Furthermore, establishing and maintaining a sound ethical management program is a necessary component of the ethical management framework. Finally, an independent assessment of the effectiveness of the ethical management framework is needed to evaluate the organization's ethical performance, which must be reported to both internal and external stakeholders.

Independent assessment and reporting to stakeholders

An ethical culture assessment by the IAF provides audit committees with an objective and independent view of the organization's ethical culture (IOD, 2014a:3). Hubbard (2002:57) states that ethics is part of an organization's control environment and that a weak ethical culture contributes to weaknesses in other business controls.

Leadership commitment

The Chartered Institute of Internal Auditors (2014:3) in the UK supports this by emphasizing that boards of organizations need assurance and confidence that acceptable values and ethical practices exist as part of the organizational culture. This is supported by Boyle, Hermanson, and Wilkins (2011:4) who argue that when auditors assess ethical culture, they are in fact auditing the organization's control environment.

Ethics governance structures

Independent assessment and reporting to internal and external stakeholders

Similar to an audit rating methodology to assess ethics, a model that assesses the maturity of the ethical culture within an organization can be applied by the IAF (IIA, 2012a:13). The IIA (2012a:7) emphasizes that a maturity model provides a basis for the IAF to verify the maturity rating through testing and then report on the strengths and weaknesses of the ethical culture.

Findings

Section 1: Ethics management and ethics assessment standards

Most of the participants' organizations have adopted a governance code, whether Namcode or King III, but the requirements for the implementation and review of ethics programs were not known, except for the implementation of ethics hotlines. However, one participant (from management) was aware of the need to implement ethics-related policies and assess compliance with these (given that this participant was an ethics officer).

Section 2: Views on ethics assessment practices within organisations The majority of participants agreed that the IIA Standards are a good start to assessing

In addition, they believed that internal audit, as an independent evaluator of ethics, would demonstrate to stakeholders the robustness of an organization's ethics programs. Some participants even believed that stakeholders would see this as a proactive step in reducing fraud and financial losses.

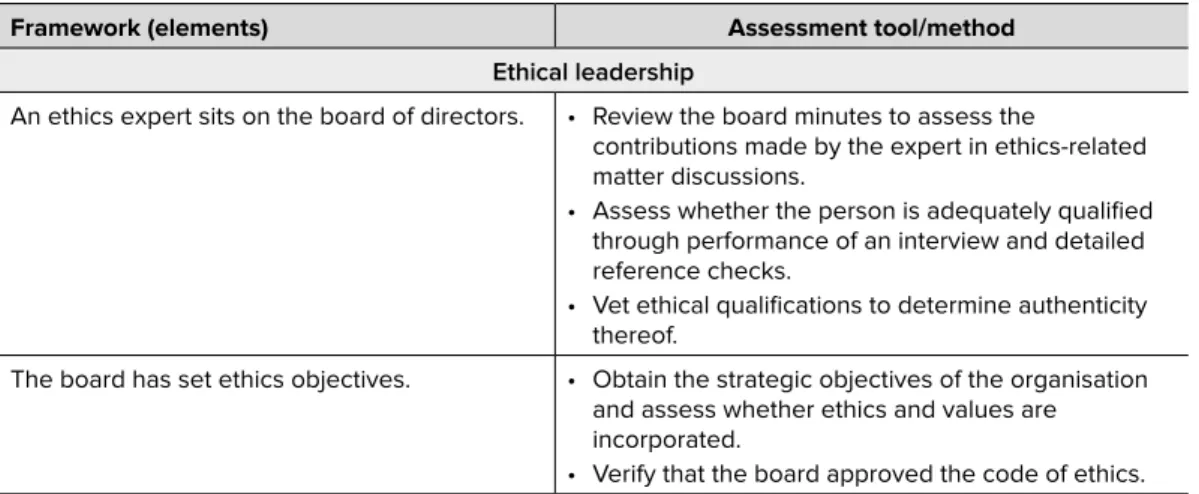

Section 3: Proposed ethics framework .1 Ethical leadership

Although the participants agreed that it was important to have these elements, the ethical risk assessment is not a separate item at the participants' organizations, but part of the annual risk assessment. In addition, participants also noted that the IAF's independence added value to the organization's ethical initiatives.

Conclusion

Recommendations

Taken together, the findings suggest that formal guidance is needed to prioritize ethics within organizations and at the appropriate level within an organization. Conducting ethics compliance assessments, with specific reference to the effectiveness of an organization's overall ethics management framework, can add value in improving the organization's ethical culture.

Areas for future research

Corporate Governance and Financial Performance of Local Companies Listed on the Namibian Stock Exchange. The Impact of Corporate Ethical Values and Enforcement of Codes of Ethics on the Perceived Importance of Ethics in Business: A Comparison of the U.S.

Responsible business practices: Aspects influencing decision-making in small,

- Introduction

- Literature review

- SMMEs in South Africa

- SMMEs versus larger businesses

- Management functions in SMMEs

- Methodology

- Sampling Stage 1 – Nonprobability purposive sampling

- Sampling Stage 2 – Probability systematic sampling

- Limitations

- Results

- Key differences between age groups (H 1 )

- Key differences between respondents’ highest level of education (H 2 ) Next, it was determined that there is a statistically significant difference between the

- Key differences between genders (H 3 )

- Discussion and conclusions

- Conclusion

H1: There is a difference between the age group of the respondents with respect to each of the aspects that influence RBP decision making. H3: There is a difference between respondents and non-respondents regarding aspects that influence RBP decision making.

Business practices influencing ethical conduct of small and medium-sized

- Problem statement

- Research objectives

- Review of literature

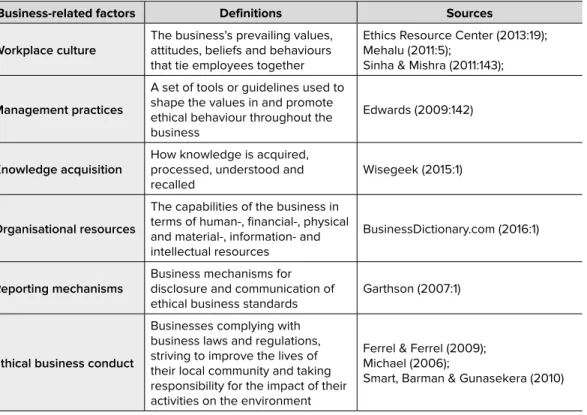

- Workplace culture

- Ethical business conduct

- Research hypotheses and operational definitions

- Research design and methodology

- Results of the validity and reliability of the measuring instrument

- Results of the descriptive statistics

- Results of the correlation analysis

- Results of the multiple regression analysis

- Conclusions and recommendations

- Limitations of the study and future research opportunities

Empirically determine which of the selected business practices influence the ethical business conduct of SMEs in Uganda; and. Employee knowledge acquisition, management practices, and ethical business had means that tended to agree with the scale (score 4). The results of multiple regression analyzes show that the independent variables (employee knowledge acquisition, management practices and management of organizational resources) explain 21.8% of the variance of the ethical business conduct of SMEs.

Inculcating ethics in small and medium- sized business enterprises

A South African leadership perspective

- Research objectives

- Method

- Are personal values reflected in the values of the business?

- Is business ethics a strategic imperative?

- Do the business leaders act in accordance with their values and the businesses rules?

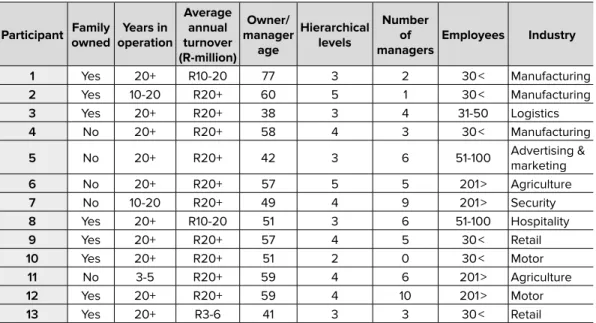

The aim of the study was to determine the ethical risks faced by SMEs and to determine how business leaders manage these risks by inculcating business ethics in their organisations. The owner provided documents as evidence of the systems and operational mechanisms used in ethical management. The responses were also evaluated to determine whether the number of hierarchical levels influenced the company's strategic (ethical) orientation.

An evaluation of the reporting on ethics and integrity of selected listed motor

Background

This has created a greater need for transparency in reporting on both financial and non-financial information (Mironiuc et al., 2013). Ethics and integrity are an integral part of business today and add value to the transparency of reporting on Corporate Social Responsibility (CSR) issues. The connection between CSR activities, ethics and integrity is that both are matters of moral responsibility and should be reported on.

Reporting on ethics, integrity and anti-corruption

The importance of ethics and integrity was highlighted in the latest King IV report. The second principle also deals with ethics and states that the governing body must control the ethics in an organization and that it must establish an ethical culture in the organization (IOD, 2016). In the case of Volkswagen, other countries were annoyed and wanted to prosecute the company for violating the sustainability concept.

Sustainability frameworks

Some irregularities can be eliminated, depending on the validity and integrity of the data provided by an organization. The Greenhouse Gas (GHG) Protocol is another accounting tool that enables governments and businesses to understand, measure and manage their greenhouse gas emissions. The content of the ISO 26000 guidelines is very similar to the aspects included in the GRI reporting guidelines.

Reporting requirements in different countries

Other mandatory reports include the Quoted Companies GHG Reporting, British Companies Act, UK Corporate Governance Code, Climate Change Act and the Carbon Reduction Commitment (CRC) (Fogelberg et al., 2013:77). Voluntary requirements include the Environmental Reporting Guidelines and Best Management Sustainable Guidelines, all based on the GRI guidelines. Voluntary guidelines include the Guidelines on Environmental Information in the Director's Report section of the Annual Report (Fogelberg et al., 2013).

Reporting according to GRI G4 guidelines on ethics and integrity

The GRI allows a company to transition to the new guidelines and in effect requires all companies to report on the G4 guidelines from January 1, 2016. The core option contains the essential elements of sustainability reporting and the comprehensive option supports the core option by requiring disclosure of the company's strategy, analysis, governance, ethics and integrity (GRI, 2015b). To comply with G4-57 guidelines under the expanded option, the company must indicate: whether internal or external mechanisms for seeking advice on ethical and lawful conduct are available to stakeholders; whether a senior-level position has been made available for someone to assume responsibility for guidance-seeking mechanisms; whether all stakeholders were aware of the mechanisms for seeking advice; whether the mechanisms are available in different languages;

To comply with the G4-SO5 guideline under specific disclosure standards, the company must provide: information on the number of confirmed corruption cases; a report on actions taken against guilty persons or parties; and a report on any lawsuits filed against the organization. When preparing the report, the company must separately identify the total number of confirmed incidents, as well as the nature of these incidents. Required information includes legal department records of cases brought against the organization or employees or business partners, minutes of disciplinary action taken, and contracts with business partners (GRI, 2015a).

Research objective and research design

Results

53 percent of the companies indicated that the search for advice was handled confidentially. Nineteen of the twenty companies indicated that there were mechanisms available for stakeholders to report any concerns regarding the company's integrity. 58 percent of the companies indicated that the mechanism was independent of the company.

Conclusions

Half of the companies indicated that a designated employee was given responsibility for the advice-seeking mechanism. Some companies indicated that the same mechanisms were used for both seeking advice and reporting concerns. Less than half of companies reported having an anti-retaliation policy.

Recommendations

It was also noted that none of the companies in Japan, South Korea or Sweden reported conducting corruption risk assessments. Companies in Germany disclosed more information about corruption incidents than in any other country. The current state of sustainability reporting by smaller S&P 500 companies: what companies are choosing to disclose.

Faculty reluctance to report student plagiarism: A case study

Process

- Background to the case

- The hearings and beyond

The final unanimous decision of the members of the Ethics Committee (from which Professor X recused himself) was to recommend that the Dean of the Faculty refer these cases to the Academic Integrity Unit (AIU) for disciplinary proceedings. The dean of the faculty showed visible support for the process by attending all hearings. Professor X's participation in the various senior ethical structures of the university has resulted in the cases achieving high and undeniable visibility in the highest structures.

Insights

During the period beginning when the cases were first reported to AIU until the conclusion of this case, Professor X sent or forwarded approximately 161 email messages related to these cases. In total, the total administrative time involving members of the faculty administration, the dean, and Professor X in handling these cases was approximately 200 hours, of which approximately 140 hours related to Professor X's time alone. The third insight relates to delayed processes. administrative actions of the University that prevented the timely completion of the investigations.

Recommendations and conclusion

Within this reflection, the insidious practices that have been unthinkingly incorporated from business into universities must be identified and brought up for discussion in the light of universities' obligations to shape the development of future leaders (Osiemo, 2012). The awareness of the personal and institutional issues raised in this paper can make those in leadership, teaching and administrative positions in universities aware of factors that can be taken into account if student plagiarism is to be addressed. New managerialism and higher education: The management of performance and cultures in universities in the United Kingdom.