One of the first responsibilities of a committee is to find an expert to rely on. An ability and willingness to attend all investment committee meetings and to do homework before each meeting - to prepare to discuss the topics and proposals to be addressed at the meeting.

ORGANIZATION OF THIS BOOK

CHAPTER 1

But it is not practical for boards to make investment decisions for the fund, so the board almost always appoints an investment committee to take on this responsibility.

STANDARDS TO MEET

This was a revolutionary concept as the old common law dictated that each investment should be prudent in and of itself. Caution should be based on the soundness of the logic and process underpinning the hiring and retention of an investment manager, and on an a priori basis – not on the basis of Monday morning quarterbacking.

COMMITTEE ORGANIZATION AND FUNCTIONS Organization

Once the board has decided on its consultant, it should expect to approve most of the consultant's recommendations. This fact leads to what I believe to be a consultant's primary responsibility: to provide continuing education to board members.

INTERACTION OF COMMITTEE AND ADVISER Committee Meetings

The adviser should include information about the asset class itself if the asset class is relatively new to the committee. Bringing a manager to meet with the committee can be a useful part of committee education.

SOCIAL INVESTING

But while endowment funds with unlimited investment may use an imputed income formula of 5% 10 , I would recommend no more than 4%, perhaps less, for an endowment limited by social investment restrictions . If everyone agrees, then of course the board should go ahead with its social investment plans.

IN SHORT

CHAPTER 2

RETURN

The dollar-weighted rate of return (also called the internal rate of return) measures the rate of return for each dollar invested over the measured interval. In this case, the exact annualized time-weighted rate of return for two years is 14.89%.

RISK

Systematic with stocks that have certain other common characteristics

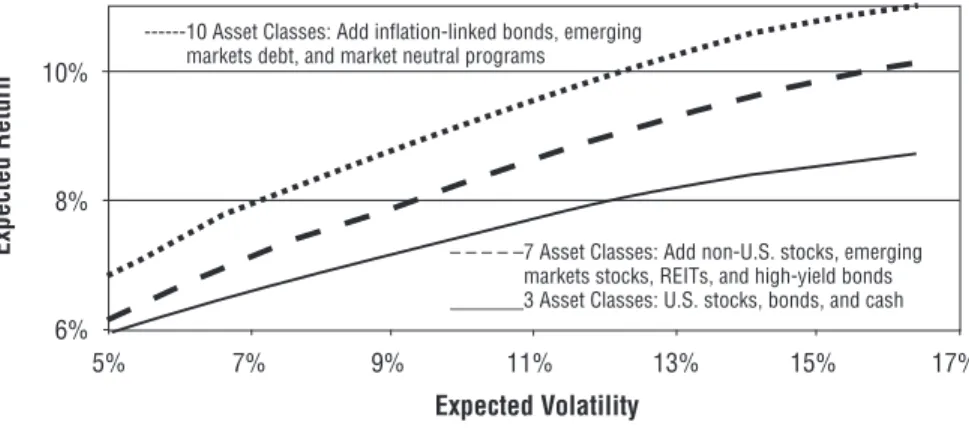

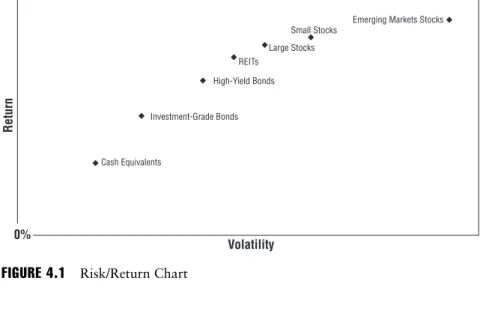

Diversifiable risk is a critically important concept that we can take advantage of, as we will see later in this book. We can reduce risk most productively by investing in various asset classes that have a low correlation with each other—domestic stocks, foreign stocks, real estate, bonds.

CORRELATION

The job of running a mutual fund is not to see how little risk we can take, but to see how much risk we can take—. By assembling a portfolio of assets whose volatilities have a low correlation with each other, we can have a portfolio of relatively risky assets that have a materially higher expected return but no more volatility than a portfolio with much less dangerous assets.

RISK-ADJUSTED RETURNS The Sharpe Ratio

Risk-adjusted returns are considered by many to be the true measure of an investment manager. Of course, we need to make sure that the high-volatility, high-return manager doesn't push us beyond the volatility limits for our overall portfolio.

DERIVATIVES—A BOON OR A DIFFERENT FOUR-LETTER WORD?

CHAPTER 3

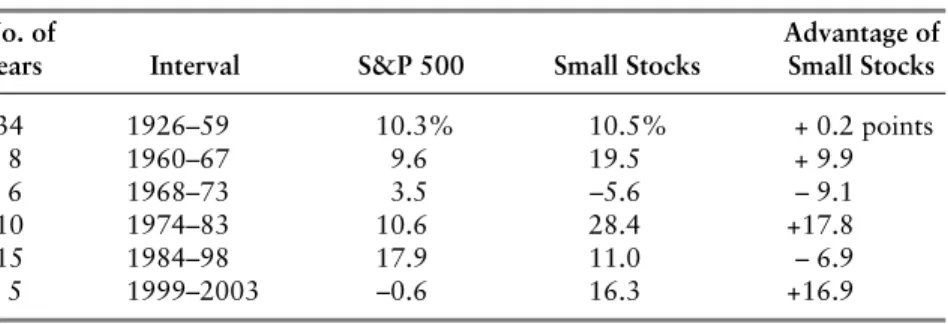

Good returns in short-term intervals are not very important except as they contribute to the long-term rate of return. At the end of each game, it's easy to see how we scored - what our long-term rate of return was.

TIME HORIZON, RISK, AND RETURN Time Horizon

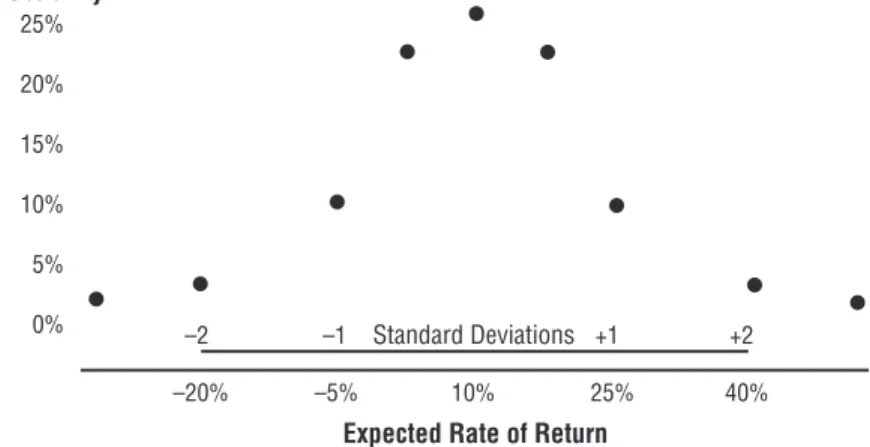

But what does it mean to say, "We would be willing to incur a standard deviation of X percentage points". But if the markets are turbulent, a standard deviation of X percentage points will be a pipe dream.

POLICY ASSET ALLOCATION Benchmark Portfolio

I think a more appropriate objective would be "to earn the highest possible rate of return without incurring more risk than the risk of our Benchmark Portfolio". We need to be greedy, aim for the best possible return – as long as we stay within our risk limit (set by our Benchmark Portfolio). Therefore, the index returns on our benchmark portfolio should be the minimum return we should aspire to earn over the long term. Therefore, we need to build this diversification into our Policy and Standards Asset Allocation Portfolio.

BENCHMARKS FOR MARKETABLE SECURITIES

We haven't even mentioned the most famous stock market index of all - the Dow Jones Industrial Average of 30 stocks. To illustrate the differences in conventional wisdom, UK pension funds have historically invested 80% or more of their portfolios in common stocks, US pension funds 60% to 70%, Canadian pension funds once more than 40%, and Swiss pension funds closer nothing. Such resource allocation is partly influenced by local law, but in most cases Company A follows the approach because it is the conventional wisdom – it is the approach followed by its peers in its country.

PREPARING A STATEMENT OF INVESTMENT POLICIES

CHAPTER 4

By far, the single most important investment decision our mutual funds make is not the particular investment managers we choose, but our asset allocation. If there is, it is not evident in other countries, where the typical distribution of assets varies greatly from country to country. Instead, let's set our asset allocation based on (1) our objectives, as discussed in Chapter 3,

CHARACTERISTICS OF AN ASSET CLASS

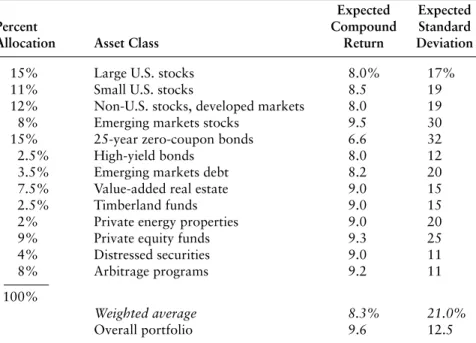

We can begin by studying historical returns, placed in the context of valuations now and at the beginning of the interval we are measuring. As of today, what growth in long-term GDP (Gross Domestic Product) do we expect for the U.S. In asset classes where there is little reliable historical information, how do we rate expected volatility.

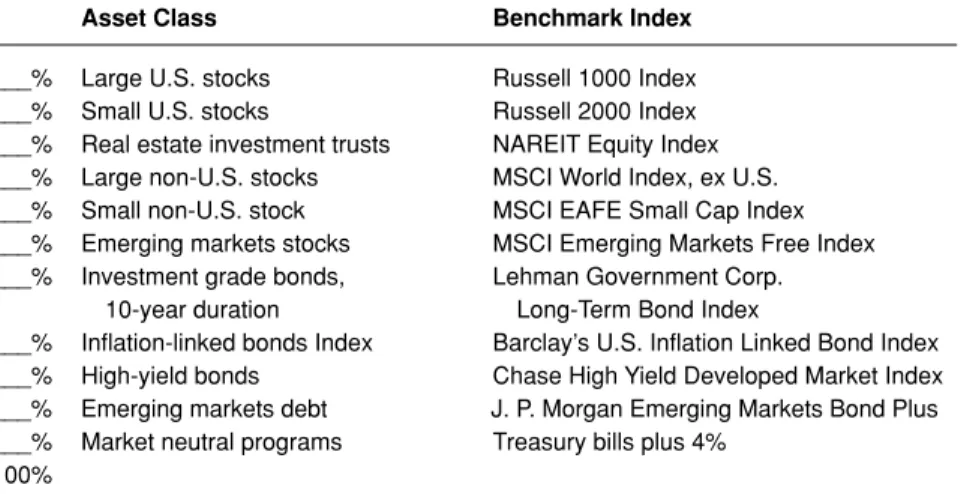

ASSET CLASSES

Emerging Markets Debt Some people view debt issued in the developing countries of the world as just another facet of high-yield bonds. It is difficult to argue that expected stock returns in the developed countries of the world should differ materially from those in the United States. The underlying annual volatility of the venture capital stocks should have been much higher.

PUTTING IT ALL TOGETHER

CHAPTER 5

We fail to think of many other types of viable—and valuable—alternative asset classes. An alternative asset class can be considered any asset class that our decision makers have not previously considered. For some, any stock other than the largest, most sought-after U.S. stocks may be an alternative asset class.

LIQUID ALTERNATIVE ASSETS

Conversely, if a convertible security is priced at a premium above its conversion value (the value of the stock into which it is convertible), and if the issuer of the convertible security should call this security - that is, force its conversion to common stock — The arbitrator would lose money. It all depends on how much leverage is used, how it is used, the underlying volatility of the leveraged investment and – of course – the expertise of the manager. In 1999, a private sector group called the Counterparty Management Policy Group issued a report to the SEC that said in part: "The policy group believes that leverage, although an extremely important concept with broad intuitive appeal, is not an independent risk factor whose measures can provide useful insights for risk managers.

ILLIQUID INVESTMENTS

It shouldn't surprise us that many of the very best investment managers become hedge fund managers, because their compensation can be astronomical. It's true that some of the best investment managers of our time are hedge fund managers, and they have made their investors rich. But the fund of funds obviously charges a high fee on top of the high fees charged by sponsors of private investment funds.

PRIVATE ASSET CLASSES Real Estate

CHAPTER 6

We should try to get the best possible managers in each individual asset class - the managers who are most likely to produce the best future performance. And simply going after managers with the best record is a losing game, because all managers have hot streaks and cold streaks. Finally, no one can come close to being a perfect judge of an investment manager's future performance.

THREE BASIC APPROACHES

Let's go back to our original goal of having the best possible managers in every asset class. We should be looking for the best manager (or managers) we can get in every single asset class, regardless of geographic location. Why the advisor believes his candidate is the best we can get in this asset class.

CRITERIA FOR HIRING AND RETAINING MANAGERS

Expected impact on the fund’s overall volatility. Two facets

Support staff. Material turnover in the research or other support staff may impair the predictive value of past performance. 50 million seems to have little predictive value for a manager now managing more than $5 billion. In this case, how many years of a driver's past performance do we think have predictive value.

HIRING MANAGERS Evaluating Candidates

Where the standard does not fit very well, we should not demote the manager because of the risk of the standard. 8 Many of the best managers fall short of a standard, and they shouldn't. However, my preference would be for whichever approach is likely to achieve the best rate of return net of all costs, and that depends on the facts of the case. This blindness in itself is a major advantage of using mutual funds exclusively.

RETAINING MANAGERS

CHAPTER 7

If the mutual fund has one or more separately managed accounts (unlike mutual funds), a custodian is a must. Some notorious fraud cases could hardly have occurred if the client had used a custodian. If the bank were ever to fail, its creditors would be unable to get their hands on any of our assets.

CUSTODIAL REPORTING

He also has an interest in keeping the trustee's records accurate because he knows that we are relying on the trustee's statements, not his (the trustee's). In addition, potential errors in trust records can affect the calculation of investment performance, which is perhaps the most important management information. If necessary, the administrator also prepares and files tax returns and special state reports.

MANAGEMENT INFORMATION

CHAPTER 8

Good past performance can be the fortuitous result of a poorly designed investment program, and poor past performance can be the fortuitous result of a well-designed investment program. But ultimately, an evaluation comes down to asking the right questions and concluding with qualitative judgments.

INVESTMENT OBJECTIVES

ASSET ALLOCATION

THE FIDUCIARY COMMITTEE

What limitations does the committee impose on its advisor – either through limits on its openness to new ideas or the frequency of its meetings.

THE ADVISER

INVESTMENT MANAGERS

CHAPTER 9

Its purpose is to divert a continuous stream of income to support the activities of the sponsoring organization. For the health of the organization, the volume of this income stream should maintain its purchasing power over the long term. While fiduciary principles generally require only that the institution maintain the nominal value of the gift, to provide true ongoing support institutions must maintain the inflation-adjusted value of the gift,” writes David Swensen of the Yale Endowment Fund.1.

THE TOTAL RETURN, OR IMPUTED INCOME, APPROACH

While there are many variations, we have found that a good definition of imputed income is: any surplus of imputed income). If they do, the fund, under the Total Return Approach, should regain the purchasing power it has lost – provided the percentage of imputed income was set responsibly in the first place. If we've got our imputed income formula right in the first place, let's not tinker with it.

OWNERS” OF THE ENDOWMENT FUND

CHAPTER 10

In both cases, the plan sponsor bears the entire risk or opportunity of investment results. Risk for the plan sponsor is therefore just that—the possibility that the sponsor will have to make larger contributions to the pension fund, perhaps suddenly much higher. 1. This is because a declining funding ratio means that the plan sponsor will have to come up with higher contributions to the plan.

PENSION PLAN LIABILITIES

For pension funds, risk is the possibility that the plan will not be able to pay all promised pension benefits to retirees. As long as the plan sponsor remains solvent, this is not much of a risk, because if the pension assets have no pension liabilities, the plan sponsor must make higher contributions to the pension fund. So trying to maintain a level of funding ratio—the ratio of assets to liabilities—is a moving target.

INVESTMENT IMPLICATIONS

CHAPTER 11

We committee members spend relatively few hours per year on the fund's investments and should not try to do it alone. We must also appoint a custodian (usually a trust company) to hold all of the fund's assets and provide timely reports on the fund's market values. To the extent we can leverage all the attractive asset classes we can, the additional diversification can meaningfully reduce the fund's volatility and even increase expected returns.