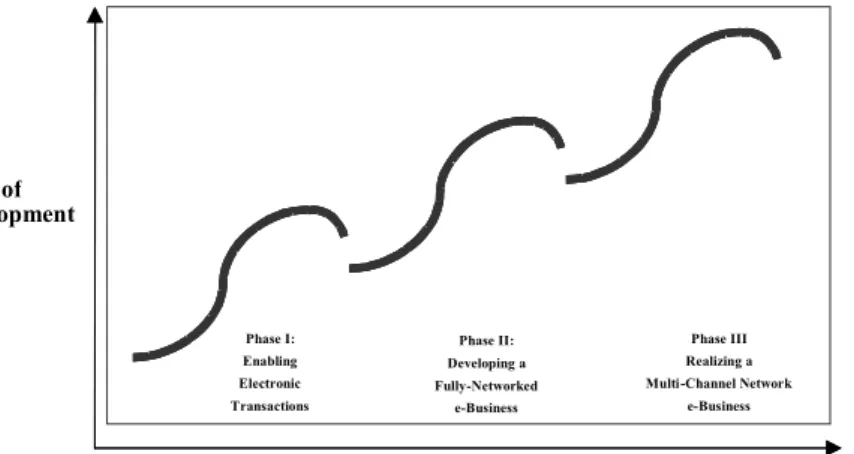

In this book, we will focus on three main themes: (1) the multichannel environment from the consumer and business perspective; (2) the markets and strategy and network of multi-channel e-business and (3) the future of the digital world. In our last section, we will try to look into the future of the digital world.

Introduction

Toward Seamless

Multi-Channel Services

Abstract

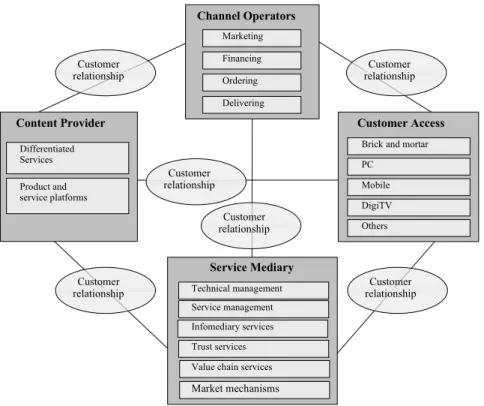

The role of service mediators in this tiered model is to provide access to different types of networks and participate in the development of customer demand. What is even more exciting about the current development in the transition to multi-channel digital content and services is that the emerging business models are ignoring the traditional boundaries of the industry.

The Future Value Chain of Service Delivery

The Future Value Chain framework describes the various actions that take place in the service delivery value chain. In the new service-based business paradigm, the central question will be where the core of the business should lie.

Business Model for Multi-Access Technologies

One of the main benefits of the BUMMAT model is that we can identify and analyze the differentiated roles that will emerge in the multi-channel environment of the future. DoCoMo has an extensive role as a transaction enabler that actively develops service offerings and takes responsibility for certified services.

The Future Model of Service Delivery

Next, we will combine the two models presented in this chapter to gain an even broader understanding of how the value chain for digital content and services will evolve in the future.

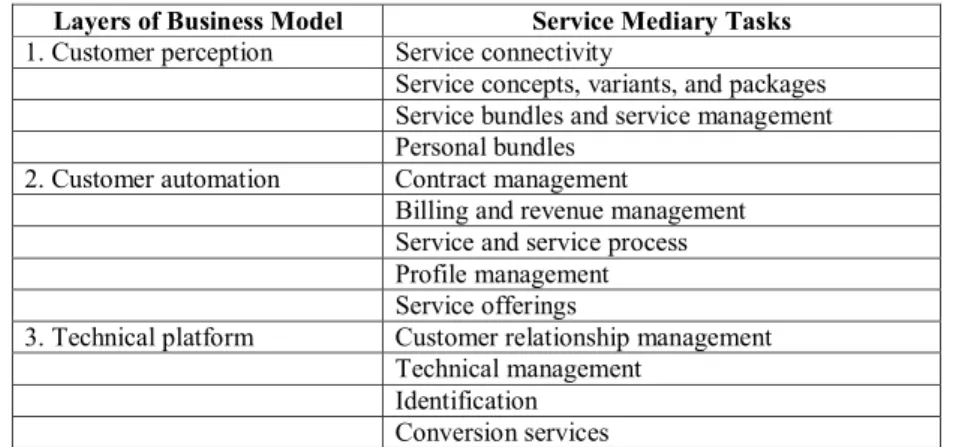

Service Mediary Tasks Related to Customer Perception

Service Mediary Tasks Related to Customer Automation

Service Mediary Tasks Related to Technical Platform

Discussion and Conclusion

Based on the analysis of the various service brokerage tasks presented in this chapter, we believe that the future is in the direction of platforms that enable business. In the future, the existing technical and service platforms will be transformed into the channels foreseen in the BUMMAT model.

For example, the analysis of customer needs should be done by a third party, who also provides this information to other players, not as in the current system, where everyone tries to fulfill every possible role with little success. We strongly believe that an individual service provider will face major technical challenges and cost inefficiencies if they choose to build all the necessary systems and skills to manage service delivery in a multi-channel environment.

Developing

Consumer-Preference Profiles as a Basis for

Concepts

These channels provide new ways to offer traditional services, such as movie tickets, in addition to new services such as ringtones. By studying the consumer's choice of channels in a multi-channel retail environment, retailers can build a consumer preference profile from which new services can be more easily developed.

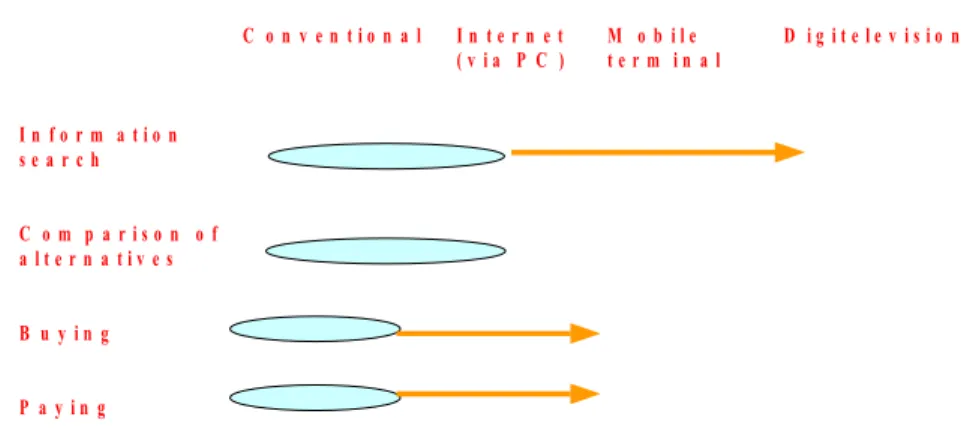

Use of Channels at Different Stages of the Buying Process

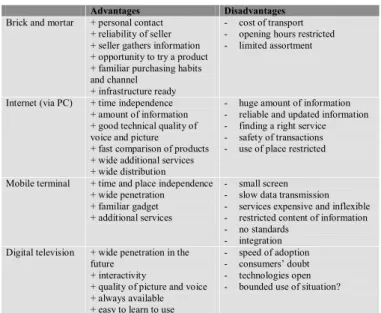

In this chapter, we will shed light on the steps of the consumer decision-making process that are most dependent on multi-channel access technologies (e.g. information search, comparison of alternatives, purchase and payment), describe the different channels, and use segmented groups of Finnish consumers to construct sample profiles of consumer preferences, based on of which new services can be developed. We assume that the steps in which the use of electronic channels is the most extensive are in the early stages of the purchase process, more precisely information search and comparison or evaluation of products.

Information Retrieval

Based on our research, these alternative channels are especially important in the early stages of the buying process, where buyers are looking for information and price comparisons. This is because consumers believe they can negotiate better through traditional channels and that electronic channels do not provide sufficient tools to examine the physical quality of the goods they buy.

Evaluation of Alternatives

In an ongoing search or update, a consumer may want to stay informed about sellers and the quality of items on the market, while a live search aims to complete a particular purchase. In Finland, we find that consumers first become familiar with an item they want to buy through a conventional channel and will not use the Internet to search for information unless they need to do so.

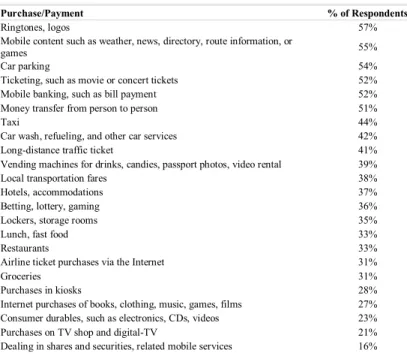

Purchases and Payments

The Channels and Their Properties

This may be partly due to the fact that the reliability of information found online is low because many retailers do not update their websites frequently. The disadvantages of using the Internet include the lack of reliability of the information received and the difficulties in finding the necessary service.

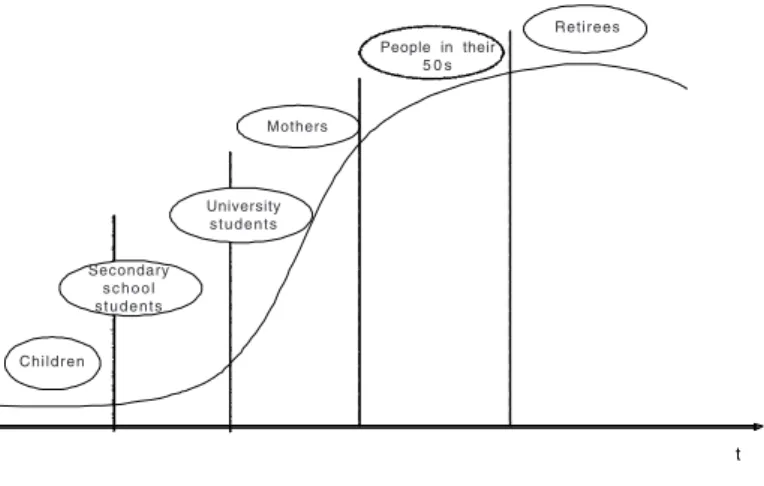

Benefits of Creating Consumer Profiles

Most of them carry cell phones to communicate and are quite familiar with using the Internet. High school students have grown up in the information society and seem to be quite comfortable using the internet and mobile phones.

Recommendations for Managers

On weekdays, they watch an average of 2.2 hours of TV, while on weekends, an average of 3.4 hours.

Consumer and

Merchant Adoption of Mobile Payment

Solutions

In order to meet the needs of the new mobile commerce arena, the banking and telecommunications industry has developed mobile payment solutions, among others. To better understand the use of mobile payments, we conducted an empirical study focusing on the following three research questions: (1) Are consumers and merchants aware of mobile payment solutions.

Knowledge and Experience in Mobile Payment Solutions

Empirical data were collected in 2003 among Finnish consumers and retailers using a qualitative and quantitative approach. The qualitative consumer study included focus group interviews with 46 consumers and a quantitative survey with 672 valid consumer responses.

Consumer Knowledge and Experience

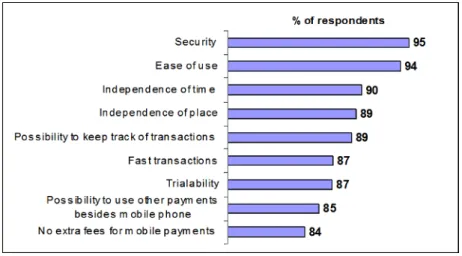

Consumer experience with mobile payment solutions is still marginal, with the exception of paying for mobile content, as shown in the survey results in Table 1. We named 11% of consumers who have experience with mobile payments and understand the concept better than most respondents as early adopters of mobile payments.

Merchant Knowledge and Experiences

More than 46% of respondents expressed interest in using mobile payments in the future and were identified as potential users. Together, early adopters and potential users are the most likely mobile payment user group in the future.

Drivers for Mobile Payment Adoption

Consumer Adoption Drivers

Most countries with high mobile phone penetration have mobile car parking service providers, such as Mint in Stockholm, Sweden (Smith, 2004). Sophisticated service providers only charge for the exact parking time and the user does not have to worry about having the correct change or adding coins to a car parking meter.

Merchant Adoption Drivers

In order to compete with dominant payment instruments and meet consumer expectations, mobile payments should also offer these advantages. New customers: Mobile payments can attract new customers, especially if purchases become easier and more accessible.

Barriers to Mobile Payment Adoption

Consumer Adoption Barriers

Lack of compliant billing procedures appears to reduce or delay consumer adoption of mobile payment solutions. Despite the general reliability of the dominant mobile payment service providers, consumers perceived more risks in using mobile payments.

Merchant Adoption Barriers

Lack of standards: Lack of standards among new mobile payment solutions is another barrier to adoption. Similar to consumers, Finnish merchants perceive banks and mobile operators as reliable providers of mobile payment services.

Preferred Applications

Applications Preferred by Consumers

Merchant Preferred Applications

Concluding Remarks

Compliance with local payment culture, jurisdiction, existing payment infrastructure and instruments is a prerequisite for the adoption of mobile payments. Interest in the future use of mobile payments is significantly higher than current use (A.T. Kearney, 2002).

Objectives of Search and Combination of

Consumer Markets

An Explorative Study

Despite these developments, there is little empirical evidence to support the supposed positive effects of electronic markets. Instead, consumers construct preferences using a variety of strategies that depend on the demands of the job.

Benefits of Electronic Markets to Consumers

If this hypothesis holds, consumers should be able to find what they are looking for using only electronic sources. Rather than being used independently, it is plausible that electronic sources are used to supplement other information sources.

Tourist Information Search

Consumer search strategy appears to be related to the combination of information sources used (Fodness & Murray, 1998). Consumers who use electronic information sources use a greater number of information sources than consumers who only resort to non-electronic sources.

Data Collection

Results

Number of Information Sources Used

Combinations of Information Sources

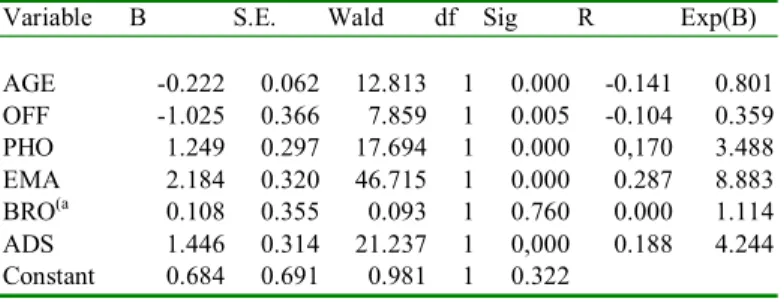

As you can see, variables excluding the use of brochures had an impact on the use of the WWW as an information source. However, the use of the WWW and other information sources without the need for transportation was positively associated.

Decision Criteria and Choice of Information Sources

Discussion

Most consumers with access to the WWW are searching for product information, and the WWW is a cost-effective medium to reach these consumers; (2) The primary web-related goal appears to be the desire to avoid moving while searching for products; it may prove difficult to try to replace electronic information channels with media which do not fulfill this objective; (3) Electronic channels may not yet provide consumers with all the information necessary to make the purchase decision; therefore companies should ensure that consumers are directed to other, supplementary sources of information when the electronic channels do not meet consumer expectations; (4) Consumers should be able to obtain product information through supplementary information channels based on human-to-human interaction; Email and telephone services should be particularly suitable for this, as they meet the previously mentioned goal that consumers seem to attach to the use of electronic channels - to avoid the need to move around.

Limitations of the Study

Topics for Future Research

The nature of competition in electronic markets : an empirical study of online travel agency offerings [working paper]. Joint purchasing decisions: a comparison of the influence structure in decision-making units of families and couples.

Consumers on the Road from

Third, the evolution and current state of B2C e-commerce and changes in consumer purchasing habits are discussed. The subject of the exam is the development of means of communication and its wider consequences (eg receiving advertisements, paying invoices and consumers' purchasing behaviour).

Historical Development of Communication

The rapid development of information technology that began in the 1990s has had a major impact on the working day of the average consumer. Due to its advanced technology and people's positive attitude towards technology, Finland participates in the first wave of this development.

Developments in Finland

Comparison to International Developments

The uses of means of communication are also similar, regardless of the user's age or economic existence. When economic growth began to slow at the turn of the last decade, it was immediately reflected in the development of communications.

The Importance of Pricing

However, the share of telecommunications in GDP is higher in Finland than in the other control countries. This shows that Finns also use more electronic communication services than consumers in other countries.

Trends

If the prices of electronic communication services are compared internationally, Finland is one of the cheapest countries (Statistics Finland, 2003b).

Consumer Reception of New Marketing Channels

Marketing Channel Preferences in Finland

Both offer marketing opportunities that don't interfere at the wrong time and can be read regardless of time and place. Monthly loyalty customer offer New recurring offer 3 holiday offers in one week E-MAIL Monthly loyalty customer offer New recurring offer 3 holiday offers in one week TEXT MESSAGE Monthly loyalty customer offer New recurring offer 3 holiday offers in one week PHONE CALL Monthly loyalty customer offer New magazine offer 3 holiday offers in one week LETTER.

Marketing Channel Preferences in Australia

Because consumers seem to want even more control over receiving direct marketing, the emphasis going forward will be on receiving messages through channels that are easy, comfortable and not annoying. In the future, senders will be required to introduce multi-channel solutions capable of targeting their marketing messages to each recipient's preferred receiving channel.

Will E-Commerce Change Shopping Habits? Assessing Potential Adoption

Potential Barriers to E-Commerce

Citizens in the EU-15 countries who made purchases via the Internet in 2003 (percentage of the population). On the other hand, as shown in Figure 7, there are several popular e-commerce product categories that were not offered by mail-order companies, such as various tickets and hotel reservations; so in these areas the internet certainly offers a whole new shopping channel.

Development of Alternative Channels for E-Commerce

This finding seems to point to the conclusion that at least a significant portion of B2C e-commerce is actually done by the same people who are customers of the traditional mail order business (where the order is placed by e.g. coupon or phone) , because the same product categories are also prominent in the relevant business area. This is why the share of distance sales can be expected to grow faster than for traditional mail order or regular retail sales alone.

Conclusion

Digital television will probably become another widely used interface, but this is unlikely to happen in the short term. If the receiver is unable to do this, he or she cannot interpret the message in the manner intended by the sender.

Development of Multi-Channel Customer Relationships

Communication is even understood as a common commodity (i.e. the distribution of common impressions and experience in the community) (Viherä, 2002). In the controlled relationship, the company sets the channels according to its own preferences and tries to direct customers to the most beneficial or pleasant channel.

Endnote

The Effects of

Digital Marketing on Customer Relationships

Introduction: Digital Marketing and Customer Relationships

Boosting Customer Relationships with Digital Marketing

Central Elements of Digital Marketing

Brand communication and service do not always have to be personalized or interactive in order to have an impact on customer relationships. Adding personalization and interactivity, however, can increase the positive effects of digital brand communication and service on customer relationships.

Brand Communication

For example, a representative of the marketer may be an active member of the brand community who joins in everyday discussions among the other members. On the other hand, a company's ability to control the discussion of brand communities may be relatively limited or non-existent.

Service

Most of these antecedents of e-loyalty—7Cs, as Srinivasan and others call them—are service-oriented, providing further evidence of the importance of e-service in building customer relationships. Also emphasizing the importance of service over other attributes when building customer loyalty via digital channels is the interesting evidence suggesting that sensory attributes, especially visual cues, will influence choice to a lesser extent online than offline (Degeratu et al., 2000 ).

Personalization

Instead, it is enough to recognize that personalization can mean different things to different people. Individualization: The system's ability to adapt itself to the user, based on the user's displayed behavior.

Interactivity

For example, some pop artists showed their live concerts on the Internet for free on sponsors' websites. For example, it has been found that it takes an average of 21 hours for e-merchants to respond to customer email inquiries, and 18% of sites never respond (The DMA's State of the E-Commerce Industry Report, 2002).

Summary and Conclusion

Consumer choice behavior in online and brick-and-mortar supermarkets: The effects of brand name, price, and other search attributes. Using e-mail for relationship marketing in the consumer market: Special interest in brand attitudes and brand loyalty [Master's thesis] (in Finnish). Helsinki School of Economics.

Strategy Turned into Action

A Case from

Global Implementation of B2B E-Business

Introduction: Logistics at the Core of Global Operations

Case Background: Solutions in After-Market Logistics

Volvo and Spare Parts Logistics

Spare parts logistics is a complex operation characterized by intensive physical and information exchange between various stakeholders; in Volvo's case, thousands of suppliers and tens of thousands of distribution points to hundreds of thousands of end customers. Industrial product families contain hundreds of thousands of parts, requiring both long-term service responsibility and complex super-session chains.

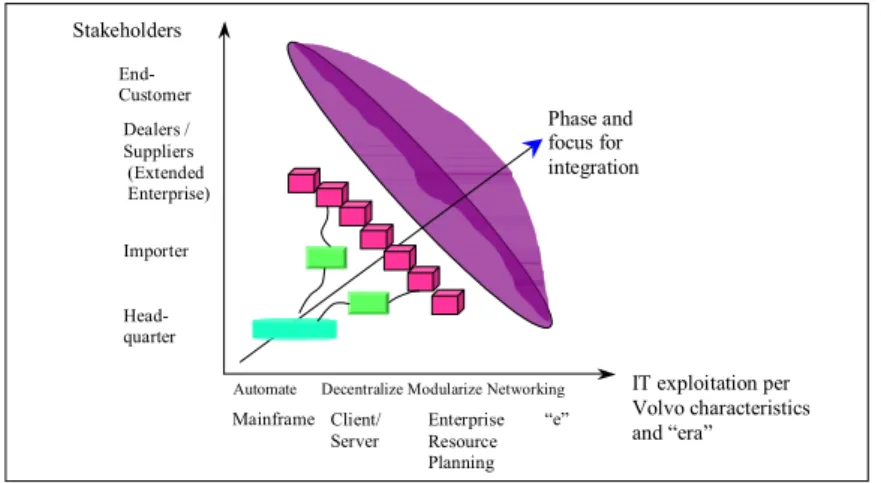

Thirty Years of Evolutional Business Development and Systems Integration

In figure 1, the distribution of parts is presented; it is not necessary (and in many cases it is not) that the flow of information goes in the same way (the end consumer is referred to as end user in the figure). Bringing the customer order point closer to the source of the demand provides streamlining benefits through the retrieval of information provided at the source as well as automatic search capabilities.

Scenario Development

- The spare parts are distributed directly from the support ware house to the end customer, which is the customer’s workshop in all sce-

- The spare parts are distributed directly from the central ware house to the dealer and then from the dealer to the end customer

- The spare parts are distributed directly from the central ware house to the end customer, bypassing both support warehouse

- The spare parts are distributed directly from the supplier to the end customer, bypassing all traditional distribution centers

Spare parts are distributed directly from the central warehouse to the dealer and then from the dealer to the end customer. Spare parts are distributed directly from the central warehouse to the end customer, bypassing both support warehouses to the end customer, bypassing both support warehouses.

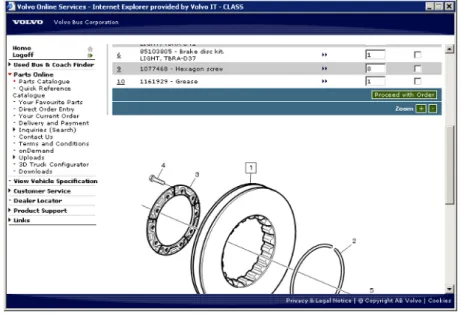

Parts Online: What Became Real?

The first implementation has increased Volvo's awareness of the dealer situation and enabled dealers to interact with end customers online. The ongoing actions can be seen as a summary of the development and implementation results in Table 1.

Opportunities and Challenges for B2B

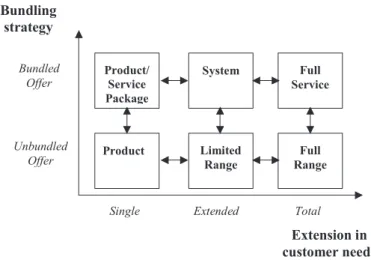

Moving from Products to Services-Case SKF

Today, managing the transition from products to services is a very important emerging managerial issue in the business-to-business environment (Oliva & Kallenberg, 2003). Also, we find that buyer trust in the supplier is an essential factor in the transition from product to service-based systems.

Full-Service Contracts

More specifically, we use the theory of full-service contracts (Stremersch et al., 2001) to describe how SKF moved from offering products to offering full-service contracts. In our research, we use the concept of full-service contracts (Stremersch et al., 2001) to investigate the transition from product-oriented thinking to service-based concepts.

Case SKF

Moving Toward Full-Service Contracts

These new concepts require SKF to build closer relationships with customers and understand customer processes.” These new concepts require SKF to build closer relationships with customers and better understand customer processes.

Setting the Stage: endorsia.com and Intelligent Bearings

This can be done using a sensor attached to the bearing or bearing housing. Of course, there are significant benefits to knowing more precisely the status of the bearing condition; for example, there is a monetary loss of more than 10,000 euros per hour when a paper machine cannot be used due to a mechanical problem (ie a bearing failure).

Theoretical Implications: Differentiated Offerings

With this new type of bearing, the user can get more precise data about the condition of the bearing by measuring the bearing runout and vibration.

Managerial Implications: IT and Trust

From the SKF case we can see that trust in the supplier is a key factor in the move to full service contracts. Full service contracts require some responsibility to be shifted from the customer to the supplier, and this naturally requires considerable trust in the supplier on the part of the customer.

Evolution of Maintenance

In addition to confidence, investments in innovative information technology played an important role in SKF's transition to full-service contracts. The customer's trust in the supplier also plays an important role in the transition from product sales to full service.

Shifting Perspective from Design

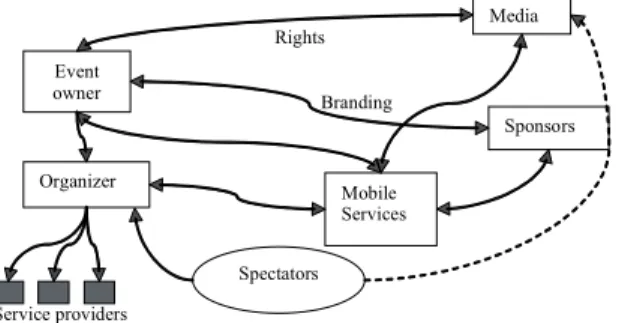

Extending the Scope from Spectators to Stakeholders

The chapter begins with a background that describes the betting business in Sweden, previous research on the development of TrottingPal and related work. By revisiting previous work on TrottingPal and adding a stakeholder perspective, the chapter discusses ways in which the implementation of mobile technology (i.e., TrottingPal) can address and adapt to emerging issues.

Background

The Betting Business in Sweden

Three Emerging Problems

Foreign Internet-based competitors are gradually taking market share of the betting industry in Sweden. Trotting track managers in Sweden are concerned about the consistent decline in attendance.

The TrottingPal Research Project

In the next section, we summarize the previous research into the development of the mobile spectator support system TrottingPal. The evaluation also provided data to reflect on the quality of the design and also a feedback process on researchers' interpretation of the context and practice (see Figure 1, A and C).

Field Work and Design

A field study was done to understand the context and practice of the spectators to a degree sufficient for design. The main goal was to investigate and verify ideas and the system while in authentic use, as opposed to simulations.

Evaluation of Technology Use

To design for personalization, a number of information channels were made available in the mobile system. Spectator interaction within the system established a common topic, which encouraged users to supplement and contribute in order to gather a unified set of information on a specific topic (e.g., an expected outcome of a race).

Electronic Business Meets Empirically Informed Design

Outlining the emerging issues for the gambling industry and trotting track managers, along with the research background of TrottingPal, the remainder of this chapter will delve deeper into the following research question: What are the benefits of TrottingPal to stakeholders. The extent to which such methods are part of the product work cycle has also been discussed (Bly, 1997).

The Potential Business Possibility

The research has focused on supporting key attributes of spectators as opposed to the business perspective of achieving the fulfillment of stakeholder objectives. The shift in focus from design work to business potential calls for further analysis, examining how the various stakeholders in the value chain as a whole benefit from the implementation of technology.

Surveying Stakeholder Goals for Business

Seamless interaction in the racetrack ecosystem improves and accelerates communication between stakeholders and provides new ways to create and measure offers. This chapter proposes a broadening of the analysis perspective to relate to stakeholder goals.

Endnotes

The chapter concludes that the challenge for design-oriented research in the attempt to reach a product stage can find support in broadening the perspective and relate to stakeholder objectives. The second contribution is that by extending the scope to stakeholder objectives, benefits to developed relationships have been identified, mediated by seamless stakeholder interaction.

Acknowledgments

Mobile Games

Emerging Content Business Area

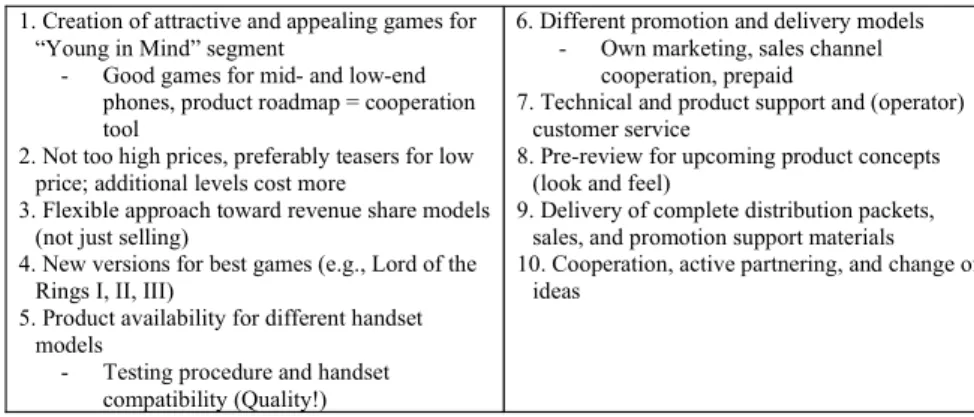

The main purpose of this chapter is to analyze and discuss the challenges in the emerging mobile gaming industry. The analysis is based on the author's experience in the mobile games market as well as various secondary sources.

Characteristics of Mobile Game Markets

In addition, this chapter is based in part on the author's report published in the European Union, established in the AcTeN Content Market Monitor Series (2004)6.

Two Original Business Areas

This can become a big hurdle for a small company starting out in the mobile gaming business. In addition, a game developer must find a way to localize their production to key markets in the most efficient way.

Risky Business Area

A company that aims to gain large revenues in the market must find methods and activities to bring its products to the main markets, such as Japan, the United States, and Korea. While it takes a minimum of 1 to 3 million euros and 12 to 24 months to develop a console game, it only takes a few hundred thousand euros and two to four months to develop a simple mobile game and four to six months for a more complex game. mobile games.

Mobile Game Production Process

In comparison, developing a full-scale advanced game for mobile consoles can take many developers more than a year. Several development companies have chosen only a few technology solutions and gaming platforms to support them.

Current Market Trends

The more advanced the technology used in game development, the more complex and time-consuming it is to make.

Growth Business, but Turbulent

S. and Japan Lead the Show

In Europe, the mobile gaming sector has developed rapidly thanks to strong support from device manufacturers and the high penetration of mobile telephony. It is expected that when the mobile game industry reaches the mass markets, the big Japanese and American companies will enter.

Consumers Increasingly Demand Quality

Business Models

Key Objective: To Make Profit

As in the film industry, the importance of this business area as a profit maker can become very important. The distribution of revenues between different markets is the key issue for understanding business models within the industry (see Table 2).

Critical Success Factors

First, the distribution technology in mobile networks is capable of delivering mobile games to consumers. Within computer gaming, the importance of mobile games is expected to increase in the near future.

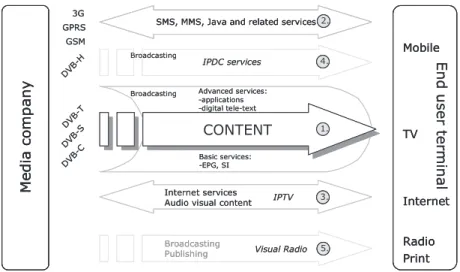

Digital Television and Multi-Channel

However, digital television today is taking its first steps and the evolution requires the contribution of every actor in the value chain. The combination of different digital media forms a multi-channel communication environment, which enables the seamless sharing of content across different channels and the possibility to interact with the viewer.

Development of Digital Television in Europe

Tomorrow, television will be an even more powerful medium due to the increased capacity to broadcast content and the ability to create interactivity with viewers through digitization.

Digital Television Markets in Europe

There are several estimates and forecasts of how digital TV markets will grow in the near future. In the following, we deal with examples of digital television development in Great Britain, Finland and Italy.

United Kingdom

Finland

Italy

An interesting feature of the Italian digital television market is the government subsidy of €120-150 million for 2004 to meet the demand of 900,000 MHP-enabled decoders (4.2% of TV households). However, to achieve the government's goal of analogue switch-off, sales of set-top boxes must increase dramatically.

Evolution of Digital

Television as a Multi-Channel

Internet access can also be used as a return channel or as a two-way enabler of interactivity. For both the return channel and the two-way interactivity, Internet access is used in the same way as the mobile channel.

Case BumtsiBum/MTV3

Issues affecting technological development are standardization, technological choices made by market actors, and the general adoption of digital television. The true multi-channel world will not be complete until digital TV has reached its maturity and all media have converged.

Case of Monopolies at Stake

Strategies for Gambling Market

Background: Why is Gambling a Monopoly Industry?

Second, most studies conclude that it is even more difficult to overcome a gambling problem than alcohol and drug addiction (NRC, 1999; Prochaska et al., 1992; Thygesen & Hodgins, 2003). Therefore, due to its special characteristics, gambling service providers are normally required to have a license from the national state where gambling services are marketed.

Online vs. Internet Gambling

Regulation of Online Gambling

The main rule is to apply the national provisions of the country where the service provider is established (ie the country of origin principle). The British government will not impose restrictions on the cross-border supply of online gambling services (Department for Culture, Media and Sport, 2004).

The Jurisprudence of the European Court of Justice

The latest cases in Denmark and Greece illustrate the EU Commission's view of what constitutes violations of the principle of proportionality. Proposal for a directive of the European Parliament and of the Council of 13 January 2004 on services in the internal market.