www.elsevier.com/locate/utilpol

The electricity supply industry in Germany: market power or

power of the market?

Gert Brunekreeft

*, Katja Keller

Institut fu¨r Verkehrswissenschaft, University of Freiburg, D-79085 Freiburg i.Br. Germany

Received 29 February 2000; received in revised form 8 September 2000; accepted 28 November 2000

Abstract

This paper analyses the electricity supply industry in Germany, which was liberalized in April 1998. Noticeable aspects are the eligibility ofallend-users, the lack of constraints on the vertical industry structure and the option fornegotiatedthird party access. There is no sector-specific regulation. This paper argues that the vertically integrated firms concentrate on excessive network access charges, whereas the stages generation and retail appear to be relatively competitive. Empirical evidence suggests that in Germany network access charges make up a significantly higher share of end-user prices than in the UK, which is used as regulation-benchmark.2001 Elsevier Science Ltd. All rights reserved.

JEL classification:L1; L43; L94

Keywords:Electricity; Competition; Market power; Deregulation

1. Introduction

The German government implemented the EU-directive for a common electricity market with the introduction of the new Energy Act (Energiewirtschaftsgesetz,EnWG) on 29 April 1998. The intended competitive pressure engen-dered by the new act seems to have shaken up the sector considerably. Whereas the sector had traditionally been stabilized by an exemption from the general prohibition on cartels, it now seems that competition puts the firms under substantial pressure. The electricity supply industry (ESI) takes a prominent place in the public discussion. The nationwide firm EnBW entered the retail market for residential end-users with the phrase: “What’s the color of power?”, the trade-mark of EnBW being “Yello”. This seems to have triggered consumers’ awareness of the possibility to switch their power supplier. End-user prices have dropped quite dramatically and competition seems tough, especially in generation.

In accordance with the options provided by the

EU-* Corresponding author. Tel.:+49-(0)761-2032373 fax:+ 49-(0)761-2032372. url: http//www.vwl.uni-freiburg.de/fakultaet/vw/lehrstuhl.html.

E-mail addresses: [email protected] (G. Brunekreeft), [email protected] (K. Keller).

0957-1787/01/$ - see front matter2001 Elsevier Science Ltd. All rights reserved. PII: S 0 9 5 7 - 1 7 8 7 ( 0 1 ) 0 0 0 0 2 - 9

electricity-directive, the German government opted for Negotiated Third Party Access (nTPA) for the access regime to the networks. Consequently, there is no sector-specific regulator, access charges are unregulated and the details of network access have been left to the industry to work out. The control of anti-competitive behaviour is the task of the antitrust agency and the courts. After 2 years of experience, empirical evidence suggests a pattern which is in accordance with what was to be expected theoreti-cally. Since the network access charges are largely unregu-lated, whereas non-discriminatory access is closely moni-tored by the antitrust agency, the network owners, which are strongly vertically integrated in generation and retail, may be expected to make excess profits on the network, and not in the complementary competitive production stages. Thus, relatively strong competition (especially in generation) might indeed be expected, but at the expense of relatively high network access charges.

Underlying this argument is the Chicago-inspired theorem which may be called the “law of single mar-ginalization”.1 An unregulated input monopolist will

set a monopolistic input price and secure marginal-cost pricing at the complementary stage; in other words, it will attempt to secure an as-if competitive outcome at the complementary stage if it can compensate via the input price (here, the access charge). Under certain conditions the input monopolist will be indifferent between vertical integration into the complementary stage or vertical separation. In contrast, if the input price is regulated (sufficiently strongly), the input monopolist will have an incentive to attempt to lever the market power of the input stage to the complemen-tary stage in order to make monopoly profits at the complementary stage. In order to do so, it will have to foreclose and thereby exclude competitors from the complementary stage.

The German option for nTPA contrasts sharply with the other EU member states. Effectively all others opted for Regulated Third Party Access (rTPA) which implies a sector-specific regulator setting and controlling an access regime. This allows an interesting comparison of different systems. Throughout, the United Kingdom will be used as a comparator country.2 The structure of the

ESI in the UK is roughly comparable with the ESI in Germany and regulation of the ESI in the UK provides a perfect counterexample of the situation in Germany.

The primary aim of this contribution is to analyse the newly liberalized ESI in Germany. The secondary aim is to indicate empirically that network costs make up a relatively higher share of the electricity bill in Germany than in the UK, which in turn implies that the relative share of the competitive components (especially generation) is lower in Germany than in the UK. The paper is organized as follows. Section 2 will describe the legal environment of the ESI in Germany, with special attention to the so-called Association Agreement II (VV II),3 which arranges the network conditions. Section 3

characterizes the sector as a whole. In Section 4, price developments are examined in detail, with the ultimate purpose of indicating the ratio of network access costs as compared to the final electricity price. Section 5 offers some conclusions.

2. Institutional arrangements

It was a cumbersome way to the final consensus and the implementation of the new Energy Act4on 29 April

1998. Three aspects of the Energy Act are noticeable:

extensive discussion of the theory see Knieps and Brunekreeft (2000, Chap. 2).

2 Where appropriate (due to, for example, data-availability), the comparison is restricted to England and Wales.

3 In German:Verba¨ndevereinbarung. 4 EnWG (Energiewirtschaftsgesetz).

O First, there are no constraints on the vertical structure

of the sector.

O Second, access to the networks has been arranged by

Negotiated-TPA; this implies that both the structure

andthe level of the access charges are to be determ-ined by the industry.

O Third, allend-users have been declared eligible.

In many countries the ESI had been a monopoly in the strict sense; the German equivalent to this was an enforced cartelization in the form of territorial demar-cation (via the so-called demardemar-cation contracts). The main contribution of the Energy Act has been the abol-ishment of §103 of the antitrust law (Gesetz gegen Wettbewerbsbeschra¨nkungen (GWB)), which exempted the ESI from the general prohibition of cartels. The demarcation contracts are now deemed illegal, and a pre-viously artificially stabilized situation may turn out to be highly unstable. In principle, maximum competitive conditions are provided. Market-entry is completely free. New generation capacity is allowed by licensing (rather than tendering). Since demarcation contracts are now prohibited, new entrants do actually have a market. Right-of-use of public ground may no longer be granted exclusively; otherwise the Energy Act would contradict the EU-directive regarding the building of a direct line. All consumers are eligible and thus, retail-competition is possible for even the smallest end-users.

The Energy Act places no constraints on the vertical industry structure. Vertical separation has been discussed but turned out not to be feasible; vertical separation would require expropriation of the networks, which would contradict the constitution. Rather than prescrib-ing vertical separation, the degree of vertical integration appears to increase through take-overs, mergers and internal growth. The Energy Act does not prescribe the trading mechanism. Even if spot markets are currently arising (e.g. in Leipzig and Frankfurt), the main trading mechanism relies on bilateral contracting.

2.1. Negotiated TPA and the essential-facilities doctrine

Network access is dealt with in clause 6 of the Energy Act, which explicitly prescribes (non-discriminatory) nTPA, in accordance with clause 17 of the EU-Directive. The conditions (including pricing) of access are explicitly left to negotiations within the industry.5 The

industry has worked out the so-called Association Agreement (VV), which sets out the frame for network-access conditions. After a false start with the first version

of the Association Agreement (VV I), in December 1999 the industry agreed on a significantly improved version with VV II. Involved in these negotiations are (the associations of) the ESI (VDEW), the cogenerators (VIK) and industrial users (BDI). The (antitrust) control of the sector is left to the federal antitrust agency. To strengthen the position of the antitrust agency, the 6th reform of the competition law (GWB), in force from 1 January 1999, has included an essential-facilities doc-trine with clause 19(4)4 GWB. It states that it is an abuse of a dominant position to refuse access to the networks (or other facilities, which are deemed essential for competition) without practical justification, if it is not possible or not reasonable to duplicate the facility. The essential-facilities doctrine appears to be the main instru-ment to handle the network operators’ market power. The most important application of the essential-facilities doctrine was the decision of 30 August 1999 against BEWAG (Berlin), after it had refused access to its com-petitor RWE.

Even if the Energy Act does not contain sector-spe-cific regulation of the access charges, the competition law includes a provision of abuse of a dominant position. Clause 19(4)2 [GWB, 6th version] prohibits excessive pricing in case of a dominant position. Excessive pricing is defined as prices being higher than prices under “as-if competition”. Common practice for ident“as-ification of excessive pricing is (international) comparison. Even if identification of excessive pricing may be difficult in practice, the network operators are certainly not free to charge whatever they like.

A peculiar problem arises with full competition on the retail level; that is, competition for even the small-est end-users, which is possible since all consumers are eligible. Because the time-of-use meters, which are required for retail competition, are still too expensive for small end-users, demand-profiling is the alterna-tive. Although VV II (clause 4.1) suggests agreement that demand profiles shall be used, there is still no agreement for a precise method. Distributors tend to impede access to their network (e.g. by requiring to install a time-of-use meter) because they disagree with the demand-profile proposed by the competitors. Recently, the federal antitrust agency investigated a case against the distributor in Munich (Stadtwerke Mu¨nchen) on precisely this issue. Even if the distribu-tors’ argument seems sensible, they may run into trou-ble with respect to the non-discrimination provision in the competition law. The antitrust agency signalled that refusal of access was indeed discriminatory, because installing these time-of-use meters was not required for the Stadtwerke’s own retail department, only for competitors. The firms recently came to an agreement in which access is allowed.

2.2. Consequences for other acts

The new Energy Act and the subsequent liberalization practically forced modifications in other acts which are quite insightful. A first development concerns the end-user tariffs for small end-users (so-calledTarifkunden). Tariff ceilings have to be authorized by the ministry of eco-nomics at state level.6 It is rather suspect whether this

“regulation” of end-user prices is actually binding. For various reasons, doubts have been expressed about the effectiveness of the regulation. Since competition at the generation and retail level appears to develop quite well and end-user prices for small users decrease more rap-idly than expected, state ministries seem to consider further authorization of end-users prices as superfluous. In December 1999, the state of Baden-Wu¨rttemberg was the first to propose omitting authorization of the end-user prices.7 This development is difficult to assess. If

the regulation has indeed been intransparent and unspecified, then abolishing the decree creates trans-parency and a reduction of (regulatory) uncertainty. On the other hand, since the access charges are largely unregulated, regulation of end-user tariffs is the only control against excessive pricing. But then again, if a control of excessive pricing is desired, disaggregated regulation of the access charges would be superior to globally capping end-user prices. It is easier and more transparent to restrict regulatory attention to the monop-olistic bottleneck (i.e. the networks) rather than to the entire sector. If the stages generation and retail do indeed exhibit competition, it is principally unnecessary to regu-late them.8From this perspective, it may be desirable to

drop the control of the user prices. In case the end-user prices are perceived as being too high, the govern-ment should consider introducing disaggregated regu-lation of the access charges.

Another modification has been forced into the

so-called decree for concession fees

(Konzessionsabgabenverordnung (KAV)) of 1992. Communities have the right to grant concession for the use of public ground, for which they can charge a con-cession fee. The level of these fees has been laid down in the decree for concession fees. Among other things, the level of the fee, which is charged per kWh, differs for small users (Tarifkunden) and large users (Sondervertragskunden); the latter pay considerably less.9 This type of differentiation appears to be in

6 This regulation is based on the the Federal Electricity Tariff Decree (Bundestarifordnung fu¨r Elektrizita¨t(BTOElt)), 1990.

7 This still has to be approved by (federal) parliament.

8 It is beyond the scope of this paper to discuss this issue in depth. The interested reader may be referred to Knieps and Brunekreeft (2000), Crew (1999), Brunekreeft (1997) and Laffont and Tirole (1996) and the literature quoted therein.

accordance with the theory on price discrimination; demand of large users may be expected to be more elas-tic, because they may substitute away from electricity or in the long run decide against a specific site due to high concession fees. After liberalization, new retail-entrants bundled small end-users so that they could qualify as a large user and consequently by-pass the high concession fee. This is a textbook example of arbitrage destroying price discrimination. The associated losses for the com-munities were politically sensitive, so that a modification of the decree followed. Basically, arbitrage is now pro-hibited; the basis for charging the fee now is the voltage-level at which the end-user is connected to the network. If a retailer supplies an end-user with a voltage level below 1 kV, the end-user still qualifies as a small user despite the intermediate retailer. One may question whether the decree for concession fees is not outdated overall; the concession fee is actually a communal tax on electricity and perhaps it might be superior to treat it as such explicitly.

2.3. Network access: the Association Agreement II

By virtue of nTPA, it has been left to the industry to work out an agreement of the network-access conditions. On 22 May 1998, the Association Agreement I (VV I) was presented to the public. On 13 December 1999, this version was replaced by the Association Agreement II (VV II).

The first association agreement has been criticized as being anti-competitive and not suited for a competitive market. Since VV I is no longer in force, it suffices to be brief.10 The main point of criticism was that it was

based upon a contract-path principle rather than postage stamps. The capacity-based price (per contract!) intro-duced a bias in favour of long-term contracts with con-stant flows. This subcon-stantially hindered the development of a spot market; a spot market lives on many different short-term transactions. Furthermore, part of the pricing was distance related. For a contract, a fictional contract path was calculated for which a km-price was charged. This created an advantage for nearby power plants which tend to be the network-owners’ own plants. The dis-tance-related price has been criticized as discriminatory, because in an interconnected network distance-related pricing of electricity transmission lacks economic justi-fication. Nevertheless, it was authorized by the federal antitrust agency with the argument that it was not empirically relevant. Overall, the VV I has been assessed as being intransparent (due to the contract-path principle), cumbersome and as leaving undue potential for discriminatory behaviour for the system operators

10The interested reader may be referred to Perner and Riechmann (1998), Brattle Group (1998), or Bergman et al. (1999, pp. 152–155).

(especially with regard to ancillary services and reserve capacity). It should be noted that the latter are the incum-bent generators.

The Association Agreement II has repaired these shortcomings. With the VV II the structure of the access-charge regime in Germany adjusted quite strongly to what appears to become the standard in the EU.11Mind,

however, that this concerns thestructureof the charges, not the level. Several aspects are of interest.

The basis for the charges is a postage stamp (also called entry–exit system), i.e. they are not distance-related. Every end-user pays an annual connection charge based on his maximum load (kW). Generators do (transitionally) not contribute; their connection charge has been set at zero. The costs of energy losses and ancillary services are included in the connection charge and not charged separately. Only the costs of special requirements for reserve capacity are charged separately. Different network levels (voltage levels) are assigned different postage stamps. The end-user pays a connection charge at the level of his point of connection, which includes the sum12of the connection charges of all

sub-sequent higher network levels; in other words, the charges of higher network levels cascade to the lower levels. In effect, the distribution networks pay the con-nection charges for the transmission network and pass this on to their own connection charges. In contrast, in the UK, the suppliers/retailers and the generators pay the transmission costs, not the distribution networks. The connection charges are allowed to differ for different (regional) networks.

The cascading principle prescribes that the lower net-work pays a connection charge to the higher netnet-work. The basis for this charge is the maximum load at the point of connection of the lower network to the higher network. This principle is known as the net-principle; the lower network pays for the actual use of the higher network rather than for the mere option to use the higher network (which is thegross-principle). This implies that if relatively much decentralized power is fed into the lower network, the maximum load at the point of con-nection between the lower and the higher network will be relatively low. Consequently, the lower network’s contribution to cost-recovery of the higher network will be relatively small. The VV II states that the correspond-ing avoided costs (of the lower network) are paidtothe decentralized generator (normally CHP).

An empirically relevant variable is the so-called

coincidence factor. The average costs of a network are determined by dividing the annual costs of the network

11The VV II shows remarkable similarity to, for example, the so-called tariff code in the Netherlands; the latter was designed by the Dutch ESI, but had to be and has been authorized by the electricity regulator (DTe).

by the network’s maximum load. The user’s connection charge is based on the user’s maximum load which need not coincide with the network’s highest load. The coinci-dence factor takes account of this divergence; it is a stat-istically derived estimation of the probability that the user’s highest load coincides with the network’s highest load. Multiplying the coincidence factor with the user’s highest load approximates the expected value of the user’s share in the network’s highest load. The coinci-dence factor is a function of the load duration (in hours per year), which in turn is calculated as the annual con-sumption (in kWh) divided by the user’s maximum load (in kW). In effect, the coincidence factor is a function of (but not equivalent to) the load factor (which is load duration divided through 8760 h). Unfortunately, the VV II is not specific on the precise calculation of the coinci-dence factors; it is left to the network operators to work out a relation. The structure of the function proposed in the VV II is as follows:

g15a11

T* is a critical number of hours after which the

para-meters of the function change;T*is to be determined by

the network operator. Ti is the actual load duration of useri. It can be seen now that the coincidence factorg1

(g2) depends on a fixed number a1 (a2) (both.0) and

is linearly increasing in the load duration with b1 (b2)

(both .0).

This specification implies that the access charge con-sists of two different two-part tariffs expressed in indi-vidual load (DM/kW) and indiindi-vidual demand (Pf/kWh), where application depends on the load duration. This is how the network operators present their access charges. LetFrepresent the network’s connection charge per kW per year and Pia user’s maximum load. The individual annual connection expenditure, Ei, then is:

Ei5F·Pi·g(Ti)

which after using the expression for g1(Ti), becomes:

Ei5(a1·F·Pu)1

S

b1·F

T∗·Pi·Ti

D

.And for g2 similarly. It can be seen that in this

expression the individual access charge depends on the individual maximum load (Pi) and energy use (PiTi).

There happened to be one aspect in the VV II which triggered severe criticism: the so-called T-component. The idea was that the German transmission network would be divided into two different zones: a north-zone and a south-zone. If transactions passed the border between these zones, a price of 0.25 Pf/kWh would be charged. Since there is neither an obvious economic nor

technical reason for this charge, it was deemed anti-com-petitive. In the recent merger-cases (see Section 3), abol-ishment of the T-component within Germany has been one of the provisions for approval of the merger. In con-trast, there still is a cross-border T-component of 0.125 Pf/kWh.

Section 4 will in examine the level of the access charges as they have been presented recently by the net-work operators. With respect to the structure, four points can be stated as an overall assessment:

O The Association Agreement II is based on postage stamps rather than on the contract-path principle (as was the VV I). Since distance-related pricing was abolished, the access charge structure is largely non-discriminatory.

O The structure of the access charges, as set out in the

Association Agreement II, enables the development of spot markets.

O The VV II does not set incentives for efficient

short-term use of the networks, since no explicit account of energy losses is taken. Moreover, no incentives are set for efficient investment of generation-capacity to take proper account of the network-configuration, since (transitionally) the generators do not contribute to the costs of the network.

O The degree of differentiation in the tariff-structure is low. An explicit peak-load element is lacking. At the moment, the structure of the access charges does not seem to fit the structure of the end-user prices very well.

3. The sector

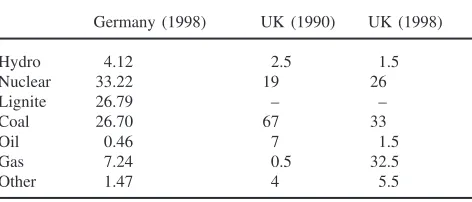

Total electricity generation (for the public network) in Germany in 1998 was 457 TWh, with an installed capacity of 98 GW. Compared with the maximum load of little over 70 GW there appears to be substantial excess capacity. The generation-mix is given in Table 1, with the two columns on the right giving the

generation-Table 1

Generation mix (based on production)a

Germany (1998) UK (1990) UK (1998)

mix in the UK for 1990 and 1998. German electricity generation still relies quite heavily on coal (and lignite); domestic coal is still (although decreasingly so) subsid-ized for socio-political reasons. The use of lignite stems mainly from special arrangements for East-Germany, which is an inheritance of reunification.

The comparison suggests that the mix in Germany is roughly comparable with the mix in the UK as it was at the time of liberalization. After liberalization, the UK witnessed a strong increase of mostly independent gas-fueled CCGT-generators (“the dash for gas”), at the expense of coal. It is noticeable that the planned and projected capacity expansion (up to 2002) in Germany is 3.5 GW lignite and 1.3 GW gas (VDEW, 1999, p. 79). This figure is probably an underestimation, because the retreat from nuclear power has been decided by government in the Summer of 2000. Although this will be a phased retreat over 30 years, it nevertheless opens up opportunities for new capacity.

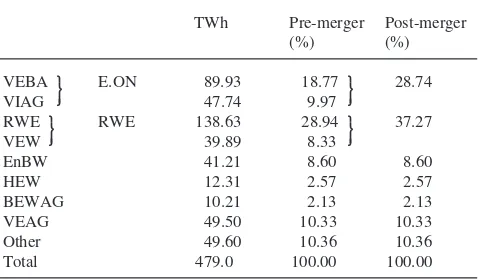

Unlike many other European countries (e.g. UK, France, Italy), the German ESI was not monopolized in a strict sense. There have been and still are many firms. Until recently, up to 1000 firms were involved in the public provision of electricity. At present, this figure is declining rapidly. Despite the fairly large number of firms, the ESI has been quite concentrated both horizon-tally and vertically. Until recently eight firms, the so-calledVerbundunternehmen(VUs) dominated the sector:

RWE, VIAG (i.e. Bayernwerk), VEBA (i.e.

PreussenElektra), EnBW, VEAG, HEW, VEW and BEWAG. Things are changing rapidly. In July 2000, a merger between RWE and VEW (now under the name RWE) on the one hand and VEBA and VIAG (now under the name E.ON) on the other hand reduced the number of VUs to six. Together these six firms control up to 80% of the generation capacity in Germany and produce up to 90% of the total production. They each control an extra-high-voltage network and together they exclusively (but not collectively) control the German transmission network. Moreover, these six VUs own and operate a significant number of distribution networks. As intended (or rather, not prohibited) by the Energy Act, the owner of the network is also the system operator. Most of these firms supply small and large end-users either directly through a fully owned subsidiary or through a participation in communal retailers.

Apart from these six VUs, there is a vast number of regional and especially communal distributors/retailers. As a rule, the communities have taken over responsi-bility for the final stage of public utilities. Sectors like electricity, gas, water, public transport and waste dis-posal may be separate legal entities, but are fully or partly owned by communal holdings (Stadtwerke), which are completely owned by the communities. These communal utilities traditionally both owned the distri-bution network and handled retail for the consumers

con-nected to the corresponding distribution network; i.e. the distribution network demarcated a closed service area. Although the communal distributors concentrate on dis-tribution and retail, they do own some generation capacity as well, especially CHP.

The communal retailers are striving for scale-enlarge-ment. Before liberalization, there were roughly up to 1000 communal retailers. Not surprisingly, the average scale of these communal retailers turns out to be too small. With billing, advertising and especially purchase of electricity on rather complex wholesale markets, scale effects can be realized. As a result, the list of cooperations between communal retailers, be it by merger, tight or loose cooperation or joint venture, is huge. In the world before liberalization, distribution and retail were one and the same and the retail service area was defined as the group of consumers connected to a specific distribution network. After liberalization, distri-bution and retail are definitely separate stages and the phrase “service area” has become meaningless. The tra-ditional concept of the communal retailer (Stadtwerke) will soon be history and many of these may be expected to either withdraw form the electricity market com-pletely or concentrate on the distribution network and leave the retail to other firms. A recent example of the latter strategy is Stadtwerke Jena (ZfK, 2000, p. 1).13

The VUs are actively buying distributors/retailers; they are penetrating the retail market on a large scale. One reason for this may be to “secure” the sale of pro-duced electricity. Shortly after liberalization, the communal retailers started switching their suppliers (i.e. the VUs). One way of responding to this is to set up a retail department and sell directly to the end-users. Another way is to buy the retailer. In the face of (idiosyncratic) excess generation capacity, this may lower transaction costs by lowering risks.14Another

rea-son may be that many communal retailers are simply too small and not sufficiently specialized to be competitive. If they are bought by the (far larger) VU, many small retailers are effectively merged into one large retailer. This also seems to aim at increasing efficiency (and ther-eby competitiveness) rather than increasing market power. In one case, the federal antitrust agency raised concern about increased concentration on the retail mar-ket as PreussenElektra intended to increase its partici-pation in the communal retailer Stadtwerke Bremen; on 5 May 1999 a lower-court in Berlin ruled that, due to liberalization, the relevant market for retail had widened to at least the national market and, consequently, that the increased participation would not substantially lessen competition.15

Forward integration may also focus on acquiring dis-tribution networks (rather than the retail stage). Apart from synergy effects, the argument of double mar-ginalization may fit. The transmission network and the distribution network are complementary stages, and if both stages charge an excessive mark-up independently from each other, the result will be worse for both the network owners and the consumers as compared to verti-cal integration.

It seems that the sector’s tendency for vertical concen-tration is merely an adjustment to new market circum-stances and increases efficiency; at present, there seems to be no antitrust-concern with this type of integration. For this conclusion, the proper framework must be stressed. Antitrust concerns arise where vertical inte-grationincreasesthe possibility or likelihood of leverage of market power. This requires that a monopolistic stage integrates into a competitive stage, which is not the case here. The current state of affairs is that the distribution networks are already integrated with retail, and the trans-mission network with generation. Integration of these two blocks does notincreasethe possibility of leverage of market power; this possibility is already given. If leverage of market power is considered a problem at all, then the monopolistic network-stages should be verti-cally separated from the competitive generation- and retail-stages. Apart from this, doubts can be raised about the incentives of the network operators; since the access charges are unregulated, and thus excessive profits can be made on the networks as such, they should not have an (anticompetitive) incentive to lever market power to the competitive stages.

The market shares in generation, taking account of share participation, are presented in Table 2; the pre-merger and post-pre-merger situation is presented separately. To recall, VEBA and VIAG merged to E.ON, and RWE and VEW merged under the name of RWE. The figures have been corrected for the shares of VEAG; a provision for the mergers was the sale of the VEAG shares under

Table 2

Market shares in productiona

TWh Pre-merger Post-merger

aSource: Europa¨ische Kommission (2000, p. 23). Note: these shares are corrected for participation shares.

Table 3

Concentration ratios in generation outputa

HHIb CR1 CR2 CR3 CR4

Germany; pre- |1560 0.289 0.477 0.581 0.680 mergers

Germany; post- |2417 0.373 0.660 0.763 0.850 mergers

UK (1990/91) |3225 0.455 0.739 0.913 0.983 UK (1998/99) |1620 0.210 0.420 0.597 0.768

a Source: Calculations based on Europa¨ische Kommission (2000) and EA (2000). Note: pre- and post-merger refers to the RWE-VEW and VEBA-VIAG mergers.

b HHI means Hirschman–Herfindahl Index, which is the sum of squared market shares of all firms (10 000 is monopoly). CR is the sum of the market shares of the largest firms.

control of the merging parties. Table 3 presents different concentration ratios from these figures and compares these with similar figures from the UK. It can be seen that the pre-merger concentration ratios were quite simi-lar; whereas the concentration ratios in the UK show a steady decline since liberalization, the recent mergers and take-overs in Germany increase concentration above those of the UK.

The ownership of the firms is mixed. Table 4 provides an impression for 1998 (VDEW, 1999, Table 12). In this table public is defined as more than 95% in public-own-ership, mixed as less than 95% public- and less than 75% private-ownership, and finally private as more than 75% private-ownership.

Two things are immediately suggested by these fig-ures. The majority of the firms are in public hands and only few in private hands. Simultaneously, production is biased towards mixed ownership but comparatively strongly biased towards private. This is caused by the communal distributors, which are relatively small but large in numbers and are mainly in public hands, whereas the VUs, which are large firms but small in numbers, are mostly privately owned and/or mixed. This is confirmed by the observation that the share of private firms in the retail to end-users is relatively small com-pared to the share of private firms in generation. The core-activities of VUs is generation and they increase

Table 4

Ownership of the ESI in Germany in 1998a Generation Retail

% in no. of % in output % in no. of % in supply

firms firms

Public 61.5 4.6 63.5 27.4

Mixed 25.9 56.8 24.3 62.9

Private 12.6 38.6 12.2 9.7

their activities in retail. As a rule, the VUs are mainly privately owned and the communal distributors are mainly in public-ownership. Since, however, the VUs are acquiring the distributors, these figures will change and more of the sector will be in private hands.

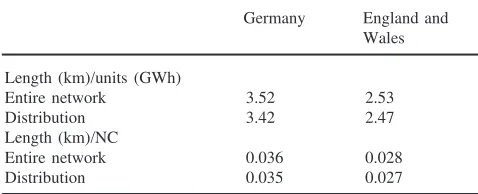

Table 5 provides an impression of the network con-figuration in both countries. The length of the network is expressed as a ratio of units distributed and as a ratio of the number of customers connected to the network. A subdivision has been made between the entire network (transmission and distribution) and the distribution net-works alone. No further specification has been made; the costs of the network depend on many factors and it would require a detailed benchmark study to come to reliable conclusions about the relative costs of the net-works. The figures in Table 5 are intended to give an impression, which should be taken with care. The com-parison indicates that the network in Germany is some-what more extensive. This might cause somesome-what higher average network costs in Germany.

4. Development of prices and assessment

The first year of liberalization of the German ESI was characterized by the setting of the frame (e.g. by probing the antitrust agency and the VV I) and the strategic reorganization of the firms and the sector. The second year witnessed severe competition for end-users; the VUs aggressively penetrated the retail-market, attracting large-scale attention of the media.

In August 1999, the VUs announced their nationwide offers for residential end-users with press-conferences, television-spots and page-sized advertisements in national newspapers. Thereby, they informed the public of the possibility to switch their electricity supplier and they started competition with communal retailers and among each other. Targeting for the masses, rather than using the firm-name, they introduced brand-names:

Avanza (RWE), Yello (EnBW), ElektraDirekt

(PreussenElektra), POWERfamily/POWERprivate

Table 5

Indication of network characteristicsa

Germany England and Wales Length (km)/units (GWh)

Entire network 3.52 2.53

Distribution 3.42 2.47

Length (km)/NC

Entire network 0.036 0.028

Distribution 0.035 0.027

aSources: VDEW (1999) and EA (2000). Note: NC means Number of Customers. For Germany, values are those for 1998, for England and Wales, values are those for 1998/99.

(Bayernwerk). This was also the moment when prices started to fall sharply. The communal retailers had no choice but to react and lower their prices. Apart from competition among incumbent firms, several new traders or retailers have entered the market with nationwide offers. As a rule, the retailer takes care of all arrange-ments with the network operator(s), including reading of the meter.

There is little (publicly available) information on actual switching of consumers. A market survey by GfK16suggests actual switching of residential users was

5% in May 2000, which is rather low. There are some market surveys on the willingness-to-switch. It is notice-able that the brand-names do have an effect. FAZ (1999) reports a remarkable popularity of Yello. This indicates that despite the homogeneity of the product, some pro-duct differentiation may be possible. The magazine Stern (1999) conducted a market-survey on the willingness to switch. In September 1999 (i.e. directly after the VUs started their campaign), around 75% of those inter-viewed said that they were informed about the possibility to switch; 15% considered themselves very well infor-med. Around two-thirds of those interviewed answered that they are principally willing to switch in order to save on the monthly bill. For a majority of these, the expected cost-saving should be at least 20%.

4.1. End-user prices

Figs. 1 and 2 plot the developments of end-user prices for business users and residential users respectively. The price drop for industrial users continued for somewhat longer now and the trend downwards is obvious. Fig. 1 shows that the price level for business consumers is fall-ing constantly, accordfall-ing to VIK (1999) up to 15% on average within 2 years. These figures stem from VIK and coincide with, but are more extensive than Eurostat-data. This figure is an average of 13 differently sized industrial customers, and is averaged for a sample (43) of suppliers around the country. The customers range from 100 kW with 1600 h load duration to 25 MW with 7000 h load duration. The former relates to the Eurostat-data as the categories Ic and higher, whereas the 25 MW users do not appear in the data. The Eurostat-categories Ia and Ib are commercial users and do not appear in the VIK-data. The industrial users are assumed to be connected at the MV-network (normally 10/20 kV).17 The price data include all price components,

exclusive of VAT. Industrial users pay approx. 0.5 Pf/kWh electricity tax (which has recently been introduced) and the concession fee, which for industrial

16Compare http://www.gfk.de.

Fig. 1. Development of industrial prices. Source: VIK (1999); www.vik-online.de.

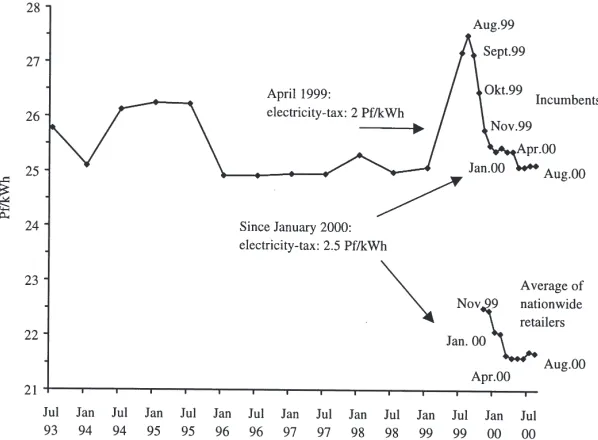

Fig. 2. Development of prices of residential users (with an annual consumption of 3500 kWh). Source: Statistisches Bundesamt; own calculations. Prices exclude VAT, but include electricity-tax.

users is 0.22 Pf/kWh. The apparent discontinuity in the price decline has a methodological explanation; the data are collected and assessed every half year rather than continuously. It is clear that a severe decline has set in, which points to strong competition for large end-users. Fig. 2 plots the development of residential end-user prices. A sharp price-drop occurred in August 1999; this was the moment the VUs started their nationwide offers for the residential retail market. This severe decline in prices is not immediately obvious from Fig. 2, because during the liberalization process an electricity tax was introduced. Formally this is an eco-tax, but actually it is a tax on electricity consumption expressed in Pf/kWh. In April 1999, this tax was introduced with 2 Pf/kWh and in January 2000 it was raised by another 0.5 Pf/kWh, so that the electricity-tax now is 2.5 Pf/kWh. Fig. 2 includes the electricity tax, but is exclusive of VAT.

The data are calculated for a typical domestic user; i.e. a user with an annual consumption of 3500 kWh (assumed load is 7 kW). This corresponds to the Euros-tat-category Dc, is used by the German Statistical Office and is very similar to what is used to characterize the typical domestic user in the UK as well (e.g. by OFGEM and the Electricity Association).

consumer has no choice but to purchase from his incum-bent supplier. Moreover, since there are regional differ-ences, an adjusted national averageof suppliers should be used to express the random probability of a represen-tative consumer living somewhere. Most communal sup-pliers do not supply electricity nationwide, but restrict their offers to the former service area.

With liberalization, end-users do have a choice, how-ever. Normally this choice is between the incumbent communal supplier and the nationwide suppliers, which, as mentioned before, are present as from August 1999. Nationwide suppliers are retailers (like Avanza or Yello), which do not have a service area in a traditional sense, but simply make an offer which is valid anywhere in the country. It turns out that the nationwide suppliers have significantly lower prices than the communal incumbents; in other words, seen from the perspective of an incumbent retailer, the entrants offer significantly lower prices. To reflects these differences, for November 1999 and onwards, two variations have been used to cal-culate end-user prices: first, as in the method of the Stat-istical Office, a national average of (mainly) incumbent communal suppliers, and second theaverage of (a selec-tion of) naselec-tionwide suppliers. The advantage of the latter is that it corresponds to the availability of choice because it emphasizes best practice. The disadvantage is that it neglects the fact that most consumers are still supplied by their communal retailers which tend to have higher prices than the nationwide suppliers. The data we used for the calculations mainly stem from an internet-based tariff-calculator of the IWR.18

Both methods are plotted in Fig. 2. First note the sharp increase in prices due to the introduction of the elec-tricity-tax in April 1999. The first round (2 Pf/kWh) appears to have been passed through to the end-users completely. The raise of the electricity-tax in January 2000, in contrast, has not been passed on to the end-users; on the other hand, the additional 0.5 Pf/kWh in January 2000 may have slowed down further price decrease. Accounting for the effect of the electricity-tax, it can be seen directly that the last few months of 1999 witnessed a sharp decrease in end-user prices. From Jan-uary 2000 onwards the price level seems to become stab-ilized or even increase somewhat. It can be seen as well that there appears to be a persistent difference between the prices of the nationwide suppliers (i.e. the entrants) and the national average of communal suppliers (i.e. the incumbents). This difference is approx. 3.5 Pf/kWh, which is approx. 14% of the incumbent end-user tariff (|25.38 Pf/kWh). For a 3500 kWh user, switching would amount to a saving of DM 122.50 per year.

Apparently, there are switching costs involved. One is that several communal suppliers charge approx. DM

18www.iwr.de.

50 for an additional meter-reading, which may be involved in switching. A second indication is the above-mentioned Stern (1999) report which suggests that a majority of end-users would consider switching only if they can save up to 20%. Similar indications come from the UK (OFGEM, 1999a).

Most importantly, residential end-user prices declined (net of the electricity tax) by 7.3% measured for the incumbents’ tariffs and almost 22%, if the nationwide suppliers are taken as a reference. The price decrease is at least partly induced by increased productivity; an analysis of the development of total factor productivity suggests an improvement of 12% from 1994 to 1998. This figure is expected to increase further since the firms are heavily cutting down the labor force; in time the improved TFP should be reflected in lower costs.19

The current price level in Germany may be compared with the UK. EA (2000, p. 32) reveals that a typical domestic tariff (3300 kWh) in the UK in 1999 was 23.25 Pf/kWh (VAT excl.).20 The incumbent tariffs in

Ger-many are higher than this, but not very much so, while the nationwide offers are lower. Roughly speaking, the difference in prices for the typical domestic end-user between Germany and the UK seems small, if it is taken into account that in the German prices the electricity tax and the concession fee are included, for which there is no equivalent in the UK.21

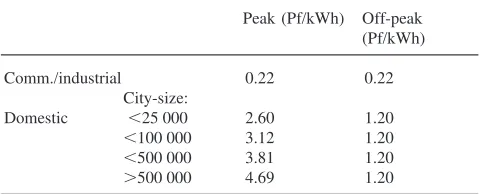

As mentioned above, the electricity tax is 2.5 Pf/kWh for domestic users. The concession fee is differentiated and depends on three criteria: first, whether a user is domestic or commercial/industrial, second, the size of the city and third, day and night differentiation. The ceil-ings are laid down in the so-called Konzessionsabgaben-verordnung and are presented in Table 6. The Eurostat-category Dc assumes an annual consumption of 3500 kWh of which 1300 kWh at night. A representative value of the concession fee for 3500 kWh-domestic users can be calculated by taking an unweighted average for the

Table 6

Concession fees in Pf/kWha

Peak (Pf/kWh) Off-peak (Pf/kWh)

Comm./industrial 0.22 0.22

City-size:

Domestic ,25 000 2.60 1.20

,100 000 3.12 1.20

,500 000 3.81 1.20

.500 000 4.69 1.20

a Source: Konzessionsabgabenverordnung.

19For further details see Brunekreeft and Keller (2000). 20Using £1=DM 3.

city-size and using the eurostat quantity weights for the peak-load element. This results in a value of 2.7 Pf/kWh. There are two more taxes. First, a levy for renewable energies. Second, since 1 July 2000, a transitionary levy to recover stranded costs in CHP at the communal level. The first is very low and the second is too recent to have had an effect on observable prices. Both can be neglected empirically.

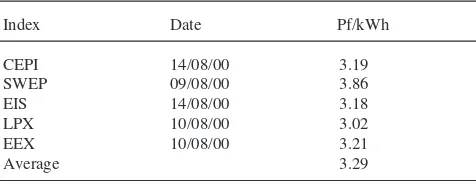

It is quite problematic to get a reliable estimate of the wholesale prices of electricity and we leave this for further research. It may be illustrative, however, to get an idea of the spot prices within the German network, which is given in Table 7. Especially LPX and EEX22

are interesting. Both are newly established power pools in Leipzig and Frankfurt/Main, respectively. It will be interesting to see whether the spot prices at both markets converge in the long run, because it would mean that the transmission network operates without significant energy losses and that the network access charges (at the highest voltage level) do not disturb free trade. The average of 3.29 Pf/kWh is rather low. To compare, EA (2000, p. 37) reveals that the (time-weighted) 1998/99 System Marginal Price in the electricity pool of England and Wales was 7.08 Pf/kWh. It seems plausible that the 3.29 Pf/kWh expresses marginal-costs pricing of excess capacity, which is especially large in the Summer.23 It

is unlikely that this price would suffice to recover all costs of generation and it is unlikely that the wholesale contract prices of electricity are generally this low. How-ever, the spot price and bilateral contract price should of course converge.

4.2. Network access charges

Since July 2000, most network operators have pub-lished their network access charges, whose structure

Table 7

Spot prices in Germany on a summer workdaya

Index Date Pf/kWh

aSources: www.cepi.dowpower.com; internet sites of LPX and EEX. Note: averages are unweighted, where applicable.

22Leipzig Power Exchange and European Energy Exchange, respectively.

23It is illustrative that E.ON announced in a press-release at the end of August 2000 its intention to disconnect some capacity.

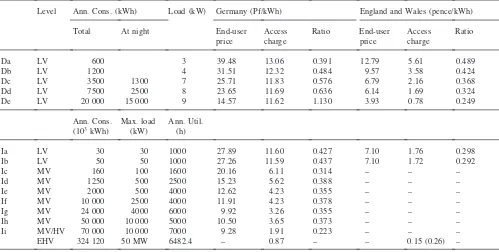

relies on the VV II. Table 8 gives an unweighted average of 14 firms, among which are the (formerly) eight VUs. As explained in Section 2, the precise charges depend on network-connection level, maximum load and load duration. The access charges have been calculated exclusive of metering costs. Because the Eurostat-cate-gorization appears to have gained wide acceptance, this categorization has been used to calculate access charges for different users. The table compares the access charges with the end-user prices, which for reasons of consistency are taken from eurostat. The Eurostat end-user prices relate closely to the national average of incumbent prices used in Figs. 1 and 2; the end-user prices of entrants (nationwide suppliers) would, at least for domestic users, be significantly lower. Column 8 of the table presents the ratio of network access charges to the end-user price; in this calculation the end-user price has been cleaned for the electricity tax and the con-cession fee. Similar ratios have been calculated for England and Wales for domestic and commercial users. A calculation for industrial users will be left for further research, because the available data are not sufficiently reliable to make such a comparison. The figures are without VAT.

The last line of the table provides an impression of extra-high-voltage transmission prices. These figures should be taken with utmost care. It is an indication for one type of “supercustomer” only (50 MW and a load factor of 0.74). For Germany the figure has been calcu-lated as an unweighted average of various EHV-net-works. For England and Wales, it is more problematic. The figure is calculated from the unweighted average of National Grid Company’s demand-zone connection charges, using a load factor of 0.74. It thereby represents what a “supercustomer” would pay NGC as a use-of-system charge. It neither includes the generation-zone charges (which are paid by the generators), nor the uplift-element in the electricity price. The latter reflects, in particular, the costs of energy losses. In the German system, both these elements are included in the network access charge as calculated here, whereas in England and Wales, these elements return in the electricity price. It is problematic to estimate a mark-up which would take account of this problem, because it is unclear how these elements are spread over various customers. If, however, the generation-zone charge and the uplift-element are included in the EHV-charge proportional to demand (kWh), the figure in round brackets would apply. With the reservations made above, the figures in the table seem to suggest that the EHV-charges in England and Wales may be lower than in Germany, but possibly not much lower.

Table 8

share of network access charges in the end-user pricesa

Level Ann. Cons. (kWh) Load (kW) Germany (Pf/kWh) England and Wales (pence/kWh)

Total At night End-user Access Ratio End-user Access Ratio

price charge price charge

Da LV 600 3 39.48 13.06 0.391 12.79 5.61 0.489

Db LV 1200 4 31.51 12.32 0.484 9.57 3.58 0.424

Dc LV 3500 1300 7 25.71 11.83 0.576 6.79 2.16 0.368

Dd LV 7500 2500 8 23.65 11.69 0.636 6.14 1.69 0.324

De LV 20 000 15 000 9 14.57 11.62 1.130 3.93 0.78 0.249

Ann. Cons. Max. load Ann. Util. (103kWh) (kW) (h)

Ia LV 30 30 1000 27.89 11.60 0.427 7.10 1.76 0.298

Ib LV 50 50 1000 27.26 11.59 0.437 7.10 1.72 0.292

Ic MV 160 100 1600 20.16 6.11 0.314 – – –

Id MV 1250 500 2500 15.23 5.62 0.388 – – –

Ie MV 2000 500 4000 12.62 4.23 0.355 – – –

If MV 10 000 2500 4000 11.91 4.23 0.378 – – –

Ig MV 24 000 4000 6000 9.92 3.26 0.355 – – –

Ih MV 50 000 10 000 5000 10.50 3.65 0.373 – – –

Ii MV/HV 70 000 10 000 7000 9.28 1.91 0.223 – – –

EHV 324 120 50 MW 6482.4 – 0.87 – – 0.15 (0.26) –

aSources: End-user prices: Eurostat (for Germany January 2000; for E&W July 1999); end-user prices E&W for Ia and Ib calculated from CRI (1998); access charges Germany: price information of the firms; access charges E&W: calculated from CRI (1998). Note: values for Germany are for 2000, and values for E&W are for 1999.

from the end-user price. For all domestic users, the elec-tricity tax has been assumed as 2.5 Pf/kWh, and for com-mercial and industrial users 0.5 Pf/kWh. The concession fee has been calculated according to the method described in Table 6, with a peak/off-peak weighting according to the Eurostat-categorization as in Table 8. For commercial and industrial users it has been set at 0.22 Pf/kWh. Due to the cascading principle in the struc-ture of the access charges in Germany, the final access charge automatically includes costs of transmission (EHV). The end-user prices are January 2000 prices and the access charges are July/August 2000 values. A small lag is unavoidable if Eurostat-data are to be used; the access charges cannot be set at January 2000, because the values based on VV II have only been published since July 2000. As shown in Figs. 1 and 2, however, the end-user prices do not seem to have changed signifi-cantly anymore since January 2000. Consequently, this short time lag should not pose a problem.

The structure in England and Wales is non-cascading; transmission costs are charged to suppliers and gener-ators and not passed through to the distribution network. Consequently, the transmission costs show up in the energy part of the end-user price and not in the distri-bution part. Column 10, the distridistri-bution charge, does not include the transmission costs. To make a comparison with Germany consistent, the transmission costs should be taken account of, however. To calculate the ratio of

network access charge to end-user price for England and Wales, the transmission costs has simply been set at 5% of the end-user price,24which then is used as a mark-up

on the distribution charge.

The data for E&W are 1999 values; they should be updated as soon as sufficient data are available. During 1999, OFGEM conducted reviews of the price caps of supply and distribution, which incorporate significant price changes. OFGEM (1999b) shows that the distri-bution charges will have a one-off of over 20% on aver-age in 2000/01, while the supply prices (in the domestic market) will have a one-off of slightly over 5%. Conse-quently, the 1999-ratios calculated for England and Wales in the table overestimate the 2000 values. It might provide a rough indication to use the 1999 prices and apply the average one-offs in order to estimate 2000 values, but it would be correct only by coincidence; it is not clear how exactly the one-offs will be spread over the various user groups.

The category De shows a remarkable value for Ger-many: the ratio is higher than 1, which would mean that the network charges are higher than the end-user prices, which in turn means that they are implicitly subsidized by the supplier (which will normally be the network owner). This implies that no alternative suppliers will

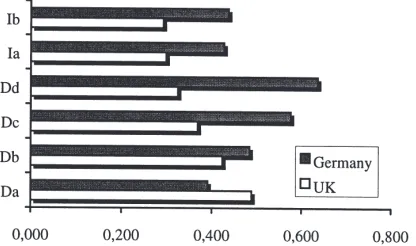

have an interest to compete for this group. This is most likely the result of not-perfectly adjusted tariff-structures of end-user prices on the one hand and distribution charges on the other hand. The former have an explicit peak-load element, while the latter do not. The flaw is noticeable for the De-category because 75% of the con-sumption is assumed to be in the off-peak period. This category does not seem to have empirical relevance in either Germany or England and Wales and can be ignored. Fig. 3 plots the ratios from Table 8, where the category De has been removed.

Fig. 3 strongly suggests that the ratio of network access charges to end-user prices is indeed significantly higher in Germany than in England and Wales. This con-clusion is further strengthened if one considers that the empirically most relevant categories are Dc and Dd.25

Moreover, the figures may underestimate true values for two reasons. First, it may be recalled that the England and Wales values are 1999 values, while the 2000 values may be expected to increase the difference between the two countries. Second, the access charges for Germany have been calculated not including metering-costs, which appear to be quite high and may make a difference depending on the type of customer.

It is remarkable to see that the share of access charges rises with larger customer size in Germany, whereas it falls in the UK. A closer look at Table 8 reveals that in Germany the end-user price falls with customer size, whereas the access charges are relatively constant. In the UK, the structure of the access charges and the end-user prices are adjusted with respect to customer size. Since the network is monopolistic and retail is not, one would actually expect the share of access charges to fall some-what with increasing customer size. This seems to imply that price differentiation of the access charges in Ger-many is not sufficiently strong. It can be expected that this will be modified in the near future.

Fig. 3. Ratio of network access charges to end-user prices. Source: own calculations.

25Approximately 90% of all households fall into the categories Dc and Dd (according to a media-release of VDEW; compare www.strom.de).

Fig. 3 appears to confirm the assertion that the unregu-lated German ESI concentrates on making profits on the genuine monopolistic bottlenecks: the networks. This will allow setting relatively low mark-ups for energy and retail and further imply that competition at the competi-tive stages (especially generation), despite increased concentration, may be relatively strong. Thus it is sug-gested that the “law of single marginalization” may to some extent apply for this particular case. It should be realized that this would be the natural result of the governmental choice of not regulating the network access charges. It should be realized, moreover, that this kind of access pricing is not discriminatory per se. It may be monopolistic pricing, but it may as well correspond to what an unregulated vertically separated network oper-ator would do. In other words, and allowing exceptions to the rule, this kind of pricing may well correspond to internal-transfer pricing.26 However, the profit margins

on both the generation- and the retail-stage will of course be small, because the monopolistic bottleneck operator is not going to leave rents on the competitive comp-lementary stages. Actually, if marginal costs are lower than average costs on the complementary stages, one would expect negative rents on the complementary stages; for the integrated firm, marginal-cost pricing on the complementary stage (and monopolistic pricing from the network) would be profit-maximizing. This may apply especially to the generation stage. Needless to say that independent competitors without a network of their own would not have a chance in such circumstances. Whether this qualifies as a price squeeze and/or should be considered predatory will be left to the antitrust auth-orities to decide.

It should be emphasized, however, that the law of sin-gle marginalization is a polar case and serves as a refer-ence only. There are several reasons why the network owner would still have an incentive to discriminate against third parties explicitly. Various media report regularly of complaints about discriminatory behavior, especially by the distributors. Moreover, there may be differences in the network characteristics between the two countries which could justify differences in the ratios to some extent. One example is that the German network appears to be relatively extensive, as shown in Table 5. This might justify higher average costs. Such and other considerations may tone down the asserted result.

5. Conclusions

This paper analyses and assesses the competitiveness of the electricity supply industry in Germany. Full lib-eralization of the market took place in April 1998 with the implementation of a new Energy Act. The German implementation of the EU-electricity-directive deviates sharply from other EU-member states. The most notice-able difference is the option for negotiated Third Party Access; almost without exception, the other EU-mem-ber-states opted for regulated Third Party Access. Obvi-ously, the networks (transmission and distribution) are monopolies with market power and it seems natural to have a sector-specific regulator securing non-discrimi-natory TPA (in order to stimulate competition in gener-ation and retail)andcapping the level of access charges. In the German electricity supply industry, non-discrimi-nation is monitored by the federal antitrust agency, while the level of the access charges is not regulated. This dif-ferent choice makes Germany an interesting case-study. The access regime is developed by the industry and controlled by the federal antitrust agency. The so-called association agreement sets out the conditions for access; to emphasize, only the structure is set out, not the level of the access charges. As from January 2000, the Associ-ation Agreement II is in force, which is broadly in line with what seems to become the European standard. Apart from the option for negotiated TPA, two other characteristics of the Energy Act should be noted. First, there are no constraints on the industry structure (neither vertically, nor horizontally), except for the general con-straints from the competition act. This implies that, in contrast to other countries, there is no such thing as verti-cal separation. Second, Germany chose to open the mar-ket completely; i.e.allconsumers are eligible, which in principle allows a maximum degree of (retail) compe-tition.

The developments can be summarized as follows. Competition in generation and retail for both industrial and residential end-users is surprisingly strong. It has become easy to switch between a wide choice of firms. Spot prices on wholesale markets are very low. Con-sumers seem well informed and willing to switch, although actual switching of domestic end-users is still rather low. End-user prices for both industrial and resi-dential users have effectively decreased substantially (on average up to 20%). On the other hand, the network access charges are relatively high. A close examination of the share of network access charges in the end-user prices suggests that this ratio is significantly higher in Germany than in the UK.

Overall, an assessment may be that competition at the generation and retail stages seems to be working, but this may very well be at the expense of excessive access charges. Theoretical reflection would suggest that the vertically integrated network operators concentrate on

making profits on the monopolistic networks and not on the competitive complementary stages (generation and retail). After all, the networks and thereby the level of the access charges are unregulated, whereas foreclosure of the competitive stages is monitored by the antitrust agency. This theoretical reflection appears to be con-firmed by empirical developments.

Acknowledgements

The authors are grateful to Richard Green, Christoph Mu¨ller, Christoph Riechmann and the participants of seminars at the DAE (university of Cambridge), the CMuR (university of Warwick) and the Annual Euro-pean Energy Conference 2000 in Bergen (Norway), and an anonymous referee for useful comments.

References

Bergman, L., Brunekreeft, G., Doyle, C., von der Fehr, N.-H., Newb-ery, D.M., Pollitt, M., Re´gibeau, P., 1999. A European Market for Electricity? Monitoring European Deregulation No. 2. CEPR/SNS, London.

Bork, R., 1978. The Antitrust Paradox: A Policy at War with Itself. Free Press, New York.

Brattle Group, 1998. Netzzugang in Deutschland im Vergleich zu anderen U¨ bertragungsma¨rkten. Brattle Group, London.

Brunekreeft, G., 1997. Local versus global price cap: a comparison of foreclosure incentives. Discussion Paper, No. 36, June, University of Freiburg.

Brunekreeft, G., 1999. Light-handed Regulierung des Zugangs zu Infrastrukturen: Das Beispiel Neuseeland. DVWG Reihe B 224: Diskriminierungsfreier Zugang zu (Verkehrs-)Infrastrukturen. DVWG, Bergisch-Gladbach, pp. 82–103.

Brunekreeft, G., Keller, K., 2000. Netzzugangsregime und aktuelle Marktentwicklung im deutschen Elektrizita¨tssektor. Zeitschrift fu¨r Energiewirtschaft 24 (3), 155–166.

Crew, M. (Ed.), 1999. Regulation Under Increasing Competition. Kluwer Academic, New York.

CRI, 1998. The UK Electricity Industry Charges for Electricity Ser-vices 1998/99. CIPFA, London.

EA, 2000. Electricity Industry Review 4. Electricity Association, Lon-don.

Europa¨ische Kommission, 2000. Entscheidung der Kommission vom 13.06.2000 zur Vereinbarkeit eines Zusammenschlusses mit dem Gemeinsamen Markt und mit dem EWR-Abkommen. Sache Nr. COMP/M.1673—VEBA/VIAG, Europa¨ische Kommission, Brus-sels.

FAZ, 1999. Jeder Zweite kann sich einen Wechsel des Stromanbieters vorstellen. Frankfurter Allgemeine Zeitung, 30 Oct. 1999, p. 13. Knieps, G., Brunekreeft, G. (Eds.), 2000. Zwischen Regulierung und

Wettbewerb: Netzsektoren in Deutschland. Physica Verlag, Heidel-berg.

Laffont, J.-J., Tirole, J., 1996. Global price caps and the regulation of interconnection, mimeo.

OFGEM, 1999a. Electricity and gas competition review. Research Study conducted for OFGEM by J. Henderson, R. Knight and C. Handford (MORI/11750).

Perner, J., Riechmann, C., 1998. Netzzugang oder Durchleitung? Zeit-schrift fu¨r Energiewirtschaft 22, 41–57.

Posner, R., 1976. Antitrust Law; An Economic Perspective. University of Chicago Press, Chicago.

Spengler, J.J., 1950. Vertical integration and antitrust policy. Journal of Political Economy 58, 347–352.

Stern, 1999. Trendprofil 09/99 Stromversorgung. Stern, Hamburg. VIK, 1999. VIK-Mitteilungen, Heft 4, Essen.

VDEW, 1999. Strommarkt Deutschland 1998. VDEW, Essen. Williamson, O.E., 1975. Markets and Hierarchies: Analysis and

Anti-trust Implications. Free Press, New York.

ZfK, 2000. Stadtwerke Jena: Konzentration aufs Netz. Zeitung fu¨r kommunale Wirtschaft, 1/2000, 8 Jan. 2000.

Further reading

Eurostat, various years. Electricity prices for EU industry. Eurostat, Luxembourg.

Eurostat, various years. Electricity prices for EU households. Euros-tat, Luxembourg.