59

ACTIVITY BASED COSTING AND TIME-DRIVEN ACTIVITY BASED

COSTING: TOWARDS AN INTEGRATED APPROACH

Alex Santana,

1Paulo Afonso

1*and Ana Maria A. C. Rocha

21 Research Centre for Industrial and Technology Management, University of Minho, Portugal 2Algoritmi Research Centre, University of Minho, Portugal

* Corresponding author: [email protected], University of Minho, Campus of Azurém, 4800-058, Guimarães, Portugal

KEYWORDS

Cost Management, Activity Based Costing, Time-Driven Activity Based Costing,

ABSTRACT

Activity Based Costing (ABC) methods and models have been presented in the literature as sophisticated approaches for cost management and costing purposes. Kaplan and

Norton’s Time-Driven Activity Based Costing (TDABC) represented an update or improvement of the initial ABC models proposed by Cooper and Kaplan. The relevance and applicability of the TDABC approach is still an open question. The purpose of this paper is to discuss TDABC from a critical analysis of the literature, checking and comparing methodologies and research techniques, as well as contributions to mitigate difficulties encountered in the implementation of the model. As a result, it is established a relation between ABC and TDABC approaches and an integrated TDABC-ABC model and methodology is proposed. Some ideas for future work and management implications are also discussed.

INTRODUCTION

Studies addressing a critical analysis of the literature are a kind of research often used to survey the quantity and quality of articles on a topic that is considered relevant to a particular area. This type of study is important because it maps the authors involved, in turn, researchers are contributing to promote science. The theme Activity Based Costing (ABC) and Time-Driven Activity Based Costing (TDABC) will help to verify how the studies are being discussed within the academy, as it makes the survey of the area, through the themes addressed in the research. The ABC is a costing system based in activities, that arose as a consequence of the recognition that traditional systems no longer met the new practices of companies, requiring adaptation to new market conditions and assuming a new cost structure. However, in an attempt to reduce some limitations of ABC, Kaplan and Anderson (2004) propose another approach to this methodology: Time-driven ABC (TDABC). This approach uses new tools, such as the time equations (equations time). Additionally, among other innovations, eliminates the need to carry out interviews with staff, which would serve to assess what activities they work for a period.

Therefore, the aim of this article is to discuss TDABC from a critical analysis of the literature, checking and comparing methodologies and research techniques, as well as contributions to mitigate the difficulties encountered in implementing the model. As a result, it is an established relationship between ABC and TDABC.

This article is divided into, with introduction, concepts necessary for a proper understanding of the study. Then, the methodology used to develop the research is described. Subsequently, the results are displayed and discussed. Finally, the concluding remarks are outlined.

STATE OF THE ART

Activity Based Costing

The ABC or Activity Based Costing enables a detailed analysis of the costs of a product, giving attention to the activities and processes that characterize the organization's business (Swenson, 1995). ABC is a particularly appropriate methodology to deal with complex and diverse manufacturing systems (Afonso and Paisana, 2009), which allows support strategic decision making at the level of three distinct areas: the definition of the price of the products, the production mix and the development and design of new products (Mitchell & Innes, 1998).

Regarding the production mix, ABC allows to measure the cost and performance of activities and cost objects, based on three basic premises: products require activities, activities consume resources and resources cost money (Afonso, 2002). Conceptually Kaplan (1984) summarizes these assumptions: the various activities consume resources and products, in turn, consume activities. As this methodology assumes that not all costs can be related to production volume or the volume of direct use of resources, these are treated more strictly (Afonso, 2002), thus making the overhead on an element more noticeable, ie makes the chargeable overhead (Tippett & Hoekstra, 1993). ABC is assumed to improved precision with respect to the product cost when compared to traditional systems (Tsai, 1996).

60 stagnated or dropped their use in the enterprise, due to the difficulty of training and employee engagement on the potential of the tool.

Kaplan and Anderson (2004 ) recognized the limitations of the method and understood that criticism was justified by the following factors: (i) high investment to implement the method, (ii) complexity to keep it in the company and (iii) difficulty to modify when needed.

Time-Driven Activity Based Costing

In this context, emerged the Time-Driven Activity Based Costing (TDABC), that is a variation of the ABC system but with a simpler and friendlier operation for execution times of the activities necessary to produce the product or provide the service (Dalci , Kosan & Tanis, 2009). A TDABC system is presented in the form of time equations which reflect the costs of different cost objects taking into account the particularities of consumption that these are the various activities that characterize the production processes or business analysis.

There are several case studies on the implementation of the model TDABC, where their advantages were observed, namely that it is a model of easy construction, ease of integration with management software and the ease of obtaining information about the consumption of resources by cost objects (Pernot, Roodhooft & Abbeele, 2007). Through the TDABC is possible to study the effectiveness of the processes at the level of available capacity versus capacity utilization (Kaplan & Anderson, 2007). These authors argue that the "time-equations" or cost equations result in a simpler and less costly system than the traditional ABC methodology.

Among other advantages, the model TDABC allows assess the added value that determines the existence of each activity, simulating the operationalization of resources and test processes of rationalization of capacity used or defray the cost of the unused time. But also limitations were noted in some case studies in which, for example, have been required there was the fact that a huge amount of data for estimating the time equations (Varila, Seppanem & Suomala, 2007).

The TDABC is supported on two parameters underlying, the cost per unit time capacity and time required to complete an activity (Kaplan, 2007). The TDABC is a simpler system more affordable and economically much more powerful system than the ABC. It simplifies the process of costing and eliminates the surveys and interviews of a typical system ABC (Kaplan, 2007). The model TDABC assigns costs of resource directly to cost objects (Kaplan, 2007). So, first the costs of all resources (equipment, personnel, etc.) are calculated and are divided by the capacity, giving the time when the work is effectively executed. Secondly, the model distributes costs of the resources using the rate of the cost of capacity, estimative resource requirements for each cost object (typically considered time as a measure of this capacity) (Everaert et al., 2006).

It should be pointed out that the model only requires estimation of time to process customer orders, not being

necessary that they are equal, since the model allows the estimation of several times depending on the specific characteristics of each application using dummy variables and equations.

Differences between ABC versus TDABC

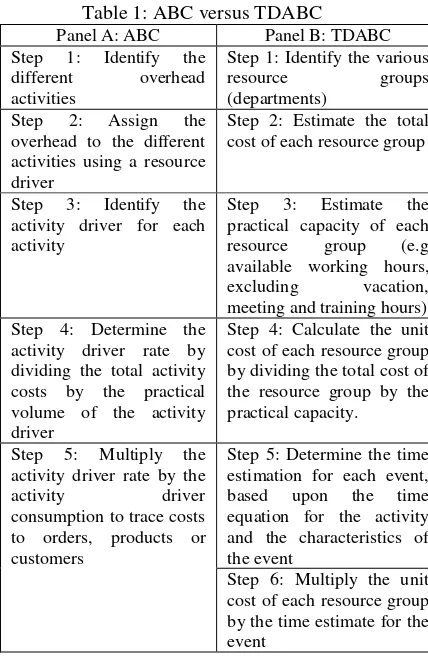

The differences between the steps for the implementation of ABC and TDABC models are presented in Table 1. (Source: Everaert, Bruggeman and De Creus, 2008),

Table 1: ABC versus TDABC

Panel A: ABC Panel B: TDABC

Step 1: Identify the

different overhead

activities

Step 1: Identify the various

resource groups

(departments)

Step 2: Assign the

overhead to the different activities using a resource driver

Step 2: Estimate the total cost of each resource group

Step 3: Identify the activity driver for each activity

Step 3: Estimate the

practical capacity of each

resource group (e.g

available working hours,

excluding vacation,

meeting and training hours) Step 4: Determine the

activity driver rate by dividing the total activity costs by the practical volume of the activity driver

Step 4: Calculate the unit cost of each resource group by dividing the total cost of the resource group by the practical capacity.

Step 5: Multiply the activity driver rate by the

activity driver

consumption to trace costs to orders, products or customers

Step 5: Determine the time estimation for each event,

based upon the time

equation for the activity and the characteristics of the event

Step 6: Multiply the unit cost of each resource group by the time estimate for the event

In an ABC, rates of cost drivers are used to distribute the costs of a department to each cost object, for example based on the number of requests, number of complaints from customers (Kaplan and Anderson, 2007).

Regarding TDABC, the phase of definition of resource consumption by the activities is ignored, so there is not necessary to allocate such costs. In this cost model there are used time equations, which directly distribute resources costs of the activities performed and processed transactions to cost objects (Kaplan and Anderson, 2007).

METHODOLOGY

61 emerging, in order to discuss matters with a great degree of intensity.

Descriptive research is concerned to observe, register, analyze, classify and interpret the facts without the interference of the researcher (Andrade, 2002). The qualitative approach, according to Denzin & Lincoln (2006), “involves the study of the use and collection of a variety of empirical materials that describe routine and problematic moments and meanings in one's life”. In the literature it can be conceptualized as a systematic study that is based on materials published in books, magazines, newspapers, electronic databases, i.e., materials that are available to the general public (Vergara, 2005).

Based on the study of Srivastava (2007), the research is driven by theoretical pre-considerations and follows a clear process, as this allows conclusions to be drawn on the reviewed literature. It may be classified as an archival research method in the framework for conducting and evaluating research suggested by Searcy and Mentzer (2003). Our process of analysis comprised the following steps:

• Definition of the unit of analysis: the unit of analysis has been defined as a single research paper. We further delimited the material in the research papers which should be analysed considering the research scope;

• Classification context: We selected and defined the classification context to be applied in the literature review to structure and classify the material, checking and comparing methodologies and research techniques, as well as contributions to mitigate difficulties encountered in the implementation of the model;

• Collecting publications and delimiting the field: our literature review focused upon papers and journal articles only. To establish a time span, a starting point was set at 2004. This seems justified, as the beginning of the debate on TDABC can be traced to this period. Library databases they were found were used where a keyword search using

some important keywords such as ‘TDABC, ‘Time-Driven

ABC’, ‘Time-Driven Activity Based Costing’.

Thus, within our defined objective, this work integrates and takes forward the literature on Time-Driven ABC since its conceptualization. According with the database, they were found and analyzed 24 items in the topic.

FINDINGS

Initially, an analysis of published articles was conducted to ascertain what were the forms of research. The application of the model was studied and also the existence of other theories and models related with TDABC were verified, according to Figure 1.

Figure 1: Application of TDABC

The objective of the study was to verify, through published articles, how the ABC model has contributed to the development of TDABC model. A thorough analysis of published articles was undertaken.

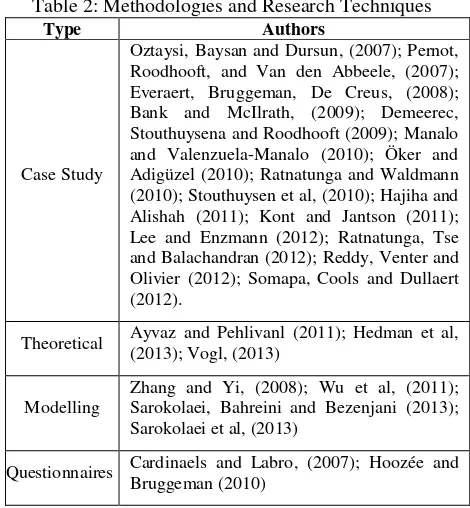

Table 2: Methodologies and Research Techniques

Type Authors

Case Study

Oztaysi, Baysan and Dursun, (2007); Pernot, Roodhooft, and Van den Abbeele, (2007); Everaert, Bruggeman, De Creus, (2008); Bank and McIlrath, (2009); Demeerec, Stouthuysena and Roodhooft (2009); Manalo and Valenzuela-Manalo (2010); Öker and Adigüzel (2010); Ratnatunga and Waldmann (2010); Stouthuysen et al, (2010); Hajiha and Alishah (2011); Kont and Jantson (2011); Lee and Enzmann (2012); Ratnatunga, Tse and Balachandran (2012); Reddy, Venter and Olivier (2012); Somapa, Cools and Dullaert (2012).

Theoretical Ayvaz and Pehlivanl (2011); Hedman et al, (2013); Vogl, (2013)

Modelling

Zhang and Yi, (2008); Wu et al, (2011); Sarokolaei, Bahreini and Bezenjani (2013); Sarokolaei et al, (2013)

Questionnaires Cardinaels and Labro, (2007); Hoozée and Bruggeman (2010)

62 For Oztaysi, Baysan and Dursun, (2007), one of the main advantages of TDABC over ABC is that the calculations are primarily based on measuring resource consumption which facilitates the formation of a simulation integrated cost justification methodology. According to the authors, the methods complement each other and the contribution reduces costs and have the potential to serve more deliveries with the same resources.

Pernot, Roodhooft, and Van den Abbeele, (2007) did not find significant difficulties when showing the ease and speed in building an accurate model, the integration with integrated management systems and the availability of accurate information. ABC also appeared to cause two significant problems. First, setting up an ABC system can be very costly, especially if the current accounting system does not support the collection of ABC information. Second, the system needs to be regularly updated, which further increases its cost. It was emphasized the benefits brought by TDABC empirically analyzed in organizations. The difficulties were hardly mentioned. It is believed that, due to the small number of samples analyzed in the study of these authors, it was not possible to conclude on the difficulties encountered in implementing the methodology TDABC.

However, despite the many advantages of TDABCpointed out by the proponents of this costing method, some criticisms have been made by some researchers. Cardinaels and Labro (2008), for example, through a study of students in a University, said that estimates of employees might not be as accurate as Kaplan and Anderson (2004). In this case, a significant degree of subjectivity is still found in TDABC, the same as in conventional ABC. Sherratt (2005), in turn, states that the TDABC is restricted to some routine and pre-determined activities.

Bank and McIlrath (2009) reconducted a study in a children's hospital, where the TDABC model was utilized to estimate costs of provider resources and was applied to three specific clinical scenarios common to any ED service. In conclusion, ED process improvements that lead to a modest decrease in patient waiting time, may achieve

larger, proportional decreases in the ED’s LWBS rate.

Although decreased waiting time in our setting was

achieved by “front-end” process improvement, “back-end”

strategies that reduce total ED census may have a greater effect on reducing the LWBS rate due to the strong association between LWBS and total ED census. It is still possible to lower LWBS rates during periods of increasing ED census and congestion.

The search of Everaert, Bruggeman and De Creus (2008) was performed on a wholesale company. For them, TDABC is extremely satisfying to cost models of complex logistics operations, especially those that require numerous tasks. For the authors, in each task, or even sub-task, it is possible to identify a time driver. These tasks can be, according to the method of study used, included in an equation of time. Moreover, these authors explained that the cost information generated by TDABC are more accurate than those generated by conventional ABC. They also stated that the new ABC approach provides better

analysis of customer profitability and efficiency of logistics processes than other costing methods. Finally, integration with ERPs was cited as another substantial advantage of TDABC. They were not mentioned difficulties in the implementation of the methodology in TDABC. However, it is noted that the research requires a series of interviews with company employees. In this case, it was observed that these interviews consisted of an obstacle to be overtaken by the executors of the new ABC approach. Furthermore, the authors emphasized that the involvement of employees in the application of TDABC seems to be fundamental. Thus, one can say that employee engagement is another problem identified in this research.

Demeere, Stouthuysen and Roodhooft (2009) stated that the TDABC system seems to be well suited since it incorporates next to the advantages of the traditional ABC system some extra features like faster model adaptability, a simpler set-up and a higher reflection of the complexity of the real-world operations. The TDABC model in this paper was set up for five different departments: Urology, Gastroenterology, Plastic Surgery, Nose-Throat and Ears and Dermatology. The TDABC system challenged healthcare managers and department heads to identify and analyze the underlying activities that drove the overhead costs. Thus, the TDABC analysis allowed managerial recommendations concerning improvement opportunities. Furthermore, the TDABC approach introduced a healthy competition and an open communication between the different departments concerning possible operational improvements. The introduction of interactive meetings on business and operational matters promoted inter-hierarchical and more important inter-disciplinary (between physicians and managers) communication. Finally, while the interaction between cost-accounting systems and strategy has been frequently viewed as a passive one, in this study the TDABC information clearly

improved the department heads and healthcare managers’

understanding of the different organizational processes. Hence, the clinic’s management was able to pursue

strategic changes that increased the value and effectiveness of the current and future outpatient clinic.

63 operational improvements during the design process of a time-driven ABC system, collective worker participation and appropriate leadership styles are indispensable.

In the study Manalo and Valenzuela-Manalo (2010) , deals with a framework that combines the complementary features of ABC and TDABC. The framework or Standard Activity Measurement Plan is anchored in the computing unit cost given the required minimum resources for a particular activity. The activity unit cost is standard and fixed for a certain period until such time significant variables change significantly. The standard unit time per activity is also used to establish the percentage of time spent. In this manner, ABC data collection is minimized if not eliminated totally. TDABC is not a replacement of the traditional ABC. They should complement each other. Their strengths should be combined to minimize their weaknesses. Thus, the Standard Activity Measurement Plan (StAMP) is developed to combine the complementary features of both methods.

Öker and Adigüzel (2010), demonstrates the implementation of TDABC in a manufacturing company, showing how it can provide far more relevant information about product profitability and capacity utilization than standard costing. The benefit of TDABC is to enable capacity utilization analysis. Through capacity utilization analysis, the company can determine the excess capacity. The management of the company can eliminate the excess capacity, which means extra cost for the company. The conclusion from the study is that the TDABC model is more appropriate and easier for service companies to implement than the manufacturing companies. This is because the capacities are generally measured in terms of labor times, and sometimes it is difficult for manufacturing companies to measure capacity in terms of labor time. Ratnatunga and Waldmann (2010) found that TDABC is

preferable to ABC in the TC modelling of ‘research only’

departments and institutes; both approaches do not provide

accurate information in ‘teaching and research’

departments. In these departments more accurate estimations could be obtained from studying the workload allocation methods and conducting direct interviews of the staff undertaking research on ACG and other externally funded grants. The TDABC model is a variant of the ABC model which is specifically designed to simplify the implementation and maintenance of activity-based cost management systems (Kaplan & Anderson, 2004; Kaplan & Anderson, 2007). The TDABC has an advantage over ABC in the service organizations, however when obtaining

‘equivalent-time’ for the research activity of staff in teaching departments will result in erroneous estimates of research effort over a annual period, and thus the costs of data collection would far outweigh the benefits (if any). However, such estimations would be more relevant in university departments and research institutes that are only conducting research. Here, overall estimations based on

‘in-situ’ observations, face-to-face interviews and the study of comparative information could be used for TDABC modelling.

The study of Stouthuysen et al. (2010) describes the development and application of a TDABC system for a small to medium sized academic library in a Belgian University. The TDABC may improve the cost management of several library processes, only focusing on the acquisition process. More specifically, the acquisition process concerns print formats (books, journals and grey literature) and covers key traditional acquisition concepts (ordering, receiving, paying, and using integrated library systems and online vendor databases in an acquisition's workflow). The implementation of the TDABC model revealed much about the acquisition process. Using this TDABC information, library management was able to identify several factors that drive the cost of the acquisition process of library items. The TDABC model indicated that the acquisition of local books was far more expensive than the acquisition of other items due to the use of specific purchasing software. Secondly, TDABC information revealed that pooling of activities could lead to substantial time and cost savings. Finally, TDABC cost information demonstrated that costs increase considerably if category a personnel are involved in the acquisition process.

Hajiha and Alishah (2011) verified the implementation feasibility of TDABC in hospitality industry and analyzed profitability of various costumer groups by this system in Iranian context. The results showed that using TDABC model, in comparison with the existing traditional system in Parsian Hotel, provides more proper data on cost and profitability of customers. Also, the proposed model distinguishes non-added value activities and demonstrates real capacity of each parts of the hotel. can calculate necessary time for activities by time equations in TDABC. According to the results, it allowedmanagers to design an optimized strategy to increase productivity and improve processes. Consequently, time equations provide this situation for a manager to update the equations without doing repeating and time-consuming interviews. TDABC enables the managers to know about the existing capacities and exploit human resources more and better.

The study of Kont and Jantson (2011) provides an overview of how university libraries research and adapt

new cost accounting models, such as “activity-based

costing” and “time-driven activity-based costing”, focusing on the strengths and weaknesses of both methods to determine which of these two is suitable for application in university libraries. However, setting up an ABC system can be very costly, and the system needs to be regularly updated, which further increases its costs. The TDABC system can not only be implemented more quickly (and thus more cheaply), but also can be updated more easily than the traditional ABC, which makes the TDABC the more suitable method for university libraries. The TDABC

considers many aspects that affect employees’ efficiency

and performance, e.g., rest periods, personal time for breaks, arrival and departure, and communication and reading unrelated to actual work performance.

64 implementation process of TDABC. By taking a case, it demonstrates the applications of this model and the effects on cost account by errors. The emphasis is laid on the demonstration of data source in the model's applications. After the construction of the TDABC model it was verified that there are three types of errors, aggregation, specification and measurement. There was then studying the effects brought by these three types of errors in the calculation of the cost model.

In TDABC model, it is generally presumed that the cost of direct resources can be directly allocated to cost objects. It is assumed that direct costs are measured without error for every cost object, and hence excluded from the analysis; as far as the share of the cost in indirect resources is concerned. There are generally three kinds of errors: aggregation error (AE), specification error (SE) and measurement error (ME). Concluding that TDABC model can give misleading information.

The authors Lee and Enzmann (2012) applied the model TDABC in a radiology department in the U.S.. The study found that, according to the current model, there was a difference of values. With the application of TDABC was really verified what are the costs related to each patient and helped to manage the porting department. There was no difficulty in deploying TDABC model, and there was no comment on the traditional ABC.

For Ratnatunga, Tse and Balachandran (2011) the ABC model, despite its theoretical superiority, has had only moderate success in replacing the traditional volume-based absorption costing models in complex organizations worldwide. Even in organizations that have launched ABC projects, the implementations often do not sustain. In response to this general lack of enthusiasm worldwide for ABC, accountants developed the TDABC model as an alternative cost allocation model. A comparison between the two models considers the TDABC easier to implement, from an international perspective, and provides comparable cost information for decision making. The research is a case study to ascertain if any country‐specific factors prevent the ABC implementation. To conclude: the TDABC model has similar implementation complexities to ABC if modelling conditions are strictly respected to; these complexities are independent of country‐specific factors; and in its simplest form, the model generates the same decision information errors of traditional costing.

In the paper of Reddy, Venter and Olivier (2012) the ABC is discussed since it is the basis from which TDABC was derived. TDABC was developed to help to overcome the problems with ABC which resulted in ABC having a low rate of uptake. The advantages of TDABC are classified into three areas: cost, ease of use and/or maintenance, and accuracy. The cost TDABC is cheaper to implement due to the fact that the TDABC process is simpler. In this regard TDABC differs from traditional costing methods that do not provide cost information at the activity and task level cost. Similarly, the use management TDABC, you need to consider issues such as the potential for resistance that may be encountered as a result of increased cost transparency.

Somapa, Cools and Dullaert (2012) reports on the development of a TDABC model in a smallsized road transport and logistics company. Activity-based costing leads to increased accuracy benefiting decision-making, but the costs of implementation can be high. TDABC tries to overcome some of the disadvantages of ABC and seems particularly useful for the road transport and logistics sector. However, the lack of quantitative data on cost drivers remains a problem. TDABC has advantages over traditional ABC which works well in the limited setting in which it was initially applied, typically a single department, plant or location, but becomes difficult when rolling out on a large scale on an ongoing basis.

According to Sarokolaei, Bahreini and Bezenjani (2013), Namazi (2009) introduced the third generation of ABC as Performance Focused Activity Based Costing (PFABC). This system, unlike TDABC that has a great emphasis on time driver, allow select the appropriate cost drivers and has more flexibility in allocating costs to activities. In fact, PFABC first allocates costs to activities, then allocates costs to products. However, this system like other costing systems is face with the phenomenon of ambiguity and uncertainty in estimating of standards as system input. To solve this problem, in this article, it has been trying for the first time using fuzzy logic to reduce of ambiguity and uncertainty in PFABC in the estimation of standards. Finally, the new system will be introduce as Fuzzy Performance Focused Activity Based Costing (FPFABC). Sarokolaei et al, (2013b) used fuzzy logic to compensate the lack of absolute data in time driven activity based counting system and design a new system entitled: fuzzy time driven activity based costing, to minimize the error coefficients of data by the new system. Time driven activity based costing system is broadly relying on time estimations and it is principally abstract. If the least error occurs in estimating the key time activities, this system will result in damaging effects which are sometimes broader than the negative effects of not using this system. Thus, it should try to use fuzzy logic in order to minimize errors in time estimations and managers should make decisions with higher assurance levels. Finally it can be stated that using fuzzy time driven activity based costing not only will result in losing the data in time driven activity based costing system, but also it will present more complete and accurate data for managers besides supplying the data.

The main objective in Vogl (2013) was to develop ways to improve patient-level cost apportioning (PLCA) in the

English and German inpatient ‘DRG’ cost accounting

65

Concluding, a best available PLCA standard in ‘DRG’ cost

accounting uses: (1) the cost-matrix from the German system; (2) a third axis in this matrix, representing service-lines or clinical pathways; (3) a scoring system for key cost drivers with the long-term objective of time-driven activity based costing and (4) a point of delivery separation. Both systems have elements that the other system can learn from. By combining their strengths, regulators are supported in enhancing PLCA systems, improving the accuracy of national reimbursement and the managerial relevance of inpatient cost accounting systems, in order to reduce costs in health care.

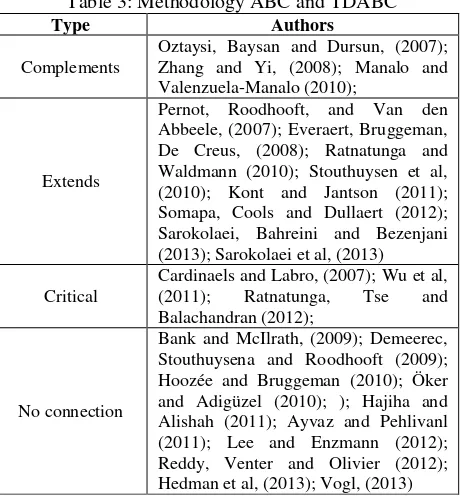

One of the proposals of the article was to determine which contributions regarding the ABC model in the new methodology TDABC.

Table 3: Methodology ABC and TDABC

Type Authors

Complements

Oztaysi, Baysan and Dursun, (2007); Zhang and Yi, (2008); Manalo and Valenzuela-Manalo (2010);

Extends

Pernot, Roodhooft, and Van den Abbeele, (2007); Everaert, Bruggeman, De Creus, (2008); Ratnatunga and Waldmann (2010); Stouthuysen et al, (2010); Kont and Jantson (2011); Somapa, Cools and Dullaert (2012); Sarokolaei, Bahreini and Bezenjani (2013); Sarokolaei et al, (2013)

Critical

Cardinaels and Labro, (2007); Wu et al,

(2011); Ratnatunga, Tse and

Balachandran (2012);

No connection

Bank and McIlrath, (2009); Demeerec, Stouthuysena and Roodhooft (2009); Hoozée and Bruggeman (2010); Öker and Adigüzel (2010); ); Hajiha and Alishah (2011); Ayvaz and Pehlivanl (2011); Lee and Enzmann (2012); Reddy, Venter and Olivier (2012); Hedman et al, (2013); Vogl, (2013)

An important contribution was to verify the contributions which argue articles about the ABC model and TDABC analyzing whether these methodologies complement, extend or contribute nothing.

CONCLUSIONS AND FURTHER RESEARCH

This article aims to discuss TDABC from a critical analysis of the literature, checking and comparing methodologies and research techniques, as well as contributions to mitigate the difficulties encountered in implementing the model. As a result, it is established the relationship between ABC and TDABC approaches and integrated TDABC - ABC model and the methodology is proposed. Opportunities for future work and managerial implications are also discussed.

As a final result, we analyzed 24 studies published in the ISI database, and the surveys were implemented in many countries, different sectors and by various authors, an essential contribution in order to have an understanding of this management tool.

The analyzes were performed 16 studies that applied the model and 08 studies that used combined with the theories TDABC model. In studies where the model was applied, it was able to identify the application process, as well as the contributions and limitations. Among the contributions, cost control, and a simple model can be rapidly applied and a tool that provides data for managerial decision making contributions that correspond to Kaplan and Anderson (2004, 2007). Regarding the difficulties, the main identified relates to the formulation of the equations of time. It was observed that a large volume of data is required for validation. Moreover, their applicability in unstable environment in which the activities are not routine, is apparently very limited.

Finally , there is the general characterization of how the method is being researched costing TDABC. We notice that this is a much studied under several different optical and some little explored by researchers whose mission is the development of studies that bring relevant news to the method.

As a recommendation for future research, we suggest the investigation of other means of publishing papers related to the topic in discussion.

ACKNOWLEDGMENTS

The first author acknowledges CAPES - BEX 1066/13-7 for the PhD grant. This work has also been supported by FCT in the scope of the projects: PEst-OE/EME/UI0252/2014 and PEst-OE/EEI/UI0319/2014.

REFERENCES

Afonso, P. (2002). “Sistemas de custeio no âmbito da

contabilidade de custos: O custeio baseado nas actividades, um modelo e uma metodologia de

implementação”, Dissertação de Mestrado, Mestrado em

Engenharia Industrial, Universidade do Minho.

Afonso, P. S., & Paisana, a. M. (2009). An algorithm for activity based costing based on matrix multiplication. IEEE International Conference on Industrial Engineering and Engineering Management, 920–924.

Alishah, Samad Safari and Hajiha, Z. (2011). Implementation of Time-Driven Activity-Based Costing System and Customer Profitability Analysis in the Hospitality Industry: Evidence From Iran. Economics and Finance Review, 1(8), 57–67.

Andrade, M. M. (2002). Como preparar trabalhos para cursos de pós-graduação: noções básicas. 5 ed. São Paulo: Atlas, 154 p.

Ayvaz, Ednan, D. P. (2011). The Use of Time Driven Activity Based Costing and Analytic Hierarchy Process Method in the Balanced Scorecard Implementation. International Journal of Business and Management, 6(3), 146–158. Bank, D. E., & McIlrath, T. (2009). 13: Utilizing Time-Driven

Activity-Based Costing in the Emergency Department.

Annals of Emergency Medicine, 54(3), S5.

doi:10.1016/j.annemergmed.2009.06.033

66 Cardinaels, E., & Labro, E. (2008). On the Determinants of

Measurement Error in Time-Driven Costing. The Accounting Review, 83(3), 735–756.

Cassel, C. & Symon, G. (2004). Essential Guide to Qualitative Methods in Organizational Research. SAGE Publications Inc.

Cucuzza, T. G &.Ness, J. (1995). Tapping the full potential of ABC. Harvard Business Review, vol. 95, pp. 130-138. Dalci, I.; Tanis, V. & Kosan, L. (2010). "Customer

profitability analysis with time-driven activity-based costing: a case study in a hotel", International Journal of Contemporary Hospitality Management, Vol. 22 (5), pp.609 – 637.

Demeere, N., Stouthuysen, K., & Roodhooft, F. (2009). Time-driven activity-based costing in an outpatient clinic environment: development, relevance and managerial impact. Health Policy (Amsterdam, Netherlands), 92(2-3), 296–304. doi:10.1016/j.healthpol.2009.05.003

Denzin, N. K. & Lincoln, Y. S. (2006). O planejamento da pesquisa qualitativa: teorias e abordagens. 2 ed. Porto Alegre: Artmed.

Everaert, P., Bruggeman & De Creus, G. (2008). Sanac Inc.: From ABC to time-driven ABC (TDABC) - An Instrictional case. Journal of Accounting Education 26, 118-154.

Hedman, R., Sundkvist, R., Almström, P., & Kinnander, a. (2013). Object-oriented Modeling of Manufacturing Resources Using Work Study Inputs. Procedia CIRP, 7, 443–448. doi:10.1016/j.procir.2013.06.013

Hoozée, S., & Bruggeman, W. (2010). Identifying operational improvements during the design process of a time-driven ABC system: The role of collective worker participation and leadership style. Management Accounting Research, 21, 185–198. doi:10.1016/j.mar.2010.01.003

Innes, J. & Mitchell, F. (1998), A Practical Guide To Activity Based Costing, Kogan Page, Londres.

Kaplan, R. S. (1984). "Yesterday's Accounting Undermines Production", Harvard Business Review, July/August, pp. 133-139.

Kaplan, R. S. & Steven R. A. (2004). "Time-Driven Activity-Based Costing." Harvard Business Review 82, no. 11, 131–138.

Kaplan, R. S. & Andersen, S. R. (2007). Time-Driven Activity-Based Costing: A Simpler and More Powerful Path to Higher Profits.

Kont, K., & Jantson, S. (2011). Activity-Based Costing (ABC) and Time-Driven Activity-Based Costing (TDABC): Applicable Methods for University Libraries? Evidence Based Livrary and Information Practice, 6(4), 107–119. Lee, C. I., & Enzmann, D. R. (2012). Measuring radiology’s

value in time saved. Journal of the American College of

Radiology : JACR, 9(10), 713–7.

doi:10.1016/j.jacr.2012.06.022

Manalo, R G, M. D. V.-M. (2010). Standard Activity Measurement Plan. Proceedings of the 2010 IEEE IEEM Output., 2470–2474.

Öker, Figen, A. H. (2010). Time-Driven Activity-Based Costing: An Implementation in a Manufacturing Company. The Journal of Corporate Accounting & Finance, 75–92.

Oztaysi, B., Baysan, S., & Dursun, P. (2007). A Novel Approach for Economic-Justification of RFID Technology in Courier Sector: A Real-Life Case Study. 1st Annual

RFID Eurasia, 1–5.

doi:10.1109/RFIDEURASIA.2007.4368147

Pernot, E., Roodhooft, F., & Van den Abbeele, A. (2007). Time-Driven Activity-Based Costing for Inter-Library Services: A Case Study in a University. The Journal of Academic Librarianship, 33(5), 551–560.

Ratnatunga, J., Tse, M. S. C., & Balachandran, K. R. (2012). Cost Management in Sri Lanka: A Case Study on Volume, Activity and Time as Cost Drivers. The International

Journal of Accounting, 47(3), 281–301.

doi:10.1016/j.intacc.2012.07.001

Ratnatunga, J., & Waldmann, E. (2010). Transparent Costing: Has the emperor got clothes? Accounting Forum, 34, 196– 210. doi:10.1016/j.accfor.2010.08.005

Reddy, K., Venter, H. S., & Olivier, M. S. (2012). Using time-driven activity-based costing to manage digital forensic readiness in large organisations. Information Systems Frontiers, 14, 1061–1077. doi:10.1007/s10796-011-9333-x Sarokolaei, M. A., Bahreini, M., & Bezenjani, F. P. (2013). Fuzzy Performance Focused Activity based Costing (PFABC). Procedia - Social and Behavioral Sciences, 75, 346–352. doi:10.1016/j.sbspro.2013.04.039

Sarokolaei, M. A., Saviz, M., Moradloo, M. F., & Dahaj, N. S. (2013). Time Driven Activity based Costing by Using Fuzzy Logics. Procedia - Social and Behavioral Sciences, 75, 338–345. doi:10.1016/j.sbspro.2013.04.038

Searcy, D.L. and Mentzer, J.T. (2003). A framework for conducting and evaluating research. Journal of Accounting Literature, 22, 130–167.

Shrivastava SK (2007): Green- supply management: a state-of-art literature review. International Journal of Management Reviews 9 (1): 53-80.

Somapa, S., Cools, M., & Dullaert, W. (2012). Unlocking the potential of time-driven activity-based costing for small logistics companies. International Journal of Logistics

Research and Applications, 15(5), 303–322.

doi:10.1080/13675567.2012.742043

Stouthuysen, K., Swiggers, M., Reheul, A.M., & Roodhooft, F. (2010). Time-driven activity-based costing for a library acquisition process: A case study in a Belgian University. Library Collections, Acquisitions, and Technical Services, 34, 83–91.

Swenson, D. (1995), "The benefits of activity-based Cost Management to the manufacturing industry", Journal of Management Accounting Research, vol. 7, pp. 167-180.

Tippett, Donald. (1993). “Activity-based costing: a manufacturing Management Decision-aid”, Engineering Management Journal, vol. 5, n.º 2; pp. 37-42.

Tsai, W. (1996). “Activity-Based Costing Model for Joint

Products”, National Central University, Taiwan.

Varila, M.; Seppanem, M. & Suomala, (2007). Detailed

cost modeling: a case study in warehouse

logistics. International Journal of Physical Distribution & Logistics Management. v. 37. pp.184 – 200

Vergara, Sylvia Constant. (2005). Métodos de pesquisa em administração. São Paulo: Atlas.

Vogl, M. (2013). Improving patient-level costing in the

English and the German “DRG” system. Health Policy,

109(3), 290–300.

Zhang, X., & Yi, H. (2008). The Analysis of Logistics Cost Based on Time-Driven ABC and TOC. IEEE 18th International Conference on Industrial Engineering and Engineering Management, 1631–1635.