KINERJA KEUANGAN

DISERTASI

Oleh:

N U R O F I K 01/1037/PS Ilmu Akuntansi

PROGRAM DOKTOR ILMU AKUNTANSI FAKULTAS EKONOMIKA DAN BISNIS

UNIVERSITAS GADJAH MADA YOGYAKARTA

KINERJA KEUANGAN

Disertasi untuk memperoleh derajad Doktor dalam Ilmu Akuntansi

pada Fakultas Ekonomika dan Bisnis Universitas Gadjah Mada

Dipertahankan di hadapan

Dewan Penguji Program Doktor Ilmu Akuntansi Fakultas Ekonomika dan Bisnis,

Universitas Gadjah Mada, pada tanggal: _____________

Oleh: N U R O F I K

Lahir di:

SUMMARY

1. Introduction

One of the contemporary issues in the business world is the issue of corporate social

responsibility (CSR). One way to find out the practice of CSR is through reporting or

disclosure of the CSR (Abbott and Monsen, 1979; Weldman, 2002).

Diversity in CSR disclosure has raised numerous questions, such as: 'Is the CSR disclosure the company’s reactive or proactive activity?' And 'Does the CSR

disclosure serve the company's interests or social interests?'. From the reactive

standpoint, CSR disclosure is expected to occur when the company suffers from

threats of legitimacy (Deegan and Rankin, 1996; 1997; Deegan et al., 2002). On the

other hand, from the proactive standpoint, CSR disclosure is expected to occur when

managers attempt to minimize the profits reported to reduce political actions that are

not beneficial for the firm (Belkaoui and Karpik, 1989).

Although many researches on the determinants of CSR disclosure had been

done, most of those studies were focused on public pressure in general (legitimacy

theory), the pressure force of certain stakeholder groups (stakeholder theory), and

political pressures (political cost theory in the positive accounting theory) as the

determinants of CSR disclosure. There are still very few studies that look at the CSR

disclosure from the psychological/manager behavioral aspect (Weldman, 2002).

CSR disclosure practices in Indonesia still vary among companies. It is

related to the voluntary nature of CSR disclosure. The voluntary nature of CSR

disclosure allows the manager to have different motivations in disclosing the CSR

thus causing differences in CSR disclosure practices. Therefore, managers’

the socio-economic perspective (Mangos and Lewis, 1995), managers’ behavior and

goals are not only influenced by certain institutions, investors, creditors or other

parties that make formal contracts with the company, but is also influenced by

noneconomic factors such as the managers’ personal relationships.

Verrecchia’s disclosure theory (1983) states that the company (managers)

would only disclose information to the public (market) if the benefits of voluntary

disclosure outweigh the proprietary cost of disclosure. In other words, in a voluntary

disclosure, the company (managers) only discloses information to the public if the

action is considered beneficial in the future. One of which is the economical benefit

for the company.

This study was aimed at achieving two objectives. First, to examine the

behavioral factors of managers that influenced CSR disclosure. Behavioral theory

basis used in this study was the Theory of Planned Behavior. Second, to examine the

relationship of CSR disclosure with corporate financial performance. Theoretical

basis used to achieve the second objective was the Stakeholder Theory.

2. Theory and Hypothesis Development Theory of Planned Behavior

Theory of Planned Behavior was developed by Ajzen (1985; 1991) and is an

extension of the Theory of Reasoned Action developed by Fishbein and Ajzen

(1975). The Theory of Reasoned Action assumes that people choose a set of actions

(behaviors) rationally/consciously by using available information and implicitly or

explicitly consider the implications of their actions.

The Theory of Reasoned Action postulate is one’s intention to perform or not

1985). A behavior is believed to be the result of behavioral intention. Behavioral

intention is defined as the subjective probability of an individual in determining the

choice made out of various alternative behaviors. The general rule of the Theory of Reasoned Action is the stronger an individual’s intention to perform a behavior is,

the greater the likelihood of such behavior’s exhibition is. Behavioral intention is a

function of two basic determinants, namely personal factors called the attitude

towards the behavior and the influence of social pressure called the subjective norms.

Attitude towards the behavior is a construct that combines individual beliefs about

the likelihood of certain outcomes of the behavior and thorough evaluation of these outcomes. Subjective norms show the individual’s beliefs of the social pressure to

perform or not to perform the behavior. Subjective norms are a construct that

combines individual’s confidence in certain referent behavior drives and the level of

compliance with these referents (Hanno and Violette, 1996).

The Theory of Planned Behavior is an extension of the Theory of Reasoned

Action. The expansion is necessary, given the limitations of the Theory of Reasoned

Action in facing the behaviors in the situation in which people do not have a

complete volitional control (Ajzen, 1991). One constructs added in the Theory of

Planned Behavior is perceived behavioral control. Perceived behavioral control is

defined as one's beliefs in the level of difficulty or ease in performing the behavior

(Ajzen, 1991). Thus, this construct is related to resources and opportunities are

believed to be owned by individuals (Ajzen, 1991). It means that the more resources

considered to be possessed by individuals, and the fewer obstacles or barriers that

The central factor of the Theory of Planned Behavior is the individual’s

intention to perform a behavior. Although the intention is expected to capture the

motivational factors that influence the behavior, a behavioral intention can find its

expression in the behavior only if the behavior is under complete volitional control,

i.e. if one can independently decide to do or not to do the behavior. On the other

hand, if a behavior is under incomplete volitional control, then the intention is not

sufficient to explain the behavior. Briefly, a behavioral intention, along with a

perceived behavioral control can be used directly to predict one’s behavior.

Stakeholder Theory

According to this theory the existence of a company requires supports from

stakeholders and all stakeholders are essential to the success of the company (Freeman and McVea, 2001). Therefore, using Jensen and Meckling’s term (1976),

the company can be viewed as a "nexus of contracts" between the company

(managers) and its stakeholders (Jones, 1995).

According to the Stakeholder Theory, the CSR disclosure is seen as a

dialogue between the company and its corporate stakeholders (Gray et al., 1995b).

The central thesis of the theory is that the corporate disclosure is a means for a

management to administer the information needs of various powerful stakeholder

groups. Managers use information to administer or manipulate the most powerful

stakeholders in order to gain their support, which is necessary for the continuity of

the company (Gray et al., 1996 in Van-der Laan, 2006).

The instrumental dimensions of the Stakeholder Theory explain that a

company could gain financial benefits from the practice of CSR towards the

arguments to support it. First, the explicit costs of the CSR are minimum and the

company will benefit significantly from the CSR action in the form of employee

morale improvement, which will eventually lead to productivity (Moskowitz, 1972).

Second, the costs of the CSR actions are significant, but will be covered by other

costs’ decline in the company (Cornell and Shapiro, 1987). Third, the CSR action

would improve the company's relationships with important constituencies such as

creditors, investors, and governments that will improve the company's access to the

capital sources (Moussavi and Evans, 1986). Furthermore, according to the

Stakeholder Theory, a company must provide satisfaction not only for the

shareholders, but also for the parties that have less explicit (implicit) claims.

Abandonment of the interests of the parties that have implicit claims will result in the

change of the implicit costs into explicit costs that are more expensive (costly) for

the company. For example, if a company does not pay attention to its negative

impacts on the environment, then the government will issue strict regulations to force

the company to take responsible actions in environmental fields, which can lead to a

more expensive explicit cost for the company.

Hypothesis Development

a. The Influence of Manager’s Attitude, Subjective Norms, and Perceived behavioral control of the CSR Disclosure on The Intention to Disclose CSR

The general rule of the Theory of Planned Behavior is the better or the more

positive one's attitude towards a behavior is, the stronger the social pressure to

perform behavior would be, and the more powerful the perceived behavioral control

is, the stronger one's intention to perform the behavior would be. In the context of the

more positive the manager’s attitude towards the CSR disclosure is, the stronger

his/her intention to disclose the CSR would be. Therefore, this study hypothesized as

follows:

H1: Manager’s attitude towards the CSR disclosure has a positive influence on the intention to disclose the CSR.

The second rule of the Theory of Planned Behavior states that the stronger one’s belief in the social pressure to perform a behavior is, the stronger the intention

to perform the behavior would be. In the context of CSR disclosure, the stronger the social pressure on managers to disclose CSR is, the stronger the managers’ intention

to disclose the CSR would be. Therefore, this study hypothesized as follows.

H2: Managers’ subjective norms of CSR disclosure have a positive influence on the intention to disclose the CSR.

The third rule of the Theory of Planned Behavior states that the more powerful someone’s perceived behavioral control is, the stronger the person's

intention to perform the behavior would be. In the context of CSR disclosure, the stronger a manager’s perceived behavioral control of CSR disclosure is, the stronger

the manager intention to disclose the CSR would be. Therefore, this study

hypothesized as follows.

H3: Managers’ perceived behavioral control of CSR disclosure has a positive influence on the intention to disclose the CSR.

b. The Influence of Managers’ Intention and Perceived Behavioral Control towards the CSR Disclosure on the CSR Disclosure

According to the theory of planned behavior, a behavioral intention, along

with a perceived behavioral control, can be used directly to predict a behavior’s

performance. The general rule of the theory of llanned behavior is the stronger the

control is, the greater the likelihood of the occurance of behavioral performance

would be. Therefore, this study hypothesized as follows.

H4: Managers’ intention to disclose the CSR has a positive influence on CSR disclosure.

H5: Managers’ perceived behavioral control of CSR disclosure has a positive influence on CSR disclosure.

c. Relationship between CSR Disclosure with Corporate Financial Performance

Instrumental dimensions of the stakeholder theory explain that a company

could obtain financial benefits from the practice of CSR towards the company's

stakeholders. According to the stakeholder theory, companies that are considered as

having a high CSR will have lower implicit claims compared with other companies,

therefore these companies will also have a higher financial performance (Cornell and

Shapiro, 1987). In addition, an unethical behavior within a company will decrease the company’s credibility and eventually will lower the company's performance

(Fritzsche, 2005). Since the CSR disclosure is a form of an ethical behavior in

business, therefore this study hypothesized as follows.

H6: CSR disclosure has a positively related to corporate financial performance.

3. Method of Research

Samples and Analysis Unit

This study used a sample of companies listed in the Indonesia Stock Exchange (IDX)

in 2007 and 2008, and engaged in the :(1) Agriculture, (2) Mining, (3) Basic and

Chemical, (4) Miscellaneous; and (5) Consumer Goods industrial sector. Selection of

criterions: (1) the companies are listed in the IDX in 2007 and 2008, (2) the

companies referred to in point (1) have an annual report for 2007 and 2008, and (3)

the annual report referred to in point (2) can be accessed or obtained from various

sources, for example through the IDX website, the website of each company, or a

library (Capital Market Reference Center) at the IDX.

This study used two units of analysis. First, the individual level. This unit of analysis was used to determine the managers’ behavioral factors that influenced CSR

disclosure. Second, the company level. This unit of analysis was used to determine

the influence of CSR disclosure on a company's financial performance.

Data and Method of Collection

The study used two sources of data, namely the secondary and primary data. The

secondary data included: (1) accounting performance, namely return on assets (ROA)

and earnings per share (EPS), (2) market performance (stock price in 2008 and 2007,

as well as dividends), and (3) CSR disclosure. The secondary data were obtained

from the company's annual report. The primary data were in the form of the response of the managers’ beliefs in the CSR disclosure. The primary data were obtained

through a questionnaire survey using three techniques, namely (1) mail survey, (2)

sending questionnaires via the internet by a direct access to

www.csr-nurofik.adkardus.com, and (3) submission of the questionnaire directly to each target

company (door to door).

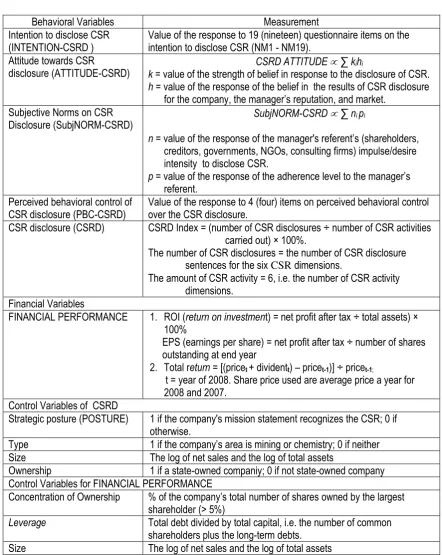

Research Variables and The Measurements

This study used five behavioral variables and one non-behavioral variable. In

influences on the CSR disclosure and financial performance. Table 1 presents the

research variables and measurements.

Table 1

Variables and Measurements

Behavioral Variables Measurement

Intention to disclose CSR (INTENTION-CSRD )

Value of the response to 19 (nineteen) questionnaire items on the intention to disclose CSR (NM1 - NM19).

Attitude towards CSR

disclosure (ATTITUDE-CSRD)

CSRD ATTITUDE ∑ kihi

k = value of the strength of belief in response to the disclosure of CSR. h = value of the response of the belief in the results of CSR disclosure

for the company, the manager’s reputation, and market. Subjective Norms on CSR

Disclosure (SubjNORM-CSRD)

SubjNORM-CSRD ∑ ni pi

n = value of the response of the manager's referent’s (shareholders, creditors, governments, NGOs, consulting firms) impulse/desire intensity to disclose CSR.

p = value of the response of the adherence level to the manager’s referent.

Perceived behavioral control of CSR disclosure (PBC-CSRD)

Value of the response to 4 (four) items on perceived behavioral control over the CSR disclosure.

CSR disclosure (CSRD) CSRD Index = (number of CSR disclosures ÷ number of CSR activities carried out) × 100%.

The number of CSR disclosures = the number of CSR disclosure sentences for the six CSR dimensions.

The amount of CSR activity = 6, i.e. the number of CSR activity dimensions.

Financial Variables

FINANCIAL PERFORMANCE 1. ROI (return on investment) = net profit after tax ÷ total assets) × 100%

EPS (earnings per share) = net profit after tax ÷ number of shares outstanding at end year

2. Total return = [(pricet + dividentt) – pricet-1)] ÷ pricet-1;

t = year of 2008. Share price used are average price a year for 2008 and 2007.

Control Variables of CSRD

Strategic posture (POSTURE) 1 if the company's mission statement recognizes the CSR; 0 if otherwise.

Type 1 if the company’s area is mining or chemistry; 0 if neither Size The log of net sales and the log of total assets

Ownership 1 if a state-owned companiy; 0 if not state-owned company Control Variables for FINANCIAL PERFORMANCE

Concentration of Ownership % of the company’s total number of shares owned by the largest shareholder (> 5%)

Leverage Total debt divided by total capital, i.e. the number of common shareholders plus the long-term debts.

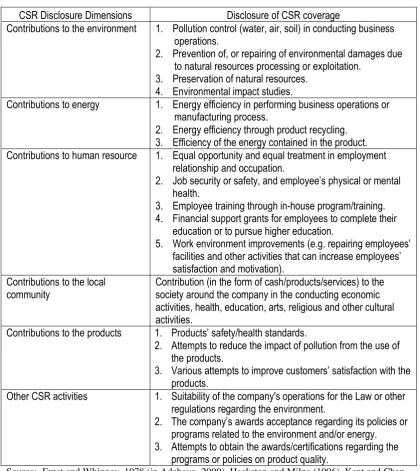

Questionnaire Development

Research questionnaire was constructed in two stages. Firstly was by identifying the

dimensions of CSR and the scope of disclosure. Table 2 presents CSR disclosure

dimensions and the scopes. Secondly, the questionnaire was constructed to find out

the existence of the CSR practice, INTENTION-CSRD, ATTITUDE-CSRD,

SubjNORM-CSRD, and PBC-CSRD.

THE EXISTENCE OF THE CSR PRACTICE. To find out the existence

of the CSR practice, nineteen CSR activities were provided for the respondents, as

shown in Table 2. Subsequently the respondents were asked to answer the question

'Does this company perform the following CSR activity?' The format of the answer

was 'yes' and 'no.' In addition, to reduce biased response, the respondents were asked

to select a range of average expenditure per year to fund the CSR activities

performed.

INTENTION-CSRD. To find out the respondent's INTENTION-CSRD, they were given nineteen items on CSR disclosure as shown in Table 2. Furthermore,

to measure the strength of INTENTION-CSRD, the questionnaire was constructed to

provide the statement 'I intend to disclose the following CSR activity in the annual

report.' The response format ranged from very unlikely to very likely, using a 5-point

Likert scale.

ATTITUDE-CSRD. ATTITUDE-CSRD construct has two dimensions,

namely the strength of beliefs to CSR disclosure and the evaluation of CSR

disclosure results (outcomes). Craighead and Hartwick (1998) present three sets of

executives/managers, and the market. This study used the aforementioned three sets

of benefits to measure the ATTITUDE-CSRD.

Table 2

CSR Disclosure Dimensions and Coverage

CSR Disclosure Dimensions Disclosure of CSR coverage

Contributions to the environment 1. Pollution control (water, air, soil) in conducting business operations.

2. Prevention of, or repairing of environmental damages due to natural resources processing or exploitation.

3. Preservation of natural resources. 4. Environmental impact studies.

Contributions to energy 1. Energy efficiency in performing business operations or manufacturing process.

2. Energy efficiency through product recycling. 3. Efficiency of the energy contained in the product. Contributions to human resource 1. Equal opportunity and equal treatment in employment

relationship and occupation.

2. Job security or safety, and employee’s physical or mental health.

3. Employee training through in-house program/training. 4. Financial support grants for employees to complete their

education or to pursue higher education.

5. Work environment improvements (e.g. repairing employees’ facilities and other activities that can increase employees’ satisfaction and motivation).

Contributions to the local community

Contribution (in the form of cash/products/services) to the society around the company in the conducting economic activities, health, education, arts, religious and other cultural activities.

Contributions to the products 1. Products’ safety/health standards.

2. Attempts to reduce the impact of pollution from the use of the products.

3. Various attempts to improve customers’ satisfaction with the products.

Other CSR activities 1. Suitability of the company's operations for the Law or other regulations regarding the environment.

2. The company’s awards acceptance regarding its policies or programs related to the environment and/or energy. 3. Attempts to obtain the awards/certifications regarding the

programs or policies on product quality.

Source: Ernst and Whinney, 1978 (in Adebayo, 2000), Hackston and Milne (1996), Kent and Chan

(2003) with some adjustments according to the relevance of its application in

To find out the strength of beliefs of the CSR disclosure, the respondents

were given nineteen items on CSR disclosure as shown in Table 2. Furthermore, to

measure the strength of beliefs, the questionnaire was constructed by providing the

following three statements:

Statement # 1 I believe that a disclosure on the annual report of following CSR activity* is ... for the company.

Statement # 2 I believe that a disclosure on the annual report of following CSR activity* is ... for the manager's reputation.

Statement # 3 I believe that a disclosure on the annual report of following CSR activity * is ... to market. "

* nineteen items of CSR disclosure

The format of the answer to each statement ranged from very bad to very good with a

5-point Likert scale.

For the evaluation dimensions of the CSR disclosure results, this study

modified the questionnaire items developed by Craighead and Hartwick (1998).

Modifications were made due to the differences in disclosure objects. The object of

the disclosure of this study is the CSR, while Craighead and Hartwick’s (1998) was

the disclosure of earnings and corporate strategy. The results of modifications

showed eight benefits of CSR disclosure as follow:

For the companies

1. The potential benefits of CSR disclosure in the annual report exceeded the potential costs for the company.

2. CSR disclosure in the annual report generally gives positive impacts to the company, that is the public would assume that the company has been responsible in managing the social and environmental issues.

For the reputation of the executives/managers

1. Reputation of the company’s executives will increase if the company communicates CSR activities to the public through annual reports.

2. Reputation of the company’s executives will improve if the CSR disclosure activity in the annual report is done compared to not disclosing it.

For the market

1. The market impact from bad news will decline if the company continuously announces good news to the public through annual reports.

2. Disclosure of information on the CSR to the public through annual reports will reduce the cost of information acquisition by the investors and stimulate investors’interests in the company’s shares.

3. The cost of raising capital will decline if the company perform an honest CSR disclosure on a regular basis to the public through annual reports because the information will enhance the investors/creditors’ confidence in and better understanding of the company.

Furthermore, to measure the benefits of CSR disclosure, respondents were

asked to make a statement of agreement or disagreement with the eight benefits of CSR disclosure. Respondents’ answers was constructed using a 5-point Likert scale,

from strongly disagree to strongly agree. The higher score reflects the higher benefits

of CSR disclosure.

SubjNORM-CSRD. This construct has two dimensions (Ajzen, 1991), namely the parties (referents) that affect the subject to perform a particular behavior (normative beliefs) and the subject’s level of compliance to the referents. This study

used 5 (five) referent managers, namely (1) shareholders, (2) creditors, (3)

government/politicians, (4) consultants, and (5) non-governmental organizations

(NGOs) engaged in the supervision of the social and environmental activities

conducted by the company.

Based on the aforementioned five referents, in order to measure the strength

of normative beliefs, the questionnaire was constructed by asking the question 'How

big/small is the impulse (desire) of the following parties for the CSR disclosure in

the annual report?' The response was constructed using a 5-point Likert scale from

In order to measure the level of compliance, the questionnaire was

constructed by asking the question 'How big/small is the possibility that you will

comply to the wishes the following parties on the CSR disclose in the annual report?'

The response was constructed using a 5-point Likert scale from very small to very

large. The higher scores reflect higher levels of compliance.

PBC-CSRD. This study adopted a questionnaire developed by Weldman (2002) by replacing the term ‘environment’ with ‘CSR’ to find out the perceived

behavioral control of CSR disclosure. The questionnaire consisted of four statements,

namely (1) I have control over the decision to disclose the CSR in the annual report,

(2) it would be very easy for me to disclose the CSR on the annual report, (3) the

authority given to my position is sufficient to make decisions regarding the CSR

disclosure in the annual report, and (4) I feel confident that the skills, the abilities,

and the quality of knowledge I possess will be helpful in the making of decisions

regarding the CSR disclosure in the annual report. Furthermore, to measure the

PBC-CSRD, the questionnaire was constructed using a 5-point Likert scale from strongly

disagree to strongly agree. The higher scores indicate higher PBC-CSRD.

Efforts to Eliminate (Decrease) Bias

Nonresponse bias. Efforts made to eliminate (reduce) nonresponse bias included (1) questionnaires delivered directly if sending by mail did not work as

expected, (2) providing questionnaires through www.csr-nurofik.adkardus.com, (3)

giving incentives to the respondents in the form of original silver craft from Kota

Gede, Yogyakarta, to express the gratitude toward the respondents, and (4)

the request for the manager to complete the questionnaire. The cover letter also

explained about the importance of the participation of the managers for the

development of science, especially accounting, in Indonesia.

Social desirability bias, leniency bias, extremity bias, and acquiescence bias. Efforts made to reduce the social desirability bias, leniency bias, the extremity bias, and the acquiescence bias included (1) requiring the respondent to answer all

questions as they are, (2) guarantying the confidentiality of respondents' answers,

including the anonymity of respondents, and (3) assuring the respondents that there

were no right or wrong answers so that they were willing to answer questions

truthfully. These efforts were written in the cover letter and at the beginning of the

questionnaire.

Ambiguity bias of item. To eliminate (reduce) ambiguity of item bias, the

efforts made were (1) providing questionnaires with the definition of the CSR to

clarify the meaning of disclosure and the limits (coverage) of each of the CSR area

therefore before answering the questionnaire respondents were expected to

understand the elements (items) of CSR and (2) conducting preliminary testing of the

questionnaire to find out as early as possible the statements in the questionnaire that

were confusing or contained multiple interpretations for the respondents.

Validity and Reliability Testing of the Instruments

Convergent validity. Convergent validity related to the principle that the

measures of a construct should be highly correlated (Hartono and Abdillah, 2009).

Parameters to determine the convergent validity were (1) score of loadings (rule of

(rule of thumb > 0.5 ). Questionnaire items that did not meet these criteria should be

removed and the test was performed only on the items that meet the criteria for

convergent validity.

Discriminant validity. Discriminant validity is the indicators of a construct

that are not only converging, but also different or negatively related with other

constructs (Neuman, 2000: 170). There are two ways to determine the discriminant

validity, namely (1) comparing between the root score of the AVE of a construct

with the correlations score of the latent variables (an indicator is said to meet the

criteria of discriminant validity if the root score of the AVE is > correlation score of

the latent variables) and (2) seeing the cross loadings score of a construct (an

indicator is said to meet of discriminant validity if the scores of cross loadings of the

constructs accumulates at their construct and have greater scores than the score of

cross loadings on other constructs).

Reliability. Reliability testing is conducted to determine the accuracy,

consistency, and precision of a measuring instrument in performing measurements

(Hartono, 2008). Parameters to determine the reliability of the instrument are the

score of Cronbachs alpha and the composite reliability. A research instrument is said

to meet the criteria as a reliable instrument if the instrument has Cronbachs alpha >

0.6 and composite reliability> 0.7.

Hypothesis Testing

Econometric equations to test the hypothesis of this study are as follows.

CSRD = α0+ α1 INTENTION-CSRD + α2PBC-CSRD + α3POSTURE + α4TYPE + α5SIZE + α6OWNERSHIP + ε. ………... (2)

FINANCIAL PERFORMANCEt = α0+ α1CSRDt-1 + α2CONCENTRATION OF OWNERSHIPt + α3LEVERAGEt + α4SIZEt + ε. ... (3)

t = year 2008

Data Processing and Analysis Method

This study used Partial Least Square (PLS) technique to process and analyze data.

Software used was SmartPLS version 2.0.M3. Processing and data analysis were

carried out through three stages, namely (1) creating an image of the research model

consisted of a structural model (inner model) and a measurement model (outer

model), (2) testing the measurement model to determine the validity and reliability

of the instrument, and (3) testing the structural model to determine the results of

hypothesis testing.

4. Empirical Results and Discussion

The research was conducted on 32 respondents of 32 sample of companies listed on

the Stock Exchange in 2007 and 2008 which engaged in these industrial sector: (1)

Miscellaneous Industry, (2) Consumer Goods Industry, (3) Basic and Chemical

Industry, (4) Mining Industry, and (5) Agricultural Industry.

Test Results of Nonresponse Bias

The t-test was used in testing the nonresponse bias. The results of the t-test showed

that the probability value (p-value) for each construct was > 0.05. This meant that

there was no significant difference between the average responses of the

questionnaires that were not late and those who were. Thus the data of this study

Test Results of Measurement Model

The first test results of the measurement model showed that some indicators of

INTENTION-CSRD, namely NM3, NM4, NM5, NM6, NM7, NM 11, NM12, and

NM 15 had score loadings < 0.6, while the loadings score required was > 0.7Besides

that, INTENTION-CSRD only had AVE and communality score of 0.4, that were

still far from th required score, ie > 0.5. These results suggested that indicators were

not valid, should be removed from the measurement model, and the measurement

model testing should be repeated without including the indicators are not valid.

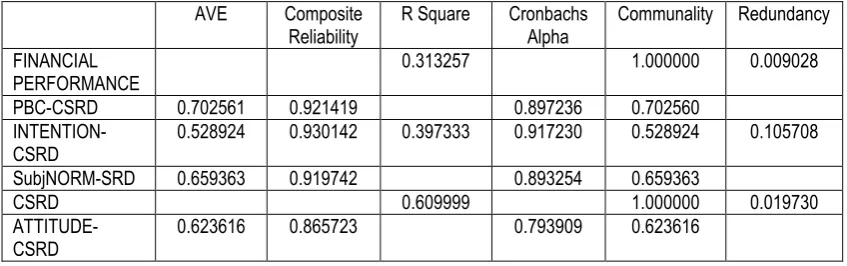

Convergent Validity. The results of repeated test of model measurement (the

advanced testing) indicated that the score loadings for the indicators in each

construct ranged from 0.74 to 0.94 (for PBC-CSRD); 0.64 to 0.82 (for

INTENTION-CSRD); 0, 67 to 0.98 (for SubjNORM-CSRD), and 0.60 to 0.95 (for ATTITUDE-

CSRD). AVE and communality scores of each construct were > 0.5 (see Table 3).

Thus, all indicators in this study had met the criteria for convergent validity.

Table 3

Quality Criteria: The Results of Advanced Test of Measurement Model

AVE Composite

0.313257 1.000000 0.009028

PBC-CSRD 0.702561 0.921419 0.897236 0.702560

INTENTION-CSRD

0.528924 0.930142 0.397333 0.917230 0.528924 0.105708

SubjNORM-SRD 0.659363 0.919742 0.893254 0.659363

CSRD 0.609999 1.000000 0.019730

ATTITUDE-CSRD

0.623616 0.865723 0.793909 0.623616

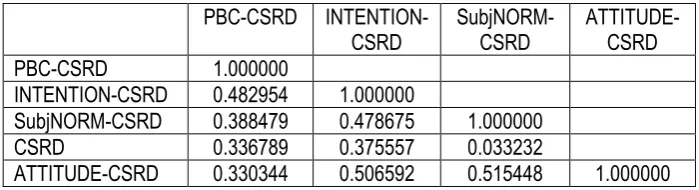

Discriminant Validity. Root of AVE for each construct was 0.838189 (for

0.528924); 0.812011 (for SubjNORM-CSRD, AVE = 0.659363); and 0.789693 (for

ATTITUDE-CSRD, AVE = 0.623616). If the scores of the root of AVE were

compared to the scores of correlation among the latent variables (see Table 4), then

the root of the AVE were > from the score of correlation among the latent variables.

Thus the indicators in this study had met the criteria for discriminant validity.

Table 4

Correlation of Latent Variables: Test Results of Measurement Model

PBC-CSRD INTENTION-CSRD

SubjNORM-CSRD

ATTITUDE-CSRD PBC-CSRD 1.000000

INTENTION-CSRD 0.482954 1.000000

SubjNORM-CSRD 0.388479 0.478675 1.000000

CSRD 0.336789 0.375557 0.033232

ATTITUDE-CSRD 0.330344 0.506592 0.515448 1.000000

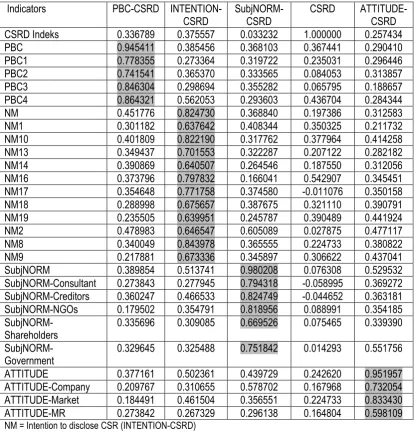

Discriminant validity could be found by looking at the score of cross loadings

of a construct. The scores of cross loadings of the measurement model test results

were presented in Table 5. From this table, it could be seen that the entire scores of

cross loadings for PBC, PBC1, PBC2, PBC3, and PBC4 indicator were accumulated

in their construct (i.e. PBC-CSRD) and had higher scores than the indicator scores to

other constructs (INTENTION-CSRD, SubjNORM-CSRD, CSRD and

ATTITUDE-CSRD). The same thing happened in other indicators. This showed that the indicators

Table 5

Cross Loadings Scores: Results of Measurement Model Testing

Indicators PBC-CSRD INTENTION-CSRD

SubjNORM-CSRD

CSRD ATTITUDE- CSRD CSRD Indeks 0.336789 0.375557 0.033232 1.000000 0.257434

PBC 0.945411 0.385456 0.368103 0.367441 0.290410

PBC1 0.778355 0.273364 0.319722 0.235031 0.296446

PBC2 0.741541 0.365370 0.333565 0.084053 0.313857

PBC3 0.846304 0.298694 0.355282 0.065795 0.188657

PBC4 0.864321 0.562053 0.293603 0.436704 0.284344

NM 0.451776 0.824730 0.368840 0.197386 0.312583

NM1 0.301182 0.637642 0.408344 0.350325 0.211732

NM10 0.401809 0.822190 0.317762 0.377964 0.414258

NM13 0.349437 0.701553 0.322287 0.207122 0.282182

NM14 0.390869 0.640507 0.264546 0.187550 0.312056

NM16 0.373796 0.797832 0.166041 0.542907 0.345451

NM17 0.354648 0.771758 0.374580 -0.011076 0.350158

NM18 0.288998 0.675657 0.387675 0.321110 0.390791

NM19 0.235505 0.639951 0.245787 0.390489 0.441924

NM2 0.478983 0.646547 0.605089 0.027875 0.477117

NM8 0.340049 0.843978 0.365555 0.224733 0.380822

NM9 0.217881 0.673336 0.345897 0.306622 0.437041

SubjNORM 0.389854 0.513741 0.980208 0.076308 0.529532 SubjNORM-Consultant 0.273843 0.277945 0.794318 -0.058995 0.369272 SubjNORM-Creditors 0.360247 0.466533 0.824749 -0.044652 0.363181 SubjNORM-NGOs 0.179502 0.354791 0.818956 0.088991 0.354185

SubjNORM-Shareholders

0.335696 0.309085 0.669526 0.075465 0.339390

SubjNORM-Government

0.329645 0.325488 0.751842 0.014293 0.551756

ATTITUDE 0.377161 0.502361 0.439729 0.242620 0.951957 ATTITUDE-Company 0.209767 0.310655 0.578702 0.167968 0.732054 ATTITUDE-Market 0.184491 0.461504 0.356551 0.224733 0.833430 ATTITUDE-MR 0.273842 0.267329 0.296138 0.164804 0.598109 NM = Intention to disclose CSR (INTENTION-CSRD)

NGOs = Nongovernmental Organization MR = Manager reputation

Reliability of the Test Results. Based on Table 3, Cronbach's alpha of each

construct has a score > 0.6. Composite reliability of each construct had a score > 0.7.

Structural Model Testing Results

Based on Table 3, the R-square value for the dependent variables of

INTENTION-CSRD was 0.397 (moderate). This meant that the construct variability of

INTENTION-CSRD could be explained by ATTITUDE-CSRD, SubjNORM-CSRD,

and PBC-CSRD construct at 0.397 (40%), the remaining 60% was explained by

other variables that were not examined (variables outside the research model).

R-square value for the dependent variable for CSRD was 0.609 (good). This meant that

the construct variability of CSRD could be explained INTENTION-CSRD construct,

PBC-CSRD construct, and the control variable at 0.609 (61%), The remaining 39%

was explained by other variables outside the model. R-square value for the dependent

variable FINANCIAL PERFORMANCE was 0.313 (moderate). This meant that the

variability of FINANCIAL PERFORMANCE could be explained by the all

independent variables in the model by 31%, the remaining 69% was explained by

other variables outside the model.

Research hypothesis would be supported if the coefficient β of ATTITUDE

-CSRD to INTENTION--CSRD, SubjNORM--CSRD to INTENTION--CSRD,

PBC-CSRD to INTENTION-PBC-CSRD, INTENTIONS-PBC-CSRD to PBC-CSRD, PBC-PBC-CSRD to

CSRD, and CSRD to FINANCIAL PERFORMANCE had a positive values and the

t-statistics values were greater than the t-table value (t-table value of significance of

5% = 1.64). In Table 6 the test result of the structural model and ROA were placed as

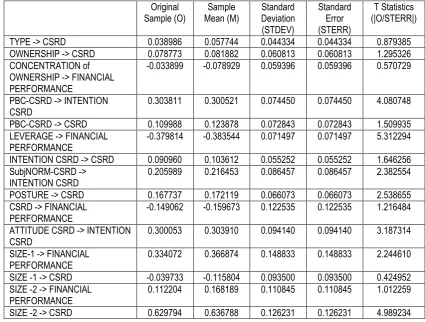

Table 6

Path Coefficient: Structural Model Testing Results – ROA as indicators FINANCIAL PERFORMANCE

Original

TYPE -> CSRD 0.038986 0.057744 0.044334 0.044334 0.879385 OWNERSHIP -> CSRD 0.078773 0.081882 0.060813 0.060813 1.295326 CONCENTRATION of

OWNERSHIP -> FINANCIAL PERFORMANCE

-0.033899 -0.078929 0.059396 0.059396 0.570729

PBC-CSRD -> INTENTION CSRD

0.303811 0.300521 0.074450 0.074450 4.080748

PBC-CSRD -> CSRD 0.109988 0.123878 0.072843 0.072843 1.509935 LEVERAGE -> FINANCIAL

PERFORMANCE

-0.379814 -0.383544 0.071497 0.071497 5.312294

INTENTION CSRD -> CSRD 0.090960 0.103612 0.055252 0.055252 1.646256 SubjNORM-CSRD ->

INTENTION CSRD

0.205989 0.216453 0.086457 0.086457 2.382554

POSTURE -> CSRD 0.167737 0.172119 0.066073 0.066073 2.538655 CSRD -> FINANCIAL

PERFORMANCE

-0.149062 -0.159673 0.122535 0.122535 1.216484

ATTITUDE CSRD -> INTENTION CSRD

0.300053 0.303910 0.094140 0.094140 3.187314

SIZE-1 -> FINANCIAL PERFORMANCE

0.334072 0.366874 0.148833 0.148833 2.244610

SIZE -1 -> CSRD -0.039733 -0.115804 0.093500 0.093500 0.424952 SIZE -2 -> FINANCIAL

PERFORMANCE

0.112204 0.168189 0.110845 0.110845 1.012259

SIZE -2 -> CSRD 0.629794 0.636788 0.126231 0.126231 4.989234

Based on Table 6, the results of hypothesis testing were described as follows.

Hypothesis 1

Coefficient β value for ATTITUDE-CSRD to INTENTION-CSRD was 0.300053

and the t-statistic was 3.187314. Thus this study supports the hypothesis that states ‘The attitude of the managers toward the disclosure of CSR has a positive influence

on their intention to disclose the CSR.’

Hypothesis 2

Coefficient β value for SubjNORM-CSRD to INTENTION-CSRD was 0.205989 and

subjective norms of the managers toward the disclosure of CSR have a positive influence on their intention to disclose the CSR.’

Hypothesis 3

Coefficient β value for PBC-CSRD to INTENTION-CSRD was 0.303811 and the

t-statistic was 4.080748. Thus this study supports the hypothesis that states ‘The

control of the perceived behavior of the managers over the disclosure of CSR has a

positive influence on their intention to disclose the CSR.’

Hypothesis 4

Coefficient β value for CSRD to INTENTION CSRD was 0.090960 and the

t-statistic was 1.646256. Thus this study supports the hypothesis that states ‘The

intention of the managers to disclose the CSR has a positive influence on the

behavior of CSR disclosure.'

Hypothesis 5

Coefficient β value for PBC-CSRD to the CSRD was 0.109988 and t-statistic value

was 1.509935. Thus this study could not support the hypothesis that states ‘The

perceived behavior control of the managers over the disclosure of CSR has a positive influence on their intention to disclose the CSR.’

In this study the control variable POSTURE had a positive influence and was statistically significant for CSRD. This meant that Ullmann’s opinion (1985) that the

strategic posture is the company's response toward social demands is supported in

this study, that the company that has an active posture will make a lot of social

SIZE-2 (proxied using the log of total assets) had a positive influence and was

statistically significant for CSRD. This finding confirmed the existence of political

cost hypothesis (Watts and Zimmerman, 1986) and previous empirical studies

(Belkaoui, 1989; Kent and Chan, 2003) which concluded that a company makes a

disclosure of CSR in order to reduce its political visibility.

Hypothesis 6

Coefficient β value for CSRD to FINANCIAL PERFORMANCE was -0.149062 and

t-statistic value was 1.216484. Thus this study could not support the hypothesis that

states 'CSR disclosure has a positively correlated to corporate financial performance.'

5. Conclusion, Implications, Limitations, and Suggestions for Further Research Conclusion

The study produced the following main findings.

1. The disclosure of CSR in Indonesia was affected by the intention of the manager

to disclose CSR. The intention of the managers to disclose CSR was influenced

by three factors, namely the attitude of the managers towards the disclosure of

CSR, the subjective norms of the managers over the disclosure of CSR, and the

perceived behavioral control of the managers over the disclosure of CSR.

2. The perceived behavioral control over the disclosure of CSR does not affect the

disclosure of CSR. The perceived behavioral control over the disclosure may

affect the disclosure of CSR only when it preceded by managers intention to

disclose the CSR programs.

3. The disclosure of the CSR in Miscellaneous Industry, Consumer Goods

Industry has no effect on the companies’ financial performance for the period of

one year after the disclosure of the CSR. This means that the disclosure of CSR

in these five industries does not bring any values for the market and for the

companies themselves for the period of one year following the disclosure of the

CSR.

Implication

Theory. This study had proven that the company's practice of providing information to public is influenced by not only the observable factors related to

characteristic of the company, but also unobservable factors inherent in the manager

himself. This suggests that the socio-economic perspective can be used to describe

the practice of CSR disclosure.

The findings that CSR disclosure is not correlated to financial performance

have important implications in the teaching of accounting and financial reporting

practices by the company. In the teaching of accounting, the results of this study will

add the knowledge of lecturers and students about the economic benefits of CSR

disclosure. For companies, the findings of this study can be the subject of extensive

study in determining the extent of information that will be given to public.

Public Policy. This study had proven that the companies in Miscellaneous

Industry, Consumer Goods Industry, Basic and Chemicals Industry, Mining Industry,

and Agriculture Industry acquire no economic benefit from their decision to carry out

CSR activities. This means that the government's decision to legally oblige

companies to undertake CSR and disclose it (as stated in Article 74 paragraph (1)

and Artikel 66 of Company Act. No. 40/2007) did not bring any economic benefits to

This study found some variation in the disclosure of CSR among the

companies observed. The variation of the CSR makes it difficult to the public in

assessing and comparing the performance of CSR among the companies with CSR

programs. Therefore, the BAPEPAM-LK as regulator of financial reporting for

public companies should set standards for the disclosure of CSR, including the scope

of disclosure. Standardization of disclosure is necessary to reduce the variation of the

disclosure of CSR and, hence, it will facilitate the public in assessing and comparing

the performance of CSR among companies.

This study proves that shareholders, creditors, government, NGOs, and firms’

consultant affect managers in disclosing the CSR. This means that the government is

not the only "actor" that can ensure the success of CSR policy and its disclosure. The

government must socialize CSR policy intensively not only to managers, but also to

other parties which have certain concern in the company of interest, including issuing

continuum policy that requires the creditor of the company to include CSR as an

important consideration in any credit decision making.

Methodology. This study managed to establish a questionnaire to measure the constructs of intention, attitude and subjective norm with proven validity and

reliability. Therefore, this questionnaire can be used as a benchmark by the

researchers who will conduct research with these constructs.

Research Limitation

1. This research includes only behavioral variables which are considered in theory

of planned behavior, not variables that may affect behavior (e.g. self efficacy).

Although Ajzen (1991: 184) claims that PBC is compatible with self-efficacy,

constructs are not entirely identical. Moreover, Bandura (1986, 1992) as quoted

in Armitage and Conner (2001) states that self-control and self-efficacy are

different concepts. While the former is more general and includes external

factors, the latter is more focus on cognitive perception on control which is based

on internal control factors.

2. This research combines primary and secondary data. These two kinds of data are

difficult to combine due to the dissimilarity in their characteristics.

Future Research

Based on the limitations presented above, future study may need to consider the

followings:

1. To include variables other than those considered in planned behavior theory. The

difference of PBC and self-efficacy characteristics may open an opportunity for

future research to develop behavioral model in predicting CSR disclosing

behavior. Self-efficacy may be included in Planned Behavioral Theory and

incorporated as independent variable (in addition to PBC). This variable may also

be associated directly to CSR disclosure. Alternatively, self-efficacy can be used

as moderating variable that may affect the relationship between PBC and CSR

disclosing behavior.

2. The development of a new model that may separate primary and secondary data