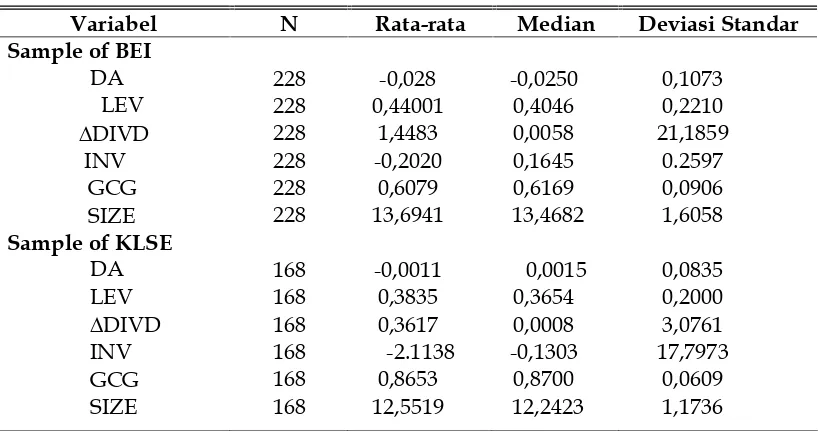

THE INFLUENCE OF FINANCIAL POLICIES ON EARNINGS MANAGEMENT, MODERATED BY GOOD CORPORATE GOVERNANCE Wahidahwati

Teks penuh

Gambar

Dokumen terkait

a. poster paling besar ukuran 40 cm x 60 cm. Desain dan materi Bahan Kampanye sebagaimana dimaksud pada angka 1 dibuat dan dibiayai oleh Pasangan Calon dan/atau Tim

Upaya diplomatik dilakukan terhadap negara-negara Eropa yang telah lebih dahulu menguasai wilayah Amerika utara seperti Inggeris, Perancis, Rusia dan Spanyol. Sejak tahun

Vane air flow meter juga memiliki sebuah sakelar untuk memgerakkan relay pompa bensin yang dihubungkan dengan plat pengukur, jika mesin tidak distart maka

Preliminary tests showed a good correspondence between estimated temperatures and measured ground surface temperatures (RMS error less than 20 C) except for some

Sedangkan fungsi social adalah fungsi yang dimainkan zakat untuk membiayai proyek-proyek social yang dapat juga diteruskan dalam kebijakan penerimaan dan pengeluaran negara dalam

Tujuan penelitian ini untuk mengetahui apakah Consumer Animosity berpengaruh terhadap Consumer Ethnocentrisme, untuk mengetahui apakah Country of Origin Reputation

Adapun perumusan masalah yang akan dibahas dalam penelitian meliputi: Berapa besarnya pencapaian rasio likuiditas, rasio solvabilitas, rasio aktivitas, dan rasio

Makalah ini akan mengulas aplikasi kombinasi metode filtrasi dan fitoremidiasi dengan menggunakan tanaman eceng gondok ( Eichhornia crassipes Mart. Solms .) serta kemampuannya