Monetary Policy Review

June 2010

The Monetary Policy Review (MPR) is published monthly by Bank Indonesia after the Board of Governors’ Meeting each February, March, May, June, August, September, November, and December. This report is intended as a medium for the Board of Governors of Bank Indonesia to present to the public the latest evaluation of monetary conditions, assessment and forecast for the Indonesian economy, in addition to the Bank Indonesia monetary policy response published quarterly in the Monetary Policy Report in January, April, July, and October. Specifically, the MPR presents an evaluation of the latest developments in inflation, the exchange rate, and monetary conditions during the reporting month and decisions concerning the monetary policy response adopted by Bank Indonesia.

Board of Governors

Darmin Nasution Deputy Governor Senior

Hartadi A. Sarwono Deputy Governor

Siti Ch. Fadjrijah Deputy Governor

S. Budi Rochadi Deputy Governor

Muliaman D. Hadad Deputy Governor

Ardhayadi Mitroatmodjo Deputy Governor

Table of Contents

I. Monetary Policy Statement ...3

II. The Economy and Monetary Policy ...6

Economy Growth in Indonesia ...8

Inflation ...10

Rupiah Exchange Rate ...11

Monetary Policy ...13

Interest Rates ...13

Deposits, Credits, and Money Supply ...15

The Stock Market ...16

The Government Securities Market ...17

Mutual Funds Market ...18

Banking Conditions ...18

I. MONETARY POLICY STATEMENT

Global indicators point to continued progress in world economic recovery despite heightened risks on global financial markets from the Greek debt crisis. Reflecting this was improvement in advanced economies, led by the US and Japan, alongside the brisk economic growth in emerging market nations. In the US, improving economic conditions are visible in strengthening domestic demand and rising imports. The European economy is also regaining ground, as reflected in slower contraction of retail sales, expansion in industry and rising consumer confidence. In Japan, improvement in the economy is being driven more by exports. China remains the leading growth economy among the emerging markets, despite initial signs of slowing in response to tightened lending. The present recovery in the global economy now faces risks from the debt crisis that has now hit a number of European nations and is ongoing.

The continued strength of global economic recovery has been

matched by steady improvement in the Indonesian economy.

Exports are forging ahead, buoyed by more optimistic developments in manufactured exports in keeping with the more upbeat condition of the global economy. Industries reporting significant growth include textiles, garments, transportation equipment and the chemicals subsector. Production has responded to rising exports with increased utilisation, particularly in export-oriented industries. Investment is also picking up as reflected in the rising imports of raw materials and capital goods as well as rising cement and industrial electricity consumption. In analysis by sector, economic performance was driven mainly by significantly gains in the trade, hotels and restaurants (THR) sector. Performance in THR was also bolstered by activity in other sectors, such as agriculture, manufacturing and imports. Outside the THR sector, another vibrant area of activity was the transport and communications sector. The upbeat pace of economic activity is supported by higher levels of bank financing, mainly in investment credit.

price decisions by the government helped maintain low inflationary pressure in administered prices. Inflation in the consumer price index (CPI) reached 0.29% (mtm) or 4.16% (yoy). These developments brought inflation for the January to May 2010 period to 1.44% (ytd).

Indonesia’s balance of payments showed solid performance in estimated figures despite heightened uncertainties over the Greek debt crisis. The robust condition of Indonesia’s economic fundamentals again contributed to the strong balance of payments. The ongoing improvement in domestic economic performance and outlook has helped attract foreign direct investment (FDI). In the current account, the more vigorous growth in export revenues compared to imports produced a surplus. Export revenues during the first 4 months of 2010 came close to levels preceding the 2008 crisis, despite slowing growth in April 2010. The steepest fall in April 2010 was recorded in exports to Europe, which came down 23%. Among Indonesia’s leading export commodities to Europe, crude palm oil (CPO) plunged significantly as a result of environmental campaigns by NGOs in Europe that have prompted a boycott of CPO products from Indonesia. In the capital and financial account, inflows of portfolio capital were impacted by negative sentiment over the European debt crisis. In response, international reserves at 31 May 2010 stood at 74.6 billion US dollars, equivalent to 5.87 months of imports and servicing of official foreign debt.

Widespread uncertainty on global financial market over the debt crisis in some European economies put added pressure on exchange rates in emerging Asia, including Indonesia. This brought a halt to the appreciating trend in the rupiah under way since early 2010. During May, the average value of the rupiah was down 1.52% at Rp 9,167 to the US dollar compared to Rp 9,028 to the US dollar one month earlier. With financial markets in the region still susceptible to negative sentiment from various quarters, the rupiah closed lower at Rp 9,175 to the US dollar, having sustained 1.77% correction from the previous month’s close. Even so, when compared to the end of 2009, the rupiah still managed 2.53% appreciation in monthly average level or 2.72% gain point to point.

on financial markets. Global liquidity is tightening further with the effects felt most in Europe due to downgrading of some sovereign ratings that has triggered decline in asset values and heightened counterparty risks. Reflecting the crunch on global money markets is the widening spread in the 3-month tenor Overnight Index Swap (OIS) over the 3-month LIBOR. This ultimately triggered flight to quality by foreign investors and sent share prices tumbling in almost all markets in the region. As a result, the JSX Composite Index (JCI) sustained 5.8% correction to close at 2,796.96 at end-May 2010. During May 2010, share volume averaged Rp 5.1 trillion in daily trading, largely unchanged from Rp 5.2 trillion the month before. The financial market turmoil during May 2010 has also begun spreading to the market for Indonesian government securities, as evident in increased yield evenly distributed across all tenors.

From the micro banking perspective, conditions in the banking system are comfortably secure alongside improvement in the bank intermediary function. Banking system stability in Indonesia is now sufficiently robust to anticipate contagion from the debt crisis in Europe. This is borne out in the high capital adequacy ratio (CAR) for the banking system, reported in the most recent data at 19.2%, in addition to the subdued level of non-performing loans (NPLs) gross at below 5%. Improvement in the bank intermediation function is reflected in credit expansion, recorded as of end-May 2010 at 17.6% (yoy). This credit growth remains within the limits of the lending plans described in Bank Business Plans and is consistent with the growing confidence of economic actors in the improving outlook for the Indonesian economy.

II. THE ECONOMY AND MONETARY POLICY

Developments in the world economy again point to buoyant recovery led by the vibrant economies of Asia. The gathering momentum of global economic recovery is manifested in the upward revision of the OECD global economic outlook and the more upbeat Consensus Forecast. The pace of world growth is not only bolstered by performance in developing nations, but also by the increasingly solid improvement in the economies of the US and Japan. So far, no indications suggest that the European debt crisis has dented the still robust outlook for global economic recovery. China’s economy continues to chart high growth despite early sings of slowing activity reflected in the declining pace of bank lending and imports. In Europe, economic fundamentals now show improvement despite the challenges posed by soaring unemployment and the potential for the Greek fiscal crisis to spill over to other European nations.

The US economy is steadily improving on the strength of a solid manufacturing sector. The upbeat recovery in the industry sector is driven by high demand for exports and low inventory levels reflected in higher capacity utilisation and US production indices. Mounting activity in US manufacturing has also resulted in positive figures in US non-farm payrolls for 4 consecutive months (Graph 2.1), a development that in turn reinforces consumer confidence. On the consumption side, the positive trend in retail sales also offers confirmation of consumer optimism.

The Japanese economy is reporting more solid growth in line with more vigorous export performance. Driving the economic growth in Japan is rapid growth in the country’s exports in response to the brisk pace of recovery in Asia and mounting volume of world trade. Stronger exports have provided a boost to Japanese manufacturing activity. In a similar vein, rising household prosperity has encouraged greater household consumption, visible in the strengthening indicators for retail sales and consumer confidence (Graph 2.2). However, the improvement in the Japanese economy has yet to be fully transmitted to the labour market. Unemployment in Japan edged upwards to 5.1% in April 2010.

In Europe, economic conditions continue to improve. Indications point to a turnaround in European household consumption, reflected in the upward trend in the consumer confidence index as retail sales show

Graph 2.1 US Nonfarm Payrolls & Unemployment

���

��������� �

�����������������

��� ��� ��� ��� ��� ��� ���� ����

��� ��� ��� ��� ��� ��� ��� ��� ��� ���� ���� ���� ���� � ��� ��� ��� ���

���� ���� ���� ���� ���� �������������������������������������

less decline. Despite this, improvements in household consumption remain daunted by high unemployment levels in Europe and the shaky condition of Europe’s banking system1. Government expenditure cutbacks under

austerity programmes are likely to fuel labour unrest and weaken the economies of Europe. In manufacturing, the weakening trend in the euro can boost the fortunes of European industry and especially export-oriented manufacturing. The solid condition of European industry is also confirmed by the Purchasing Manager Index (PMI) survey with manufacturing and services in an expansionary phase and industrial production on the rise. Despite this, the fiscal crisis in the PIGS countries (Portugal, Italy, Spain and Greece) has begun taking a significant toll on financial markets in Europe and worldwide. The growing potential for economic decline in Europe has even ignited fears of contagion spreading through the world economy as a whole.

Global inflationary pressures mounted higher, mainly from the contributions of developing economies. The forecast for year 2010 inflation in advanced nations edged up slightly in May to 1.57% (yoy), while inflation in the developing world also mounted to 5.36% (yoy) from 5.30% (yoy) one month earlier. The brisk pace of economic improvement in developing and advanced nations, led by the US and Japan, led to rising inflationary pressure in comparison to preceding months.

Most advanced nations have maintained an accommodative

monetary policy stance with the notable exception of the tight bias in Australia. During May 2010, almost all central banks in the developed world decided to stay the course in monetary policy given subdued levels of inflationary pressure and to bolster economic activity. Some central banks even reinstituted quantitative easing programmes, such as dollar swaps provided by the Fed, purchase of securities (ECB) and liquidity injections by the Bank of Japan (BoJ) aimed at calming liquidity turmoil. In Australia, the overnight cash rate was raised for the third time in 2010 by 25 bps to 4.50% in an effort to curb the asset price bubble in the housing sector and domestic inflationary pressure.

In Asia, some nations have begun normalising their policies in efforts to curb inflationary pressure and asset price bubbles. The Graph 2.2 Japan Retail Sales &

Unemployment

1 The precarious condition of European banks is illustrated by the bankruptcy of Spain’s Bank Cajasur under the weight of burgeoning NPLs. Besides this, the close interconnection among the nations within the European banking system has fuelled concerns over the potential for systemic risk in European banks.1

��� ������������

������������������

�

�� �� �� �� �� �� � � � � �

���

��� ��� ��� ��� ��� ��� ��� ���

���� ���� ����

��� ��� ��� ��� ��� ��� ���

�������������������

������������

������������������

Graph 2.3 Growth of Vehicle Sales

��������

�������

��� ��� ��� �� �� �� �� �� ���

���� ���� ����

central bank of China raised its reserve requirement by a further 50 bps to 17.0% for major banks and 15.0% for minor banks. In a similar move, the Malaysian central bank hiked its reference rate by 25 bps to 2.50%.

Economic Growth in Indonesia

In Q2/2010, the Indonesian economy is expected to maintain growth in line with forecasted levels. The economic crisis in Europe is predicted to have only limited impact on the domestic economy, due to Indonesia’s robust economic fundamentals. On the demand side, growth will remain predominantly demand-driven with a larger than expected contribution from external demand. Household consumption is forecasted to rise in keeping with buoyant public purchasing power and the upbeat trend in consumer confidence. Brisk growth in investment is predicted in response to stronger demand in trading partner nations, a conducive domestic investment climate and the launching of government infrastructure projects. However, this strong boost for investment growth is based primarily on the upbeat growth trend in exports as world economic conditions continue to improve. This will also generate added momentum in import growth. On the supply-side, the stronger sectoral performance in Q1/2010 is predicted to carry forward into Q2/2010, particularly in agriculture, trade and manufacturing. The miscellaneous sector is also forecasted to maintain brisk growth.

Household consumption in Q2/2010 is predicted to remain strong.

The buoyant growth in household consumption is supported by a range of leading consumption indicators. The rise in household consumption is thought to originate from non-food consumption, as indicated by the upward trend in motor vehicle sales (Graph 2.3), electronics sales (Graph 2.4), retail indices for various commodities and imports of non-food consumer items as of April 2010. In regard to financing, potential for increased household consumption is also indicated by high growth in real M1 growth, real consumption credit and debit/credit card transactions (Graph 2.5). The upward trend in household consumption is also supported by the 5% hike in civil servant, military and police salaries and in the regional minimum wage for 2010. Added boost for household consumption is also expected from the election of regional heads of government in 2010. In related developments, consumer confidence improved slightly in keeping with stronger consumer confidence in the

Graph 2.4 Sales of Electronic Products

Graph 2.5 Growth of Transaction Value using Debit and Credit Card �����

condition of the economy and future income expectations. Indications of this are evident in the continued optimism of the May 2010 Consumer Confidence Index (BI Consumer Survey) even though slightly lower at 0.8 points compared to the previous month (Graph 2.6).

Investment is projected to maintain an upward trend in response to buoyant household consumption and a conducive investment climate. Key to investment growth in Q2/2010 is construction investment supported by the increased pace of work in the construction sector and infrastructure projects (Graph 2.7). This is also demonstrated in the high levels of cement consumption during April 2010 (Graph 2.8). Similarly, improvement in non-construction investment is indicated by increases in capital goods imports, raw material imports, commercial vehicle sales and business electricity consumption as of March 2010. Lower interest rates on investment credit during Q1/2010 offer potential for accelerating the pace of investment growth.

In view of the positive business sentiment and global consumer confidence, exports are predicted to stay upbeat during Q2/2010 despite some slowing from the preceding quarter. In Q2/2010, the Baltic Dry Index and export commodity prices climbed by 28.6% (yoy) and 26.6% (yoy), having slowed considerably from the previous quarter’s levels of 94.05% (yoy) and 25.3% (yoy). The more modest increases in export commodity prices are consistent with the slowing trend in international commodity prices during Q2/2010 triggered by the crisis in Europe. Nevertheless, this decline was not as serious as predicted due to the upward trend in the production indices in major destination countries and positive business sentiment in major export destinations. Further improvement in export growth is predicted for Q2/2010, led by mining and manufactured exports to the US, Europe and China.

The Q2/2010 forecast for imports is brisk growth on the strength

of improving domestic demand and keen external demand. This

outlook is supported by movement in leading indicators showing that imports have entered an expansionary phase. Higher imports are also suggested by rising import VAT revenues (Graph 2.10) and demand for imports from major countries of origin. The largest proportion of Indonesia’s imports originate from Japan and China. In disaggregation by merchandise category, the increase is explained primarily by higher imports of consumer goods, followed by raw materials and lastly by increased imports of capital goods.

Graph 2.7 Building and Non-Building Investment Growth

Sectoral performance in Q2/2010 is predicted to chart higher

growth, marked by improvement in both tradable and non-tradable sectors. Manufacturing growth is forecasted to gain momentum driven by the robust growth in the transportation equipment and cement subsectors. Despite this, manufacturing faces pressure from the impact of ACFTA on some subsectors and a planned hike in electricity billing rates. Growth is also expected to taper off in food and beverages in the wake of the surge in this subsector fuelled by the election activities of last year. However, stronger growth is forecasted in the non-tradable sectors. Trade, which represents the most important activity in non-tradable sectors, is set to maintain vigorous growth as indicated by the brisk pace of imports.

Inflation

Inflation remained subdued in May 2010 despite resurgence triggered by non-fundamentals involving mainly volatile foods. Monthly CPI inflation reached 0.29% (yoy) or 4.16% (yoy), up from 0.15% (yoy) and 3.91% (yoy) recorded one month earlier. The unabated price increases in miscellaneous seasonings have boosted inflationary pressure. Supply disruptions triggered by crop failures caused by poor rainfall in some horticultural centres are thought to be one reason for the high rate of inflation in this category. Contrasting this was stable movement in the administered prices category. In analysis of fundamentals, core inflation was curbed slightly by the rise in gold prices in keeping with developments on international commodity markets. Nevertheless, core items still recorded low levels of inflation, also marked by decline. Key to this are secure public expectations of inflation and the modest impact of demand pressure on prices.

Disaggregated by expenditure categories, CPI inflation in May 2010 was fuelled mainly by foodstuffs (Graph 2.12). The surge in the foodstuffs index is explained by high pressure from seasonings. Also generating significant upward pressure in CPI inflation was the clothing category with a contribution of 0.08%.

Administered prices generated minimal inflationary pressure during the month in the absence of decisions to raise prices for strategic administered commodities. Inflationary pressure in this category resulted in part from increases in cigarette prices, including clove filter cigarettes at 0.41% (mtm). So far in 2010, cigarettes have accounted for a 0.13%

Graph 2.10 Import VAT

Graph 2.11 Inflation

������ ������

contribution to inflation. In other areas, the smooth implementation of the household fuels conversion programme has helped curb inflation in administered prices. Taken together, administered prices in May 2010 registered low inflation at 0.15% (qtq) or 2.50% (yoy).

The volatile foods category underwent inflation prompted by disruptions in production and distribution of a number of miscellaneous seasonings. Increases in rice prices, on the other hand, were quite modest. Prices for red chilli peppers, hot chilli peppers and garlic climbed significantly during the month under review (Graph 2.13). Since the end of 2009, red chilli peppers and garlic have generated significant pressure in the volatile foods category. Inflation in garlic prices soared to as much as 233.52% in May 2010. Indonesia is highly dependent on garlic imports from China, which supply for 90% of domestic demand. At this time, China’s production of various foodstuff items, including garlic, is in decline as a result of weather disturbances that have brought on harvest failure. This has prompted the Chinese government to give priority to supplying domestic needs over exports. At the same time, rice prices have mounted due to the delayed harvest in some cultivation centres and hindrances to distribution outside individual local areas. During the month under review, prices for rice edged upwards by 0.12% (Graph 2.14). Prices for rice also climbed in response to reduced stocks of dry unhulled rice at the farmer level and tighter supply of rice drawn from the “rice for the poor” (raskin) programme. Taken together, the volatile foods category recorded inflation at 0.57% (yoy) or 7.29% (yoy), up from 0.34% (yoy) and 6.39% (yoy) in the preceding month.

Core inflationary pressure was low and stable, a result of subdued inflation expectations and modest demand-side pressure. During May 2010, core inflation reached 0.25% (mtm), up from 0.15% (mtm) one month earlier. The resurgent core inflation is explained largely by higher gold prices in keeping with the escalating international market prices for this commodity. Core inflation remains low, having maintained downward trend since the start of the year, and currently stands at 3.81% (yoy).

Rupiah Exchange Rate

The appreciating trend in the rupiah since early 2010 halted due to outflows of foreign portfolio capital. The heavy pressure bearing down on global financial markets from the debt crisis and fiscal crisis in Graph 2.14 Volatile Food Inflation and Rice

Graph 2.13 Herbs and Spices Inflation

some European nations triggered a round of risk aversion towards assets on emerging markets, including Indonesia. Under these conditions, the combination of positive fundamentals in the Indonesian economy and attractive investment returns failed to stem outflows of foreign capital from the domestic financial market. During May 2010 the average rupiah exchange rate weakened 1.52% to Rp 9,167 to the US dollar from Rp 9,028 to the US dollar in the preceding month (Graph 2.17). At month-end, the rupiah shed 1.77% (ptp) of its value from the previous monthly close, reaching Rp 9,175 to the US dollar. In response to these developments, the average value of the rupiah from beginning of year to May 2010 reached Rp 9,192 to the US dollar. The weakening of the rupiah was also accompanied by increased fluctuation at 0.69% (Graph 2.18).

Capital reversal brought on by declining investor risk appetite triggered significant depreciation in the rupiah. Flight to quality, with investors migrating to US dollar-denominated assets, has driven up the value of the US dollar. In contrast, Asian currencies weakened across the board against the US dollar (Graph 2.19). Despite this, the fundamentals of the domestic economy remain solid. Economic growth is forecasted to gain further momentum while the current account will continued to post a surplus. The solid performance in Indonesia’s exports has potential to increase the supply of foreign exchange on the domestic market and thus bolster the resilience of the domestic economy to external shocks.

Fears over contagion from the European crisis triggered a rise in Indonesia’s risk indicators albeit within a limited range. The EMBIG spread was recorded at 324 bps during the month, up from the previous month’s spread of 260 bps (Graph 2.21). The yield spread on Indonesia global bonds over US T-Notes also widened during the month from the previous 170 bps to around the 200 bps mark. The risk indicator for Indonesian bonds (CDS spread) was recorded in the 180 bps range, up from 162 bps one month earlier. However, the swap premium, another of the risk indicators, remained stable. This is indicative of positive global investor expectations for the Indonesian economy (Graph 2.22).

Attractive returns on rupiah investments when compared to other countries in the region again helped attract foreign capital inflows into the domestic economy. The broad interest rate differential has kept foreign funds pouring into Asia, including Indonesia. The subdued level of risk indicators has enabled covered interest rate parity (CIP), which factors in risks, to maintain a rising trend. Indonesia’s CIP in May 2010

Graph 2.16 Domestic and International Gold Prices

Graph 2.17 Average Rupiah Exchange Rate ������

Graph 2.18 Rupiah Exchange Rate Volatility

reached 3.99%, ahead of other countries in the region and particularly the Philippines, Malaysia and Korea (Graph 2.23).

Monetary Policy

Interest Rates

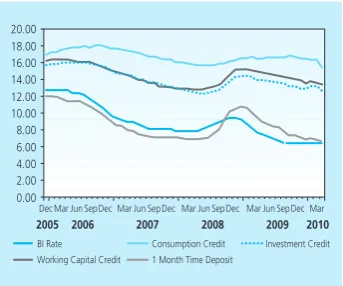

Monetary policy transmission operated by means of conducive overnight interbank rate maintained at around the BI Rate level. During May 2010, the overnight interbank rate mounted slightly over the previous month, moving into closer proximity with the BI Rate. The overnight interbank rate, which had declined in past period to near the lower standing floor (FASBI Rate, 6%), recovered to near the BI Rate level set at 6.5%. The overnight interbank rate averaged 6.15%, up slightly from the previous month’s average of 6.10%. Despite the slight increase in the overnight rate, banking liquidity remained plentiful, also reflecting perceptions of stable risk on the interbank market. At the same time, interbank rates for longer tenors continued to rise. Average interbank rates in longer tenors shifted 1-3 bps, except in the 27-30 day tenor and the over 30 day tenor where rates climbed 5 bps and 13 bps.

Interbank transactions were comparatively stable during May 2010.

Average total daily volume (borrowing and lending) on the overnight market and the interbank market in all tenors reached Rp 15.3 trillion and Rp 21.3 trillion. This reflects an improvement in bank perceptions of counterparty risk.

Concerning bank interest rates, deposit rates recorded steady decline during March 2010. That month, the 1-month deposit rate narrowed by 16 bps from the previous month’s level of 6.77%. Rates in longer tenors (3, 6 and 12 months) similarly eased, while the 24 month tenor was an exception. This resulted in improvement in the deposit rate structure during March 2010 compared to the preceding month. The improved interest rate structure was visible in the rising level of deposit rates in keeping with maturity. However, in analysis by category of bank, private banks provided the momentum for this improvement in the deposit rate structure, while other bank categories and particularly foreign and joint venture banks continued to emphasise provision of greater incentives to customers for 12-month fund placements.

Graph 2.19 Asia’s Exchange Rate Movement

Graph 2.20 Appreciation / Depreciation of Exchange Rate (Average) May 2010 compare to April 2010 ����������������

Transmission of deposit rates to loan interest rates began to operate more effectively during March 2010. Average lending rates (working capital credit, investment credit and consumption credit) fell 52 bps during March 2010 to 13.89%, considerably faster than the 2% drop one month earlier. Consumption Credit provided the most important contribution to decline in lending rates. Consumption credit rates fell 94 bps to 15.42%, while rates for investment credit and working capital credit eased by smaller margins at 49 bps and 14 bps.

In analysis by category of bank, private banks recorded the steepest decline in loan interest rates, with cuts made primarily in consumption credit and working capital credit rates. On average, private banks lowered their lending rates by 124 bps, more than in any other category of banks. Regional development banks and foreign and joint venture bank lowered their loan interest rates by no more than 4 bps and 9 bps, while state-owned banks in fact raised their lending rates by 16 bps.

Graph 2.22 Premi Swap ����������������������������

�

� � �� �� ��

��������� ��������� ��������� ����������

��� ������ ��� ��� ������������ ��������� ��� ��������� ��� ���������

���� ���� ����

Graph 2.23 CIP Indicator in Asia Countries

����

���� ����

����

�

���� ���� ���� ���� ������� ��� ��� ��� ��� ��� ���

���� ���� ���� ����

��� ������ ������������������ ������ ������������������ ���������

�������� ���������

����� �����������

Table 2.1

Development of Various Interest Rates

Interest Rate (%)

BI Rate 8.75 8.25 7.75 7.5 7.25 7.00 6.75 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50 6.50

Deposit Guarentee 9.50 9.00 8.25 7.75 7.75 7.50 7.25 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00 7.00

1-month Deposit (Weighted Average) 10.52 9.88 9.42 9.04 8.77 8.52 8.31 7.94 7.43 7.38 7.16 6.87 7.09 6.93 6.77 na Base Lending Rate 14.18 13.98 13.94 13.78 13.64 13.40 13.20 13.00 12.96 13.01 12.94 12.83 12.65 12.66 12.58 na Working Capital Credit 15.23 15.08 14.99 14.82 14.68 14.52 14.45 14.30 14.17 14.09 13.96 13.69 13.75 13.68 13.54 na Invesment Credit 14.37 14.23 14.05 14.05 13.94 13.78 13.58 13.48 13.20 13.20 13.03 12.96 13.24 13.21 12.72 na Consumption Credit 16.46 16.53 16.46 16.48 16.57 16.63 16.66 16.62 16.67 16.53 16.47 16.42 16.32 16.36 15.42 na

2009 2010

Funds, Credit, and Money Supply

Depositor funds recorded further improvement in annual growth.

From the beginning of the year until April 2010, depositor funds climbed by Rp 7.4 trillion to Rp 1,980.5 trillion, bringing funding growth. In analysis by component, funding growth again received a boost from growth in time deposits, despite reductions in time deposit rates. This is consistent with the larger share of depositor funds held by individuals, most of whom place their funds in rupiah-denominated time deposits. During April 2010, growth in foreign currency deposits mounted from 4.6% (yoy) to 7.8% (yoy), mainly involving non-financial corporate demand deposits. The invigorated growth in foreign currency deposits and particularly demand deposits came not only from export revenues, but also in response to the appreciating trend in the rupiah.

Policy transmission through the credit channel is steadily improving in response to rising domestic demand and progressive decline in loan interest rates. In April 2010, credit expansion (including channelling) reached 13.8% (yoy), ahead of the previous month’s expansion of 10.7% (yoy). Additional lending volume in April 2010 came to Rp 45.2 trillion (3.1%, ytd). Lending is expected to mount higher from demand side and supply side growth. On the demand side, the improvement in domestic economic conditions has fuelled demand for credit. In regard to credit supply, one factor contributing to increased lending is the downward movement in loan interest rates. Indications point to credit growth as high as 17.6% (yoy) in May 2010.

In analysis by use of credit, credit expansion is explained primarily by the contribution of consumption credit. In April 2010, growth in consumption credit reached 28.2% (yoy). Investment credit and working capital credit also recorded expansion at 17.9% (yoy) and 5.4% (yoy) (Graph 2.26). In disaggregation by currency, foreign currency credit expansion was up in keeping with the rise in foreign currency deposits and renewed activity in export and imports. In analysis by sector, the increased rate of credit expansion is explained by growth in the miscellaneous items sector consistent with the rise in consumption credit. The trade sector also improved during April 2010 with growth at 0.75% (yoy) compared to the preceding month’s expansion at 0.5% (yoy), while manufacturing growth remained negative. On the other hand, the mining, social services and transportation sectors and the electricity, gas and water utilities sector reported brisk growth in the range of 24%-82% (yoy).

Graph 2.24 Development of Various Interest Rates

Graph 2.25 Development of Funds, Credits, and BI Rate

Economic liquidity reflected in the base money indicator is steadily improving. During May 2010, base money growth steadily mounted in keeping with upbeat economic activity. Base money growth strengthened to 14.4% (yoy), compared to 13.9% (yoy) one month earlier. In analysis by component, the base money acceleration was driven more by heavy demand for cash outside banks. During May 2010, the added public demand for cash outside banks reached Rp 8.2 trillion. Accordingly, the May 2010 expansion in cash outside banks reached 13.3% (yoy), ahead of the previous month’s level of 11.3% (y-o-y). These developments reflect an improvement in economic conditions for the general public, although still short of full recovery.

On the other hand, M1 growth in April 2010 was down slightly at 8.3% (yoy) from 9.7% (yoy) one month earlier (Graph 2.27). This is explained largely by a reduced position in demand deposits held by private non-financial business following the payment of corporate taxes in April 2010, as well as indications of migration of funds from demand deposits to time deposits and foreign currency deposits alongside the upward exchange rate trend. This development in M1 led to a rise in M2 growth from 11.4% (yoy) in the preceding month to 11.8% (yoy) in April 2010 (Graph 2.28). The improvement in M2 came in response to the upward trend in credit expansion.

The Stock Market

Stock market performance was impacted by external turmoil. The

debt crisis in the PIIGS countries (Portugal, Ireland, Italy, Greece and Spain) sparked negative sentiment on stock markets around the globe, including Indonesia. As a result, the JSX Composite Index (JCI) sustained 5.8% correction to close at 2,796.96.

The weakening of the JCI was consistent with the correction on global exchanges and offloading by foreign investors (Graph 2.29) related to market pessimism over debt resolution for the PIIGS nations. Furthermore, global financial market actors have begun to question the global monetary policy exit strategy and the pace of recovery in world growth. This

ultimately triggered a sell-off by foreign investors and a round of share price correction on almost all markets in the region.

The wave of foreigner selling was followed by plunging market confidence, reflected among others in falling volume of share trading. During May

Graph 2.27 Growth of Currency in Circulation (Nominal)

2010, foreign investors booked an accumulated net sale of Rp 1.7 trillion, in contrast to behaviour during preceding months (March and April 2010) with net purchase recorded at Rp 4.9 trillion and Rp 1.5 trillion. Foreign investors embarked on flight to quality by offloading assets in emerging market countries and migrating to more secure instruments such as US government securities. Accompanying this was a drop in trading volume, albeit on a limited scale. During May 2010, daily turnover in share trading reached Rp 5.2 trillion, down slightly from the previous month’s average of Rp 5.2 trillion (Graph 2.30).

Stock performance underwent correction across almost all sectors. The market correction in mining and agribusiness stocks, both heavily capitalised and activity traded on the exchange, resulted in a significant contribution to the weakened performance of the JCI. The correction sustained by the two sectors was closely linked to the drop world oil prices brought on by escalating fears of a derailing of the world economic recovery. Despite this, the consumer goods sector has taken a positive turn. However, modest levels of capitalisation meant that the consumer goods sector was unable to withstand the market correction on the stock exchange.

Government Securities Market

The financial market turmoil during May 2010 also spread to the market for Indonesian government securities, driving up yield evenly across all tenors. Average yield on government securities widened by 35 bps over the preceding month to close at 8.9% (Graph 2.31). The steepest rise in yield took place in medium-term government securities. Accordingly, short, medium and long-term yield mounted by 35 bps, 38 bps and 29 bps. Nevertheless, this represented a relatively modest increase in yield when compared to yields during the 2008 crisis.

Like with the stock market, external risk indicators appear to have influenced yield on government securities. Domestic market fears reached a peak in May 2010 and ultimately drove up external risk indicators such as the EMBIG spread and Indonesian CDS. In May 2010, the EMBIG spread and Indonesia CDS mounted by 68.1 bps and 16.3 bps.

This eventually prompted foreign investors to offload their holdings on the government securities market. During May 2010, foreign investors booked a net sale of Rp 3.9 trillion in contrast to the previous months’ net Graph 2.30 JCI and Average Daily Trading

Volume

Graph 2.31 Yield SBN, BI Rate and 1-Month SBI ������������

� � � � � ��

���� ���� ���� ���� � � � � �� �� � � � � �� �� � � � � �� �� � � ���

����� ����� ����� ����� ����� �����

�������������������������������������� ���������

��� ��� ��� ��� ��� ��� ��� ��� ������ ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� �

� � �� �� �� �� �� �� ��

���� ���� ���� ���� ���� ����

�������

purchase at Rp 15.6 trillion. Foreigner selling behaviour on the government securities market was similar to that on the stock market, with foreign investors beginning to pull out of emerging markets in favour of safe havens. This prompted a drop in market confidence that in turn bore down on trading volume on the government securities market. During May 2010, daily average turnover reached Rp 4.4 trillion, down from the April 2010 average of Rp 6 trillion per day (Graph 2.32).

Mutual Funds Market

The slide in stock market and government securities market during May 2010 had spillover effects on the mutual funds market. Reflecting this was index decline across almost all mutual fund products. Equity funds recorded the steepest correction, followed by mixed funds. Equity funds, fixed income funds and mixed funds sustained 11.3%, 0.6% and 8.1% correction (Graph 2.33). NAV (net asset value) is also estimated on a downward track in line with the performance of underlying assets.

Condition of the Banking System

Key factors in the financial sector are the continued stability in the banking system and improvement in the bank intermediation function. Banking system stability in Indonesia is sufficiently robust to anticipate contagion from the debt crisis in Europe. This is borne out in the high capital adequacy ratio (CAR) for the banking system, reported in the most recent data at 19.2%, in addition to the comfortably safe level of non-performing loans (NPLs) gross at below 5% (Table 2.2). Improvement in the bank intermediation function is reflected the upward trend in credit expansion. Alongside this, Return on Assets (ROA) was stable at 2.9%, as was the level of Net Interest Margin (NIM) at 0.5% (Table 2.2).

Graph 2.32 Yield SBN and Daily Trading Volume

Graph 2.33 Mixed Mutual Fund Index, Permanent Income, and Stocks

������������ �

� � � � � ��

���� ���� ���� ���� ���� ���� � � � � � �� � � � � � �� � � � � � �� � � � � � �� � � � � � �� � � ��

�� �� ��

�������������������������������������� �������������������

� �� ��� ��� ��� ��� ���

����

��������������� ��� ��� ������������ ������������������ ��� ������ ��������� ��������������� ���� ���� ���� ���� ����

������������������� ������������ ����

III. MONETARY POLICY RESPONSE

In the Board of Governors’ Meeting on 3 June 2010, Bank Indonesia decided to keep the BI Rate at 6.50%. This decision was taken after a comprehensive evaluation of the latest developments and outlook for the economy, which is now showing steady improvement. In the opinion of the Board of Governors, the BI Rate at this level is consistent with achievement of the 5%±1% inflation target in 2010 and 2011 and remains conducive to the strengthening the process of economic recovery. This decision is also consistent with measures to safeguard domestic financial stability amid the rising risks and uncertainties brought on by the debt crisis in Greece and a number of other European nations.

Table 2.2

Main Indicators of Banking System

Main Indicators

Total Asset (T Rp) 2,307.1 2,344.9 2,352.1 2,327.4 2,309.8 2,354.3 2,331.4 2,384.6 2,388.6 2,392.7 2,439.7 2,534.1 2,501.8 2,517.0 2,563.7 2,576.3

DPK (T Rp) 1,745.6 1,767.1 1,786.2 1,780.9 1,783.6 1,824.3 1,806.6 1,847.0 1,857.3 1,863.5 1,897.0 1,973.0 1,948.6 1,931.6 1,982.2 1,980.5

Credit (T Rp) 1,325.3 1,334.2 1,342.1 1,332.1 1,339.2 1,368.9 1,370.2 1,400.4 1,399.9 1,410.4 1,430.9 1,470.8 1,435.7 1,459.7 1,485.9 1,516.0

LDR (%) 75.9 75.5 75.1 74.8 75.1 75.0 75.8 75.8 75.4 75.7 75.4 74.5 73.7 75.6 75.0 76.5

NPLs Gross* (%) 4.2 4.3 4.5 4.6 4.7 4.5 4.6 4.5 4.3 4.3 4.4 3.8 3.9 4.0 3.8 3.5

NPLs Net * (%) 1.6 1.6 1.9 2.0 1.9 1.7 1.7 1.5 1.3 1.2 1.4 0.9 1.1 1.0 1.0 0.9

CAR (%) 17.6 17.7 17.4 17.6 17.3 17.0 17.0 17.0 17.7 17.6 17.0 17.4 19.2 19.3 19.1 19.2

NIM (%) 0.5 0.3 0.6 0.5 0.5 0.5 0.5 0.5 0.4 0.5 0.5 0.5 0.5 0.5 0.5 0.5

ROA (%) 2.7 2.6 2.8 2.7 2.7 2.7 2.7 2.7 2.6 2.7 2.6 2.6 3.1 2.9 3.0 2.9

2010 2009

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr

* Provisional Figures

* Using 2000 base year (BPS-Statistic Indonesia) 1) end of week

2) weighted average 3) end period closing 4) closed file

Sources : Bank Indonesia, except stock market data (BAPEPAM), CPI, export/import and GDP (BPS)

Latest Indicators

FINANCIAL SECTOR

P R I C E S

EXTERNAL SECTOR

QUARTERLY INDICATOR INTEREST RATE & STOCK

One month SBI 1) Three month SBI 1) One month Deposit 2) Three month Deposit 2) One week JIBOR 2) JSX Indices 3)

MONETARY AGGREGATES (billions Rp) Base Money

M1(C+D) Currency (C) Demand Deposit (D) Broad Money (M2 = C+D+T)

Quasi Money (T) Quasi Money (Rupiah) Time Deposit Saving Deposit Foreign Currency Deposit Broad Money Rupiah Claim on Business Sector Credit by DMBs

CPI - monthly (%, mtm) CPI - 1 year (%, yoy)

Rp/USD (endperiod,midrate) Non oil/gas Export (f.o.b, million USD) 4) Non oil/gas Import (c$f, million USD) 4) Net International Reserve (million USD)

Real GDP Growth (% y-o-y) Consumption Investment Changes in Stocks Export Import

7.25 6.95 6.71 6.58 6.48 6.49 6.47 6.46 6.45 6.41 6.27 6.20

-7.39 7.05 6.79 6.63 6.55 6.60 6.59 6.59 6.60 6.59 6.56 6.50

-8.77 8.52 8.31 7.94 7.43 7.38 7.16 6.87 7.09 6.93 6.77 - -

9.68 9.25 8.99 8.73 8.35 7.97 7.68 7.48 7.31 7.08 6.99 -

-7.69 7.09 6.96 6.56 6.46 6.46 6.47 6.46 6.45 6.40 6.38 6.30

-1,917 2,027 2,323 2,342 2,468 2,368 2,416 2,534 2,611 2,549 2,777 2,971 2,797

309,232 322,994 322,850 324,663 354,297 364,869 376,938 402,118 384,176 380,145 374,406 388,752

-456,955 482,621 468,949 490,128 490,502 485,538 495,061 515,824 496,527 490,084 494,461 - -

193,733 203,406 200,774 200,424 210,822 205,864 212,054 226,006 211,811 211,708 205,083 208,358

-263,221 279,215 268,174 289,704 279,679 279,674 283,007 289,818 284,716 278,376 289,378 - -

1,808,979 1,859,258 1,840,715 1,871,508 1,889,158 1,900,466 1,928,347 2,013,425 1,942,999 1,936,273 1,972,683 -

1,352,024 1,376,637 1,371,766 1,381,381 1,398,656 1,414,928 1,433,286 1,497,601 1,446,473 1,446,189 1,478,222 -

1,217,906 1,245,822 1,245,247 1,251,225 1,272,217 1,285,497 1,297,781 1,359,667 1,317,461 1,317,102 1,347,094 -

-715,139 726,088 724,888 727,889 731,202 741,072 738,118 756,347 736,999 744,823 772,718 -

-502,767 519,733 520,359 523,336 541,015 544,425 559,663 603,320 580,462 572,280 574,376 -

-134,118 130,815 126,519 130,156 126,439 129,431 135,505 137,934 129,011 129,086 131,128 -

1,674,861 1,728,443 1,714,196 1,741,352 1,762,719 1,771,035 1,792,842 1,875,491 1,813,988 1,807,186 1,841,555 -

1,392,747 1,419,799 1,435,290 1,465,870 1,463,662 1,478,447 1,503,304 1,543,901 1,530,338 1,557,520 1,592,410 -

1,297,211 1,319,240 1,359,101 1,351,565 1,347,876 1,360,639 1,379,527 1,403,686 1,350,803 1,378,227 1,370,033 -

-0.04 0.11 0.45 0.56 1.05 0.19 -0.03 0.33 0.84 0.30 -0.14 0.15 0.29

6.04 3.65 2.71 2.75 2.83 2.57 2.41 2.78 3.72 3.81 3.43 3.91 4.16

10,340 10,225 9,920 10,060 9,681 9,545 9,480 9,400 9,365 9,335 9,115 9,012 9,180

8,229 8,470 8,437 8,966 8,200 9,760 8,449 10,936 8,399 8,712 10,701 -

-6,366 6,987 7,720 7,313 5,589 7,883 6,759 7,936 7,523 7,534 9,054 -

-51.65 50.99 50.72 50.84 53.81 55.68 56.15 57.69 61.59 62.14 63.60 70.75 68.54

5.7 4.4 6.9

19.0 21.1

May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May

2009 2010