financing costs.

Business Description

- Hotels managed under Hotel Management Agreement

- Other businesses, Rental property

- The ERAWAN Group’s strategy

With the AccorHotels franchise agreement, ERW has the right to use the Mercure and ibis brands to operate the mid-range hotel and budget hotel. In 2015, ERW has 10 hotels under the ibis brand and 2 hotels under the Mercure brand, all of which are located in Thailand's top destinations.

Macro-Economic Analysis

- Global GDP growth at 3.4% while Thailand remains at 3.2%

- World Travel Trend Changing - The Millennial Travel

- New Economic Model - Thailand 4.0

- Global Travel and Tourism sector growth is better than the world GDP

While Thailand 1.0, 2.0 and 3.0 emphasized agricultural development, the improvement of low-income households reach average income and the growth of industrial industry, respectively, Thailand 4.0 emphasizes the creation of creativity and innovation through the application of technology and becomes Smart Thailand. Developing regions, especially in Asia, are leading the direct GDP growth of travel and tourism.

Industry Analysis: Thailand’s Tourism Industry Remains Strong in line with Global

- Thailand Hotel Performance has significant Growth compared to ASEAN market

- Number of International tourist arrivals Reaffirmed strong fundamental of Thailand’s Tourism Industry

World Travel & Council (WTTC) and its partner, Oxford Economics, forecast that global direct and tourism GDP growth will reach 3.1% in 2016, better than global GDP growth of 2.3 %. Travel and tourism is one of the largest industries in the world, supporting 284 million jobs and generating 9.8% of global GDP.

Competition Analysis: Smaller than Competitors but Higher Growth with Profitability

- Not No.1 in Thailand currently but keep watching on ERW While ERW purely plays in hotel investment and operating business, MINT

- ERW’s Operating figures are stronger than its peers

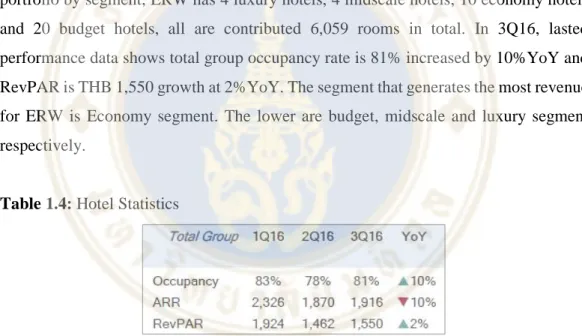

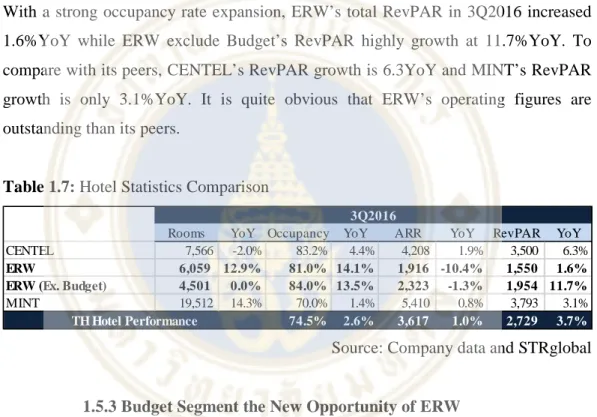

In addition to the rising contribution from the Budget segment (Hop Inn), the average room rate (ARR) of the total group decreased by 10.4% year-on-year. Thanks to strong occupancy expansion, ERW's total RevPAR increased 1.6% year-over-year in the third quarter of 2016, while ERW excludes Budget's RevPAR growth of 11.7% year-over-year.

Investment Summary

- A value stock with diversification and expansion growth

- Diversified Portfolio, Expected Higher EBITDA Margin

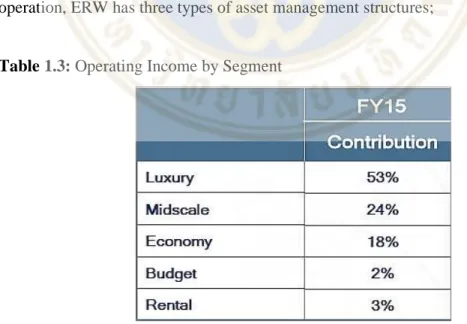

- HOP Inn Growth together with Millennial Travel and AEC HOP INN hotels are in Budget segment which the price per room is lower

- Government Disbursement in infrastructure always supports Tourism industry

In 2017, the government disbursement for investment projects is about THB 477.519 million, namely investment in 4 high-speed rails and Suvarnabhumi Airport phase 2. To track the relationship between government disbursement and tourism industry, our team used 10-year historical PROPCON price index and tourism price index. . The movement of Tourism price index is in line with the movement of PROPCON index.

Source: Thailand Stock of Exchange, Team's analysis Figure 1.11: 5-year historical ERW and events affected by the price.

Valuation: Multiple Valuation Model

- Valuation of ERW derives from Discounted Cash flow Model and Multiple Methods

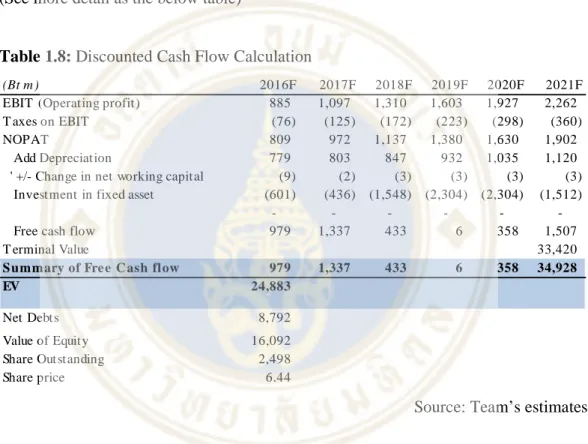

This model is suitable for ERW because the company depends on long-term debt with a stable financial structure. While FCFF is likely a mechanism to reflect the value of the company based on the time value of money, DCF valuation looks forward to future growth and the long-term perspective. The elements of the DCF valuation include: 1) 5-year cash flow projection, 2) Terminal value, 3) Capital expenditures and 4) Weighted average cost of capital (WACC).

The 5-year cash flow projection

Thanks to the organic growth, ERW has the potential to grow its business by expanding new hotels and penetrating the new market segment. The elements of the DCF valuation include: 1) 5-year cash flow projection, 2) Terminal value, 3) Capital expenditures and 4) Weighted average cost of capital (WACC). star hotel to budget hotel). Moreover, ERW believes that “HOP Inn” will be the flagship for the company to diversify the sales concentration on luxury hotels and the high competition in the hotel industry to make its performance positive thanks to the know-how of the hotel chain management.

Stability Growth of COGS and SG&A: COGS and SG&A are considered fixed costs for the hotel business, with ERW able to maintain both costs at 46% - 48% and 36% -37% of revenue, respectively. We are confident in ERW's business strategy and Thailand's tourism industry continues to grow thanks to its low cost of living.

Terminal value

Capital expenditure (CAPEX)

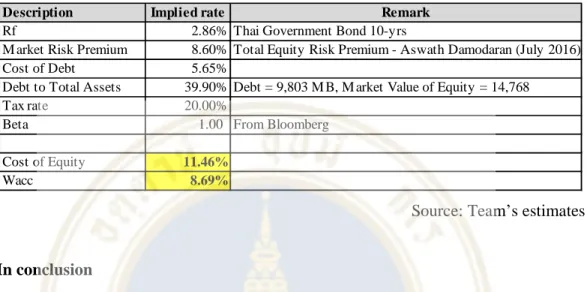

Weighted average cost of capital (WACC)

- Financial Analysis

- Turnaround from net loss in 2014 to net profit in 2015

- No concerns about mismatch funding even low liquidity with current ratio < 1.00x

- Cash flow from operations and bank loans used to finance in expanding the new hotels

- Trend Analysis: Income Statement

- Trend Analysis: Balance Sheet

- Return on Equity (ROE)

- Additional Upside Possibilities

- Investment Risks

- Macro-Economic risks

- Operation Risks

- Sensitivity Analysis

- Basis of the Corporate Governance Principle

- Corruption as defined by the anti-corruption policy

- Whistle blowing and controlling measurement

- Corporate Governance Policy

Based on ERW's business strategy, including sales growth, a high amount of capital expenditures and high volatility of net income, we believed that the FCFF valuation adequately reflected the true value of the company. In addition, the company's source of funds in 2015 mainly came from S/T and L/T debt financing of 67% and equity 33% accordingly. The development and management of human resources is one of the company's key priorities.

With a view to limiting the interest rate risk, the Company has previously converted part of the long-term loans from variable interest to fixed interest. Although COGS is still considered an important factor that can have a negative impact on the company's performance. 1.12.2.4.1 Disciplinary measures must be in accordance with the Employee Disciplinary Regulations issued by the Company and/or relevant laws.

1.12.2.4.2 If the Company is able to contact the whistleblower or the person submitting the grievance, it will notify the person in writing. To ensure that the Erawan Group Public Company Limited and its subsidiaries (the Company”) comply with the laws on anti-money laundering (AML) and international criteria on anti-money laundering and against the financing of terrorism (AML/CFT). In addition, the Board also allows the management to formulate a management policy based on the Company's goals and missions, which will be subject to the Board's approval.

DATA

Company’s Information

- History of the Erawan Group Public Company Limited

Furthermore, The Erawan Group PCL has built up new luxury shopping mall called "The Erawan Bangkok". 2007: The Erawan Group sells 100% shares of Amarin Plaza Shopping Center to Gaysorn Holdings and expands into the hospitality industry. The Erawan group also opened the luxury hotel in Phuket named "Six Senses Sanctuary Phuket".

2009: The Erawan Group opened Holiday Inn Pattaya and 2 ibis hotels in Bangkok Nana and Phuket Kata. 2010: The Erawan Group changed the brand name, ERAWAN to ERW and opened ibis Bangkok Riverside. In 2012, the Erawan Group also opened 2 ibis Hotels, Ibis Hua Hin and Ibis Bangkok Siam.

The Erawan Group had a new investment project, hotels in the Budget segment under the HOP Inn hotel brand.

Company’s Business Structure

Operation Structure

- Hotels managed by Erawan under the Franchise Agreement The Erawan Group has entered into franchise agreement with Accor to have

- Hotels managed by Erawan with own brand

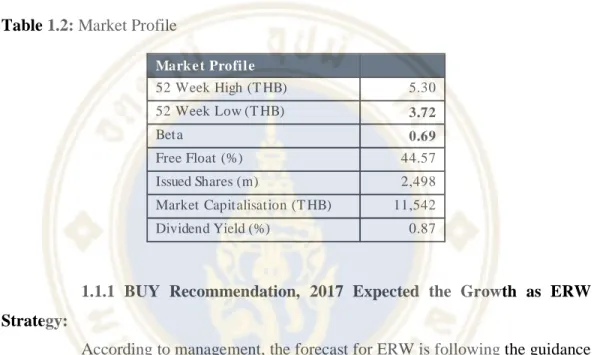

Major Shareholders and Free Float

Management and Organization Chart

Corporate Governance (CG)

In relation to corporate governance, The Erawan Group has set up the Nomination and Corporate Governance Committee (CGC) to regularly review and update corporate governance policies and practices so that the company will continue to have up-to-date criteria that can actually be implemented . To comply with the policy, the President was instructed to promote corporate governance among staff at all levels. The Erawan Group has signed the Collective Action Coalition (CAC), a movement founded by the Thai private sector against corruption and certifies that the company has declared against corruption by putting in place good business principles and anti-bribery controls. Full member of the CAC) and has completed a level 4 "certified" anti-corruption progress indicator.

The Erawan Group also ensures that staff understand the concept of Corporate Social Responsibility (CSR) where business is managed by properly considering the interests of all stakeholders, whether employees and family, customers, suppliers/creditors, competitors, public sector , society and environment. Results of the survey are used to improve business efficiency and to be one of the factors that evaluate our staff performance annually.

SWOT Analysis

- Internal Factors: Strengths .1 Hotel Location

- Internal Factors: Weaknesses

- External Factors: Opportunities

- External Factors: Threats .1 Economic slowdown

Currently, half of the hotels in the ERW portfolio are partnered with hotel contracts with world-class hotel operators, including Hyatt, Marriott, Accor, IHG and Starwood. Since the hotels are under a hotel contract, the quality of the hotel is one of the requirements. Due to the high capital requirement for any hotel investment, ERW has a lot of debt and interest costs.

In accordance with the standards of hotels under brand management and customer price sensitivity, when the room price is changed to be higher than the prices of other hotel rooms, customers simply book a room in other hotels instead. Given that the tourism industry has played an important role in Thailand, the Thai government has activities to support the industry, such as the domestic travel tax refund policy and additional long holiday notices. A major trade and business connection through 10 ASEAN countries, this is an opportunity for hotels that are suitable for both leisure and business travel, especially hotels located in key destinations in Thailand.

If the situation arises, it will directly affect Thai imports and indirectly affect the tourism sector.

Porter's five forces Analysis

- Bargaining Power of Buyers (Moderate) – Favourable to ERW Due to ERW and other big players in the market, namely CENTEL and

- Bargaining Power of Suppliers (High) – Most Favourable to ERW Suppliers of shortage raw materials, differential components, skilled labour,

- Threat of New Entrants (Low) – Most Favourable to ERW We rate the threat of new entrants as high. In addition to the hotel industry

- Threat of Substitute Products or Services (High) – Least favourable to ERW

- Rivalry among Existing Competitors (Moderate) – Favourable to ERW

In addition, ERW benefits from economies of scale as it is one of the leading hotel investment companies in Thailand. ERW also has bargaining power over suppliers such as contractors for new build hotel projects, farmers or traders for food ingredients in hotel restaurants and security companies for hotel security system. Apart from the hotel industry, We rate the threat of new entrants as high.

But as for the threat to the big ones, the new entrants will face the threat as economies of scale. Overall, from Porter's five forces analysis, we conclude that ERW is the competitive hotel investment and operating company in Thailand. There is bargaining power vis-à-vis suppliers and the business nature makes this quite difficult for newcomers.

In terms of bargaining power over customers and rivalry between existing competitors, ERWs are moderate and finally, the only weakness for ERWs is the threat of substitute products or services.

Income Statement

Although the rivalry between existing competitors in this industry is high, but the experiences and skills of ERW's management team are the key factors that keep ERW in competitive position. In terms of asset size, ERW is smaller than its competitors namely CENTEL and MINT. ERW has the competitive strategy as the expansion of its owned brand hotels which are in the budget segment, the segment with the highest EBITDA margin, while other players focus on others and investments abroad.

Balance Sheet

Cash Flow Statement

Financial Ratio

WACC Analysis

EV/EBITDA Peer Group Average