The research was conducted in the eThekwini region of KwaZulu Natal; A sample of 120 department employees was randomly selected and 91 responses were received (76% response rate). An overwhelming majority agreed that the ministry is a victim of fraud perpetrated by greedy and unethical employees.

M OTIVATION FOR S TUDY

P ROBLEM S TATEMENT

R ESEARCH Q UESTIONS

R ESEARCH OBJECTIVES

L IMITATIONS OF THE S TUDY

O UTLINE OF THE S TUDY

I NTRODUCTION

In South Africa, the Ministry of Public Health remains the sector most targeted by fraudsters (Talane, 2013). Despite the government prioritizing fraud by enacting various legislations, creating Chapter 9 institutions, intervening politically and fighting fraud at the National Department of Health (DOH), these are all an important and very expensive exercise (Nxumalo, 2010).

F RAUD S TATISTICS

According to Public Service Commission (PSC) statistics on fraud in the public sector, the government lost about R1 billion in 2011/2012 and about R130.6 million in 2006/2007 to fraud. A press release dated 25 November 2015 from the Office of the Auditor General of South Africa (AGSA) highlights the challenge facing the government.

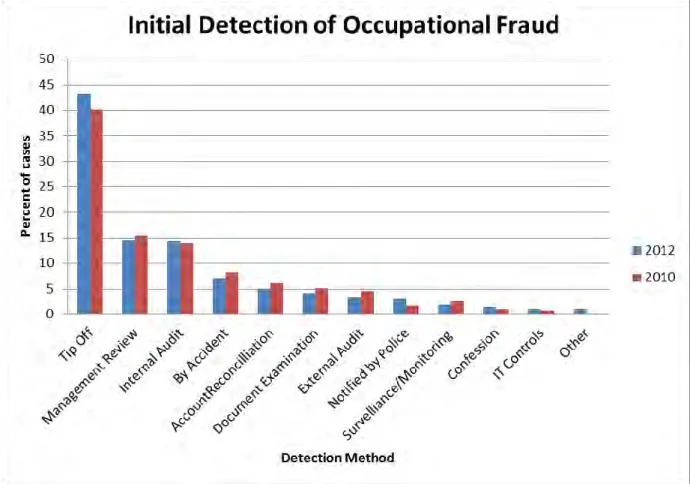

D ETECTION OF FRAUD

It said the findings of the 2014/2015 national and provincial department audit report revealed an irregular expenditure of R25.7 billion. Eight out of the 16 departments in KZN received clean audits, an increase from only six departments in 2013/2014.

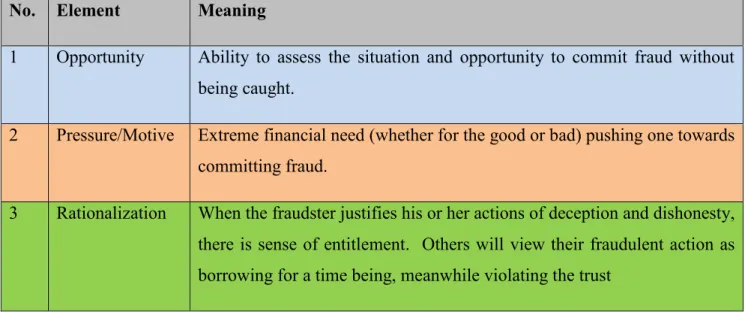

F RAUD THEORIES

Fraud triangle

His study, which slightly disagreed with Sutherland's, concluded that embezzlement by employees was not necessarily illegal (Cressey, 1953). Cressey (1953) concluded that there are three basic factors that lead to "breach of trust."

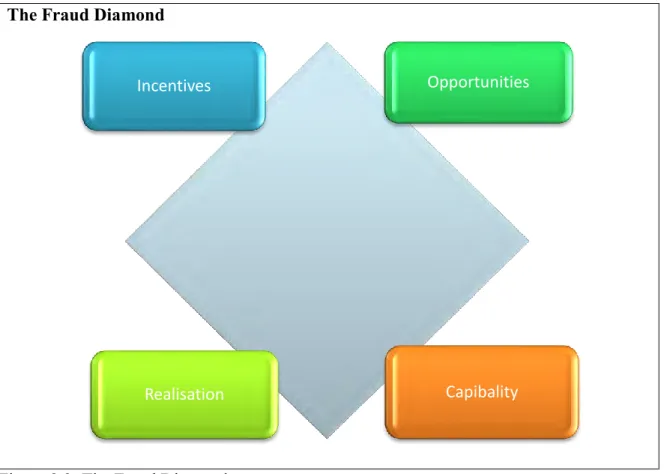

The fraud diamond concept

To achieve this, they will need staff with knowledge on how to identify the characteristics of those who commit fraud.

T HE TWO MAIN FRAUD THEORIES

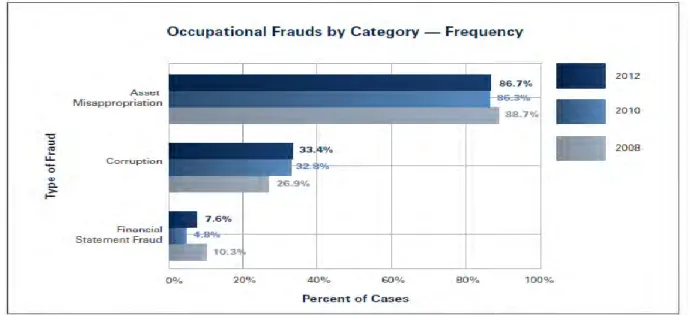

Occupational Fraud

They contribute significantly to any financial and reputational damage to the company because their goal is to steal, defraud and line their pockets to the detriment of the organization (Beigelman and Bartow, 2012). In recent times we have witnessed the collapse of large companies such as Enron, Tyco, Worldcom and Aldelphia.

Corporate fraud

Fraud was so prevalent in the United States (US) in early 2002 that former President George W. Bush, realizing that fraud was a problem, made corporate accountability a central element of his administration along with the war on terror . (Beigelman and Bartow, 2012).

F RAUD R ISK M ANAGEMENT

Fraud Prevention

Strong and committed leaders are integral to the success of fraud prevention and internal control programs. Fraud prevention strategies should educate their employees about these values regardless of the positions they hold (Beigelman and Bartow, 2012).

F RAUD R ISK A SSESSMENT (FRA)

Organizations that have a strong culture of fraud prevention programs and good internal controls are sure to enjoy a better and superior competitive advantage. A culture of compliance must be embraced by all stakeholders in the organization (Goldman and Kaufman, 2010).

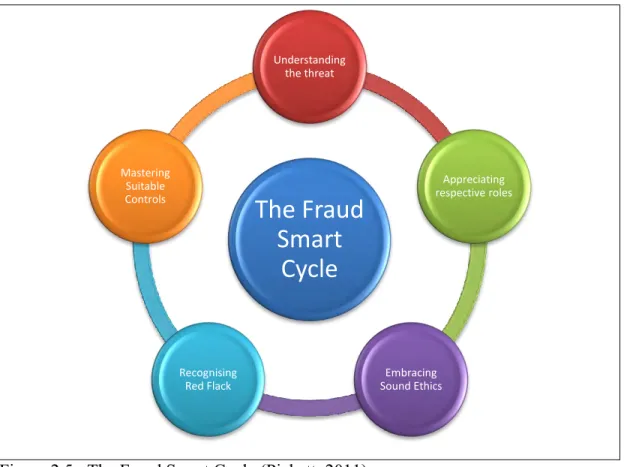

F RAUD S MART ORGANISATION

- Understanding the threat

- Appreciating respective roles

- Embracing sound organisational codes of ethics

- Recognizing red flags

- Mastering suitable controls

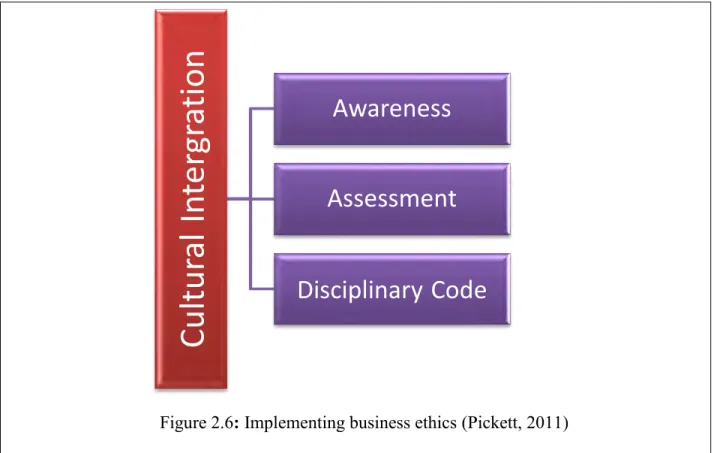

The last group are those who can help the company fight fraud and can learn more about the impact of fraud in the organization (Pickett, 2011). An organization must therefore know the internal and external threats it faces through its comprehensive fraud risk management strategies. Evaluation: After implementing an organization's code of ethics, management must continue to evaluate whether the efforts made have been successful.

P UBLIC SERVICE FRAUD RISK MANAGEMENT

National government frameworks

In addition, they also came up with a fraud risk management policy aimed at national and provincial departments, constitutional institutions, public bodies, provincial bodies, municipalities (metropolitan, local and district administration). As mentioned in the introductory chapter, the challenge facing public and even private entities is measuring the efficiency and effectiveness of their fraud risk management initiatives. He further states that fraud and corruption are very complex and that continued research in this area is necessary.

Kwa-Zulu Natal Department of Health

The few studies on corruption that have been conducted in South Africa do not address this phenomenon comprehensively and in detail. He states that these studies will remain incomplete unless they focus on certain factors such as the nature, causes, functions, financial costs, human costs of fraud and corruption and the role of the media, the historical context of South Africa and the never ending fight against corruption. Measuring the effectiveness and efficiency of FRM at the University of KwaZulu Natal The University takes fraud very seriously and has adopted a zero tolerance policy towards it.

The success of this intervention is measured by employee and management feedback. Reporting of suspected fraud is done on an independent line called Anonymous Tips. Proactive fraud detection is performed to find evidence of fraudulent transactions, identify environments vulnerable to fraud, and address the root causes of fraud.

I MPLEMENTATION

On this basis, special analytical tests of forensic data are carried out on the University's databases (eg employee master files against suppliers) to identify suspicious transactions. Where outliers are identified among the data, they will be analyzed to determine if a full-scale investigation is necessary (Sivnarain, 2013). In addition to these, all University divisions are subject to fraud risk assessments. e) Forensic investigations.

S UMMARY

We can conclude that perpetrators commit fraud because organizations relax their controls, allowing them to do so. Employees and customers pose a significant threat to organizations due to their role in committing fraudulent acts. To achieve this, extensive controls aimed at preventing or combating fraud must be put in place (Epsley, 2008).

I NTRODUCTION

A IM AND O BJECTIVES OF THE S TUDY

S AMPLING TECHNIQUES

To identify areas susceptible to fraud (risk areas) and how more efforts and resources can be used to combat fraud constructively. The employees to respondents were not selected in any specific criteria, such as position, number of years with the department or level of education. Lohmann and Schmucher (2008) noted that the quality of a survey is dependent on the response rate during data collection.

P ARTICIPANTS AND LOCATION OF THE STUDY

D ATA COLLECTION METHODS

Section A: Question 1 to 6: Profile of respondents such as gender, age, level of education and role at work. Section C: Question 13 to 17: Respondent's opinion on the causes of fraud committed by employees (professional fraud) in the Department. Section D: Question 18 to 23: Respondent's knowledge about the existence of fraud risk management and other strategies used to combat fraud.

R ESEARCH D ESIGN AND M ETHODS

R ELIABILITY OF THE STUDY

V ALIDITY OF THE STUDY

It indicates the ability of the questionnaire to differentiate between individuals with reference to a future criterion. The feedback was based on the structure, the questions, the time taken and whether the questionnaire was comprehensible. The above process was carried out by the researcher to establish the validity of the instrument and the results were positive.

D ATA A NALYSIS

Estimated criterion validity: When the results from the instrument correlate or accurately predict some of the internal variables;. Prior to data collection, the researcher conducted a pilot test asking 12 random employees of the Department (including some in management) to complete the questionnaire and provide feedback. The questionnaire was also distributed and discussed among the researcher's colleagues and other fellow researchers to identify potential gaps and contradictions.

S UMMARY

I NTRODUCTION

S URVEY R ESPONSE R ATE E VALUATION

D EMOGRAPHICS OF THE RESPONDENTS

- Gender

- Age

- Educational level

- Respondent’s Divisions

- Work experience

- Job role

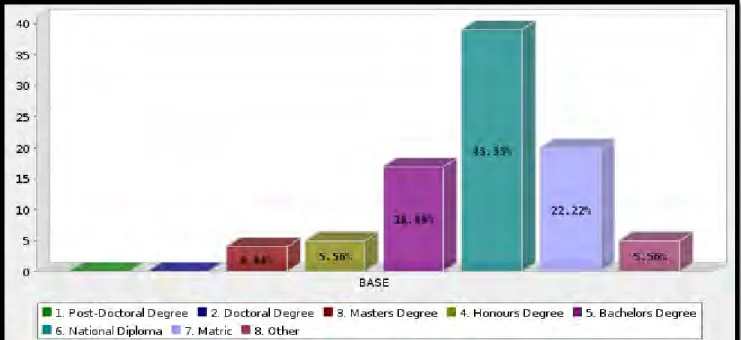

Age is an integral part of this study, figure 4.2 below illustrates the age of the respondents. The graph shows that 8% of the total respondents were between 20 and 25 years old. More than 57% of the total sample (52 respondents) have more than 5 years of work experience with the institute, while the rest have less than five years.

F RAUD R ISK M ANAGEMENT AT KZNDOH

- Fraud Risk Management concept

- Knowledge of Forensic Investigations Unit

- Concern with the level of fraud

- Problem with fraud

- Participation in the fraud awareness training

- Tip-Offs anonymous number

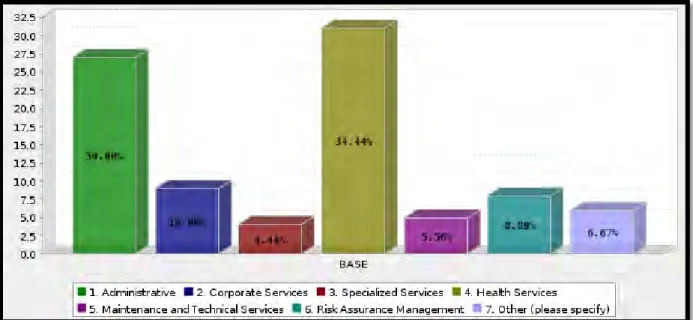

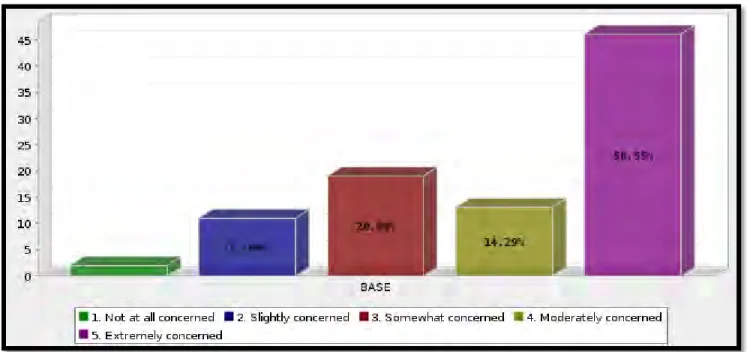

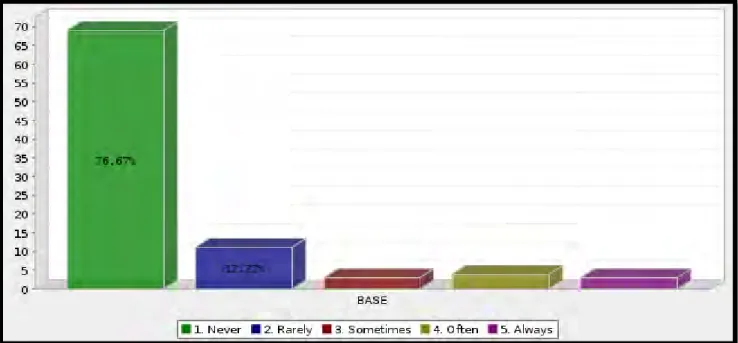

Thirty-two respondents (more than 35% of the sample) have other roles within the Department. concept, representing a total of more than 43% of the sample). Eleven respondents (12% of the sample) were slightly concerned, thirteen were moderately concerned and 19 were somewhat concerned about the level of fraud in the Department. The results show that more than 82% of the sample (73 respondents) have never participated in fraud awareness training while only 16 respondents (more than 17% of the sample) have participated in the same training.

O PINION ON THE CAUSES OF FRAUD COMMITTED BY EMPLOYEES

Department has been a victim of fraud committed by staff

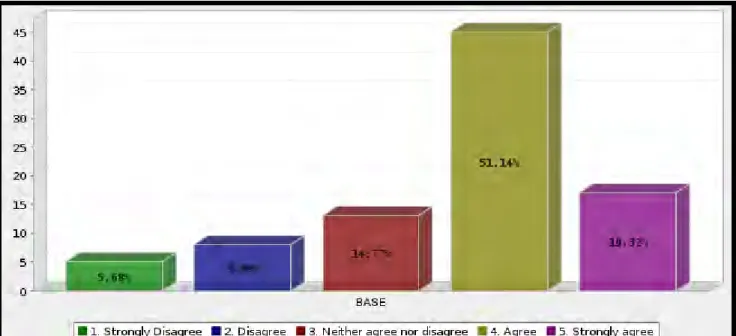

The results showed that 84% of the sample (70 respondents - consisting of 39 who agreed and 31 who strongly agreed) believe that the Department has been the victim of fraud perpetrated by staff members. Nine respondents (five strongly disagreed and four strongly disagreed), representing more than 8% of the sample, believe that KZNDOH has not been a victim of fraud perpetrated by staff.

Greedy employees commit fraud

Thirteen respondents (more than 14% of the sample) neither agreed nor disagreed, while five strongly disagreed and eight disagreed that unethical employees commit fraud. The results reveal that the majority of respondents, representing more than 69% of the sample (61 respondents, consisting of 39 who agreed and 22 who strongly agreed), believed that inadequate internal controls caused employees to commit fraud . 17 respondents (representing more than 19% of the sample) neither agreed nor disagreed, while only 10 respondents (consisting of two who strongly disagreed and eight who disagreed, representing more than 11% of the sample) believed that inadequate internal controls do not cause employees to commit fraud.

Poor ethical culture led to employees committing fraud

C URRENT FRM INTERVENTIONS

- Fraud risk training attended

- Fraud awareness campaigns

- Fraud risk on the intranet

- Types of fraud that might occur

- Awareness of the investigation findings

- Fraud hotline

Seventeen respondents (19%) have always been informed, while six respondents (7%) have rarely been informed about the types of cases that might arise. The above results show that 48 respondents (representing 53% of the sample) were never informed of the findings of fraud cases investigated by the ministry. At least three and six respondents (representing 10% of the sample) were often and always informed of the research results.

I NVOLVEMENT OF EMPLOYEES IN COMBATTING FRAUD

- Allegations to be investigated by internal staff

- Allegations of fraud to be investigated by consultants

- Strong internal controls prevent the occurrence of fraud

- Management is responsible for preventing fraud

- Auditors are responsible for preventing fraud

- Code of ethics of staff

- Department should provide a whistle blowing hotline for staff and other stakeholders to report

- Conduct regular surprise fraud audits

As shown in Figure 4.25, it appears that most respondents agree that the Department's investigations should be conducted by external parties (consultants). Approximately 81% of the sample (consisting of 37 respondents who agreed and 33 who strongly agreed) believed that it was management's responsibility to prevent fraud. As shown in Figure 4.28 above, approximately 69% of the sample (consisting of 32 respondents who agreed and 44 who strongly agreed) believed that it was the responsibility of internal auditors to prevent fraud.

S UMMARY

The results show that 84 respondents, consisting of 28 who agreed and 56 who strongly agreed, and representing more than 92% of the sample, believed that the Department should conduct regular surprise fraud audits. Three respondents (representing only 3% of the sample) neither agreed nor disagreed, while 3% neither agreed nor strongly disagreed about conducting a surprise fraud audit. The findings identified all the variables (negative or positive) needed to determine whether the current FRM in the Department is efficient and effective.

I NTRODUCTION

D ISCUSSION

- Demographics of the sample

- Objective One: To investigate whether the current fraud risk management strategies are

- Objective Two: To investigate employee’s knowledge of fraud risk management

- Objective Three: To establish employee involvement in the fight to combat fraud

- Objective Four: To investigate the effectiveness and efficiency of the Department’s current

- Objective Five: Help the Department in identifying areas that are susceptible to fraud (risk

The objectives of the department's fraud prevention plan are to involve all the employees in the fight to combat fraud within the department. Objectives B, C and D of the Department's fraud prevention plan emphasize how all employees must be part of the fight against fraud (Dlamini, 2014). Ultimately, the goal should be to ensure that all employees in the Department are aware of the various fraud risk strategies.

S UMMARY

I NTRODUCTION

R ECOMMENDATIONS

Consider developing a computer program that requires employees to read and answer questions about the department's fraud prevention plan. This exercise should be made mandatory for all employees and part of the department's annual performance management processes. This will demonstrate that the ministry is serious about taking decisive action against fraud, corruption and mismanagement.

L IMITATIONS OF THE S TUDY

R ECOMMENDATIONS FOR FURTHER RESEARCH

CONCLUSION

A Quick Guide to Fraud Risk Fraud Prevention and Detection, England and USA, Gower Publishing Limited. Available: http://www.corruptionwatch.org.za/why-is-corruption-getting-worse-in-South-Africa/ [Accessed 29 October 2015]. Available: www.corruptionwatch.org.za/no-accurate-stats-for-corruption-in-South-Africa/ [Accessed 20 September 2015].

ACFE Report on occupational fraud and abuse

Elements of fraud triangle

The fraud diamond

Occupational frauds by categories

The fraud smart cycle

Implementing business ethics

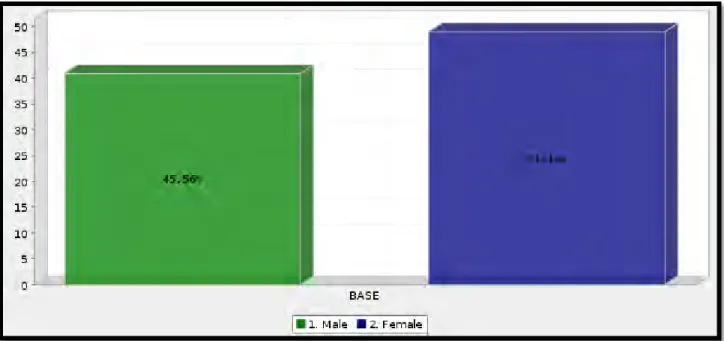

Gender of Respondents

Age of Respondents

Respondent’s highest level of education

Respondent’s division

Respondent’s number of years with the Department

Respondent’s job role

Fraud risk management concepts

Forensic Investigations Unit awareness

Concerns with level of fraud

Problem with fraud

Fraud awareness training

Tip-offs anonymous number

Victim of fraud committed by staff

Non ethical employees commit fraud

Inadequate internal controls

Poor ethical culture

Fraud risk training attended

Fraud awareness campaigns

Fraud risk on intranet

Types of fraud that might occur

Awareness of the investigation findings

Fraud hotline

Investigation to be investigated by the internal staff

Investigations to be conducted by a consultant (external entity)

Strong internal controls prevent the occurrence of fraud

Management is responsible for preventing fraud

Internal Auditors are responsible for preventing fraud

Whistle blowing hotline for staff and other stakeholders

Conduct surprise fraud audits often