INTRODUCTION

Kung (2001) contended that “democratic administra-tion” make up the result of bureaucracy and democracy reconciliation as of two become a force promises. While these two concepts (bureaucracy and democracy) before the two contradicts and difficulty’s to be adjusted (Albrow 1989, Bethan 1990, Blau and Meyer 2000) and when be

complused both of them give rise the conflict (Denhardt and Denhardt, 2006). This conflict can be detected in the ground instill forwith that Etzioni and Halevy (2011:144-147) propose a proposition: “Democracy as a dilemma bureaucratic” and bureaucracy as the dilemma of democ-racy”. Democracy proposition as dilemma bureaucratic can interpret in this research that on one side of the required bureaucracy to implement the principles of transparency, but on the other side of bureaucracy are also required to maintain or protect the public information that is exempt or classify.

Transparency and Accesibility will insistence on demo-cratic countries such as Indonesia have come to the enact-ment of Law No. 14 of 2008 on Public Information (here-inafter referred to as the Law No.14/2008 about public information disclosure). This law upholds the principle “every public information is accessible and can be

suscipteble by any user of public information, unless exempt public information is strict and limited. Each public infor-mation must be obtained each claimants quickly, timely, low cost, and simple way. Exempt public information

Budget

http://dx.doi.org/10.18196/jgp.2015.0011

ABSTRACT

This study aims to present a reconciliation model of bureaucratic principles (Secretion) and democracy (Transparency) through the mapping of public in-formation about managing a local government bud-get which is accessible to the public and which ones are excluded (secret) based on bureaucracy and public perceptions. This study uses a mixed method with sequential exploratory design and data collec-tion research procedures using surveys, depth inter-views, and documents. The validation data use source of triangulation techniques. The subjects of this study was divided into 2 (two) information as-sembling that is government bureaucracy and pub-lic Kupang determined by purposive. The results of this research showed that Kupang Goverment bu-reaucracy has 22 types of information perception (33,85%) in category information which is open and 42 types of information (64,62%) in category infor-mation that are closed while the public perceives 29 types of information (44,62%) in category informa-tion which is open and 26 types of informainforma-tion (40%) in the category of information that are closed. There-fore, to achieve the main of reconciliation to end of conflict between bureaucracy and public, later on the amount of information is open budget of man-agement that are 32 types of information (49,2%) and the amount of information that is enclosed which includes 33 types of information (50,8 %) of the 65 types of management budget information by Regu-lation No. 13 of 2006 on local Financial Manage-ment.

confidential to protect the consideration of greater interest”.

In Law No.14 / 2008 on the public information disclosure particularly in Article 9 (c) regarding the disclosure of financial statements mentioned that the real information of financial statements is one of four public information required (without being asked) was announced to the public on a regular basis. But ironically, based on the results of pre-study is conducted by the authors establish that the Kupang Government tend to conceal documents management of the local government budget from public. The evidence through interviews with the Head of Finance Secretariat of the Kupang city

(June 27, 2014) which explains that “ local

govern-ment budgets are confidential docugovern-ments that area, therefore not all areas of financial information may be published”. If you need information about the financial area must submit a written request addressed to the Mayor and / or the Regional Secretary. After the approval of our new mayor can serve”.

The existence reasons that require a direct recommendation letter from the Mayor for data and budget information is accessible to the public as the author indicated the presence of a strong cultural hierarchy in Kupang city government bureaucracy where most of the leaders work unit area waiting for disposition/command from the top-level bureaucratic leaders (mayor or local secretary) for control of the publicity budget management documents are in the leadership of the bureaucracy. Ironically, when the same letter submitted to the Mayor and the Secretary of the author only contains disposition area “consciously” till the data can not be given to the author.

The results of this reseacrh showed similarities

with Sayrani researchers, et al (2010) when doing

research Access Public Information Test on sectors in the scope of NTT Province by submitting a letter of public information, including information about local government budgets and local govern-ment budgets accountability report on each re-gional work unit. The appeal letter was not ad-dressed by the relevant regional work unit. This conditions mentioned above illustrates that at least the government was reluctant to be responsible and open to the public in the use of public

inaugu-rate. Thus are the results of Dwiyanto, et al (2003)

is still verified that “information about local government budget in many constituency and cities are dominated by the executive and legisla-tors. Society is very difficult and must follow the procedures that are difficult if want to obtain the data use of the local government both in regional house of representatives office and in the district office/town office”.

The principle conflict of democracy and bureau-cracy are represented by the values of transparency and secretion as upon description, need to find a solution. Otherwise both of them will be poten-tially conflict. One solution is a clear need to map out where the budget information that is classified as public information that must be periodically published by the bureaucracy and which are ex-empt information that does not need to be pub-lished. Local governments and the public need to know clearly demarcated indeterminately periodi-cal government has an obligation to publish on a regular basis and the public can obtain their rights, especially in terms of freedom of access to informa-tion and local government budgets.

public information about the local government budgets which are classified as accessible to the public and the public are excluded information (confidential) is a very important thing to remem-ber with the bureaucracy and democracy reconcilia-tion will bear “democratic state administrareconcilia-tion”. Administration of a democratic state is when there is a responsibility and sensitivity officials in under-standing and responding to the needs of the public and easily obtain information (Finer and Hyneman in Albrow, 1989: 111).

At least there are several reasons underlying the importance of the implementation in reconcilia-tion secrereconcilia-tion value (bureaucracy) and transparency

(democracy) in this study, namely: First, based on

the preliminary findings known that Kupang government does not have opennes governing law in the field of public information, but the new draft Draft Regulation Kupang Mayor Number (no) Year 2013 on Guidelines for the Management of Information and Documentation (PPID) in Kupang City Governments. However, when ana-lyzed in the Draft Regulation turns negative for the implementation process if it gets approved by the Mayor of Kupang. As for some of these weak-nesses is that there is doubt that is owned by the City of Kupang in classifying management of local government budget information which is open (transparent) and which is closed (secret). This can be seen in the preamble subsection of the

informa-tion that is open, especially at point c is “Information

on financial statements, such as realization of budget reports, reports of local income, financial accountability reports and others”. At the word “others” has the potential to multiple interpretations and

multipersepsi that ultimately may lead to disputes between the public and government information,

especially with regard to management of local goverment budget information. Potential occurs due to multiple interpretations and multiple-perception standards and policy objectives are vague, it will happen multiple interpretations and easily lead the conflict between the agent imple-mentations (Van Metter and Van Horn, 1975).

Second, at the national level, the laws in the field of public disclosure is not detail describing the types of information which the budget management that can be accessed by the public (transparent) and which are not accessible to the public (confiden-tial). The ambiguity in classifying this information will certainly lead to dispute the information on the level of policy implementation. More detail can be seen in the table below:

There are differences regarding the type of management of local government budget informa-tion/finance which is transparency between Com-mission Regulation information No. 01 Year 2010, Law No.14 / 2008 on the KIP, and Draft Regula-tion Mayor in 2013 and the lack of the amount of local governmnet budget management informa-tion/budget is categorized as a type of information that will be open when compared to the overall number of budget management information that are 65 kinds of information according to Regula-tion No. 13 Year 2006 on Regional Financial Management. Obviously this will cause multiper-ception and inconsistencies in the application of legislation in the field of public disclosure, particu-larly regarding information disclosure both at the level of local government budget management of the Central Government and Local Government.

bureaucratic principles (secretion/Esoteric/Secrets) and democracy (Transparency) through mapping public information about local government man-agement of the budget which are relatively inacces-sible by the public and the public are excluded information (confidential) based on bureaucracy and public perception.

THEORITICAL FRAMEWORK

1. SECRETION IN BUREAUCRACY

Bureaucracy at the beginning of its development as a closed organization. This is not surprising since the beginning of principles designed by Weber’s bureaucracy more emphasis on accountability aspects of hierarchy and professional manner so that the flow of information held only internal bureaucracy (for the bureaucrats themselves rather than to the public as the party being served). This was pointed out by Friedrich that “officials working in all areas of government services more esoteric (more confidential, only known and understood by certain people-red).” This happens because the bureaucracy works for the good of the publication understanding on their (professional) to what the public needs, not on what the public wants (Denhardt and Denhardt, 2007: 122-123).

Bureaucracy is exteremely concerned with the efficiency value, centralized, hierarchical (nondis-closure State), formality, and internal accountabil-ity/responsibility. Therefore, the bureaucracy has the esoteric or secret principle of confidentiality in each activity (Denhardt and Denhardt, 2006). Julia Black in Meijer (2012: 6) define secretion/confi-dentiality as an opacity to measure policy measures, where it is difficult to find who brought the deci-sion, who they are, and who benefits and who loses.

The principle secretion/clasified in bureaucracy stems from the emergence of the principle of

reporting proposed by Gulick and Urwick in his

Paper on the Science of Administration that

PODSCORB (Planning, Organizing, Directing, Staffing, Coordinating, Reporting and Budgeting) which known in the study of public administration as a paradigm of the principles of administration (1927-1937) (Thoha, 2008: 18-34). Reporting Principle is a form of internal accountability of bureaucrats to managerial superiors. The principle of reporting is understood as internal reporting hierarchy is why the bureaucracy is more likely to be closed and keep every activity of the external environment so that the appearance of secretion

or esoteric terms that evolved as a “state secrecy1”

in the study of modern public administration. Secretion occurs in the bureaucracy body as a result of the emphasis that is more focused on the aspects of accountability and reporting hierarchy (internal) in the body actually designed by Weber’s bureaucracy so that the bureaucracy is able to be a rational and effective organization in achieving this aims. This is visible from the principle of central-ized requires the flow of information, reporting and accountability internally among the profession-als (bureaucrats) in the hierarchy of the officiprofession-als who have the knowledge and competence level higher (internal) and not to the public as the party served and non-professional (Gerth and Mills, 1958 : 337). Hence, at this point, then the bureau-cracy had been born into a closed organization and esoteric.

2. TRANSPARENCY IN DEMOCRACY

popular then given meaning of democracy as “government of, by, and for people” (Sparingga and Kleden, 2006). Abraham Lincoln said that

government of people, by people, for people (Arfani, 1996: 181).

Democracy stands on the assumption that in a sovereign country is the people. Theoretically, democratic justification based on the theory of the social contract (social contract Du ou principes du droit politique) form a state organization for the

benefit of all the people (res publica) (Rousseau,

1712-1778). From a legal standpoint, the agreement embodied in the constitution as the supreme law of

the gain authority of constituent power, ie the people

themselves.

Transparency is basically promoted by demo-cratic principles. Because the essence of democracy calls for openness/transparency in the bureaucracy so that people can watch and participate in every activity of the bureaucracy so that in the end the principle of transparency developed into one of the principles or pillars of democracy for the realiza-tion of social control. Transparency and social control needed to improve the weakness of institu-tional mechanisms to ensure truth and justice.

Participation in Democracy understand John Dewey expressed in Varma (2007), in which he said a democratic society depends on the social consen-sus which is based on freedom, equality, and political participation. Participation is vital for policy choices, then at this point we can implicitly know that one of the prerequisites of effective realization of community participation are (1) ensuring the fulfillment of people’s basic rights to

information, (2) the existence of political will from

the government or bureaucracy to transparent for any activities that do, especially in terms of

finan-cial governance and local government.

In boundary with this, Dahl (1985: 9-10) in view of pluralist democracy added to ensure communi-ties get all their rights in a democratic state, then the state is obliged to give to the community to

have a civil liberties (civil liberties), both in terms of

the opinion, information, participate or supervise the government (bureaucracy) as a representation of the state. Therefore, in a democracy, the gov-ernment must fulfill and guarantee civil liberties (civil liberties), which is owned by the community through the formulation and enforcement of rules including mandatory government transparent and accountable for any activity to the public. Because actually it is the public who will bear the impact of any action taken by the bureaucracy through the formulation and implementation of policy.

Therefore, actually the government through the state bureaucracy as an agent aimed at the welfare of the people is required to be transparent to the public for any activity that is done through the mechanism of the provision of public information easily, quickly and cheaply. Without this, the citizens’ rights to information will not be achieved. In this way the real value of transparency is part of democracy. Without transparency, it is the goal of democracy can not be realized, namely the sover-eignty of the people.

3. RECONCILIATION DEMOCRACY (TRANSPAR-ENCY) AND BUREAUCRACY (SECRETION)

democracy. While on the other hand the develop-ment of democratic theory introduced direct democracy, representative democracy/representa-tive, elitist democracy, participatory democracy, (Varma,2007; Budiardjo, 2009), deliberative democracy (Hubermas in Hardiman, 2009). Theo-ries of democracy is the principle of popular partici-pation positioning - directly or indirectly - in the formulation of public policy. This means that the bureaucracy in a democracy are required to accept and apply the principles of democracy as well. The presence of democratic principles in the bureau-cracy is clearly contrary to the principles in the bureaucracy.

Therefore closed and mechanical characteristics making it difficult to accept the changes that occur in the surrounding environment makes Beniis (in Robbins, 1995) states “bureaucratic death” because of its own characteristics. However, we can not ignore the fact that the bureaucracy are every-where (Robbins 1995). Even Moloney (2007) explains that the bureaucracy today as yesterday, and remains the dominant form of government organizations in many countries. Bureaucracy is very concerned with the efficiency, centralized,

hierarchical (keeping the Secret State), formality, secretion/confidentiality and internal accountabil-ity/responsibility has a characteristic that is incom-patible with democracy very concerned with the value of participation, decentralization (spread of power), non-hierarchical, external accountability and transparency.

Hence then, Basic bureaucracy does not have transparency principle, but it has the opposite principle, namely: the principle of esoteric or secret (Dendhardt and Dendhardt, 2006). being that then Gerth and Mills (1958) states in order that bureaucracy can pose a threat to democracy Mod-ern caused by the existence of bureaucratic secrecy, namely the fact that most of the areas of bureau-cratic activity is closed to public observation.

Transparency is promoted by democratic ciples. While secretion (confidentiality) is a prin-ciple that was carried bureaucracy. Reconcile the values of democracy and bureaucracy potentially conflict. But it is a fact that is hard to avoid the bureaucracy in a democracy - like it or not, had to accept democratic values.

At the practical level, a reality in which the bureaucracy that always upholds the value of

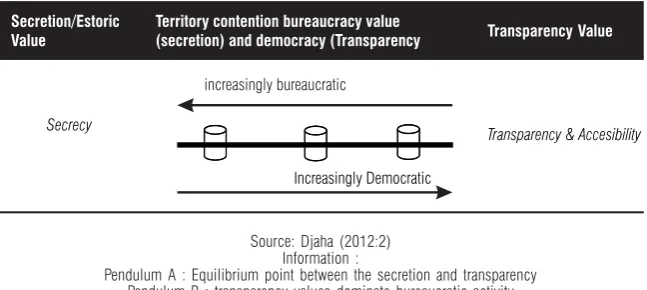

Source: Djaha (2012:2) Information :

Pendulum A : Equilibrium point between the secretion and transparency Pendulum B : transparency values dominate bureaucratic activity

Pendulum C : Value secretion activity dominates bureaucracy

secretion (confidentiality) in any activity or known by the term “State Secrets (secretion/esoteric)” specialized in the management of state and local finances Suffered a severe collision with the wishes of the public calls for “transparency” in the man-agement of state and local finances. Conflict of

democracy and transparency as bureaucracy-esoteric

and shift the pendulum on a line from the side of democracy to bureaucracy or otherwise as shown in the figure 1.

The conflict between bureaucracy and democ-racy originated begin from the theoretical debate about the accountability of the bureaucracy that occurred between Carl Friedrich and Herbert Finer in the year 1940-1941. In this context the Haryamoko Guy Peters (2011: 109) equate account-ability and transparency. Friedrich explained “the officials working in all areas of government ser-vices more esoteric (more confidential, only known and understood by certain people-red). The propo-sition put forward by Friderich (1940) is based on the argument that the key to responsibility respon-sible bureaucracy is professionalism. The adminis-trators are professionals and have special knowl-edge and technical skills that are not owned by citizens in general. Because of their responsibilities based on professional knowledge and norms of behavior, the administrator should be responsible to fellow professionals to meet the standards mutually agreed-standard (Denhardt and

Denhardt, 2007: 122-123). Thus Friedrich empha-sis focused on the flow of openness/transparency of information intended only internally (the professional bureaucrats).

On the other hand Finer (1941) argued other-wise by submitting the proposition that external control is the best and the only means to ensure

accountability. One of the requirements of exter-nal control implementation is the openness or transparency of information externally. Finer view that officials formulate policies and implement policies wishes/needs of the public, should notify the (transparent) or account for what it does to the public. Conflicts between Friedrich and Finer can be modeled in the following matrix form:

The clasically debate theory between Finer and Friedrich was the starting point conflict between the principle of confidentiality (esoteric) with the principle of transparency in the bureaucracy. The principle of confidentiality is represented as bu-reaucratic characteristics that tend to be closed, and the principle of transparency is represented as a characteristic of democracy are always demanding transparency of bureaucracy.

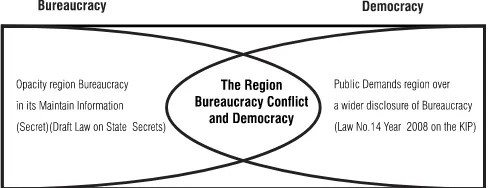

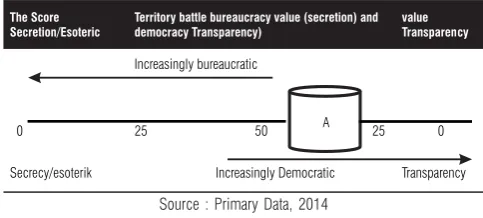

But the pressure on the transparency level of bureaucracy should have boundaries that can be clearly identified so that the public and the bureau-cracy know and realize it either. Otherwise both will potentially conflict, in which the bureaucracy will try to expand their secretions, while trying to sue public bureaucracy to be more open (transpar-ent). The conflict between the bureaucracy and the public can be modeled in Figure 3 below:

FIGURE 3. CONFLICT VALUE BUREAUCRACY (SECRETION) AND DEMOCRATIC VALUES (TRANSPARENCY)

which is to find a point or points peaceful reconcili-ation between the two. Peaceful point in question is the point where the two are receiving and not cause further friction resulting in inconvenience in governance. This is important, given the clash between these two values actually had a negative

effect or a positive effect both for the bureaucracy and the democratic system adopted a country.

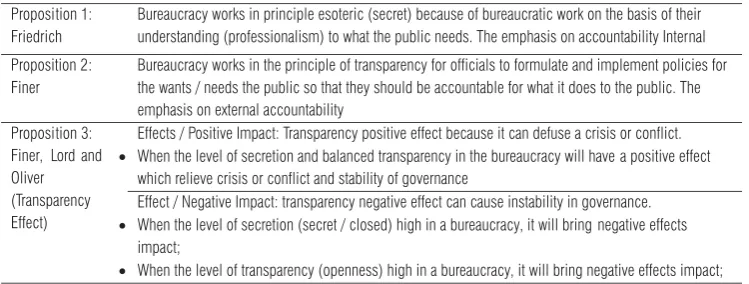

Alongside esteem to public pressure and stake-holders who tend do not recognize boundaries or excessive been pushed Finel and Lord (1999) argued about the positive and negative effects of

Source : This model is a combined visualization of the opinion Friedrich (1940), Finer (1941), Finel and Lord (1999), Oliver (2004).

Information :

Pendulum A: Equilibrium point between the bureaucracy and democracy. Pendulum B : Democratic values dominate bureaucratic activity. Pendulum C : Value is dominated bureaucracy bureaucratic activity.

PROPOSITION

transparency. Transparency positive effect because it can defuse a crisis or conflict, while the negative effects of transparency which is causing instability in governance. Positive or negative effect, of course, with regard to what is proposed by Oliver (2004), namely the increasingly fierce debate about which information should be published and which information should not be published. The debate is expected to produce a draw point where the negative effects can be minimized.

Model unify the bureaucracy (secretion) and democracy (Transparency), particularly on the issue of budget management of public disclosure is directed to a mapping model of the information through the study of the perception of the area which include confidential information and open based on the perception of the bureaucrats/ administrators and the public (NGOs, mass media, academics, community) and the reasons that follow. Mapping information is based on a percep-tion of things that are truly important to be imple-mented. Given today, of any information you want to access the public budget, the bureaucracy is only able to meet most of the information. And even not infrequently bureaucracy unable to fulfill the request. One reason is the difference in perception between the bureaucracy and the public for which information is classified as secret and classified information which may be published as well as open and accessible to anyone at any time. For more details, you will be creating a model of reconciliation bureaucracy (secretion) and democ-racy (transparency) in this article are as follows (see Table).

Thus the mapping of the classified information confidential and open in order to achieve reconcili-ation point bureaucracy and democracy is one of

the important aspects that need to be done which can bring positive effects to the bureaucracy in a democracy. With the reconciliation of bureaucratic and democratic values, the bureaucracy as a public institution can implement its obligation to publish information and budget documents to the public through public information disclosure mechanism but still be able to maintain the confidentiality of the area where the budget documents are not able to test the consequences of the information pub-lished by the public.

RESEARCH METHOD

The method used in this study is a mixed meth-ods design with sequential exploratory study is to collect and analyze the qualitative data through interviews then collect and analyze quantitative data is through surveys (Creswell, 2013). In this study, quantitative data is is used to explain the qualitative data. The approach in this study using a deductive approach, the Instrumental case study is a case study is used to examine a particular case that presented a perspective on an issue or theory (Miles and Huberman, 2009).

This research regarding the case of bureaucratic transparency in the management of government budget Kupang by focusing on public information about the budget that must be published and is excluded. All the focus of the research that has been described above will be used to locate the point of reconciliation bureaucracy and democracy are represented by the values of transparency and secretion, particularly with regard to budget man-agement information which is required to be published to the public and which are confidential (exempt/secretion).

survey the opinions of the informants regarding the type of budget management information which is open (publicly accessible) and which is closed (not accessible to the public) through a questionnaire instrument, then continue with interviews to determine reasons, The reason underlying the informants bureaucracy Kupang City Government and Institutions Examiner choose the type of such as information.

Informants in this study were divided into 2 (two) clusters, namely (1) informants from govern-ment bureaucrats Kupang City consists of the Regional Secretary, Assistant I, II Assistant, Assis-tant III, Chief Regional Work Unit, Regional Work Unit Secretary, Treasurer and Head of Sub-division Regional Work Unit Expenditure Finance Regional Work Unit as Financial Officials at the Department of Revenue Administration, Depart-ment of Health, Education, Youth and Sports, the Office of Communications and Information Technology, Department of Mines and Energy, the Department of Transportation, Department of Population and Civil Registration, Planning and Regional Development Agency, Research and Development Agency and the Secretariat of Kupang City Council. (2) The informant from the public comes from the NGO Workshop APPeK NTT, academics (lecturers and students), Mass Media East Express and the Ombudsman Repre-sentative NTT. Informants determination tech-nique is determined purposely selected with consid-eration and specific purposes. Intended destination was the informant who has authority with regard to the budget document in terms of accountability, transparency and accessibility. Another informant is public (stakeholders) with an interest in account-ability, transparency and accessibility of the budget.

Means of data collection in this study using survey techniques, documentation and interviews with open-ended nature of the interview. Interview techniques used are in-depth interview. Analysis using qualitative data through the process of finding and systematically collate all the data obtained from the field based on the results of interviews, field notes and study documents. All data collected through the document, archive footage and interviews were analyzed through three stages: (1) reduction data, (2) the presenta-tion of the data, and (3) the stage of decision-making and verification of data.

RESULTS AND ANALYSIS

This section will explain about the mapping of the budget management information according to the perception of Government Bureaucracy public about Kupang and local government budget management information types which are rela-tively open (transparent) and which are classified as closed (secret). Map of transparency and secretion of local government budget management informa-tion based on four (4) secinforma-tions stages budget man-agement which is a cycle of financial manman-agement according to Minister Regulation No. 13 Year 2006 on local Financial Management Guidelines. The fourth part of the area of financial management cycle, namely: 1) The process of budget prepara-tion; 2) Implementation and Administration Shopping; 3) Accounting and Reporting; 4) Changes in the local gorvernment budget.

1. AGAINST BUREAUCRACY PERCEPTIONS OF INFORMATION AND DOCUMENT OF LOCAL GOVERNMENT MANAGEMENT BUDGETS

Government Bureaucracy Kupang perceive 22 types of information, or by 33.85% in the category of information which is open means accessible to the public and 42 types of information, or by 64.62% included in the categories of information that are closed means not accessible to the public as well as the first type of information that fall within the type of information that is less open means that the type of information that can be accessed by the public after the approval or recommenda-tion of Regional Work Unit leaders but not be published. More detail can be seen in Table 3 below:

From the aloft description, it still appears that the government bureaucracy in Kupang still tend to be closed and keep all the activities of the management of revenue and expenditure budget of hers from public scrutiny. Then surely we can know that the bureaucracy is still very dominating bureaucratic activity compared with democratic values. For more details perception Kupang city government bureaucracy will be visualized in the image below 4:16 this:

Sumber : Data Primer, 2014

FIGURE 4.16. MAP TRANSPARENCY AND SECRETION 65 TYPES OF INFORMATION MANAGEMENT BUDGETS BASED ON PERCEPTION KUPANG

CITY GOVERNMENT BUREAUCRACY

The perception held by the informant Kupang City Government bureaucracy that not all docu-ments Budget management area is accessible to the

public is motivated by five (5) basic reasons that led to the budget documents sealed from the public , namely: First, document management and Expen-diture Budget the domestic affairs sector depart-ments so that enough is known internally only, or in other words a confidential state documents, as well as civil servants oath to protect and safeguard state secrets; Second, because the document man-agement of the Regional Budget is a confidential document states that the document can only be given if there is a recommendation or disposition of the head region or area secretary; Third, the existence of policies that financing is not in the budget heading contained in the Supreme Advi-sory Council, the regional work units so that the funds taken from other budget items and of course this has resulted in liability for proof of expendi-ture of these funds is just a flower wreaths formal-ity like purchase, service members of the Regional Representatives Council, August 17 celebration, birthday celebration, agencies and so on; Fourth, the financial administration system culture that developed long ago in the bureaucracy shows that the document management and Expenditure Budget can be known only internal bureaucracy includes Head of the regional work, the Secretary of the SKPD, Head of Finance and Treasurer subpart and audit institutions; Fifth , lack of clarity in the budget information classification legal instruments in the field of public information disclosure both at the national level as well as at the regional level.

can be opened to the public as the result of inter-views with the Head of Finance Secretariat of the city of Kupang (June, 27th 2014), Assistant I (inter-view, June 27th 2014), Assistant II (inter(inter-view, June, 26th 2014), Assistant III (interview, June 24, 2014), the Secretary of the Regional Representatives Council (interview, May 19, 2014), Acting Secretary Bappeda Kupang (interview, July 11th 2014), Head of the Department of Revenue (interview, July, 11th 2014), Head of Communications and Infor-mation Technology (interview, May, 20th 2014), Head of the Department of Mines and Energy (interview, May 13th 2014), Chief Department of Health (interview, May, 21th 2014), and Head of Research and Development Kupang (interview, May, 22th 2014).

Statement submitted by the Secretary of the Region, Assistant I, II, and III Regional Secretary of the city of Kupang, the Head of the local work and Head of Finance Ironically, Reviews These are the main actors Officials bureaucracy have access and authority over the use of budgets in the bu-reaucracy. Indeed this does not surprise because it will cause the bureaucracy Kupang tend to work in secrecy space dim. The views are not much differ-ent also addressed by several heads of regional work units were found budget transparency is understood as the management of information disclosure Budget and Expenditure that can be monitored by the public, but the degree of trans-parency of document management and Expendi-ture Budget is merely a summary/overview general and not detailed . Understanding like this shows the fear and reluctance of the bureaucracy to publish the information contained in the docu-ment managedocu-ment of the Regional Budget as a whole, complete and detailed due if the documents

and the information is misused by the parties that publish public will bear the risk of publicity action does (possible careers and positions are at stake).

Thus through the mapping of the above it can be seen why during this bureaucracy Kupang City Government has not been willing or difficult to open / transparent on information management and Expenditure Budget hers to the public because most of Kupang city government bureaucracy still perceive the information management of the Regional Budget classified in the information that is covered in the amount of 64.62% or amounted to 42 information management and estimation budget Revenue and Expenditure according to Regulation No. 13 Year 2006 on Regional Finan-cial Management as Document RKA (budget plan), DPA (Budget Implementation Document) , and LRA (Budget Realization Report).

2. PUBLIC PERCEPTION TO INFORMATION AND DOCUMENT MANAGEMENT REVENUE AND EXPENDITURE BUDGET

The results showed that of the 65 types of information management and Expenditure Bud-get, the public perceives the 29 types of informa-tion, or by 44.62% in the category of information which is open means accessible to the public and 26 types of information, or by 40% in the category information that is closed means not accessible to the public as well as 10 types of information, or by 15.38% were categorized in the types of informa-tion that are less open means that the type of information that can be accessed by the public after the approval or recommendation of the leadership of the regional work units but shall not be publicity.

more open, where it is visible from a public percep-tion that wants all types of document management of the local budget can be accessed by the public and not complicated. Then surely at this point, the public seeks to democratic values can be institution-alized in Kupang city government bureaucracy that can be more open access to information manage-ment The annual budget to the public. For more details, the perception of the government bureau-cracy would be Kupang 4:20 visualized in the image below:

Source : Primary Data, 2014

FIGURE 4.16. MAP TRANSPARENCY AND SECRETION 65 TYPES OF INFORMATION BUDGET AND EXPENDITURE BASED ON KUPANG CITY

GOVERNMENT BUREAUCRACY PERCEPTION

The perception held by the public that some document management and Expenditure Budget shall be open to the public such as the Work Plan and Budget Unit of Local/Regional Financial Management Officer, Supreme Advisory Council Unit of Local/Regional Financial Management Officer, and report on the realization Budget Work Unit Area/Regional Finance Officer business backed by 4 (four) basic reasons that led to the budget documents sealed from the public, namely: First, the document management estimation Revenue and Expenditure as Local regulations Regional Budget, Work Plan and Budget Unit Regional Work/Acting Manager Regional Finance and the Supreme Advisory Council Unit of Work Areas/Regional Finance Officer business includes

budgetary policies bureaucracy, so worth a large public. Second, document management and Expenditure Budget as budget realization report regional work units and Regional Financial Man-agement Officer shall be published so that the public can know the extent of the government's performance in the management of the Regional Budget and participate in supervising the use and management of the budget so as to minimize the misuse of funds by certain elements. Third, docu-ment managedocu-ment and Expenditure Budget at different stages of the Regional Budget as the plan of local estimation Revenue and Expenditure, local government draft budget-Government Regional, and Local regulations Regional Budget and Budget and Local regulations Regional Shopping-Govern-ment is a public docuShopping-Govern-ment because the formulation has passed Musrenbang mechanism followed by the community and afterwards discussed in the House of Representatives that the mechanism built Regions indicate that the budget document is a public document. Fourth, document management and Expenditure Budget as the Work Plan and Budget audited local government is open because it is a financial document which has been audited and accounted for in the House of Representatives to be published.

Management Officer, Supreme Advisory Council Unit of the local work/Commitment Officer, reports the Regional Finance Officer budget realization of business and government areas of financial statements that have been audited belong to the type of information that is open. This is a positive signal that the public wants access to information management and Expenditure Budget

can be opened by the bureaucracy so that the public can also Contribute to monitor and super-vise the performance of the bureaucracy in manag-ing Budget notabene area is public money Because It comes from taxes and levies the area.

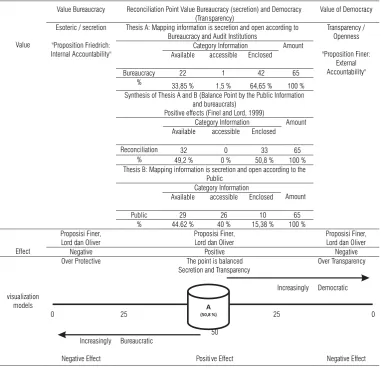

3. RECONCILIATION BUREAUCRACY (SECRE-TION) AND DEMOCRACY (TRANSPARENCY)

Source: Primary Data, 2014

Infromation:

"Open: Type of Information Management of the budget that must be publicized through the media, electronic media, TV, radio, online media or website on a regular basis and can be accessed by the public (community, NGOs, academics, and so

on)

"Closed: Type of Information Management of the budget that can not be publicized through the media / electronic and online media and is not accessible to the public (citizens, NGOs, academics, and so on)

This section presented a point of reconciliation/ balance (mapping) between the principles of

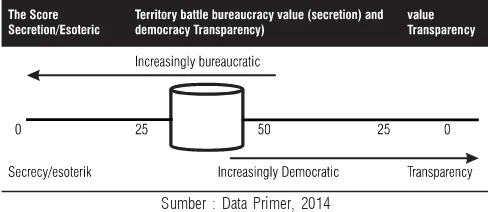

transparency and secretion 65 Type of Information Management of the budget, as described in the section above. Mapping point is really important reconciliation to resolve conflict of values between the values of democracy (transparency) and the value of the bureaucracy (secretion) which can have negative effects as well as positive effects for both the bureaucracy and the democratic system adopted a country as proposed by Finer and Lord (1999). For more details, the authors present the reconciliation table maps secretion transparency and budget management information on the 4 (four) stages of budget management below.

(see Figure 4.16).

Therefore, based on the table 4.46Peta Recon-ciliation Transparency and Secretion 65 Type of Information Management Revenue and Expendi-ture Budget above it can be seen that to reach the point of reconciliation or peace points to end the conflict between the bureaucracy and the public, then the amount of information management and Expenditure Budget nature open that are 32 types of information, or by 49.2% and the amount of information that is enclosed which includes 33 types of information, or 50.8% of the 65 types of information management and Expenditure Budget by Regulation No. 13 of 2006 on Regional Finan-cial Management. This reconciliation point is the point where the bureaucracy and the public are able to accept and not to cause further friction with the result that can bring a positive effect because it can defuse a crisis or conflict as proposed by Finel and Lord (1999). For more details, point reconciliation transparency and secretion of 65 kinds of information management and

Expendi-ture Budget will be the author visualized at 4:30 in the image below.

(see Figure 4.30).

Therefore, based on the framework to unify the bureaucracy (esoteric) and democracy (transpar-ency) information management of the local gov-ernment budget above can know that point recon-ciliation/balance transparency (democratic values) and secretion (value bureaucracy) information management of the local government budget as a point where mutual acceptance and not cause further friction resulting in inconvenience in governance can only be achieved if the type of information the local government budget manage-ment that are open are 32 or 49.2%, and the type of information management of the local govern-ment budget that are closed are 33 types informa-tion management of the local government budget, or 50.8%, consisting of: 1) All kinds of information management of the budget at this stage of the process of drafting the local government budget is open; 2) All kinds of information management at the local government budget implementation phases and administration expenditures are cov-ered except the Supreme Advisory Council, the regional work units and the Supreme Advisory Council Regional Financial Management Officer; 3) All kinds of information management at the local government budget accounting and reporting stages are open except Letter Expenditure Account-ability Unit of Local and Regional Government Financial Statements Discussion Document; 4) All Types of Information Management of gross domes-tic product in the stages of change in the local government budget is open.

indi-cated by Finel and Lord (1999) is 1) The public's right to information management of the local government budget can remain assured; 2) People can also supervise and participate by providing feedback, suggestions and criticisms on the activity of the local government budget management through the use of information management of the local government budget that is published periodically by the government through mass media and online media; 3) With several publish this type of information management of the local government budget as RKA SKPD / PPKD, DPA SKPD / PPKD, LRA SKPDs / PPKD and LKPD which has been audited by the degree of transpar-ency is quite open, then the government will be able to implement the mandate of Law Number 14 Year 2008 on Public Information Transparency and peoples' rights to information management of the local government budget while doing the control or supervision over the management of information the local government budget to be accessed by the public in order to prevent misuse of such information so that it can interfere with the performance and cause instability of governance on SKPD/District/Municipal Government con-cerned.

CONCLUSION

The occurrence of a conflict between the bureaucracy and the public with respect to the type of budget management information has sparked conflict and tension. On one side of the bureau-cracy tend to be closed for any activity, in particular regarding the budget management activities with the main jargon "state secrets" while demanding public bureaucracy tends to be more open / trans-parent governance on each activity budget. This is

evident from the fact that the Government Bu-reaucracy Kupang perceive 22 types of information (33.85%) fall into the category of information which is open and 42 types of information

(64.62%) fall into the category of information that are closed while the public perceives the 29 species information (44.62%) fall into the category of information which is open and 26 types of infor-mation (40%) fall into the category of inforinfor-mation that are closed.

Therefore, to reach the point of reconciliation to end the conflict between the bureaucracy and the public, then the amount of information that is open budget management that are 32 types of information (49.2%) and the amount of informa-tion that is enclosed which includes 33 types of information (50.8 %) of the 65 types of informa-tion management budget by Regulainforma-tion No. 13 of 2006 on Regional Financial Management.

as said by Ralph Nader in Moller (1998) that information is the currency of democracy (Informa-tion is the currency of democracy) is that democ-racy can not work if there is no open information flow as the economy can not run if there is no the money).

ENDNOTES

1 See Article 1, paragraph 1 and 2 of Draft Act on

State Secrets, in which the State Secrets defined as information, material, and / or activity are formally defined and needs to be kept secret to be protected through confidentiality mecha-nism, which, if known to unauthorized parties can membahyakan sovereignty, integrity, safety of the Republic of Indonesia and / or may result in the undermining of state administration, national resources, and / or public order, which is regulated by or under this Act.

2 The reason is obtained based on the results of

in-depth interviews were conducted to study informants include (1) the Regional Secretary, Assistant I, II Assistant, Assistant III, Chief Financial Officer at the Regional Secretariat of Kupang, (2) Head of the regional work, the Secretary of Work Unit area, Treasurer Expen-diture regional work units and Finance

Kasubbag regional work units in Department of Revenue, Department of Health, Education, Youth and Sports, the Office of Communica-tions and Information Technology, Department of Transportation, Department of Population and Civil Registration, Planning and Regional Development Agency, Research and Develop-ment Agency and the Secretariat of the Re-gional Representatives Council Kupang.

3 This statement is a conclusion made by the

authors based on the results of in-depth inter-views with informants research is the Regional Secretary, Head of Finance, Assistant I, II Assistant Regional Secretary of Kupang, the Secretary of Parliament, Acting Secretary of Bappeda Kupang, the Secretary of the Depart-ment of PPO, Head of the DepartDepart-ment of Revenue, Chief Department of Revenue De-partment, Head of Communications and Information Technology, Head of Department of Transportation, Head of the Department of Population and Civil Registration, and Head of Research and Development of Kupang.

4 The reason is obtained based on the results of

in-depth interviews were conducted to study informants include (1) the Regional Secretary, Assistant I, II Assistant, Assistant III, Chief Financial Officer at the Regional Secretariat of Kupang, (2) Head SKPD, SKPD Secretary, Treasurer and Expenditure SKPDs Financial Kasubbag SKPDs the Department of Revenue, Department of Health, Education, Youth and Sports, the Office of Communications and Information Technology, Department of Trans-portation, Department of Population and Civil Registration, Planning and Regional Develop-ment Agency, Agency for Research and Devel-opment and the Parliament Secretariat Kupang.

REFERENCE

Adang Djaha, Ajis Salim, 2012. Transparansi Birokrasi, Jurnal Administrasi Publik Volume 11 No. 1 Oktober 2012, ISSN 1412-825X, Kupang. Albrow, Martin. 1989. Birokrasi, Tiara Wacana,

Yogyakarta.

Jakarta.

Bethan, David, 1990. Birokrasi, Bumi Aksara, Jakarta.

Blau, Peter M dan Marshall W. Meyer, 2000. Birokrasi Dalam Masyarakat Modern, Penerbit Prestasi Pustakaraya, Jakarta.

Budiardjo, Miriam, 2009. Dasar-Dasar Ilmu Politik, Edisi Revisi, Gramedia Pustaka Utama, Jakarta. Creswell, John. 2012. Research Design :

Pendekatan Kualitatif, Kuantitatif dan Mixed. Yogyakarta: Pustaka Belajar.

Dahl, A. Robert. 1985. Dilema Demokrasi Pluralis: Antara Otonomi dan Kontrol. CV. Rajawali, Jakarta.

Denhardt, Robert, B. and Janet, V. Denhardt. 2006. Public Administration:An Action Over-view, Firsth Edition. United States of America: Thomson Wadsworth.

________. 2007. The New Public Service - Serving, Not Steering, Expanded Edition.M.F. New York, London, England: Sharpe, Armonk.

Dwiyanto, Agus, et al. 2003. Governance Decen-tralized Survey 2002 dalamReformasi Tata Pemerintahan dan Otonomi Daerah. Pusat Studi Kependudukan dan Kebijakan Universitas Gajah Mada. Yogyakarta.

Etzioni, Eva dan Halevy, 2011. Demokrasi dan Birokrasi Sebuah Dilema Politik, Total Media, Yogyakarta.

Finel, Bernard I and Lord, Kristin M. 1999. The Surprising Logic Of Transparency Author: Reviewed Work. Source: International Study, Vol.43, No. 2 (Jun. 1999), pp.315-339 Published by : Blackwell Publising on behalf of The Inter-national Studies Association Stable URL: http:/ /www.jstor.org/stable/2600758. Accessed: 23/ 03/2012 09:58.

Finer, Herman. 1941. Administrative Responsibil-ity in Democratic Government. Public Adminis-tration Review, Vol.1.

Friedrich, Carl J. 1940. Public policy and the

nature of administrative responsibility. In Carl J. Friedrich (ed). Public Policy. Cambridge:

Harvard University Press.

Gerth, H.H, dan Mills, C.W. 1958.From Max Weber: Essay in Sociology. New York: Oxford University Press.

Hadirman, Budi. 2009. Demokrasi Deliberatif-Menimbang Negara Hukum dan Ruang Publik dalam Teori Diskursus Jurgen Hubermas. Yogyakarta: Penerbit Kanisius.

Haryatmoko. 2011. Etika Publik untuk Integritas Pejabat Publik dan Politisi. PT. Gramedia Pustaka Utama. Jakarta.

Miles Mattew, B dan Huberman, A. Michael. 2009. Analisis Data Kualitatif : Buku Sumber tentang Metode-Metode Baru, Penerjemah Tjetjep Rohendi Rohidi, Penerbit Universitas Indonesia - UI Press, Jakarta.

Moloney, Kim. 2007. Comparative Bureaucracy: Today as Yesterday- Book Reviuews, Public Administrative Review; Nov/Des.2007; 67,6; ABI/INFORM GlobaL.

Kung, Edwin W. 2001. Disertation : Transit Strat-egy: A Study of Bureaucracy- Democratic Recon-ciliation, Golden Gate University.

Mangabeira, Roberto Unger. 1976. Law In Mod-ern Society: Toward a Criticism of Social Theory. New York. The Free Press.

The Policy Implementation Process: A Concep-tual Framework dalam Administration and Society 6. London: Sage.

Moller, Gary M. 1998. Toward a Reconciliation of the Bureaucratic and Democratic Ethos, Pub-lished by: SAGE, http://

www.sagepublications.com.

Oliver, Richard, W. 2004. What is Transparency. United States of America: The McGraw-Hill Companies, Inc.

Peraturan Komisi Informasi Pusat Nomor 01 Tahun 2010 tentang Standar Layanan Informasi Publik.

Peraturan Menteri Dalam Negeri Nomor 13 Tahun 2006 Tentang Pedoman Pengelolaan Keuangan Daerah.

Robbins, Stephen, P. 1995. Teori Organisasi: Struktur, Desain, dan Aplikasi, Edisi 3, Penerbit Arcan, Jakarta.

Sparingga, Daniel dan Ignas Kleden, 2006. Konsepsi Demokrasi, Seri Modul Simpul Demokrasi, Komunitas Indonesia untuk Demokrasi, Modul 005. Cetakan Perdana, diterbitkan oleh Komunitas Indonesia untuk Demokrasi, Jakarta.

Sayrani Lorens, et al. 2010. Uji Akses Keterbukaan Informasi Publik Berdasarkan UU No. 14 Tahun 2008 Tentang Keterbukaan Informasi Publik, Bengkel APPek, Kupang.

Thoha, Miftah. 2008. Ilmu Administrasi Publik kontemporer. Kencana Prenada Media Group. Jakarta.

Undang-Undang Nomor 14 Tahun 2008 tentang Keterbukaan Informasi Publik.