Subject: Submission of Internship Report on “An Analysis of Credit Risk Management in Rupali bank Limited”. I am presenting my internship report on the topic “An Analysis of Credit Risk Management at Rupali bank Limited”. Under my guidance, she prepared her internship report titled “An Analysis of Credit Risk Management for Rupali Bank Limited.” It appears that the data and reports in this internship study are authentic.

Associate Head and Assistant Professor Department of Business Administration Faculty of Business and Entrepreneurship Daffodil International University. I am Omme Tanjila Deepa and I would like to thank the people who helped me all the way to complete my internship report "An Analysis of Credit Risk Management in Rupali bank Limited" At the absolute starting point, I have to thank God, i which is volatile the guidance helped me complete this assistant report. Arif Hassan, Associate Director and Assistant Professor of Daffodil International University, for providing me with all the key partners to complete this study.

One of the most profitable and modern state-owned banking financial institutions is among those restricted by Rupali Bank. The vision of Rupali Bank Limited is to be a leading financial institution and a leading contributor to the economy. The report preparation process is totally dependent on my 3 months internship program in minimum rupali bank.

The main objective of the report is to Credit Management Analysis of Rupali Bank Limited customer understanding to enhance the performance of rupali bank limited and analyze the financial performance related to credit management.

Introduction

Origin of The Study

Objectives of The Study

Methodology of the Study

Primary Sources

Secondary Sources

Scop of the Study

Limitation of the Study

- About Rupali Bank Limited

- Vision of Rupali Bank Limited

- Mission of Rupali Bank Limited

- Objectives of Rupali Bank Limited

- Products and services of Rupali Bank Limited

- Types of loan of what are offered by RBL

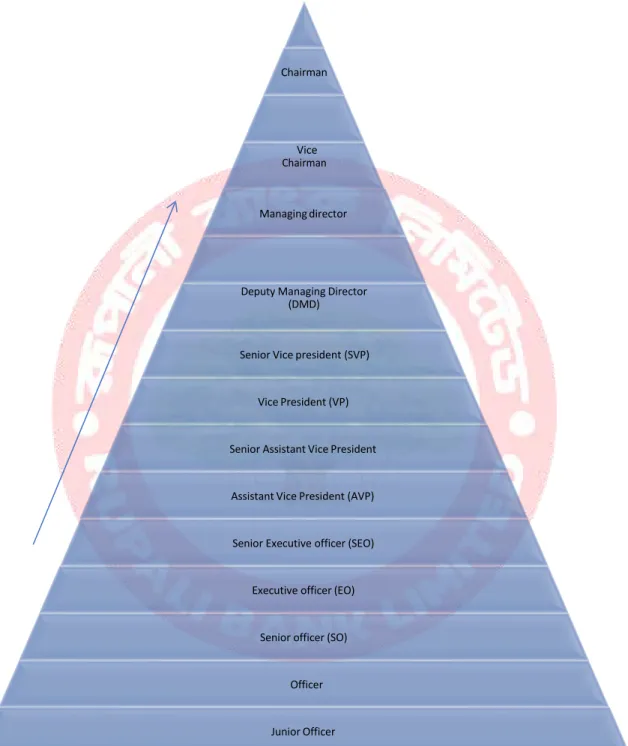

- Management Hierarchy of Rupali Bank Limited

To emerge as the country's main financial agency to finance private sector manufacturing projects and other projects with a significant effect on the country's economic growth. Uphold ethical values and meet the customer's financial needs in the fastest and most appropriate way and continue to innovate work to achieve human resources with superior qualities, technological infrastructure and service packages.

- Introduction

- Credit Risk

- Credit Risk Management System

- Credit Principles of Rupali Bank Limited

- Credit Facilities of Rupali Bank Limited

- Lending Criteria of Rupali Bank Limited

- Technical Viability

- Commercial viability

- Financial Viability

- Economic Viability

- Credit Evaluation Principles

- Different Types of Credit Facilities by RBL

- How Rupali Bank recover their Loan

- Problems in Loan Recovery

- Problems created by economic environment

- Problems created by government

- Problems created by the bank

- Overall Procedure for Sanctioning Loan

- Computation of Credit Risk Grading

The fundamental role of the bank is to build a channel by storing cash from the surplus unit and supplying borrowers with financing. Hazard is defined as the outcome of a risk (eg cost of damage) and the probability that this risk will occur. In other words, probability) x (hazard) = risk. This fundamentally increased the risk of CEO culture and created a standard for isolating the responsibilities and duties identified with the bank's credit department.

In accordance with the CRM Guideline, the head office's operational framework has been divided. Credit requirements integrate the general rules of the department administrator or credit officer granting credit into the part. Production liquidity means repayment on the due date or at short notice upon request.

A large part of the bank's salary is the difference between the premium earned on the drives and the premium charged in the trade, and unknown trade deals are often extremely profitable. Recruit Purchasing is a form of work credit where the hirer decides to take the goods at the expressed rent at the announcement, much of the client's repayment and excitement in a predetermined duration to change the advance. Advance consideration of the purchase of unknown cash against letters of credit (Back-to-Back) for installments where commissions do not occur before the date of the import installment.

To give the division supervisor more rights in the credit structure of the board's complex loop. Many of the time, difficulties could arise from the approval of advance measures, the analysis of the undertaking and the examination of the credits and so on, that is, the issue of advance recovery shows the effects of the default period of advance delivery. Banks often penalize credit to lose interest in the further development of the sector in question, but in other situations they struggle to make improvements. iii.

Rupali Bank often fails to adequately analyze the market risk of borrowers before lending, and the bank does not assume whether the business will flourish or fall flat. We should follow a few steps to have a factual limit of the danger to calculate the real risk associated with the advance that the bank will pay to the individual customer. To end, because of the small piece of the pie and the helpless growth of the market, this takes advantage of the chance of failure.

Risk that the bank may be exposed due to poor quality or strength of the security in case of default. These risk areas include assessing utilization of limits, account efficiency, borrower compliance with conditions/covenants and deposit ratios.

Financial Data Analysis

- Loan and Advance

- Loan to Deposit Ratio

- Standard Loan

- Sub-standard Loan

- Doubtful Loan

- Bad/Loss Loan

- Sector wise Distribution of Loan and advances

I have dissected some important information regarding RBL's credit activities from the previous five year report. When it is able to respond to the difficulties thrown by the earth and transform them into a preferred position, the true quality of an association is tested. Despite the falling borrowing cost pattern, the interest rate on private partial loans has generally been low despite us winning in the positive movement.

From the chart, it can be very well seen that RBL's full credit and advances are expanding as a direct result of their attractive and adaptable advance packages. The loan-to-deposit ratio applies to a bank's liquidity by measuring the bank's cumulative deposits with its total deposits over the same time period. If the ratio is too high, it means that the bank does not have enough capital to meet any unforeseen requirements of the store.

The graph shows that RBL's overall loan-to-deposit position is increasing due to their attractive and versatile loan packages. With regard to the segment provisions, these credit accounts are attractive and there is no delinquency. The above table shows that their sub-par loan growth in 2019 is 59%, which is higher than other years.

This proposal includes where there are still questions about the full recovery of the credit and advances close to a tragedy are expected anyway cannot be quantified at this stage. Bad/Loss Loan is a special credit and advance decline in this class, as it appears that even if all the protection is exhausted, this advance and advance is not recoverable or worthless. From the above graph, it represents that the total bad/loss loan and its growth rate was fluctuating.

The graphic presentation above reflects that RBL maintained a balanced approach to lending to various industrial sectors and enjoyed a fair share of RMG and textile industry business. Loans in small and medium-sized enterprises dominated the total loan portfolio in RBL, which amounted to 30.00%, and loans in Agriculture stood at 5.00% of the total outstanding loans.

Findings of the Study

Although RBL's bank loan has also increased year-on-year and the ratio stood at 55.52% in 2015, it is the lowest in five years.

Recommendation

Conclusion