The ASEAN

1. Introduction 5

2. Context: a growing region 8

Gross domestic products in ASEAN 6 Foreign investment 12

3. The AEC vision 14

The road to 2015 14

The AEC blueprint 16 An ambitious blueprint 18

4. The AEC reality 21

Progress to date 21

The challenges ahead 22

What will the new AEC look like? 29

5. Is Indonesia ready for the AEC? 33

Strengths 33

Weaknesses 36

Opportunities 38

Threats 40

6. What will the AEC mean for foreign investors? 42

1

Introduction

Welcome to The ASEAN Economic Community: can the reality match the vision?

In this publication, which builds on our earlier report

ASEAN 2015 and beyond: Are German investors missing out?, we outline the growth story in the ASEAN region

and set out the ASEAN’s ambitious plans for the ASEAN Economic Community (AEC) as it prepares to launch

later this year.1

All 10 ASEAN member states have signed up to the blueprint for the AEC, which aims to create a tariff-free zone while setting a timetable for the removal of non-tariff barriers (NTBs) across the region.

Chart 1: The member states of the ASEAN Economic Community

Myanmar

51 million inhabitants 63e billion US$ GDP 1.222 US$ GDP per capita

Thailand

68 million inhabitants 374 billion US$ GDP 5.518 US$ GDP per capita

Cambodia

15 million inhabitants 17e billion US$ GDP 1.071 US$ GDP per capita

Singapore

6 million inhabitants 308e billion US$ GDP 55.307 US$ GDP per capita

Indonesia

Philippines

108 million inhabitants 285 billion US$ GDP 2.646 US$ GDP per capita

Laos

7 million inhabitants 11e billion US$ GDP 1.716 US$ GDP

per capita

Vietnam

93 million inhabitants 186e billion US$ GDP 1.991 US$ GDP

per capita

Brunei Darussalam

0.4 million inhabitants 15e billion US$ GDP 35.730 US$ GDP per capita

Malaysia

2

Context: a growing region

Gross Domestic Product (GDP) in ASEAN

After the recent boom in eficiency-driven markets, particularly Brazil, Russia, India, China and South Africa (BRICS), attention is now shifting to the ASEAN region.

In the past ive years, the GDP of ASEAN has grown by 5.6% on average. The International Monetary Fund (IMF) predicts GDP growth will remain above 5% during 2015– 2020 for the ASEAN region.

Already, ASEAN accounts for more than 5% of the world’s GDP. This proportion is rising: ASEAN created US$2.4 trillion of nominal GDP in 2014, about two-thirds the GDP of Germany and just under half that of Japan (Chart 2).

2

Japan

US$4.9t

Germany

US$3.9t

China

(mainland)

US$10.4t

India US$2.0t Taiwan US$0.5t ASEAN US$2.4t South Korea US$1.4t Vietnam 8% Philippines 11% Brunei 1% Laos 0% Indonesia 36% Cambodia 1% Myanmar 3%GDP of ASEAN countries, 2014

Chart 2: ASEAN GDP compared to major

As a result, industrial nations such as Germany, the US and Japan face slightly decreasing shares of global GDP based on purchasing-power-parity (Chart 3). Such changes will eventually have a greater effect on the world economy.

Chart 3: GDP based on purchasing-power-parity (PPP) share of world total

GDP b

as

ed on PPP in %

25

20

15

10

5

0

Source: IMF World Economic Outlook Database, April 2015

Foreign investment

Foreign direct investment (FDI) into ASEAN continues to grow, and now rivals FDI into China (Chart 4).

Japanese investors, for example, have already shifted FDI from China to ASEAN. According to the Japan External Trade Organization (JETRO)2, FDI by Japanese investors into China in 2013 totalled US$9.1 billion, a dip of 32.5% from 2012; compared to US$23.6 billion invested in ASEAN in the same year, marking an increase of 120%.2

German companies are increasingly interested in the ASEAN market: In our recent report, ASEAN 2015 and beyond: Are German investors missing out?, 75% of the

135 German companies we interviewed plan either to increase their FDI or to make their irst investment in ASEAN in the coming years.3

Some 65% see the implementation of the AEC as a factor

that will increase their willingness to invest in the region

in future.

2 2014 JETRO Global Trade and Investment Report – On making Japan a base for international business circulation (JETRO, August 2014).

3 ASEAN 2015 and beyond: Are German investors missing out?

Chart 4: Value of annual foreign direct investment

inflows (US$ million)

140,000

120,000

100,000

80,000

60,000

0

Source: UNCTAD World Investment Report 2015 40,000

20,000

South

Africa

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

ASEAN China

Brazil

India Russia

3

The AEC vision

The road to 2015

The proposed launch of the AEC at the end of 2015 is a culmination of more than two decades of economic

integration.

1992

ASEAN Free Trade Area (AFTA) agreement signed

• This establishes the Common Effective Preferential

Tariff scheme (CEPT): customs tariffs to be reduced to 0–5% within 15 years

1998

ASEAN Investment Area (AIA) framework signed

• Foreign investors to receive “national treatment”

2003

“Bali Concord II” signed, agreeing to establish

the AEC on three pillars:

3

2007

AEC blueprint adopted

• Creates roadmap for setting up the AEC in 2015

2009

ATIGA (ASEAN Trade in Goods Agreement) signed

• Enhances CEPT scheme

2015

The AEC blueprint

The ASEAN Community comprises three pillars:

• Economic Community (AEC) • Political-security Community • Social-cultural Community

Characteristics and elements of the Economic Community (AEC) involve:

1. Establishing a single market and production base. The aim is to break down barriers to trade and investment, and to free up the movement of skilled workers.

2. Developing a competitive economic region. This will include:

• Breaking down non-tariff barriers (NTBs) • Reducing transport costs by developing

infrastructure

• Encouraging innovation by enforcing intellectual

The AEC will in theory

be the “strongest”

Asia-Paciic FTA

3. Building a region characterized by equitable economic development. There will be support for small businesses, as well as technical assistance and capacity-building programs to help the region’s less developed economies.

An ambitious blueprint

There are currently 119 free trade agreements (FTAs) in the Asia-Paciic region. Most of them – including AFTA – are considered “weak” agreements, with regard to customs, controlling mechanisms and their many

exceptions.4

The AEC will be much more ambitious:

• Customs: The blueprint envisages a general tariff-free

zone without exceptions. The common objective for ASEAN member states is “0% tariffs on 100% of traded goods and services”.

• Non-tariff barriers: The ATIGA, signed in 2009,

envisages that countries remove NTBs according to the following schedule:

• ASEAN-6 countries (Brunei Darussalam, Indonesia,

Malaysia, the Philippines, Singapore and Thailand):

2015

• CLMV countries (Cambodia, Laos, Myanmar,

Vietnam): 2015, with lexibility until 2018

4 The ASEAN Economic Community – A Work in Progress, p. 25 (Asian

“ASEAN recognizes that the

group is far more inluential

collectively than individually.

The launch of the AEC at

the end of 2015 will forge

closer ties between

other-wise highly diverse nations.”

Dr. Georg Witschel, Ambassador of the Federal

4

The AEC reality

Progress to date

In some ways, ASEAN is already well down the road to economic integration.

Tariff rates are almost zero on 99% of goods traded among ASEAN-6 countries (Brunei Darussalam, Indonesia, Malaysia, Philippines, Singapore and Thailand), although much work remains to be done on non-tariff barriers.

CMLV countries (Cambodia, Myanmar, Laos and Vietnam) are set to abolish all import tariffs by the end of 2015, with a three-year grace period on up to 7% of items.5

The challenges ahead

Challenge 1: Slow reduction of NTBs

Many important trade barriers – such as import limitations, mandatory registration or licensing of products, standardized speciications, admissions processes and customs handling – are “non-tariff” barriers; that is, they do not involve a customs tariff. Countries use them to protect their local markets by complicating market access for foreign providers. This means that, with regard to regional integration, their impact is as important as customs tariffs.

Reducing NTBs in ASEAN is a gradual process. This is often a result of poor past experience; e.g., after the ASEAN-China FTA, some local companies in Indonesia were put out of business by cheaper producers from China. It can also take a long time to make changes, even when the intention and willingness are there, because of the lack of irm and consistent controlling mechanisms in many ASEAN countries.

Indeed, some countries, such as Indonesia, have not reduced their NTBs but have actually set up more regulations to protect their domestic economies.6

“The issue right now is not

so much about wider trade

liberalization, but rather

about non-tariff measures

and technical barriers to

trade, which are much more

challenging to address than

tariffs alone.”

Challenge 2: Public perception of the AEC

Another major challenge for the AEC is public awareness – or rather, the lack of it. Well over half (about 55%) of ASEAN SMEs do not know what the AEC is, according to a survey by the Institute of South-East Asian Studies (ISEAS) in 2013.7

In Indonesia, these numbers are even higher: more than three quarters (77%) of Indonesian SMEs do not know

what the AEC is.

Challenge 3: Power and resources of ASEAN

Although the plans for the AEC are promising,

implementing them will be more dificult. ASEAN has no power or mechanism to ensure individual countries keep to their side of the bargain. The likelihood is that there will be plenty of sticking points, especially on politically sensitive issues, even if governments do recognize the economic beneits of the AEC.

Related to this are the ASEAN Secretariat’s limited

resources. An article in The Diplomat recently noted that

Further hurdles

Further challenges to the future of the AEC may be summarized as follows:

• Language barriers and cultural differences could

inluence future agreements and implementations, which might result in internal competitions.

• The increased movement of skilled workers across

borders is likely to meet resistance.

• Infrastructure deiciencies, which raise the transport

costs of doing business, will take years to address.

• Political instability and regulatory overkill, combined

“It’s dificult. There are

different languages,

different systems and

different ethnicities and

very little homogeneity.”

Seng-Leong Teh, Partner,

What will the new AEC look like?

The act of launching the AEC on 31 December 2015 will not transform the ASEAN region overnight. As long as the tariff-free trade plays a minor role compared to the individual diverse NTBs in ASEAN member states, the AEC will not become a true “single market”. If realized, the AEC could make ASEAN a common market, with free low of goods, services, investment and labor – and freer, but not free, low of capital.

“Free trade area

with beneits”

Indeed, ASEAN countries will still have issues creating a “common market”. Failure to meet the initial requirements within individual countries will prevent the AEC becoming what it is intended to be. The free low of labor, for example, is today only accessible in eight occupational

areas.

Initially the AEC will therefore be an economic alliance with a highly diverse group of member states that strengthens ASEAN’s competitiveness on a global scale, creating incentives for investors. There is already evidence of increased investment: FDI into Indonesia grew by 22.8% in

Q1 2015.9

This increased competitiveness should lead to better global integration for the ASEAN region, which is likely to continue to improve and prosper.

“With ASEAN we have

embarked on a longer

journey. Even the new date

of 31 December [2015]

should be seen more as

an aspirational milestone

rather than a inal deadline.

Will everyone be 100%

ready by then? No. But we

deinitely are on the move.”

5

Is Indonesia ready

for the AEC?

Indonesia has the largest population in ASEAN, with 254 million inhabitants. As a “test case” of how the wider ASEAN might fare in the AEC, here we outline the strengths, weaknesses, opportunities and threats facing Indonesia, as the 2015 launch gets closer.

Strengths

• Indonesia’s vast population is an indisputable strength

(Chart 5), as are its favorable demographics, with the average age being 29.2 years.

• Highly competitive wages.

• The possibility of tariff-free trade with other ASEAN

member states, due to the launch of the AEC.

• The 2014 Indonesian Government’s gross debt, as a

• Resistant and strong domestic market

• Robust domestic demand makes up about two thirds

of GDP

• Exports represent around 30% of GDP

• Natural resources (oil, natural gas, coal) • Strategic location

• Indonesia’s current economic growth is forecast to be

above ive percent per year until 2020 (Chart 6)11 300 250 200 150 100 0 Brun ei

Chart 5: Population of ASEAN member states in 2014

50 Sing apor e Laos Cam bodi a Mal aysi a Mya nm ar Thai land Viet nam Phili ppin es Indo nesi a

Source: The World Factbook

15 10 5 0 −5 −15

Chart 6: Indonesia’s economic growth

−10

Sources: GDP annual growth data from World Bank (1980–2013) and estimates from IMF World Economic Outlook Database, April 2015 (2014–2020)

GDP gr

o

wth (in %)

1980 1985 1990 1995 2000 2005 2010

2015e 2020e

Average over 14 years: 7.27% (1983–1996)

Average over past 10 years: 5.79% (2005–2014)

Forecast growth based on IMF estimate

Rarely influenced during financial crisis

Oil crisis

Weaknesses

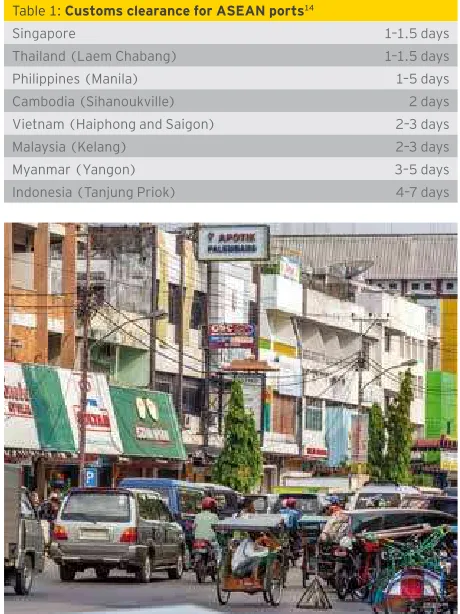

Among ASEAN member states, Indonesia has the most restrictive NTBs; these add 30% on costs on more than half of imported goods.12 In addition to such cost drivers,

Jakarta’s Tanjung Priok has the longest customs clearance time of any of the ASEAN ports (Table 1).

Other weaknesses include:

• Infrastructure deiciencies • Instable politics

• Corruption

• Risk of natural disaster

• Severe environmental pollution • Language barriers

• Diverse population with more than 15 ethnic groups

• Governance and bureaucracy

• Poor education levels/educational system • Rising wages

• High inlation

• Stagnating productivity13

12 ERIA – AEC Blueprint Implementation Performance and Challenges: Non-Tariff Measures and Non-Tariff Barriers. 13 ILO Global Wage Database, ILO Trends Economic Models,

January 2014.

Table 1: Customs clearance for ASEAN ports14

Singapore 1–1.5 days

Thailand (Laem Chabang) 1–1.5 days

Philippines (Manila) 1–5 days

Cambodia (Sihanoukville) 2 days

Vietnam (Haiphong and Saigon) 2–3 days

Malaysia (Kelang) 2–3 days

Myanmar (Yangon) 3–5 days

Opportunities

• The ASEAN region’s middle-class population is

predicted to double to 400 million by 2020.15

This is likely to herald a signiicant rise in demand for consumer goods.

• Primarily beneiting investors in industries such

as e-commerce, health care, tourism and inancial

services.

• Companies are planning to operate more production

hubs in Indonesia, especially in manufacturing and production industries (Chart 7).

• Tariff-free trade with other ASEAN member states as

well as reduction of NTBs

• ASEANs numerous free-trade agreements with other

partners (e.g., China, India, South Korea, Japan, Australia, New Zealand).

Brun ei Laos Cam bodi a Mya nmar Viet nam Sing apor e Thai land Phili ppin es Mal aysi a Indo nesi a

Chart 7: How many factories do you operate in ASEAN

today? How many will you operate in five years?

Source: Economist Corporate Network

Response from 75 companies with manufacturing operations in ASEAN Increased number of

factories over the next five years

Number of factories today

54 79 11 90 74 81 70 51 24 17 8 24 27 6 3 0 1

Threats

• Empirical studies show that trade liberalization is highly

beneicial to market actors. However, there are two important exceptions to this:

• Local companies operating just above break-even

might be pushed out of the market;

• State-owned enterprises, usually unaccustomed to

open markets, may be left behind (there are 139 state-owned companies in Indonesia – within ASEAN, only Vietnam has more).

• Investment conditions/prohibitions in certain business

ields (Negative Investment List)16

• Ineficient implementation of investment plans for

infrastructure development

• Indonesian economy depends heavily on commodity

exports and lately faces changes:

• Commodity cycle has passed its peak

• Weaker demand especially of China and Japan • Current account deicit due to imports outstripping

exports (Chart 8) which puts high pressure on the currency with a trend of a weaker Rupiah

• Dependence on monetary policy of the US Federal

Reserve

• If economic conditions tighten, consumers may be

less likely to spend

Chart 8: Indonesian current account

Numbers in billion US$ Sources: World Bank

2009 2010 2011

2012 2013

10.6 5.1

1.7

−24.4

6

What will the AEC mean

for foreign investors?

From foreign investors’ point of view, the main

opportunity from the launch of the AEC is that tariffs on goods and services will, in theory, be limited to those imported from outside the ASEAN region. Tariffs within the ASEAN countries will no longer apply.

By 2016, foreign investors with a production hub within the ASEAN region will largely beneit from the AEC arrangements. Investors may, for instance

• Concentrate production lines in a chosen ASEAN

country, thus creating economies of scale, and then export the inished product tariff-free to other ASEAN countries as well as to ASEAN’s free-trade partners in the region (China, India, South Korea, Japan, Australia, New Zealand);

• Identify comparative advantages of individual ASEAN

In our recent report, ASEAN 2015 and beyond: are German investors missing out?, 91% of the German

investors we surveyed cited ASEAN’s internal market as a key factor driving them to invest.17 Most expected

the implementation of the AEC to make ASEAN more attractive as a production hub and to simplify

international trade.

Closer ties with Europe

Further in the future, there is also the possibility of an FTA between the EU and ASEAN.

According to research company Ecorys, for example, an ambitious “FTA Plus” agreement between the EU and ASEAN would lead to GDP growth of 0.23% inside the EU, and growth in ASEAN ranging from 3.66% in Indonesia to 15.27% in Vietnam. For the EU, missing out on what could be the fastest growing market in the next 5–10 years

“Within ASEAN, different

countries are beginning

to establish their own

competitive advantages.

For example, Thailand is

one of the automobile

centers of Southeast Asia.

The Japanese have brought

their entire auto supply

7

A continuing journey

The launch of the AEC in late 2015, as discussed above, will not be the end of the journey to ASEAN economic integration. It will be just the latest step along that road. Many hurdles both intra-regional and national will continue to challenge on true economic union.

“10 states with 600 million

potential consumers and

workers bring an ininite

amount of business

opportunities, especially

in automotive, logistics and

infrastructure.”

8

Find out more

For more information, read ASEAN 2015 and beyond: are German investors missing out?.18This March 2015 report

is the result of cooperation between AHK-ASEAN, EY and the German Embassies in ASEAN.

The following online sources may also be useful:

The Association of Southeast Asian Nations

www.asean.org

ASEAN competition policy and law www.aseancompetition.org

Asia-Studies.com www.asia-studies.com

Germany Trade & Invest

www.gtai.de

Indonesia Investments

www.indonesia-investments.com

Institute of Southeast Asian Studies

www.iseas.edu.sg

18 ASEAN 2015 and beyond: Are German investors missing out?

The Organisation for Economic Co-operation and Development

www.oecd.org

United Nations Conference on Trade and Development

www.unctad.org

ASEAN 2015 and beyond: Are German investors missing out?

In our report we comprise opportunities offered by the AEC; things you need to consider before entering the ASEAN market; cultural, iscal and legal obstacles you need to be aware of and

other interesting questions. We present

Contacts

Contacts

Holger SeubertHead of Economic Department

Embassy of the Federal Republic of Germany Jl. M. H. Thamrin No. 1

Menteng Jakarta Pusat DKI Jakarta 10310, Indonesia Tel: +62 21 3985 5141 [email protected]

Thomas Wirtz

Partner, Transaction Advisory Services,

EY

| Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust

and conidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member irms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2015 EYGM Limited.

All Rights Reserved.

APAC no. 00000313

SKN 1506-087 ED None