Managing Electronic Media

Making, Marketing, and Moving Digital Content

Joan Van Tassel

Lisa Poe-Howfield

AMSTERDAM•BOSTON•HEIDELBERG•LONDON NEWYORK•OXFORD•PARIS•SANDIEGO SANFRANCISCO•SINGAPORE•SYDNEY•TOKYO

Nopartofthispublicationmaybereproducedortransmittedinanyformorbyanymeans,electronicormechanical, includingphotocopying,recording,oranyinformationstorageandretrievalsystem,withoutpermissioninwritingfromthe publisher.Detailsonhowtoseekpermission,furtherinformationaboutthePublisher'spermissionspoliciesandour arrangementswithorganizationssuchastheCopyrightClearanceCenterandtheCopyrightLicensingAgency,canbefound atourwebsite:www.elsevier.com/permissions.

ThisbookandtheindividualcontributionscontainedinitareprotectedundercopyrightbythePublisher(otherthanas maybenotedherein).

Notices

Knowledgeandbestpracticeinthisfieldareconstantlychanging.Asnewresearchandexperiencebroadenourunderstanding, changesinresearchmethods,professionalpractices,ormedicaltreatmentmaybecomenecessary.

Practitionersandresearchersmustalwaysrelyontheirownexperienceandknowledgeinevaluatingandusingany information,methods,compounds,orexperimentsdescribedherein.Inusingsuchinformationormethodstheyshouldbe mindfuloftheirownsafetyandthesafetyofothers,includingpartiesforwhomtheyhaveaprofessionalresponsibility. Tothefullestextentofthelaw,neitherthePublishernortheauthors,contributors,oreditors,assumeanyliabilityforany injuryand/ordamagetopersonsorpropertyasamatterofproductsliability,negligenceorotherwise,orfromanyuseor operationofanymethods,products,instructions,orideascontainedinthematerialherein.

Library of Congress Cataloging-in-Publication Data VanTassel,JoanM.

Managingelectronicmedia:making,marketing,andmovingdigitalcontent/JoanVanTassel,LisaPoe-Howfield. p.cm.

Includesbibliographicalreferencesandindex.

ISBN978-0-240-81020-1(pbk.:alk.paper)1.Massmedia—Management.I.Poe-Howfield,Lisa.II.Title. P96.M34V362010

302.23—dc22

2009052491

British Library Cataloguing-in-Publication Data

AcataloguerecordforthisbookisavailablefromtheBritishLibrary. ISBN:978-0-240-81020-1

ForinformationonallFocalPresspublications visitourwebsiteatwww.elsevierdirect.com

101112131454321

PrintedintheUnitedStatesofAmerica

iii

Contents

INTRODUCTION AND ACKNOWLEDGMENTS ... ix

CHAPTER 1 The Media Industries: Segments, Structures, and Similarities ... 1

Chapter Objectives ...1

Introduction ...1

Structure and Characteristics of the Media Industries ...3

A Day in the Life of Craig Robinson ...18

Common Characteristics of the Segments of the Media Industries ...20

Summary ...25

What’s Ahead ...25

Case Study 1.1 Media Expansion ...25

Case 1.2 Planning Ahead for Success ...26

References ...26

Internet Resources ...28

CHAPTER 2 Media Organizations ... 29

Chapter Objectives ...29

Introduction ...29

Defining an Organization ...31

Organizational Information Flows ...32

A Day in the Life of Lloyd Kaufman...40

Organizational Processes and Workflows ...43

Economic Factors That Affect Enterprises in the Creative Industries ...51

The Organizational Context: Economic and Social Factors ...53

Summary ...54

What’s Ahead ...55

Case Study 2.1 Media Organizations ...56

Case Study 2.2 The Meaning of Media Convergence ...57

CHAPTER 3 Leadership and Management ... 61

Chapter Objectives ...61

Introduction ...61

Defining Leadership: Doing the Right Thing ...62

Approaches to Leadership ...63

Videogame Mogul: Nolan Bushnell ...64

Movie Mogul: Walt Disney ...66

TV Mogul: Brandon Tartikoff ...67

Movie Mogul: Irving Thalberg ...69

New Meta Approaches to Leadership ...70

Digital Mogul: Steve Jobs ...71

TV Mogul: Ted Turner ...72

Linking Leadership and Management: Motivation ...74

Digital Mogul: Mark Cuban...76

Defining Management: Doing Things Right ...77

Leadership and Management in the Creative Industries ...84

Movie Mogul: Sherry Lansing ...84

TV and Movie Mogul: Lew Wasserman ...86

Summary ...87

What’s Ahead ...87

Case Study 3.1 How Would You Lead? ...87

Case Study 3.2 Leadership Observations ...87

References ...88

CHAPTER 4 Managing Human Resources ... 91

Chapter Objectives ...91

Introduction: People Who Need People ...91

Human Resources Strategies ...95

Different Strokes for Different Workers ...97

Employees ...97

Guilds and Unions ...103

Contract Workers ...107

Partners ...108

Vendors ...109

Summary ...110

What’s Ahead ...110

Case Study 4.1 Meeting with a Human Resource Professional ...111

Case Study 4.2 Conducting the Interview ...111

CONTENTS v

CHAPTER 5 Financial Management ... 113

Chapter Objectives ...113

Introduction ...113

Structures for Managing Finances ...115

Fundamental Financial Concepts ...115

Key Financial Statements ...119

Financial Responsibilities in the Age of Sarbanes-Oxley ...125

A Day in the Life of Sam Bush ...126

Financial Management Systems ...129

Managerial Finance: Strategic Planning and Budgeting ...129

Financial Strategies ...134

Summary ...139

What’s Ahead ...139

Case Study 5.1 Performance Reports ...140

Case Study 5.2 Setting the Budget ...140

References ...140

CHAPTER 6 Media Consumers: Measurement and Metrics ... 143

Chapter Objectives ...143

Audiences: Consumers and Customers, Viewers, Listeners, Readers, Users, Players, Friends, and Followers. ...144

Research and Content ...145

A Day in the Life of Debbie Carter ...148

Identifying Market Segments ...150

Summary ...170

What’s Ahead ...171

Case Study 6.1 Audiences and Programming ...171

References ...172

CHAPTER 7 Managing the Production Process ... 175

Chapter Objectives ...175

Introduction ...175

The Many Languages of Digital Creation ...178

Traditional Production ...179

A Day in the Life of Ann Marie Gillen ...188

Videogame Production ...190

Media Asset Management, Digital Asset Management, and Content Management ...192

Organizationally Generated Content ...197

User-Generated Content ...198

Summary ...199

What’s Ahead ...199

Case Study 7.1 The Producer ...200

Case Study 7.2 The Game Developer ...200

Key Terms ...200

References ...201

CHAPTER 8 Strategies for Marketing Content ... 203

Chapter Objectives ...203

Introduction ...203

Marketing Management and Managing Marketing ...206

A Day in the Life of Dorothy Hui...209

Marketing Strategies ...211

Integrated Marketing Communications (IMC): Reaching Across the Wire and the Ether ...211

Defining the Market ...216

Universal Marketing Appeals: The New, the First, the Only, and the New and Improved ...219

Summary ...220

What’s Ahead ...220

Case Study 8.1 The Road to Marketing a Newscast ...220

Case Study 8.2 3, 2, 1 … Launch of a New Web Site ...221

References ...221

CHAPTER 9 Packaging, Repackaging, and Marketing Content ... 223

Chapter Objectives ...223

Introduction ...223

Defining the Content Product ...224

Channel Marketing ...231

A Day in the Life of Elliot Grove ...232

Pricing Strategies: We Do Windows ...239

Summary ...241

What’s Ahead ...241

Case Study 9.1 Details, Details ...241

Case Study 9.2 You Package the Goods ...242

References ...243

CHAPTER 10 Managing Sales: An Insider’s View ... 245

Chapter Objectives ...245

Introduction ...245

CONTENTS vii

A New Approach to Selling Media ...250

A Day in the Life of Wendy Y. Shelton ...256

Summary ...266

What’s Ahead ...267

Case Study 10.1 CNA (Customer Needs Analysis) ...267

Case Study 10.2 The Pitch ...268

References ...269

CHAPTER 11 Distributing Content ... 271

Chapter Objectives ...271

Introduction ...272

Distribution Revolution...273

Bricks and Clicks ...277

A Day in the Life of Valerie Geller ...283

Wired Digital Bitpipes ...288

Wireless Bitpipes ...293

Content Management: Transcoding Content into Different Formats for Distribution ...297

Digital Rights Management ...299

Summary ...301

What’s Ahead ...301

Case Study 11.1 Create Your Own Digital Assembly Line ....301

References ...302

CHAPTER 12 The Changing Media Value Chain ... 305

Chapter Objectives ...305

Introduction: New Markets, New Models, New WWWorld ...305

The Digital Value Chain ...306

The Changing Value Chain ...312

A Day in the Life of Richard Conlon ...316

Disruptive Innovations ...318

Industry Responds to the Technological Challenge: Value Chain Systems ...321

Summary ...322

What’s Ahead ...323

Case Study 12.1 A Case of “B and C” ...323

References ...323

CHAPTER 13 Media Industry Business Models ... 325

Chapter Objectives ...325

Introduction: Business Plans and Models ...325

A Day in the Life of Bob Kaplitz ...341

Marketing Models ...344

Distribution Models ...349

Revenue Models ...349

A Day in the Life of Vivi Zigler ...361

Summary ...363

What’s Ahead ...364

Case Study 13.1 Back to the Future ...364

References ...365

CHAPTER 14 Legal and Regulatory Issues ... 367

Chapter Objectives ...367

Federal Laws and Regulations ...370

State ...379

Local ...380

A Day in the Life of Brad Williams ...380

Cycles of Regulation ...382

International Media Regulations ...383

Summary ...383

Case Study 14.1 News for Sale ...384

References ...385

CHAPTER 15 Ethical Issues ... 387

Chapter Objectives ...387

Follow the Law? ...390

Follow a Code of Ethics? ...392

Thinking Ethically: Introducing the Potter Box ...393

Practical Perspectives on Ethics ...402

Ethics and User-Generated Content ...406

Summary ...407

Case Study 15.1 A Piece of Advice ...408

References ...409

ix

Introduction and Acknowledgments

For almost 15 years, I wrote for the Special Issues section of theHollywood Reporter,writingabouttheeffectsofdigitaltechnologiesonthemediaindus

-tries.Inthecourseofthatreporting,Iinterviewedvirtuallyalloftheexecutives whowereguidingthemajormediaandentertainmentcompaniesthroughthe choppywatersofanewmedialandscape.Theywerecalledupontoaddress the changes brought about by the introduction of digital content creation technologies – cameras, nonlinear editing, computer-generated imagery for animationandspecialeffects,theInternetandpeer-to-peernetworks,andthe proliferationofchannelsandmediaplayers,suchasmobile,gameconsoles, DVRs,HDTV,Blu-ray,andalltheotherrapidlychangingconsumerelectronics devices.

Notsurprisingly,theripplesofchangesintechnologysoonreachedthepublic, whicheagerlyadoptedmanyofthenewwaystoconsumemedia,changingtheir mediausesandhabits.Theyalsosentunceasingtidesofchangethroughthe mediaindustryitself,withwhichmanagersateverycompanyandeverylevel hadtodeal.Itwasatrulychaoticbusinessenvironment–asneezeinChicago maynotcauseatsunamiinBeijing,butcomputerprocessorsinSanJosecer

-tainlycausedatsunamiinthemediaindustrythathaslastedforlongerthan twodecades.

Digitalcontentcreationchangedthespeed,flexibility,andcostofcontentpro

-duction,makingitcheaperforconsumers,butsometimesmoreexpensivefor blockbustersloadedwithspecialeffects,suchasTitanic.Networkeddistribu

-tion enabled media companies to employ skilled creators from around the world,openedupglobalmarketforcontentproducts,andgreatlyloweredthe costofsendingmediatoallcornersoftheglobe.Italsoenabledconsumers tosendmediafilestoallthosesamecorners,undercuttingexistingbusiness practicesandvaluablesourcesofrevenue.

isindevelopmentaroundtheworld.Theuniversitiesandgovernmentsofmany countries are connected to it, and scientists and engineers are hard at work buildingthetechnologiesneededforitsintroductionandpublicadoption. Thepurposeofthisbookistolayafoundationforunderstandingandpartici

-patingintheongoingevolutionofthemediaindustry.Itprovidestheconcepts andvocabularythatmanagershavedevisedtomeetthechallengesoftoday’s market and to position their organizations to succeed in a dynamic future businessenvironment.Atthesametime,managersrelyonmanytraditional ideasandprocessestoguidetheiractions.Insomeways,mediabusinessesare notsodifferentfromhowtheywereinthepast,orisolatedfromthepractices thatgovernmodernbusinesseseverywhere.

Thebooktriestokeeponefootintherecentpast,anotherinthenearfuture, withoutlosingsightofthepresent,whichdemandsknowledgeofbothpast andfuturedimensions:

•■ Chapter1introducesstudentstothemediaindustries–theirsize,

structure,segments,androleinsociety.

•■ Chapter2looksatmediaorganizations,whattheydo,andhowthey

createvaluetobesuccessfulandprofitable.

•■ Chapter3examinesleadershipandmanagementtechniques,withbrief

biosofthebusinessaccomplishmentsofmediaindustrymanagers.

•■ Chapter4detailshowmediacompanieshandlehumanresources,in

industriesthatarehighlydependentonskilledcreativepeople.

•■ Chapter5showsstudentshowtofollowthemoney,givingtheminsight

intothepervasiveimportanceinmediaindustryorganizationoffinancial planning,budgeting,andmanagement.

•■ Chapter6exploresthenewparadigmofmediaconsumers,whomaybe

customers,viewers,listeners,readers,users,players,friends,andfollowers, dependingonwhichmediasegmentanexecutivemanages.

•■ Chapter7discussestherevolutioninmediacontent,includingtraditionaland

newmeansofproduction,contentacquisition,anduser-generatedcontent.

•■ Chapter8presentstheBigPicturestrategiesformarketingmediacontent,

attheheartoforganizationalgrowthandprofitability.

•■ Chapter9getsintothedetailofmarketing–readyingcontentproducts

andshapingthemtosucceedinthemarketplace.

•■ Chapter10coverssalesmanagement,akeyfunctioninanyorganization,

wheretherevenuesflowintothecashregister.

•■ Chapter11laysoutthenewworldofcontentdistributionascompanies

maintainthetraditionalmeansofdeliveringcontenttoconsumers,even astheytrytoseizetheopportunitiesofferedbydigitalchannels.

•■ Chapter12considersthelanguageofconductingmediabusiness,

xi

Acknowledgments

•■ Chapter13presentsever-evolvingmediaindustrybusinessmodelsthat

serveasashorthandwayofdescribingtheproductsthebusinesswill bringtomarketandhowitwillattractconsumers.Thebusinessmodel alsoincludeshowtheorganizationwilldelivertheproductorserviceand deriverevenuefromit.

•■ Chapter14providesanoverviewofthelegalandregulatoryissuesthat

affectmediaenterprisesthatoperateinbothU.S.andinternationalmar

-kets,includingthenewfrontieroftheInternet.

•■ Chapter15askssomeofthemostdifficultquestionsthemediaindustries

face:theethicalconsiderationsbroughtupbytheirinfluentialroleinthe publicsphereandprivateconsciousnessofindividuals.

Some readers may want to know why there is no chapter – perhaps even several chapters – specifically looking at communication technologies. To some extent, these topics are covered in Chapter 11, in the discussion of distributing content. The distribution infrastructure – wired and wireless networks–figuresolargeinallourlivesthatsuchatopicdeservesitsown booktoestimatethelikelyfuturegrowthandcapacity.Suchprojectionsare more or less impossible for consumer devices. There are probably college studentsatworkintheirgaragesanddormsrightnowfiguringoutsomenew fabulous way to consume content that no one has ever thought of before andwillturnsomepartofthemediaindustryupsidedown.Ilookforward totheirproductsandtheenchantingcreationsthatwillfollow,butIwillnot attempttoguesswhattheymightproduce!Indeed,ifIcould,Iwouldbeout inmyowngarage.

ACKNOWLEDGMENTS

Joan Van Tassel

I want to thank so many people for their help, guidance, and patience as I wrote this book. First and foremost, Elinor Actipis and Michele Cronin at FocalPressdeservemedalsfortheirforbearanceandkindnesstomeasIwrote thisbook.Iadmirethemandcannotexpressentirelymygratitudetothem, excepttosayaheartfelt“Thankyou.”Iamalsoindebtedtotheskilledcopy editingofNancyKotary.

Tomyco-authorLisaPoe-Howfield,Iextendmyappreciationforherknowl

-edge,willingness,andcreativity.Shehasbeenastalwartcompanioninthispro

Todd Chambers, John Allen Hendricks, and a reviewer who wished to be anonymoushaveimprovedthebookfarbeyondwhatitwouldhavebeenwith

-outtheirgenerousassistance.

Anauthor’sfamilyalwayspaysaprice,includingmysiblings,ElaineBaerand Nancy,Gordon,Karen,Bailey,Emmy,andLucilleVanTassel.RobertandIrene Newton, Mona Nasir, and my personal coach, star journalist Mary Murphy. Havealwaysbeenhugesupporters,too.Ilovethem,eachandeveryone. NationalUniversitycolleagueshavegivenmetime,encouragement,andsup

-portinthewritingofthisbook.Imustmentionmembersoftheadministra

-tion,DebraBean,PatriciaPotter,andKarlaBerry.Iwouldnotwanttoleave outmywonderfulfacultycolleagues:CynthiaChandler,LouisRumpf,Scott Campbell, Sara Ellen Amster, Sara Kelly, Roger Gunn, John Banks, Maureen O’Hara,andIsmailSebetan.

Finally,PeterClarkeandSusanEvansattheUniversityofSouthernCalifornia weremymentorsattheAnnenbergSchoolforCommunicationandcontinue toinspire,encourage,andhelpmetothisday.IrememberEverettRogers,a member of my dissertation committee when I was a graduate student, and alwaysregrethispassing.TheworldwithoutEvisalesserplace.ToRonRice, IwillalwaysbegratefulforhisdirectiongiventomeonthedayIdefendedmy dissertation:“Goforthandcommunicate.”Withthisbook,IhopeIhave.

Lisa Poe-Howfield

Firstandforemost!Inmymaidenvoyageascoauthor,Isendoutmyeternal gratitude,respectandthankstoJoanMarieVanTasselforprovidingmewith thisincredibleopportunity.Yourdedicationtoshareyourknowledge,notto mentionyourpatienceinwalkingmethroughtheprocess,servesasagreat inspirationtoall…thankyou!

ThankyoutoElinorActipisandMicheleCroninatFocalPressMediaforkeep

-ingmeontrackandprovidingjusttherightguidance.

Professionally,Ihavebeenblessedwithgreatrolemodelsinmylifeincluding JimandBeverlyRogers(OwnersofSunbeltCommunications);RalphToddre (PresidentandCOOofSunbeltCommunications);DesireeLong(Executive Assistant,KVBCTV3)andmydearfriendandformercolleague,JudyReich-Milby.Youhaveallinspiredmetogreaterheights-thankyou.

Sincere appreciation to those who contributed to our “Day in the Life” seg

xiii Day in the Life Features

Thankyouallfortakingtimefromyourbusyschedulestoshareyourreallife experiences.

Onapersonalnote,Igivethankstomyparents,AllenandPeggyPoe,who sacrificedmuchandworkeddiligentlytoprovidemewiththemeanstoobtain my college education at Pepperdine University and to my Mother-in-law, Margaret Howfield, who lost her battle with leukemia while this book was beingwritten,butleftalegacyoftruestrength.Averyspecialthankyouand muchlovetomyhusband,IanHowfield,andson,KyleRoot,whocontinually demonstrateincrediblesupportwiththeirkindwords,wittyhumorandpow

-erfulhugs–makingallthingspossible.

DAY IN THE LIFE

FEATURES

Day in the Life sectionfeaturetopmediaexecutivesandhighlighttheireveryday routines,showcasingsomeoftheirkeyconcernsandperspectivesontoday’s media.Eachsectionincludesabriefessayandadailyrundown.

Craig Robinson – President and General Manager, KNBC/TV-Los Angeles, California(Chapter1)

Lloyd Kaufman –Co-FounderandPresidentofTromaEntertainment;Chair

-manoftheIndependentFilm&TelevisionAlliance(IFTA);authorofDirect Your Own Damn Movie, Produce Your Own Damn Movie, andMake Your Own Damn Movie(Chapter2)

Sam Bush –SeniorVicePresidentandChiefFinancialOfficerofSagaCom

-munications,Inc.(Chapter5)

Debbie Carter – Vice President and Director of Sales for Blair Television (Chapter6)

Ann Marie Gillen –CEOandFounderoftheGillenGroup,LLC;FilmPro

-ducer&EntertainmentIndustryConsultant(Chapter7)

Dorothy Hui –VicePresident,PartnershipMarketing&Sales,Wind-upRecords (Chapter8)

Elliot Grove –DirectorandFounderoftheRaindanceFilmFestivalandthe BritishIndependentFilmAwards;authorofRaindance Writers’ Lab and Rain-dance Producers’ Lab(Chapter9)

Wendy Y. Shelton – Sales Manager, KVBC TV-3 (NBC), Las Vegas, Nevada (Chapter10)

Richard Conlon – Vice President, New Media & Strategic Development - BroadcastMusic,Inc.(BMI)(Chapter12)

Bob Kaplitz – Principal and Senior Station Strategies for AR&D, author of

Creating Execution Superstars with Budgets Cut to the Bone(Chapter13)

Vivi Zigler –PresidentofNBCDigitalEntertainment(Chapter13)

1

C H A P T E R 1

The Media Industries: Segments,

Structures, and Similarities

INTRODUCTION

Movies, music, games, magazines, books, newspapers, Internet, comedy, drama,news–thismediacontentconstitutestheexcitingvisiblefaceofthe mediaworldthatthrillsandenthrallsaudiencesaroundtheworld.Manypeo

-ple have fantasies of being in the public eye as actors, singers, writers, and journalists,andafewofusgoontoperform.Butbehindthescenes,thereare manyrewardingcareersinthemediaindustriestodiscover,promote,support, andmanagealltheactivitiesthatmustbecompletedtobringthesewonderful workstolifeandtoaudiences.

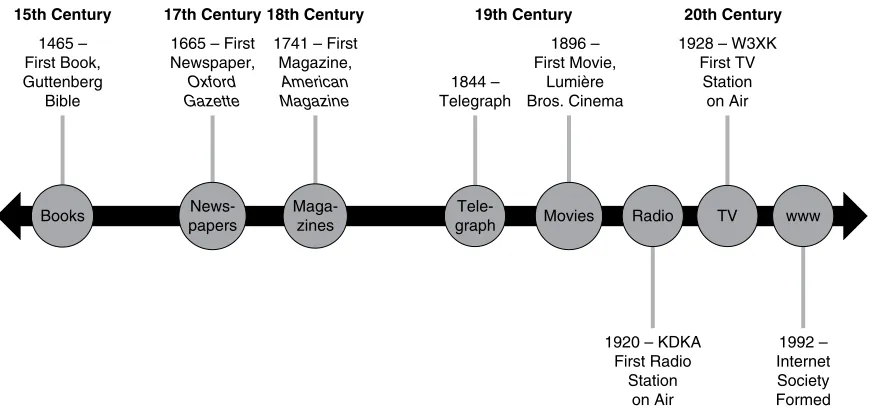

Thehistoryofelectronicmassmediaisshort.Theprecursors,booksandnews

-papers,havebeenaroundforseveralhundredyears,butthephenomenonof massmediaislessthan150yearsold.Electricity-basedtechnologieshavetheir rootsinthenineteenthcentury,butallemergeasmediaplatformsinthetwen

-tiethcentury,asshowninFigure1-1.

Don’t hate the media. Be the media.

Jello Biafra

Theobjectiveofthischapteristoprovideyouwithinformationabout:

■ Thestructureandcharacteristicsofthecontentindustries ■ Thesegmentsthatmakeupthecontentindustries

■ Thewiderangeofbusinesseswithinthesegmentsofthecontent

industries

■ Thechangingcultural,social,political,andeconomicconditionsthat

establishthebusinesscontextofthecontentindustries

CHAPTER OBJECTIVES

Chapter Objectives ...1

Introduction ...1

Structure and Characteristics of the Media Industries ...3

A Day in the Life of Craig Robinson ...18

Common Characteristics of the Segments of the Media Industries ...20

Summary ...25

What’s Ahead ...25

Case Study 1.1 Media Expansion ...25

Case Study 1.2 Planning Ahead for Success ...26

References ...26

Internet Resources ...28

CONTENTS

DOI: 10.1016/B978-0-240-81020-1.00001-4

Theshortlifetimeofelectronicmediameansthatthestructureofmediacom

-FIGURE 1-1 Timeline of mass media platforms

Movies Radio TV www

Books 1465 – First Book, Guttenberg

Bible

15th Century 17th Century 18th Century 19th Century 20th Century

1665 – First Newspaper,

Oxford Gazette

Structure and Characteristics of the Media Industries 3

Managersworkineverykindoforganization,industry,geography,nation,and society.Theirresponsibilitieshaveagreatdealincommon,whetherthetask ismanagingachemicalcompany,alargefarm,anot-for-profitsocialservice agency, or a music label. Yet each business enterprise and environment has itsowncharacteristicsthataffecthowmanagersconceptualizeproblemsand solutionsandhowtheycarryouttheirduties.

Theglamorousmediaindustriesarenoexception–evenroutine,predictable workcarriesthepatinaofthepowerandvisibilitythatsurroundstheseenter

-prises. Human resources hire personnel – sometimes performers like Sean Penn. Legal departments negotiate and approve contracts – sometimes for albums likeOK Computer by Radiohead. Business development units estab

-lish partnerships, finance and accounting departments handle payables and receivablesandimposeorganizationalcost-reductionprograms,andmarket

-ingteamstraversethecomplexwholesaleandretailchannelsthatfinallyput productsinthehandsofconsumers,forallproducedcontent–evenacompel

-linghitTVserieslikeHouse.

STRUCTURE AND CHARACTERISTICS OF

THE MEDIA INDUSTRIES

Itisagiventhatmanagerswillknowagreatdealabouttheindustryinwhich theywork.Theygetthatinformationfrommanysources.Somemediaenter

-prisesgatherandanalyzeinformationabouttheirconsumersandcustomers fromdirectcontact.Iftheydon’thaveinternalinformation,companiesreceive researchreportsthattellexecutivesabouttheiraudience,productperformance, andmarkets.Thereisalotofpublicinformationaswell,asthemediaarefre

-quentsubjectsofjournalisticcoveragethatreportonfinancial,technological, andculturalaspectsoftheindustry.Managersalsogainvaluableinformation fromtheirownpersonalexperienceswithbuyingandconsumingcontent. Anotherfactorthatinfluenceshowmanagersmakedecisionsistheimportance ofthemediainpeople’slives.Manyspendmoretimewatching,listening,and readingthemediathantheydoanythingelse,exceptbreathing.Addingupall ofthetimetheyengagewithmedia–wakingtothesoundoftheclockradio/ CDplayerandtelevisionset,checkingandrespondingtoemailthroughout theday,listeningtoacarradioandaniPod,watchingaportableDVD,play

-inggamesonmobilephones,surfingtheNet,andwatchingtelevisionbefore bed–theaveragepersonintheUnitedStatesspendsmorethan9.5hoursper daywiththemediaandwillspend$936.75peryearonmediaconsumption.2

Nineandahalfhoursismoretimethanmostpeoplespendsleeping!

Indeed,themediaconstituteapervasive,virtualenvironmentwhoseimpact sometimes seems to transcend even the physical world. Managers find that theirbusinesscanbeaffectedbythecontenttheyprovide–rememberJanet Jackson’s“wardrobemalfunction”?Itupsetmanyviewers,resultinginfinesfor thenetworkandelectronicbanishmentforJackson.

Industry Size and Composition

In2011,theglobalmediaindustrieswillaccountfornearly$2.0trillioninrev

-enue.3However,theyarepartofalargercommercialcomplex,calledthe copy-right industries.Theorganizationsthatmakeupthecopyrightindustriesengage inthe“generation,productionanddisseminationofnewcopyrightedmate

-rial.”4Thespecificcontentmaydiffer,butthemanagementoftheseactivities

isstrikinglysimilar,regardlessofthespecificindustrysegmentorenterprisein whichtheytakeplace.

Fourcomponentsmakeupthecopyrightindustries:

■ Core industries: Industrieswhoseprimarypurposeistocreate,produce,

distribute,orexhibitcopyrightedmaterials,includingbroadcast,music, motionpictures,entertainmentsoftware,newspapers,andmagazines,as showninFigure1-2.

■ Partial copyright industries: Industriesforwhichonlysomeaspect

orportionoftheproductsqualifyforcopyrightprotection,suchasthe FordMotorCompany,whosecarsmaybepatented,butnotcopyrighted. However,thebrochures,TVspots,andotherpromotionalmaterialsthe companyproducesarecopyright-protected.

■ Nondedicated support industries: Industriesthatprovidedistribution,

marketing,andsalessupporttothecopyrightedcontenteconomy,includ

-ingtransportationservices,telecommunicationsservices,wholesalers,and retailestablishments.Examplesofnondedicatedsupportindustriesare telephonecompaniesandInternetinfrastructuresthatprovidethetrans

-portnetworksforcontent.

■ Interdependent industries: Industriesthatmanufactureandsellprod

-uctsthatenablethecreation,production,distribution,orconsumptionof copyrightedmaterial.Suchindustriesincludemanufacturersofconsumer electronicsproductsandmedia–televisions,DVDplayers,gameconsoles, cameras,microphones,lightingequipment,discsandtape,headphones, andsoforth–thetechnologiesthatdependonthecopyrightindustries forcontentthatdriveconsumerstobuyplaybackdevices.

Mediacompaniesmakeupthelargestcomponentofthecorecopyrightindus

Structure and Characteristics of the Media Industries 5

radioprograms,andcomputersoftware(includingvideogames).Asshownin Figure1-2,thecopyrightindustriesareanimportantpartoftheU.S.economy andcopyrightedproductsarethelargestU.S.export.

InEurope,thecopyrightindustriesareequallyimportant.In2000,theycon

-tributedmorethanatrillioneuros(€1,200billion)totheEUeconomy–about

5.3percentofitstotalvalue.Andtheyemployedmorethan5millionpeople intheEuropeanUnion,constituting3.1percentofthetotalEUworkforce.5In

theUnitedKingdom,theimportanceofthecreationofcopyrightedmaterialis evengreater:creativeindustriesaccountfor8percentoftheeconomy.6

Althoughtherearemanymanagementjobsinthecoreindustries,theyalso existinlargenumbersinthesupportandinterdependentindustries.Thepar

-tialcopyrightcategoryisaninterestingonefortoday’sjobseekers.Thiscat

-egorycoversthemedianeedsofenterprisesthatofferproductsandservices inotherindustries:automobiles,clothing,cosmetics,fishinggear,restaurants, andcarwashingestablishments.Allthesecompaniesneedmaterialtocommu

-nicatetoconsumers,investors,andemployees.Increasingly,thesecommunica

-tionsincludevideoandaudio,whichrequiremoreexpertiseandmanagement supervisionthanprintmedia.7

Industry Segments

Peoplewhoworkinoneofthecopyrightindustrysegmentsusuallythinkof themselvesasbeinginthemusicbusiness,televisionbusiness,ormoviebusi

-ness. In other words, they identify with the specific segment they work for. Evenso,theyoftenknowquiteabitaboutothersegments,particularlythose thatarecloselyrelated,perhapsdrawingonthesamecontentortalentpool. Analystsbreakdownthemediaindustriesintosegmentsinseveralways.For thepurposesofthischapter,segmentsofthemediaindustriesincludefilmed

COPYRIGHT

A legal framework that applies to original works that reserves the right of copying to the creator. Different countries have different legal frameworks that define these rights in different ways with respect to duration, enforcement mechanisms, and penalties for violation. In the United States, copyright is constitutionally protected.

FIGURE 1-2 The core copyright industries

Motion Pictures

Radio & Television (Cable, Broadcast,

and Satellite)

Music Recording, CDs, Downloads

Entertainment and Business Software

Newspapers, Periodicals, and

entertainment, broadcast and cable television networks, television distribu

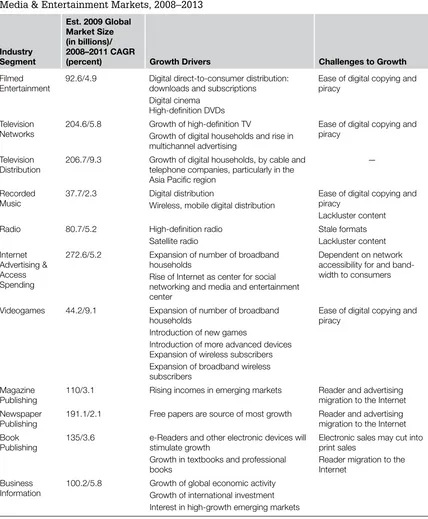

-tion,recordedmusic,radio,Internetadvertising,Internetaccess,videogames, book,newspaper,magazineandotherprintpublishing,andcorporatemedia. Thenextsectionswilllookatthesizeandstructureofeachofthesegments. Managers within each segment of the creative industries need to consider theparticularsoftheirorganizationandthemarketstheyface.Typically,the marketsarelarge,oftenglobalinscope.Insomethegrowthrate(CAGR,for compoundannualgrowthrate–seetheboxonthisterm)ishigh,inothers moremoderate.Table1-1describessomeofthedifferencesbetweencreative industrysegments.Inthetable,noticethatallthesesegmentsfaceasimilar formidablechallenge:theeaseofcopyingandlarge-scalepiracyinthedigital environment.

Filmed Entertainment

LosAngeles,NewYork,London,Paris,Mumbai,andHongKongaretheglobal centersoffilmedentertainment.Thecategoryincludesrevenuesreceivedfrom motionpictures,theaterboxoffices,rentalincomefromvideostores,salesin retailestablishments,andonlinesubscriptions(includingdownloadedfilms andTVprogramsandDVDssentthroughthemail).Thiscategorydoesnot includerevenuesreceivedfromdistributionviacable,satellite,telephonecom

-panies–allcoveredintheTVdistributionsegment.

Filmedentertainmentoccupiesaspecialplaceinthemediaindustry,because itdrivesrevenuesbeyondtheboxofficetomanydifferentbusinessesinthe mediaindustries.Forexample,whenamotionpictureissuccessfulatthebox office,itislikelytoattractDVDpurchasesandrentalsaswell.Itmayspawna sequel,prequel,orTVseries.Itscharactersmaybespunofftootherproperties. Ifthemovieappealstochildren,theremaybelucrativedownstreamlicensing opportunitiesforeverythingfromcalendarstobedsheetsandkeychainfobs. AhitTVshowopensupsomeofthesameopportunitiesandhastheadded advantageofrunningoveraperiodofyears.

CAGR

In business, compound annual growth rate describes changes in value over time, taking into account year-to-year changes. In media and entertainment industries, CAGR normally refers to revenues, but the formula applies to any asset. It is a more accurate measurement than simply saying, “revenues are expected to double over the next five years.” (When an industry is shrink-ing, the CAGR will be a negative value.) The formula to calculate CAGR is:

1 CAGR

Beginning Value Ending Value

1

# Years

-=d

d

Structure and Characteristics of the Media Industries 7

Table 1-1 Comparing Media Industry Segments. Based on PricewaterhouseCoopers Media & Entertainment Markets, 2008–2013

Industry Segment

Est. 2009 Global Market Size (in billions)/ 2008–2011 CAGR

(percent) Growth Drivers Challenges to Growth

Filmed Entertainment

92.6/4.9 Digital direct-to-consumer distribution: downloads and subscriptions Digital cinema

High-definition DVDs

Ease of digital copying and piracy

Television Networks

204.6/5.8 Growth of high-definition TV

Growth of digital households and rise in multichannel advertising

Ease of digital copying and piracy

Television Distribution

206.7/9.3 Growth of digital households, by cable and telephone companies, particularly in the Asia Pacific region

—

Recorded Music

37.7/2.3 Digital distribution

Wireless, mobile digital distribution

Ease of digital copying and piracy

Lackluster content Radio 80.7/5.2 High-definition radio

Satellite radio

Stale formats Lackluster content Internet

Advertising & Access Spending

272.6/5.2 Expansion of number of broadband households

Rise of Internet as center for social networking and media and entertainment center

Dependent on network accessibility for and band-width to consumers

Videogames 44.2/9.1 Expansion of number of broadband households

Introduction of new games

Introduction of more advanced devices Expansion of wireless subscribers Expansion of broadband wireless subscribers

Ease of digital copying and piracy

Magazine Publishing

110/3.1 Rising incomes in emerging markets Reader and advertising migration to the Internet Newspaper

Publishing

191.1/2.1 Free papers are source of most growth Reader and advertising migration to the Internet Book

Publishing

135/3.6 e-Readers and other electronic devices will stimulate growth

Growth in textbooks and professional books

Electronic sales may cut into print sales

Reader migration to the Internet

Business Information

Filmedentertainmentisafairlylargesegmentofthemediaindustries,butnot nearlyasbigasthemarketfortelevisionnetworksandtelevisiondistribution.8

Forecasts of worldwide revenues anticipate growth at a modest 4.9 percent (CAGR) over the next 5 years. The United States and Europe are the largest markets,buttheyarealsorelativelyslow-growing.TheAsiaPacificandLatin Americaregionsaretheworld’sfastestgrowingmarkets.

Filmedentertainmentbringsinsignificantrevenue,butitisalsoexpensiveto create. High costs impose a significant barrier to entry for many producers, althoughwiththetransitiontodigitalproductiontoolsanddistribution,there issomecostreduction.Nevertheless,therealityremainsthatbigblockbusters comefrombigstudios.Withtheexceptionofonlyafewindependentstudios andproducers,largestudiosthatarebusinessunitsofhugemultinationalmedia corporationsproduceanddistributemostgloballysuccessfulmotionpictures. Forecastingrevenuesforthissegmentisdifficult,becausefilmedentertainment isahit-drivenbusiness–incomedependsonthereleaseofcompellingcon

-tent. However, they will continue to grow through 2010, stimulated by new technologiessuchasdigitalcinema,modernizedtheatricalauditoriums,high-definition television screens and DVDs, subscription and on-demand Inter

-netdownloadingservices,mobileplayersandreceivers,andtheexpansionof the number of broadband households. According to copyright owners, one inhibitorofgrowthisthecopyinganddistributionofcontentwithoutpermis

-sionfrom(andusuallywithoutpaymentto)thecopyrightholder.Professional counterfeitersandcasualcopyingthroughpeer-to-peernetworkingbothcon

-tributetosomelossofprofitsbymediacompanies,althoughthereisdisagree

-mentaboutexactlyhowmuchmoneyisinvolved.

Broadcast and Cable Television Networks

Economistsbasethesizeofthemarketforbroadcastandcabletelevisionnet

-worksontheincomethesenetworksattractfromadvertisersaswellasrevenue fromcarriers,suchascableandsatelliteoperators.Thegeographicalcentersof televisionnetworksmirrorthoseoffilmedentertainment,andtheyareusu

-ally operated by the same media giants. In the United States, this category includeslocaltelevisionstationsandcableoperators.InEuropeandAsia,it includesmoniesfrompubliclicensefees.Estimatesofglobalrevenuesforthis segmentpredictitwillgrowfromabout$181.4billionin2007to$228.3in 2011,aCAGRof4.8percent.9Thefastest-growingregionsareLatinAmerica

andEurope,whicharelikelytoexperienceamodestgrowthrateduetonet

-worksintheregionsrelyingonstagnantgovernment-collectedlicensefees. A rising standard of living in many countries around the world, increased advertising, and the penetration of high-definition television will stimu

Structure and Characteristics of the Media Industries 9

Internetvideoandthegrowthofvideo-on-demandplatformswillalsodrive increasedrevenueat6.5percentCAGR.Revenuefromthereleaseofseasonsof TVprogrammingonDVDsaddsincrementallytoincome,althoughpiracyisa concernasthismarketgrows.

Inthepast,U.S.broadcasttelevisionnetworkscreatedhitshowsthathadbroad appeal.Manyyearsago,whentherewereonlythreenetworks,ahitshowmight attainashareof70percentoftheviewingaudience.(NielsenMediaResearch measuresthepopularityoftelevisionshowsfortheindustrybyreportingrating points and shares.ThesetermswillbecoveredmorefullyinChapter6,which examinesaudiencesandprogramming.)

Todaytherearehundredsofnetworksandthemassaudiencehassplintered undertheonslaughtofcablenetworkswithnicheappeal.Inthefirstweekof October2009,Nielsendatashowedthatthefourlargestbroadcastnetworks wereashadowoftheirformer30percentormoreselves:CBSaveraged11.3 millionviewers(7.2rating,12share).ABChad9.6millionviewers(6.2,10), NBChad7.8million(4.9,8),andFoxhad7.6million(4.5,7).Eventhemost popularshowsfarelittlebetter.Inthefallof2009,Housebeganthenewseason witha6.5rating(6.5percentofallTVhouseholds)anda16share(16percent ofallTVhouseholdswatchingatelevisionshowatthetime).

Eventhoughthenumberofpeoplewatchinganyparticulartelevisionshow went down, the cost of buying television advertising time actually went up. Broadcastnetworksactuallychargeapremiumforcommercialtime.Therea

-son?Thereareonlyafewplaceswhereadvertiserscanreachamassaudience. Theremaybeapointofdiminishingreturns,butitisnowhereinsight.Any mediumthatcanaggregatealargeaudiencewillattractadvertiserswhomarket productsthathavebroadappeal,andtelevisionstilldoesthatjobbetterthan anyothermedium.

Asteadyriseinthenumberofdigitalhouseholds,whichwillbringinmore advertisingandhigh-definitiontelevisionchannels,willstimulatethegrowth inthissegment.Inaddition,therentalandsaleofDVDsthatholdanentire

The Nielsen company, which provides television viewing data for the industry, defines ratings and shares:

Rating: A rating is a percent of the universe that is being measured, most commonly dis-cussed as a percent of all television households.*

Share: A share is the percent of households or persons using television at the time the program is airing and who are watching a particular program […]. Shares can be useful as a gauge of competitive standing.10

seasonofshowsisagrowingsourceofrevenuefortelevisionnetworksthat havecreatedhitshows.BothclassicandcontemporaryTVshowscansellwell. As with other content distributed on DVDs, piracy could threaten this new revenuestream.

However,theaudiencecontinuestofragmentacrossmultiplemediavenues. Broadband Internet access is growing rapidly. More than 54 million house

-holdshaveaccesstovideo-on-demandservices.11Morethan35millionhave

DVRs(digitalvideorecorders).12OnApril9,2007,Appleannouncedthatit

hadsold220millioniPods.13

Television Distribution

Television distribution includes the amount consumers spend on subscrip

-tionsandpremiumchannelaccess,suchaspay-per-viewandvideo-on-demand access.ItalsoincludesrevenuesforTVprogrammingdistributedonmobile phonesinAsia,whereconsumerspaysubscriptionfeesforthisservice.Growth fortelevisiondistributionwillbehigh:9.3percentCAGRbetween2007and 2011.14 However, this overall figure hides the large discrepancy in regional

growth:TVdistributionwillgrow18.1percentCAGRinAsia,withespecially bigincreasesintheAsiaPacificregion,12.3percentinLatinAmerica,and12.3 percentinEurope,theMiddleEast,andAfrica.

However,intheUnitedStates,growthwillbeamodest5.4percent,because consumers can already choose cable or satellite television delivery, and the marketissaturated–subscriptionpenetrationisatnearly90percent.Viewers in other regions have fewer choices, and many have only satellite subscrip

-tionserviceasamultichannelprovider.Astelephonecompaniesbegintooffer high-speedInternetaccessservices,theyarelikelytomarketbundledoffersof televisionsubscriptionandInternetaccessbothinallregionsoftheworld,but intheUnitedStates,theyarelikelytotakemarketshareawayfromcableand satellite,ratherthanincreasingtheoverallmarketverymuch.

Recorded Music

Music is recorded around the globe, in most major cities of the world. The equipmentisessentiallythesame,whetherthegigtakesplaceinLosAngelesor Lima.IntheUnitedStates,mostmusiclabelsandmuchmusicrecordingtakes placeinNewYork,Nashville,andLosAngeles.

Executivesintherecordedmusicsegmenthavefacedangry,skeptical,disdain

-ful,anddisbelievingaudiencesoverthepastdecadeandahalf–audiences thatincludeconsumers,performersandmusicians,andmanagersfromother mediaindustries.Theypointtopoorplanningandlazymarketing,inepttal

Structure and Characteristics of the Media Industries 11

Byanymeasure,ithasnotbeenagood15yearsforthisindustrysegment.The marketforrecordedmusicencompassesphysicalmedia–albums,singlerecordings, andmusicvideo–andpaiddigitaldistributionviabothwiredandwirelessnet

-works.Inadditiontosongsandalbums,thecategoryalsoincludesrevenuefrom thesalesofringtones,ringtunes,andringbacks.Theglobalmarketisgrowingvery slowly,from$36.1billionin2006toabout$40.4billionin2011,a2.3percent CAGR.Eveninfast-growingregionslikeAsiaPacificandLatinAmerica,themarket willgrowonlyat5.4percentCAGR.ForecastscallfortheUnitedStates,thelargest marketinthiscategory,todeclineby0.4percentCAGR.

Thedeclineofthemarketforrecordedmusicseemstobeaccelerating.Inmid-2007,reportedsalesofthetop-sellingCDalbumsweredown30percent,com

-paredtothesameperiodtheyearbefore.Someanalystsattributethelowering revenuestopiracy,andbothprofessionalcounterfeitingandpeer-to-peerfile sharinghaveprobablyplayedaroleinthedeclineofsales.However,others pointtopoormarketleadershiponthepartoflargemusiccompanies,ormusic labels,astheyareoftencalled.

“Themightymusicbusinessisinafreefall–ithaslostcontrolofradio;retail outletslikeTowerRecordshaveshutdown;MTVrarelybroadcastsmusicvideos; andtheoncelucrativealbummarkethasbeenovershadowedbydownloaded singles,whichmainlybenefitsApple,”writesHirschberg(2007)intheNew York Times Magazine.15Commentinginthearticle,DavidGeffen,thelegendarymusic mogul,said,“Themusicbusiness,asawhole,haslostitsfaithincontent.Only tenyearsago,companieswantedtomakerecords,presumablygoodrecords, andseeiftheysold.Butpanichassetin,andnowit’snolongeraboutmaking music,it’sallabouthowtosellmusic.Andthere’snoclearanswerabouthow tofixthatproblem.ButIstillbelievethatthetoppriorityatanyrecordcom

-panyhastobecomingupwithgreatmusic.”Onebloggerofferedthefollow

-ingexplanationoftheindustry’swoes:“Freemusicdownloading;suingyour customers; alienating your customers by spying on them; inexpensive single downloads;lowornoqualityproduct;overpricedmedium;greedyindustry.” Theindustryisinthemidstofarapidtransitionfromphysicaldistributionto digitaldistribution.Between2006and2011,globalphysicaldistributionwill declineby9.6percentCAGR.Thischangeinthebusinessenvironmentmeans thatlabelsthathopetobesuccessfulwillneedtofindmethodsofdoingbusi

-nessbasedondigitaldistribution.16

Ringtones: The sounds your mobile phone makes when it rings

However,digitalfilesarevulnerabletoeasycopying,sotheyhaveengagedin manyeffortstoreducecasualcopyingandfilesharingbyconsumers.Between 2003and2007,themusiclabels’tradegroup,theRecordingIndustryAssocia

-tionofAmerica,initiatedorthreatenedlegalactionagainstmorethan20,000 people.17 They have also adopted technological barriers such as proprietary

fileformatsthatrequirespecialplayersorsoftwarethatrestrictscopying.These technologiesareoftencalleddigital rights managementorDRM.

Radio

The radio segment includes advertising revenue spending, local over-the-air free broadcast radio stations, and advertising spending and consumer sub

-scriptionspendingforsatelliteradio.Companiesthatownradiocompanies are usually in financial centers of the country where they operate; however, transmitterscanbeanywhereor,aswithsatellitedelivery,everywhere.Likethe music industry, broadcast radio is experiencing a difficult business environ

-ment.Overallglobalrevenuesareprojectedtogrowat5.2CAGR.18InEurope,

increasesinradioadrevenueareunlikelytotop3percentbetween2007and 2011.IntheUnitedStates,advertisingonradiohasbeenflatfor3yearsand forecasterspredictthat2007levelswillrangebetween2percentupand2per

-centdown.19Despitethestagnantrevenues,thesaleofradiostationshasnot

slowed,becauseinvestorscontinuetofindradiostationsveryprofitablebusi

-nesses,particularlyinmediumandlargemarkets.

Thereareseveralexplanationsfortheindustry’slackofgrowthinmaturemar

-kets, such as the United States and Europe. Some analysts cite concern with businessprocesses,suchasthecomplexityadvertisersfacewhenbuyingtimeon multiplestations,lackofelectronicinvoicing,andaudiencemeasurement.Other observersbelievethatformatsandprogrammingpracticesareaproblem. “Radioisastalemedium,”saysSteveKalb,seniorVPanddirectorofbroadcast mediaforMullen’smediaHUB,whonotesthathekeepsacloseeyeondeclining listeninglevels.“Everytownhasthesamekindofformat.It’sthesamemusic.It’s verygenericandwhite-bread.Thehomogenizationofradioisfrightening.”20

IntheUnitedStates,consolidationisoftenblamedforthedeathofprogram

-ming that would attract new viewers. Throughout the 1990s, large national media companies bought up many local stations that were formerly “mom andpops,”individual-orfamily-ownedstationswithtiestothelocality.For example,ClearChannel,thelargestradiogroupintheUnitedStates,owned morethan1,150stations.However,thereappearstobesomedeconsolidation occurringin2007,asClearChannelannounceditwassellingmorethan362 ofitsstations,mostlyinsmall,ruralmarkets.Bymid-2009,manyanalystspre

-dictedthelargestU.S.radioconglomeratewouldhavetodeclarebankruptcy, andlaterintheyear,Citadelhadfiledforbankruptcyandseveralotherterres

Structure and Characteristics of the Media Industries 13

IntheUnitedStates,consolidationoccurredasaresultofchangesinregulations bytheFederalCommunicationCommission(FCC),whicheliminatedbarri

-ers to the number of stations companies could own. The FCC also lowered therequirementsforlocalprogramming,sothatmanystationsrunsimplyas automatedcomputerservers,transmittingcontentproducedelsewhere.Inthis way,consolidationhasreducedthenumberofjobsintheradioindustry,so thataverysmallnumberofmanagersrunaverylargenumberofstations.The lossofindividualstationshasalsocausedstationdiversitytodecline,sothat stations(andtheirmanagers)appeartospeakwithonevoice.

Analystsexpectradioformataudiencestoshiftinthenextfewyears,withcoun

-trymusiclistenershipgrowingby24percent,news/talkformatsby20percent, urbanstationsby15percent,andSpanishradio14percent.Allotherformats, suchasoldies,adultcontemporary,rock,jazz,andadulthits,areprojectedto decline.22Independentmusiclabelssufferthemostfromthenear-monopoly

oncommercialradiobymajorlabels–theirpay-for-playdominationofradio makesitimpossibleforindependentmusicianstogetairplay,confininginde

-pendentartiststothemargins.NowfilesharingandCDburninghavecreated the first real opportunity to break the major label cartel, and independents have the most to gain. Many independents are no longer pounding on the doorsofradiostations,becausetheybelievethatthelinkbetweenradioplay andmusicsalesisnowbroken.23Intheirview,theInternetprovidesamuch

moreflexible,discovery-orientedmediumforfanstofindnewmusic.

Internet Advertising and Access Spending

Internetadvertisingisthefastestgrowingadmedium.Itisasegmentwhere jobseekersjustoutofcollegemaybeabletofindajobandbeabletogrowa careerastheindustrymatures.MuchofthejobofInternetmanagersiseducat

-ingthosenotintimatelyinvolvedwiththeindustryaboutwhattheNetcando forthemandtheircompanies.

Internetcompaniesareeverywhere,buttheyarethickonthegroundintech

-nological centers. They are likely to be near universities that offer sophisti

-catedcomputerscienceandothercommunicationsengineeringprogramsand confermaster’sanddoctoraldegrees.IntheUnitedStates,theselocationsare SiliconValleyinCalifornia;Austin,Texas;andBoston,Massachusetts.InAsia, Tokyo,Seoul,andSingaporearemajorcentersofInternetactivity.InEurope, London,Paris,Rome,andothercapitalcitiesdominate.InAustralia,Auckland andSydneyarecentersofInternetinnovation.

In2003,Internetadvertisingandaccessspendingmadeup3percentofglobal advertising; by 2011, it will rise to 14 percent. PricewaterhouseCoopers esti

the global Internet access market will rise from $169.5 billion to $298.4, a 12.2 percent CAGR. The access market differs across regions, because some territoriesalreadyhavealargenumberofsubscribers.TheU.S.Internetaccess marketwillgrowata7.1percentCAGR;AsiaPacificwillexpandata16.9per

-centCAGR.24

In2004,Internetadvertisingrevenuessurpassedthoseofoutofhomeadver

-tising(outdoorboardsandsigns).In2007,theNetovertookradio.In2010, itwillbringinmoreaddollarsthanmagazines.However,asof2007,Internet adincome($49.6billion)isfarbehindtheremainingmassmedia–television ($196.9billion)andnewspapers($117,878).

Globally, Internet advertising is growing at a double-digit rate, about 18.3 CAGR.Asfastasthiscategoryisexpanding,itisstilllimitedbyoverallrates ofconnectivity.IntheUnitedStates,whereadvertisingisalong-established part of media environments, the Internet advertising market is well devel

-oped.In2007,almost40.3percentofadvertisers’budgetswenttowardkey

-wordsearch–aboutthree-quartersofthisspendingwenttoGoogle.Classified ads received 25.6 percent of ad money, video brought in 3.3 percent, and otherformsofadvertisingsuchasbanneradsanddisplayadsaccountedfor 30.8percentofallmoneyspentonInternetadvertising.Forecastscallforkey

-wordsearchadvertisingtoincreaseoverthenext5years.Spendingonbanner adsandotherstaticformatswilldeclineasbroadbandusageexpands,allowing advertiserstousemorevideocontent.

Managers of Internet companies agree that one barrier to faster ad revenue growthinthismediasegmenthasbeentheabsenceofagreed-uponmethods ofmeasuringeffectiveness,ormetrics.Advertisingmanagersusemetricstocon

-vincetheirsupervisorstospendpartoftheirbudgetsonWebsites.Theyalso usemetricsafterthecampaigntoshowtheeffectivenessoftheadspend.

Theuniversallanguageofadvertising,irrespectiveofmedium,isimpressions.

TheInternetAdvertisingBureau(IAB),atradegroup,hasbeenworkingon establishingindustry-widemetricsforimpressions.Twocompaniesdominate themeasurementofInternetadvertising,ComScoreandNielsen/NetRatings. Advertisersareconcernedwithdiscrepanciesbetweenthemeasurementsof each firm of the same sites as well as differences between what the mea

-surementcompaniesreportandtherecordsmaintainedontheadvertisers’ servers.

InApril2007,IABpresidentandCEORandallRothenbergwrotetoComScore and Nielsen/NetRatings, asking them to hold a summit meeting to resolve measurementissues:“Weareseekingyouragreementtoanear-termtimeta