To test the hypothesis, I proposed an empirical measure to identify the abnormal returns of insider trading. I also conducted two additional tests to shed more light on the observed relationship between good corporate governance and abnormal returns on insider trading.

Research Objectives

The researcher examined the relationship between insider trading abnormal return and board size, board independence, board meeting frequency, institutional ownership and block stakes. If good corporate governance helps mitigate opportunistic insider trading, then characteristics of board composition and ownership structure that reflect good corporate governance are expected to be negatively related to abnormal insider trading returns.

Scope of Study

LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT

Thai Capital Market, Insider-Trading Law and Regulation

According to Section 241 of the EIA, insider trading in Thailand was categorized as a legal offence. Only required corporate executives to disclose the benefit they received from insider trading after the SEC disclosed such trading activities.

Insider Trading

- Argument for Deregulation Insider Trading

- Argument for Regulating Insider Trading

Some academics try to explain the harmfulness of insider trading in the ethical and moral perspectives. In the next section, I will elaborate on the main incentives of insider trading and illustrate hypothesis development.

Incentives for Insider Trading

- Information Asymmetry

- Agency Cost

And the concept of corporate governance was later accepted and developed widely in the academic field. In this case, a corporate governance index has been implemented in this research and the detailed information will be disclosed in the sub-section.

Corporate Governance Index

- Board Composition and Function

- Ownership Structure

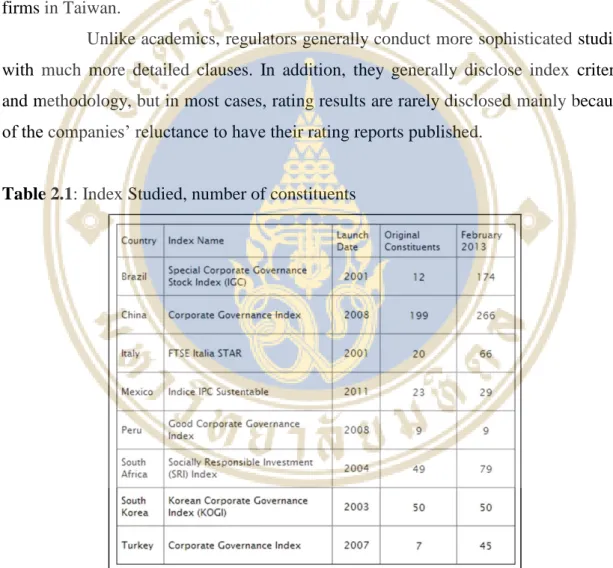

From previous research, I addressed the above suggestions that agency problem was significantly shaped by the good corporate governance mechanism (Shleifer and Vishny, 1997; Berglöf, and Claessens, 2006). The results imply that the corporate governance index is successful in evaluating the effectiveness of the governance mechanism of firms in Taiwan. In Thailand, the regulatory entity that conducts the corporate governance index is The Thai Institute of Directors Association (IOD).

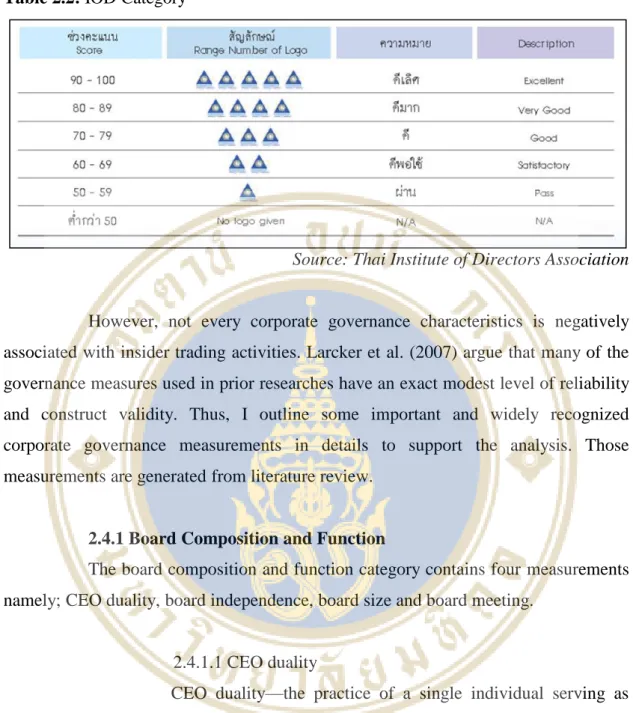

The assessment criteria are based on the principles of good corporate governance of the Organization for Economic Co-operation and Development (OECD Principles of Corporate Governance) and the Stock Exchange of Thailand. Companies are classified into six groups based on their corporate governance scores in the CGR publication. Each group achieves a different level of recognition, indicated by the National Corporate Governance Committee logo number, ranging from one to five and none for those with a score below 50.

Source: Thai Institute of Directors Association However, not all corporate governance characteristics are negatively associated with insider trading activities. 2007) argue that many of the management measures used in previous research have a precisely modest level of reliability and construct validity. Ferreira and Matos (2008) find that foreign institutional ownership is positively associated with firm value and performance outside the US, but there is no direct evidence that foreign investors are able to change corporate governance mechanisms and outcomes. In general, previous research on the relationship between good corporate governance and block shareholders' ownership has been somewhat mixed.

Hypothesis Development

- Hypothesis related to information asymmetry problem

- Hypothesis related to agency cost problem

- Hypothesis about Board Composition and Function

- Hypothesis about Ownership Structure

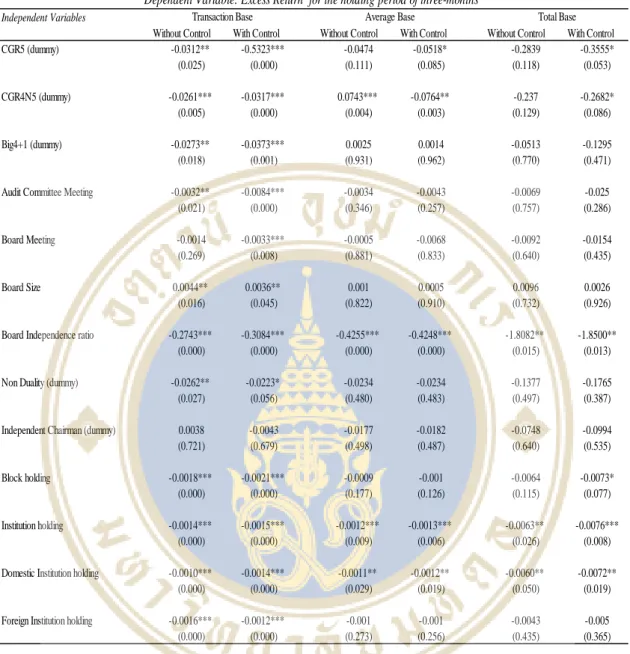

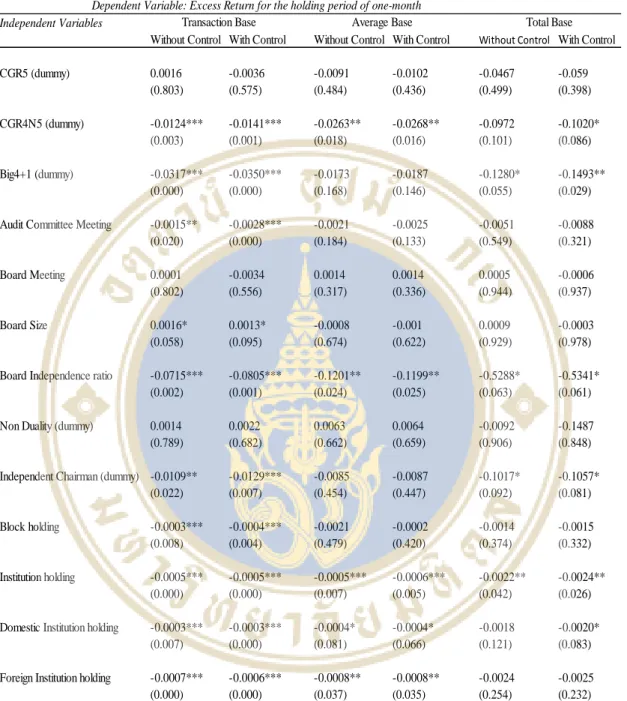

H1b: There is a negative relationship between abnormal return from insider trading and the frequency of audit committee meetings. However, my hypothesis may not be significant and may show no relationship between opportunistic insider trading and good corporate governance. This is important because even good corporate governance mechanisms are unlikely to prohibit insider trading based on information that has been disclosed.

Additionally, based on prior literature, some measures of government firms are not necessarily negatively related to insider trading abnormal returns. As the literature is based on different countries, it is reasonable to assume that there is a relationship between BoardSize and insider trading abnormal returns in Thailand. Consistent with the main research findings, I predict that the frequency of board meetings is negatively related to the abnormal return of insider trading.

H4a: There is a negative relationship between the sum of institutional ownership and insider trading abnormal returns. H4c: Foreign institutional investors play a better role in mitigating insider trading abnormal returns compared to domestic investors. However, consistent with majority results, I estimate Block as a proxy for good corporate governance and hypothesize that there is a negative relationship between blockholder ownership and opportunistic insider trading.

RESEARCH DESIGN AND DATA

Data

Since 2001, the Thai Association of Directors (IOD) in cooperation with the Stock Exchange of Thailand (SET) and the Office of the Securities and Exchange Commission (SEC, Thailand) has continuously evaluated the corporate governance practices of listed companies. The overall results of the survey are published in reports entitled "Thai Corporate Governance Report (CGR)" and disclosed to all listed companies and related parties in the capital market.

Sample Selection

The overall survey results are published in the reports entitled "Corporate Governance Report of Thai Listed Companies (CGR)" and disclosed to all listed companies and related parties in the capital market. trade value less than 10,000 Baht; 2) companies with limited historical transactions from SETSMART. The first restriction was intended to eliminate the insider trading likely to be due to random activities or personal liquidity purposes, the second restriction was intended to eliminate the possible error in determining the beta figures for each company. Considering the accuracy and consistency of the data, SETSMART beta can provide more stable results.

It is possible that some insiders profit from negative movements in share prices. However, it is also possible that some insiders sell shares for liquidity reasons or simply sell shares when they leave the organization. Therefore, it is difficult to tell the true relationship between the abnormal return on inside sales and the level of corporate governance of the company.

According to this question, purchases are more information oriented and will therefore be the main focus of the analysis. These restrictions limited the final observation to 4,567 insider purchase transactions among an annual average of 101 firms. To interpret the excess returns cautiously in light of the restriction on the actual purpose of the transactions, the excess return was calculated according to the following three categories: (i) the excess transaction return for each company, (ii) the total excess transaction returns during the year per insider for each company, and (iii) the average of the excess transaction returns during the year per insider for each firm.

Empirical Methodology

By analyzing the excess returns of insider traders using different windows, we can look at the efficiency of the Thai market. In addition, the control variable for the debt ratio (Debt in relation to total assets) is included. Independent chairman = The independent chairman is the best scenario, as the chairman of the board does not hold a senior position in the company.

Block = Block holding is the major shareholder that has at least 5% of the company's total shares. The variable is calculated as the percentage of the share held by the large investors. Institution = Institutional holding is the institutional investor who owns at least 1% of the company's total shares.

The variable is calculated as the percentage of the institutions' share ownership. DomesticIns = The domestic institutional holding company is the domestic institutional investor that owns at least 1% of the total shares of a company. ForeignIns = The foreign institutional holding company is the foreign institutional investor that owns at least 1% of the total shares of a company.

EMPIRICAL RESULTS

- Insider Trading and Corporate Governance Index

- Insider Trading and Auditor & Auditor Committee

- Insider Trading and Board Composition

- Insider Trading and Ownership Structure

- Supplementary Analysis

- Trader identity

- Trade size

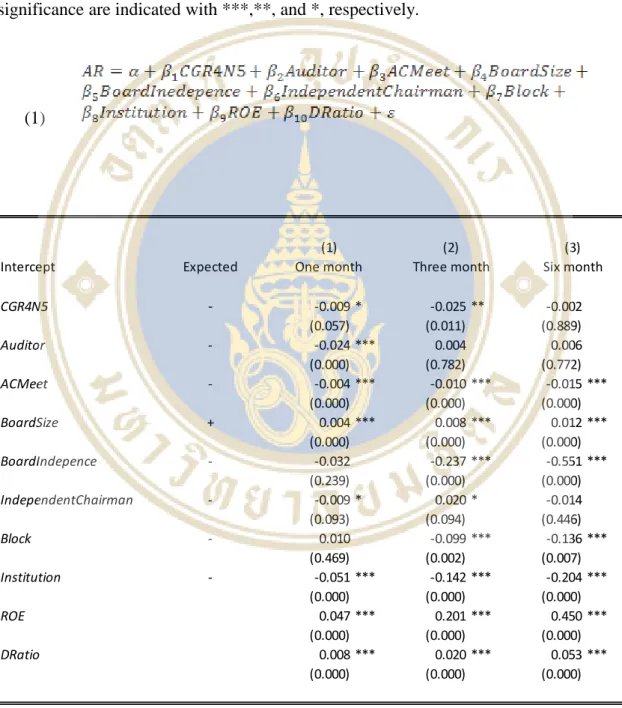

Auditor is also positively associated with insider trading abnormal returns at three-month and six-month intervals, although the relationship is insignificant. First, I find BoardSize (in terms of the number of directors present on the firm's board) is positively associated with insider trading abnormal returns. Second, I find that BoardIndependence (the ratio of independent directors to the total number of boards) is negatively associated with insider trading abnormal returns.

Moreover, the independent chairman is positively related to the abnormal return of insider trading in the three-month interval and the relationship is significant. The findings suggest that the Independent Chairman is not an effective mechanism in mitigating the abnormal return of insider trading. The results show that both DomesticIns and ForeignIns have a significant negative relationship with the abnormal return of insider trading at the 1 percent level.

I also examine the relationship between corporate governance characteristics and insider trading abnormal returns for small versus large transactions. Furthermore, BoardIndependence shows a strong negative relationship with insider trading abnormal returns at three-month and six-month intervals. In addition to these characteristics, other mechanisms of corporate governance show no consistent relationship with insider trading abnormal returns.

CONCLUSION

The more frequent the audit committee meetings, the smaller the board size, and the higher percentage of block and institutional shareholders are associated with fewer abnormal returns from insider trading. On the one hand, the analysis in this paper contributes to insider trading studies. Although the debate regarding the merits of such trading is still far from settled, the continued efforts of policymakers and capital market regulators to mitigate insider trading reflect the underlying perspective that such trading should be limited and is harmful to foreign investors.

Although some believe that insider trading is an effective tool for increasing the informational efficiency of the stock price and providing better incentives for insiders to produce more valuable results. The findings are consistent with the formal view and the analysis in this paper suggests that good corporate governance reduces insider trading, which is most likely based on private information. An empirical test could be used to investigate the variation in insider trading by different types of insiders, such as lower-level employees and company management.

Finally, although not required by the SET, many Thai firms currently employ the corporate governance committee under the Board of Directors. In such a case, the firms with the corporate governance committee should perform better in terms of firm corporate governance level, as well as mitigating abnormal returns from insider trading. This is also an interesting phenomenon to look at in the extension of this paper.

Constructing a corporate governance index from an ownership and management perspective for firms in Taiwan. New Evidence on the Effects of Federal Regulations on Insider Trading: The Insider Trading and Securities Fraud Prevention Act (ITSFEA). The Effects of Board Composition and Stock Ownership on "Poison Pill" Adoption Academy of Management Journal December 1, 1992.

APPENDICES