i

Statistik Asuransi Gempa

Bumi Indonesia 2010

Indonesian Earthquake Insurance Statistic 2010]

Sesuai dengan tujuan pendiriannya, MAIPARK

selalu berusaha melakukan inovasi dalam

memberikan pelayanan terbaik bagi industri

asuransi Indonesia dalam hal ilmu dan statistik

mengenai risiko bencana.

Inovasi

terus

kami

lakukan

untuk

menyempurnakan laporan statistik ini, sehingga

menjadi lebih akurat, rinci dan komperhensif.

Berikut kami sajikan laporan Statistik Asuransi

Gempa Bumi Indonesia 2009 – 2010 yang

mencakup :

o

Inovasi terhadap sistem dan proses

pengolahan data statistik.

o

Peta Kejadian Gempa Bumi Indonesia.

o

Peta

Exposure

Gempa Bumi Indonesia.

o

Penggolongan tersendiri atas risiko multi

lokasi, dalam laporan profile risiko dan

klaim.

o

Analisa asuransi gempa terkait kondisi

makro ekonomi.

o

Analisa seismitas terkini.

o

Laporan dengan dua bahasa (Bahasa

Indonesia – Bahasa Inggris).

o

Panel navigasi yang akan memudahkan

dalam menelusuri laporan statistik ini.

o

Tabel, peta dan grafik yang kreatif.

Dengan semangat ”Go Green”, dan laporan

tersebut disajikan dalam bentuk soft copy dan

tidak lagi diproduksi dalam bentuk hard copy.

Usaha

yang

kami

lakukan

dalam

menyempurnakan laporan statistik ini tidak akan

berarti apa - apa tanpa dukungan dari seluruh

perusahaan asuransi. Data yang lengkap dan

akurat akan sangat menentukan kualitas dari

hasil statistik ini.

In line with the intention of MAIPARK

establishment, MAIPARK keeps on innovating to

provide the best services for the Indonesia’s

insurance industry in terms of science and

statistics on Catastrophe risks. We keep on doing

innovation to make this statistics report more

accurate, detailed and comprehensive. Herewith,

we present Indonesian Earthquake Statistical

Report of 2009 - 2010 which include:

o

Inovation of the system and statistical

data processing.

o

Map

of

Indonesian

Earthquake

Occurence.

o

Map

of

Indonesian

Earthquake

Exposure.

o

Separate classification of multi-location

risks in Risk and Loss Profile report.

o

Analysis of earthquake insurance related

to macro economic conditions.

o

Current Seismic Analysis.

o

Bilingual reports (Indonesian - English).

o

Navigation Panel to ease to trace the

statistical report.

o

Creative tables, maps and graphs.

With the spirit of "Go Green” the report is

presented in soft copy rather than hard copy.

Our efforts to continously improve this statistic

report are nothing without all insurance

companies’ support. Complete and accurate data

will greatly determine the quality of these

statistical results.

Kata Pengantar

Foreword

Kami berharap laporan statistik ini dapat

memberikan manfaat tidak hanya bagi

perusahaan asuransi yang menangani asuransi

gempa bumi, namun juga berguna bagi industri

Asuransi Umum di Indonesia.

We hope that this statistic report is useful for both

insurance companies having earthquake

business and general insurance industry in

Indonesia.

Salam Inovasi MAIPARK !!

Frans Sahusilawane

President Director

Daftar Isi / Contents

Kata Pengantar ... i

Daftar Isi ... iii

Informasi Statistik... vi

Ikhtisar Asuransi Gempa Bumi Indonesia

2010...

A.Pendahuluan ... 1

B.Struktur Pasar ... 1

C.Pertumbuhan Premi Bruto ... 2

D.Jumlah Risiko ... 6

E.Kontribusi Asuransi Gempa Bumi Indonesia

... 7

F.Pertumbuhan

Incurred Claim

... 15

Exposure Asuransi Gempa Bumi Indonesia

...

Tabel 2.1.Exposure Per Cresta Zone ... 21

Tabel 2.2.Exposure Per Okupasi ... 23

Tabel 2.3.Exposure Per Interest ... 25

Tabel 2.4.Exposure Per Provinsi ... 27

Gross Premium Asuransi Gempa Bumi

Indonesia

...

Tabel 3.1.Gross Premium Per Cresta Zone . 28

Tabel 3.2.Gross Premium Per Okupasi ... 30

Tabel 3.3.Gross Premium Per Provinsi ... 32

Jumlah Risiko Asuransi Gempa Bumi

Indonesia

...

Tabel 4.1.Jumlah Risiko Per Cresta Zone ... 33

Tabel 4.2.Jumlah Risiko Per Okupasi ... 35

Klaim Asuransi Gempa Bumi Indonesia

...

Tabel 5.1.1.Klaim Frekwensi Per Okupasi .... 37

Tabel 5.1.2.Klaim Frekwensi Per Cresta Zone

... 39

Tabel 5.2.1.Jumlah Klaim Per Okupasi ... 41

Tabel 5.2.2.Jumlah Klaim Per Cresta Zone .. 43

Foreword ... i

Table of Contents ... iii

Statistical Information ... iv

Summary of Indonesia Earthquake

Insurance 2010

...

A.Introduction ... 1

B.Market Structure ... 1

C.Growth of Gross Premium ... 2

D.Number of Risks ... 6

E.Earthquake Insurance Contribution

... 7

F.Growth of Incurred Claim ... 15

Indonesia Earthquake Insurance Exposure

....

Table 2.1.Exposure By Cresta Zone ... 21

Table 2.2.Exposure By Occupation ... 23

Table 2.3.Exposure By Interest ... 25

Table 2.4.Exposure By Province ... 27

Indonesia Earthquake Insurance Gross

Premium

...

Table 3.1.Gross Premium By Cresta Zone .. 28

Table 3.2.Gross Premium By Occupation .... 30

Table 3.3.Gross Premium By Province ... 32

Indonesia Earthquake Insurance Number of

Risks

...

Table 4.1.Number of Risk By Cresta Zone .. 33

Table 4.2.Number of Risk By Occupation... 35

Indonesia Earthquake Insurance Claim

...

Table 5.1.1.Claim Frequency By Occupation 37

Table 5.1.2. Claim Frequency By Cresta Zone

... 39

Table 5.2.1.Claim Amount By Occupation .... 41

Profil Risiko dan Klaim

...

Tabel 6.1.Semua Tahun Underwriting, Semua

Okupasi, Semua Cresta Zone ... 45

Tabel 6.2. Tahun Underwriting 2010, Semua

Okupasi, Semua Cresta Zone ... 46

Tabel 6.3. Tahun Underwriting 2009, Semua

Okupasi, Semua Cresta Zone ... 47

Tabel 6.4. Tahun Underwriting 2008, Semua

Okupasi, Semua Cresta Zone ... 48

Tabel 6.5. Tahun Underwriting 2007, Semua

Okupasi, Semua Cresta Zone ... 49

Tabel 6.6. Tahun Underwriting 2006, Semua

Okupasi, Semua Cresta Zone ... 50

Profil Risiko dan Klaim Tahun Underwriting

2010

...

Okupasi Agricultural ... 51

Okupasi Commercial ... 52

Okupasi Industrial ... 53

Okupasi Residential ... 54

Profil Risiko dan Klaim Tahun Underwriting

2009

...

Okupasi Agricultural ... 55

Okupasi Commercial ... 56

Okupasi Industrial ... 57

Okupasi Residential ... 58

Profil Risiko dan Klaim Tahun Underwriting

2008

...

Okupasi Agricultural ... 59

Okupasi Commercial ... 60

Okupasi Industrial ... 61

Okupasi Residential ... 62

Profil Risiko dan Klaim Tahun Underwriting

2007

...

Okupasi Agricultural ... 63

Okupasi Commercial ... 64

Risk and Loss Profile

...

Table 6.1.All Underwriting Year, All

Occupation, All Cresta Zone... 4

5

Table 6.2. Underwriting Year 2010, All

Occupation, All Cresta Zone... 46

Table 6.3. Underwriting Year 2009, All

Occupation, All Cresta Zone... 47

Table 6.4. Underwriting Year 2008, All

Occupation, All Cresta Zone... 48

Table 6.5. Underwriting Year 2007, All

Occupation, All Cresta Zone... 49

Table 6.5. Underwriting Year 2006, All

Occupation, All Cresta Zone... 50

Risks and Loss Profile Underwriting Year

2010

...

Agricultural Occupation ... 51

Commercial Occupation ... 52

Industrial Occupation ... 53

Residential Occupation ... 54

Risks and Loss Profile Underwriting Year

2009

...

Agricultural Occupation ... 55

Commercial Occupation ... 56

Industrial Occupation ... 57

Residential Occupation ... 58

Risks and Loss Profile Underwriting Year

2008

...

Agricultural Occupation ... 59

Commercial Occupation ... 60

Industrial Occupation ... 61

Residential Occupation ... 62

Risks and Loss Profile Underwriting Year

2007

...

Agricultural Occupation ... 63

Okupasi Industrial ... 65

Okupasi Residential ... 66

Profil Risiko dan Klaim Tahun Underwriting

2006

...

Okupasi Agricultural ... 67

Okupasi Commercial ... 68

Okupasi Industrial ... 69

Okupasi Residential ... 70

Peta.7.1 Distribusi Kejadian Gempa di

Indonesia 2004 - 2010 ... 71

Daftar Istilah ...

Lampiran

1.

Tarif Asuransi Gempa Bumi Indonesia ...

2.

Skala First Loss ...

3.

Tabel Jangka Waktu Pertanggungan

Kurang dari satu tahun ...

4.

Tabel Indemnitas ...

Industrial Occupation ... 65

Residential Occupation ... 66

Risks and Loss Profile Underwriting Year

2006

...

Agricultural Occupation ... 67

Commercial Occupation ... 68

Industrial Occupation ... 69

Residential Occupation ... 70

Map 7.1 Indonesia Earthquake Distribution of

occurrences 2004-2010 ... 71

Glossaries ...

Attachments

1.

Indonesia Earthquake Insurance Tariff ....

2.

First Loss Scale ...

3.

Short Period Table

less

than one year

period

...

1.

Statistik dibuat berdasarkan Underwriting

Year yang tercatat sampai dengan posisi

31 Desember 2010.

2.

Sesi Limit

2.1.

Limit Sesi didasarkan atas setiap

risiko.

2.2.

Yang dimaksud dengan setiap risiko

(

anyone risk

) adalah akumulasi

(

aggregate

)

jumlah

harga

pertanggungan seluruh risiko pada

lokasi yang sama untuk

masing-masing

perusahaan

asuransi.

Definisi setiap risiko atau setiap

lokasi ditentukan oleh perusahaan

asuransi atau penerbit polis sesuai

dengan interpretasi perusahaan

asuransi dalam

underwriting

polis

kebakaran.

2.3. Besarnya Limit Sesi atas setiap

risiko (

any one risk

) untuk gabungan

kerugian fisik dan gangguan usaha

adalah sebagai berikut :

2.3.1.

Untuk daerah Jawa Barat,

Banten dan DKI : 5%

(lima prosen) dari jumlah

seluruh pertanggungan (

total

sum insured

) maksimum

USD 2,500,000.00 (dua juta

lima ratus ribu Dollar

Amerika) atas setiap risiko,

setiap perusahaan asuransi

atau penerbit polis.

2.3.2 Untuk daerah Indonesia

lainnya 25% (dua puluh lima

prosen) dari jumlah seluruh

pertanggungan (

total sum

insured

) maksimum USD

2,500,000.00 (dua juta lima

ratus ribu Dollar Amerika)

atas setiap risiko setiap

1.

Statistics

are

made

based

on

Underwriting Year basis, which is

recorded as at December 31 2010.

2.

Cession Limit

2.1.

Cession Limit is based on any one

risk.

2.2.

Anyone risk is the accumulation of

(aggregate) total sum insured of all

risks at the same location for each

insurance company. The definition of

anyone risk or any location is

specified by the insurer or policy

issuer in accordance with the

interpretation of insurance companies

in underwriting fire policy.

2.3.

Cession Limit of any one risk for the

combined material and business

interruption damage are as follows:

2.3.1

For West Java, Banten and DKI

: 5% (five percent) of the total

sum insured, a maximum of

USD 2,500,000.00 (two million

five hundred thousand U.S.

Dollars) for any one risk, each

insurance company or policy

issuer

2.3.2

Others area within Indonesia

are 25% (twenty five percent) of

total sum insured, maximum of

USD 2,500,000.00 (two million

five hundred thousand U.S.

Dollars) for each risk, each

insurance company or policy

issuer.

Informasi Statistik

Statistics Information

perusahaan asuransi atau

penerbit polis.

2.4.

Dalam hal penutupan secara

First

Loss Basis / Sub-limit

, jumlah yang

disesikan sebagaimana diatur dalam

butir

2.3.

diatas,

dikalikan

prosentase

First Loss Basis /

Sub-limit Basis

.

2.5.

Bilamana risiko ditutup secara

ko-asuransi, jumlah maksimum sesi dari

semua Anggota ko-asuransi adalah

sesuai dengan ketentuan yang diatur

dalam 2.3. diatas. Sesi

masing-masing

perusahaan

adalah

proporsional sebanding sahamnya

dalam ko-asuransi.

Dalam hal terdapat penutupan lain

selain polis ko-asuransi tersebut

pada obyek pertanggungan yang

sama, perusahaan asuransi tetap

dapat mensesikan risiko dimaksud,

dengan catatan jumlah seluruh sesi

perusahaan asuransi bersangkutan

tidak melebihi ketentuan yang diatur

pada butir 2.3.

3.

Tarif Premi

3.1. Penutupan dengan menggunakan

Full Value Basis mengaplikasikan

Tarif Premi Standar Gempa Bumi

Indonesia (lampiran 1)

3.2. Penutupan dengan First Loss / Sub

Limit Basis mengaplikasikan standar

First Loss Scale (lampiran 2)

3.3. Perhitungan premi untuk penutupan

kurang dari 12 (dua belas) bulan

diberlakukan skala premi jangka

pendek (lampiran 3)

3.4. Untuk perhitungan premi Bussiness

Interruption diberlakukan Indemnity

Period Scale (lampiran 4)

4.

Obyek Pertanggungan

4.1. Obyek pertanggungan yang dapat

disesikan

adalah

obyek

pertanggungan asuransi kebakaran

berupa :

2.4

In term of first loss basis / sub limit

policies, the amount cessions are

stipulated in item 2.3 above, then

multiplied by the percentage of First

Loss Basis / Sub-limit Basis.

2.5

For coinsurance policies, maximum

cession from all members of

coinsurance is stipulated in item 2.3

above. Each ceding company cedes

proportionally depending on its

share.

In the even there are other policies

on the same risk beside that

coinsurance policy, insurer still can

cede such risks subject to the

maximum limit set out in item 2.3

3.

Premium Tariff

3.1.

For the coverage of Full Value Basis,

Indonesian earthquake rate standard

is applied (attachment 1).

3.2.

The coverage First Loss / Sub Limit

Basis uses standard First Loss Scale

(attachment 2).

3.3.

Premium calculation for short period

coverage is based on Short Period

Scale (attachment 3).

3.4.

Premium calculation for business

interruption is based on Indemnity

Period Scale (attachment 4)

4.

Insured Objects

4.1.

Insured objects that can be ceded

are insured objects in fire policy.

such as :

4.1.1. Kerusakan Fisik :

Bangunan

Pondasi

Penggalian dan

Sejenisnya

Persediaan Barang

Lain-lain

4.1.2 Gangguan Usaha :

Keuntungan Bruto

Upah

Kenaikan

Biaya

Operasional

Lain-lain

4.2 Penutupan sebagaimana dimaksud

pada butir 4.1. adalah yang ditutup

secara langsung (direct business)

termasuk ko-asuransi. Penutupan

tidak

langsung

(indirect

business/Reasuransi) tidak dapat

disesikan.

5.

Pelaporan Bordero.

Pelaporan bordero dilakukan setiap

bulannya untuk semua risiko yang ditutup

pada bulan yang bersangkutan dan sudah

harus diterima selambat-lambatnya pada

akhir bulan berikutnya.

6.

Untuk kasus “Multi Location Risk” yang

mengalami kesulitan dalam memberikan

detail harga pertanggungan perlokasi

maka dengan persetujuan AAUI pensesian

risiko dan perhitungan premi dilakukan

pada zona-zona tertentu.

7.

Untuk menggambarkan premi dan harga

pertanggungan yang sebenarnya dalam

penutupan

asuransi

gempa

bumi

berdasarkan ko-asuransi, diharapkan agar

seluruh anggota ko-asuransi mensesikan

risiko gempa bumi tersebut.

4.1.1.

Material damage :

Buildings

Foundations

Excavation and the like

Stocks

Others

4.1.2.

Business Interruption

Gross Profit

Wages

Increase in cost of working

Others

4.2.

Insured objects referred in item 4.1

are objects from direct business

insurance, including coinsurance.

Indirect businesses cannot be

ceded.

5.

Bordereaux Report.

Bordereaux reports is submitted on a

monthly basis for all risk underwritten in the

month concerned and should be received

by the end of the following month.

6.

In the case of Multi Location Risks with no

details of sum insured provided per

location, the risk cession and its premium

calculation specified zones after approved

by AAUI.

7.

In order to get overall pictures of each

earthquake insurance covers, it is strongly

hoped that all coinsurance members could

cede the earthquake cession.

A.

Pendahuluan.

Dengan mengukur Pendapatan Domestik Bruto

(PDB) berdasarkan laporan yang dikeluarkan

Biro Pusat Statistik dalam laporan triwulan

2010-nya, ternyata PDB nasional pada triwulan

keempat 2010 meningkat sebesar 14,42% dari

Rp. 5.613,40 triliun di tahun 2009 menjadi Rp.

6.422,91 triliun di tahun 2010 ini.

Tingkat Pendapatan Domistik Bruto (PDB)

Indonesia dalam lima tahun terakhir dapat dilihat

pada grafik 1.1 dibawah ini

B.

Struktur Pasar.

Maipark dimiliki oleh seluruh perusahaan

asuransi dan reasuransi umum di Indonesia,

Partisipasi kepada Maipark bersifat wajib.

Data-data dalam laporan ini merupakan hasil dari sesi

wajib statistik gempa bumi tersebut ditambah

sesi bukan statistik.

A.

Introduction

By measuring its Gross Domestic Product (GDP)

based on the quarterly report in 2010 issued by

Statistic Centre Bureau, the national GDP has

increased 14,42% or from Rp. 5.613,40 trillion in

2009 to Rp. 6.422,91 trillions in 2010.

The level of Indonesia’s Gross Domestic Product

during the last five years is shown in graph 1.1

below.

B.

Market Structure.

Maipark is owned by all general insurance and

reinsurance

companies

in

Indonesia.

Participation to Maipark was made compulsory.

All data in this report is generated from

stastistical compulsory cession and non

statistical cession.

Pendapatan Domestik Bruto (PDB)

Gross Domestik Product (GDP)

Grafik 1.1 / Graph 1.1

Ikhtisar Usaha Asuransi Gempa Bumi Indonesia Tahun 2010

Summary of Indonesian Earthquake Insurance Business Activities in 2010

Dalam Miliar Rupiah

In Billion Rupiah

Per 31 Desember 2010, seperti yang dilaporkan

oleh Bapepam LK – Departemen Keuangan

dalam laporan

Indonesian insurance directory

2010

, jumlah perusahaan asuransi dan

reasuransi umum di Indonesia adalah 90

perusahaan. Dengan rincian 86 perusahaan

asuransi umum dan 4 perusahaan reasuransi

umum. Dari ke 86 perusahan asuransi umum ini,

20 diantaranya adalah perusahaan patungan.

Sedangkan 66 sisanya adalah perusahaan

swasta nasional. Dari 4 perusahaan reasuransi

umum, kesemuanya adalah juga perusahaan

swasta nasional.

C.

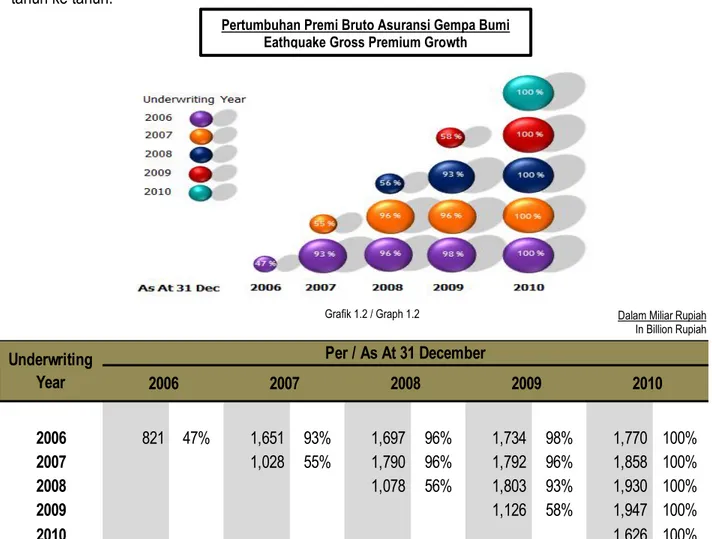

Pertumbuhan Premi Bruto

Seiring dengan meningkatnya laju pertumbuhan

ekonomi Indonesia, seperti yang terlihat dari

pertumbuhan Pendapatan Domestik Bruto,

pendapatan premi bruto asuransi gempa bumi

pun meningkat dari tahun ke tahun.

Sampai dengan posisi per 31 Desember 2010,

pendapatan premi bruto untuk tahun underwriting

2006 adalah sebesar Rp. 1.770 Milliar. Premi

Bruto untuk tahun underwriting 2007 tercatat

sebesar Rp. 1.858 Milliar, sedangkan tahun

underwriting 2008 adalah Rp. 1.930 milliar. Untuk

tahun underwriting 2009 dan 2010 pendapatan

premi bruto asuransi gempa bumi adalah

sebesar Rp. 1.947 milliar dan Rp. 1.626 milliar.

Angka-angka ini dipastikan akan terus bergerak

naik karena pensesian yang masih terus

berlanjut, terutama untuk tahun underwriting

2009 dan 2010.

Jika mengasumsikan tidak ada pertumbuhan

premi yang berarti pada tahun underwriting 2006,

2007 dan 2008, maka dapat dikatakan bahwa

premi asuransi gempa bumi di tahun underwriting

2007 tumbuh sebesar 4,97% dibanding tahun

2006, sedangkan untuk tahun underwriting 2008

premi tumbuh sebesar 3,87% dari tahun

sebelumnya.

As at December 31, 2010, Based on the report in

Indonesia Insurance Directory 2010 issued by

Bapepam LK- Ministry of Finance, there are 90

insurance companies which consist of 86 general

insurance companies and 4 reinsurance

companies. 20 general insurance companies are

joint venture and the remaining are private

national companies. The four reinsurance

companies are also private national.

C.

Gross Premium Growth

As reflected in the development of Gross

Domistik Product, the growth of the gross

premium of earthquake insurance is in line with

the growth of Indonesian economic every year.

As at December 31 2010, earthquake gross

premium income for underwriting year 2006 is

Rp. 1.770 billions. Gross premium for 2007 was

booked for Rp. 1.858 billions. While underwriting

year 2008 premium is Rp. 1.930 billions. Gross

Premium for underwriting year 2009 and 2010

are Rp. 1.947 billions and Rp. 1.626 billions. This

gross premium income will keep moving up

because

earthquake

cession

continues,

especially for underwriting year 2009 and 2010.

If there is no significant movement on the

underwriting year 2006,2007,and 2008, the

earthquake insurance premium for underwriting

year 2007 would be 4,97% higher than

underwriting year 2006. While premium growth

for underwriting year 2008 is 3,87% higher than

underwriting year 2007.

Tabel 1.1 dan grafik 1.2 berikut ini

menggambarkan pertumbuhan premi bruto dari

tahun ke tahun.

Dari tabel dan grafik diatas tampak bahwasannya

pertumbuhan premi bruto asuransi gempa bumi

pada tahun ke dua, untuk setiap tahun

underwriting, rata-rata sudah mencapai lebih dari

90% dari maksimum pertumbuhannya.

Pada setiap tahun underwriting, pelaporan sesi

asuransi gempa bumi di tahun pertama, juga

menunjukkan

peningkatan.

Untuk

tahun

underwriting 2006 tercatat rasio sebesar 47%

dari total premi tahun underwriting tersebut.

Angka ini meningkat tajam di tahun underwriting

2007 menjadi sebesar 55% dan terus menaik di

tahun underwriting 2008 sebesar 56% dan tahun

underwriting 2009 sebesar 58%.

Table 1.1 and graph 1.2 below show gross

premium development from year to year.

The table and graph above shows that, on

average, the growth of gross premium income

reaches over 90% maximum at its second

underwriting year.

For each underwriting year, earthquake

insurance cession report at its first year shows

increament. For underwriting year 2006, the ratio

is only 47% from total. It increased more sharply

than underwriting year 2007 to become 55% and

keeps moving up at 56% for underwriting year

2008 and 58% for underwriting year 2009.

2006

821 47% 1,651 93% 1,697 96% 1,734 98% 1,770 100%

2007

1,028 55% 1,790 96% 1,792 96% 1,858 100%

2008

1,078 56% 1,803 93% 1,930 100%

2009

1,126 58% 1,947 100%

2010

1,626 100%

2007

2006

Underwriting

Year

Per / As At 31 December

2008

2009

2010

Grafik 1.2 / Graph 1.2

Tabel 1.1 / Table 1.1

Dalam Miliar Rupiah

In Billion Rupiah

Pertumbuhan Premi Bruto Asuransi Gempa Bumi

Eathquake Gross Premium Growth

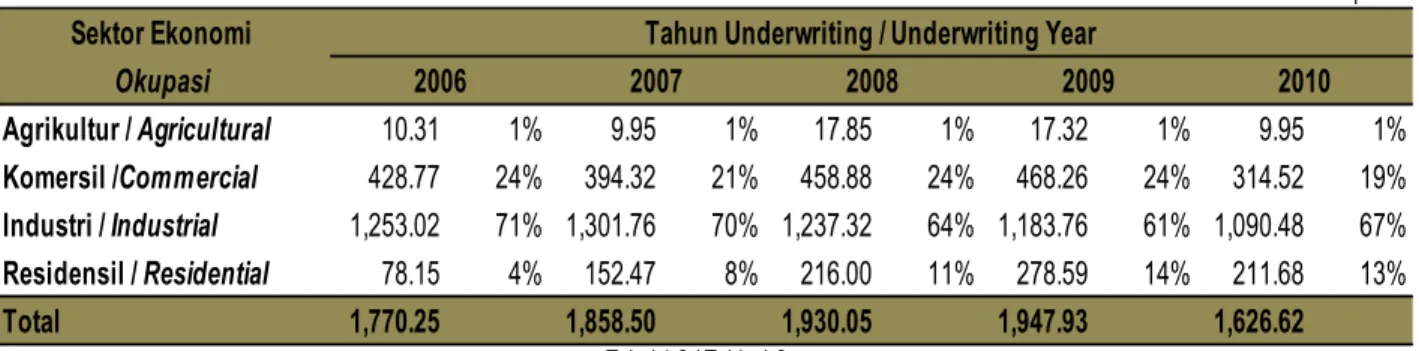

Kontribusi terbesar premi asuransi gempa bumi

yang tercatat sampai dengan 31 Desember 2010

untuk

tiap

tahun

underwriting

masih

menunjukkan tingginya tingkat pendapatan premi

yang diperoleh dari okupasi industri, dengan

rata-rata rasio pendapatan dalam 5 tahun

terakhir underwriting sebesar 66% dari total

premi. Diikuti oleh okupasi komersial dengan

rasio sebesar 23% dan residensial sebesar 10%.

Sedangkan okupasi agrikultural menyumbang

hanya sebesar rata-rata 1% disetiap tahun

underwriting.

Meskipun okupasi agrikultural dan residensial

memberikan kontribusi yang tidak sebesar

okupasi industri ataupun komersial. Namun jika

melihat pertumbuhan premi bruto disetiap tahun

underwriting, kedua okupasi ini mengalami

pertumbuhan premi yang cukup tinggi dan diatas

rata-rata pertumbuhan premi semua okupasi

disetiap tahunnya. Pertumbuhan yang cukup

tinggi dan berlangsung tiap tahun pada okupasi

residensial terjadi, baik itu jumlah maupun rasio

kontribusi pada total pendapatan premi di setiap

tahun underwriting.

Dibanding dengan tahun underwriting 2006,

pendapatan premi bruto dari okupasi residensial

di tahun underwriting 2007 tumbuh hampir dua

kali lipat. Pertumbuhan ini terus berlanjut

meskipun tak sebesar pertumbuhan ditahun

underwriting 2007. Di tahun underwriting 2010,

dimana pensesian masih terus berlangsung,

okupasi ini telah mengumpulkan pendapatan

premi bruto sebesar Rp. 211,68 milliar. Angka ini

diproyeksikan akan terus tumbuh hingga

mencapai Rp. 350 milliar.

Pertumbuhan premi yang cukup tinggi di okupasi

agrikultural terlihat pada tahun underwriting

2008, dimana pendapatan premi tumbuh hampir

80% lebih besar dibanding tahun underwriting

sebelumnya.

Tabel 1.2 berikut ini menyajikan rincian premi

bruto untuk tiap tahun underwriting berdasarkan

okupasi.

As at Desember 31 2010, the highest earthquake

premium contribution for each underwriting year

is coming from industrial occupation, the average

income ratio is 66% for the last five underwriting

years. Followed by commercial occupation with

ratio of 23% and 10% from residential

occupation. The other side, agricultural

occupation contributes only about 1% for each

underwriting year.

Although contributions of agricultural and

residential occupation are not as high as

industrial or commercial, their gross premiums

still increase significantly every year. Their

increaments of each underwriting year are even

above average in all occupations combined. For

residential occupation in each underwriting year,

the significant increase are both on its total gross

premium and its contribution ratio.

The gross premium of residential for underwriting

year 2007 is almost doubled comparing to that of

underwriting year 2006. This growth continued

although it is not as high as in underwriting year

2007. In underwriting year 2010, where cession

continues, this occupation has produced Rp.

211,68 billions of gross premium income. This

figure is projected to grow and reach Rp. 350

billions.

The significant growth in agricultural occupation

is in underwriting year 2008, where premium is

80% higher than previous underwriting year.

This following table 1.2, shows detail gross

premium for the last five years by occupation.

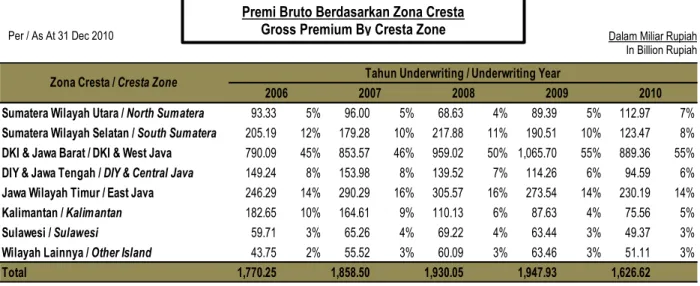

Dilihat dari distribusi premi berdasarkan cresta

zone dalam 5 tahun underwriting terakhir,

penyebaran risiko gempa bumi masih terpusat di

zona 3 (DKI Jakarta dan Jawa Barat). Meskipun

pendapatan premi masih terus dapat berubah

dikarenakan pensesian masih terus berlangsung,

namun terlihat tingkat rasio pada zona 3 ini terus

beranjak naik dari 45% pada tahun underwriting

2006 menjadi 55% di tahun underwriting 2010

dengan rata-rata tiap tahun underwriting sebesar

50%.

Jika zona 3 terus bertambah naik, penurunan

justru terjadi pada zona 6 (Kalimantan).

Penurunan ini tampak secara rasio maupun

jumlah pendapatan premi brutonya, hal ini terlihat

Dari tahun underwriting 2006-2008, dimana pada

ketiga tahun underwriting ini, premi tidak akan

banyak berubah. Pada tahun underwriting 2006,

zona ini memberikan kontribusi sebesar 10%.

Tingkat rasio ini terus turun pada setiap

tahunnya, hingga hanya mencapai sebesar 5%

pada tahun underwriting 2010.

Pada zona lain, rasio distribusi premi untuk tiap

tahun underwriting terlihat stabil. Seperti yang

terlihat pada tabel 1.3 berikut ini.

The premium distribution based on cresta zone

for the last last 5 underwriting years is centralized

in zone 3 (DKI Jakarta and West Java). The ratio

is growing from 45% in underwriting year 2006 to

55% in underwriting year 2010 with the average

of 50% each year. This is due to the cessions are

still in process.

While zone 3 is increasing, the decrease on the

other hand occurred on zone 6 (Kalimantan) on

both ratio and its earthquake gross premium.

Underwriting year data of 2006 – 2008 shows the

decrease, where gross premium for these

underwriting years remain steady. On

underwriting year 2006, this zone contributes

10%. This contribution ratio keeps decreasing

each underwriting year until only 5% contribution

ratio on underwriting year 2010.

On the other zones, premium distribution ratio for

each underwriting year seems consistent as

shown in table 1.3 below.

Agrikultur /

Agricultural

10.31

1%

9.95

1%

17.85

1%

17.32

1%

9.95

1%

Komersil /

Commercial

428.77

24%

394.32

21%

458.88

24%

468.26

24%

314.52

19%

Industri /

Industrial

1,253.02

71% 1,301.76

70% 1,237.32

64% 1,183.76

61% 1,090.48

67%

Residensil /

Residential

78.15

4%

152.47

8%

216.00

11%

278.59

14%

211.68

13%

Total

1,770.25

1,858.50

1,930.05

1,947.93

1,626.62

Sektor Ekonomi

Okupasi

2006

2007

2008

2009

2010

Tahun Underwriting / Underwriting Year

Premi Bruto Berdasarkan Okupasi

Gross Premium By Occupation

Dalam Miliar Rupiah

In Billion Rupiah

Tabel 1.2 / Table 1.2

Per / As At 31 Dec 2010

D.

Jumlah Risiko

Seiring dengan pertumbuhan jumlah premi bruto

yang terus meningkat, jumlah risiko asuransi

gempa bumi juga terus meningkat. Dari keempat

okupasi yang ada, peningkatan yang cukup

berarti terlihat pada okupasi residensial.

Tabel dibawah ini menyajikan jumlah risiko,

namun tidak termasuk risiko multilokasi yg tidak

lengkap datanya. Dimana kami kesulitan

memisahkannya untuk menjadi satu risiko.

Pertumbuhan gross premi yang terus meningkat

pada okupasi residensial, tampak pada tabel

diatas, pertumbuhan ini diiringi dengan

peningkatan jumlah risikonya. Baik itu di tahun

underwriting 2006, 2007, 2008 dan 2009.

D.

Number of Risks

The gross premium of earthquake insurance

grows as well as the number of earthquake risk.

The growth of gross premium in residential keeps

increasing as shown in the above table.

This following table shows earthquake number of

risks, excluding unidetified multi location risks. As

we see it is difficult to separate them into single

risk.

The gross premium grow is increasing on

residential occupation, as shown by the above

table. This growth is in line with the number of

risks on residential occupation in underwriting

year 2006, 2007, 2008 and 2009.

Sumatera Wilayah Utara /

North Sumatera

93.33

5%

96.00

5%

68.63

4%

89.39

5%

112.97

7%

Sumatera Wilayah Selatan /

South Sumatera

205.19

12%

179.28

10%

217.88

11%

190.51

10%

123.47

8%

DKI & Jawa Barat / DKI & West Java

790.09

45%

853.57

46%

959.02

50% 1,065.70

55%

889.36

55%

DIY & Jawa Tengah /

DIY & Central Java

149.24

8%

153.98

8%

139.52

7%

114.26

6%

94.59

6%

Jawa Wilayah Timur / East Java

246.29

14%

290.29

16%

305.57

16%

273.54

14%

230.19

14%

Kalimantan /

Kalimantan

182.65

10%

164.61

9%

110.13

6%

87.63

4%

75.56

5%

Sulawesi /

Sulawesi

59.71

3%

65.26

4%

69.22

4%

63.44

3%

49.37

3%

Wilayah Lainnya /

Other Island

43.75

2%

55.52

3%

60.09

3%

63.46

3%

51.11

3%

Total

1,770.25

1,858.50

1,930.05

1,947.93

1,626.62

Zona Cresta /

Cresta Zone

2006

2007

2008

2009

2010

Tahun Underwriting / Underwriting Year

Premi Bruto Berdasarkan Zona Cresta

Gross Premium By Cresta Zone

Dalam Miliar Rupiah

In Billion Rupiah

Per / As At 31 Dec 2010

Tabel 1.4 / Table 1.4

Agricultural

464

100%

414

89%

626

135%

409

88%

228

49%

Commercial

38,231

100%

39,128

102%

65,009

170%

56,713

148%

46,101

121%

Industrial

9,236

100%

11,746

127%

9,773

106%

11,791

128%

9,418

102%

Residential

23,680

100%

31,594

133%

36,070

152%

41,414

175%

36,128

153%

Total

71,611

82,882

111,478

110,327

91,875

Okupasi

2006

2007

2008

2009

2010

Tahun Underwriting / Underwriting Year

Pertumbuhan Jumlah Risiko Asuransi Gempa Bumi

Earthquake Insurance Risk Number Development

Tabel 1.3 / Table 1.3

Per / As At 31 Dec 2010

Dalam Miliar Rupiah

In Billion Rupiah

Peningkatan jumlah risiko juga dialami oleh

okupasi komersial, meskipun dilihat dari tingkat

pertumbuhan pendapatan premi brutonya

tidaklah terlalu berubah banyak.

E.

Kontribusi Asuransi Gempa Bumi

Pertumbuhan yang dialami ekonomi Indonesia

juga tampak dari pertumbuhan industri asuransi,

baik itu asuransi jiwa maupun asuransi kerugian.

Dalam catatan terakhir yang dikeluarkan oleh

Biro Perasuransian Bapepam LK, dalam buku

Perasuransian

Indonesia

2009,

tercatat

penerimaan premi bruto asuransi di tahun 2009

meningkat

sebesar

17,9%

dari

tahun

sebelumnya menjadi Rp. 106,4 triliun. Rasio

antara premi bruto terhadap Produk Domestik

Bruto sebesar 1,9%.

Pada tahun 2009, Asuransi kerugian dan

reasuransi mencatat premi bruto sebesar Rp.

25.07 triliun, atau meningkat sebesar 6,08% dari

tahun 2008. Di lini usaha asuransi properti

sendiri pendapatan premi bruto tumbuh sebesar

4% menjadi Rp. 7,72 triliun.

Asuransi gempa bumi merupakan bagian dari

asuransi properti. Sebelumnya, asuransi gempa

bumi

hanyalah

merupakan

perluasan

(ekstension) atas polis asuransi properti, namun

sejak tahun 2007 telah ada Polis Standar

Asuransi Gempa Bumi Indonesia (PSAGBI) yang

memungkinkan asuransi gempa bumi ditutup

secara terpisah.

Dengan memproyeksi pendapatan premi bruto

asuransi gempa bumi untuk tahun 2009 dan

2010, maka rata-rata kontribusi asuransi gempa

bumi terhadap produk domistik bruto dalam lima

tahun terakhir adalah sebesar 0,04%.

Sedangkan, kontribusi asuransi gempa bumi

terhadap penutupan asuransi property dalam

lima tahun terakhir adalah sebesar 27,54%. Atau,

dari tiga sampai empat penutupan asuransi

property terdapat satu penutupan asuransi

gempa bumi, baik itu yang hanya merupakan

The growth of number of risk also occurs in

commercial occupation, despite less change in

the premium.

E.

Earthquake Insurance Contribution

Indonesian economic growth is reflected on its

insurance industry’s growth. On last publications

of Indonesia Insurance 2009 issued by

Indonesian Insurance Bureau, the gross premium

for 2009 rose 17,9% to become Rp. 106,4 trillion.

The ratio of gross premium to gross domestic

product is about 1,9%.

In 2009, gross premium of general insurance and

reinsurance is Rp. 25,07 trillion, or increase for

6,08% from 2008. For property insurance itself,

the gross premium increases for 4% than

previous year and become Rp. 7,72 trillions.

Earthquake insurance is a part of property

insurance. At the beginning, earthquake

insurance is only an extension of property

insurance policy. Since 2007, there is Indonesian

Earthquake Insurance Standard Policy which

enables earthquake insurance policy to be

covered separately.

By projecting earthquake gross premium for year

2009 and 2010, the average earthquake

contribution to gross domestic product for the last

five years is about 0,04%. While, earthquake

contribution to property insurance for the last five

years is around 27,54%, it means that in every

three or four property insurance issued, there is

one earthquake cover, whether it is as a property

insurance extension or a stand-alone policy.

perluasan dari polis property maupun penutupan

yang berdiri sendiri.

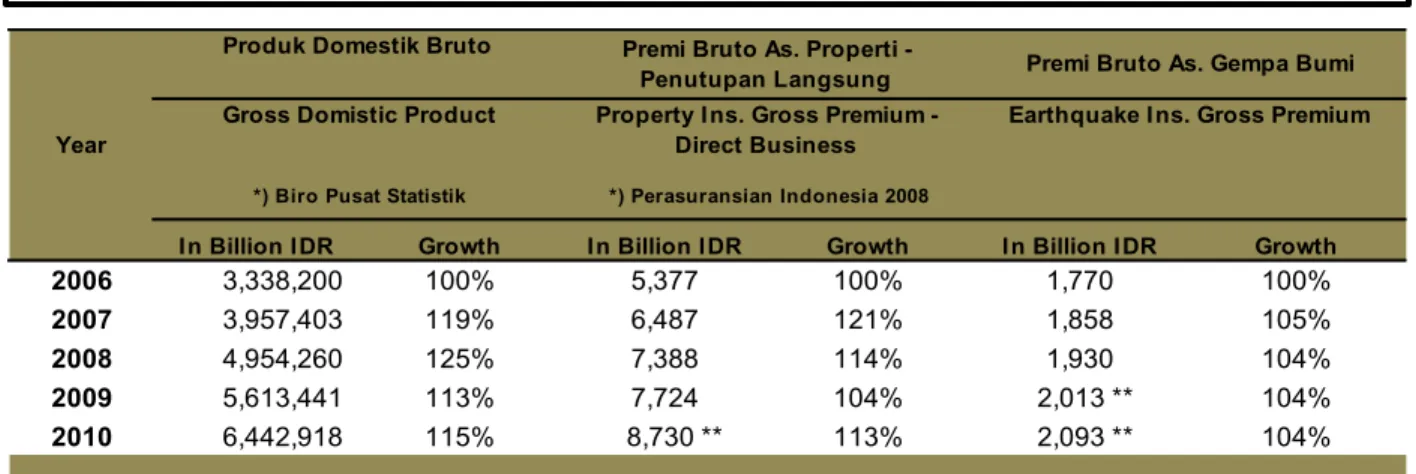

Produk Domestik Bruto, Premi Bruto Asuransi

Property yang bersumber dari penutupan

langsung serta Premi Bruto Asuransi Gempa

Bumi selama 2006 hingga 2010, dapat dilihat di

tabel 1.5 berikut.

Seperti yang terlihat dari penyebaran asuransi

gempa bumi berdasarkan zona cresta, ternyata

cresta 3 adalah pusat dari penyebaran asuransi

gempa bumi di Indonesia. Jika dilihat per provinsi

maka Provinsi DKI Jakarta, Jawa Barat dan

Banten yang merupakan bagian dari cresta 3,

adalah pusat-pusat provinsi asuransi gempa

bumi. Dalam lima tahun terakhir,masing-masing

provinsi tersebut menyumbang rata-rata sebesar

20%,17% dan 10% dari total pendapatan premi

asuransi gempa bumi nasional. Diikuti oleh

Provinsi Jawa Timur yang mencatat kontribusi

sebesar rata-rata 14% dan Jawa Tengah dengan

kontribusi rata-rata sebesar 7%.

Di kepulauan Sumatera, Provinsi Riau, dengan

pendapatan premi yang besar dari industri gas,

minyak bumi serta kertas, mencatatkan diri

sebagai penyumbang terbesar premi asuransi

gempa bumi di kepulauan ini. Dengan kontribusi

sebesar 4,24%, diikuti oleh provinsi sumatera

Gross Domestic Product, gross property

premium income from direct business and

earthquake gross premium from 2006 to 2010

are shown in table 1.5 below:

As we can see the spread of the earthquake

insurance by cresta zone, cresta 3 is the central

spread of the Indonesian insurance. If we see the

insurance earthquake spread by province,

province of DKI Jakarta, West Java and Banten

(all are in cresta 3) are the central province of

earthquake insurance. Within the last five years,

each province contribute the average of

20%,17%, and 10% of total national earthquake

insurance premium. It is followed by province of

East Java which contributed the average of 14%,

and Central Java with the average of 7%.

In Sumatera Island, Riau Province with gross

premium income from oil, gas and pulp industries

is the biggest producer of earthquake gross

premium within this island. It contributes about

4,24%, followed by North Sumatera Province

3,68% ,South Sumatera 2,4% and Lampung

1,35%.

In Billion IDR

Growth

In Billion IDR

Growth

In Billion IDR

Growth

2006

3,338,200

100%

5,377

100%

1,770

100%

2007

3,957,403

119%

6,487

121%

1,858

105%

2008

4,954,260

125%

7,388

114%

1,930

104%

2009

5,613,441

113%

7,724

104%

2,013 **

104%

2010

6,442,918

115%

8,730 **

113%

2,093 **

104%

Year

Premi Bruto As. Gempa Bumi

Earthquake Ins. Gross Premium

Produk Domestik Bruto

Gross Domistic Product

*) Biro Pusat Statistik

Premi Bruto As. Properti -

Penutupan Langsung

Property Ins. Gross Premium -

Direct Business

*) Perasuransian Indonesia 2008

Tabel 1.5 / Table 1.5

**) Nilai proyeksi / Projection value

Produk Domistik Bruto,Premi Bruto Asuransi Property dan Premi Bruto Asuransi Gempa Bumi 2006 – 2010

Gross Domestic Product, Property Gross Premium, and Earthquake Gross Premium 2006 - 2010

utara 3,68%, sumatera selatan 2,4% dan

lampung 1,35%.

Dari Pulau Kalimantan, Provinsi Kalimantan

Timur merupakan penyumbang terbesar

terhadap pendapatan premi asuransi gempa

bumi dengan rasio sebesar 5,49% diikuti oleh

Kalimantan tengah sebesar 1,52%.

Tabel 1.6 dibawah ini menyajikan kontribusi

pendapatan premi asuransi gempa bumi yang

dibagi berdasarkan provinsi, catatan per tanggal

31 Desember 2010.

In Kalimantan Island, province of East

Kalimantan is top producer with 5,49%

contribution. It is followed by Central Kalimantan

which contributes about 1,52%.

This following table 1.6 shows earthquake

insurance contribution by province, as at

December 31, 2010.

2006 % 2007 % 2008 % 2009 % 2010 %

1 Nanggroe Aceh Darussalam 26,797 1.51 28,766 1.55 6,285 0.33 9,523 0.49 13,787 0.85 2 Sumatera Utara 66,528 3.76 67,234 3.62 62,342 3.23 79,865 4.10 99,186 6.10 3 Sumatera Barat 13,122 0.74 10,457 0.56 20,579 1.07 17,844 0.92 19,372 1.19 4 Riau 103,014 5.82 73,556 3.96 94,743 4.91 44,412 2.28 25,528 1.57 5 Jambi 4,452 0.25 4,062 0.22 5,024 0.26 33,238 1.71 3,155 0.19 6 Sumatera Selatan 54,983 3.11 51,470 2.77 35,475 1.84 37,427 1.92 26,717 1.64 7 Bengkulu 1,243 0.07 2,372 0.13 6,069 0.31 5,465 0.28 4,486 0.28 8 Lampung 15,867 0.90 20,423 1.10 35,129 1.82 30,702 1.58 28,992 1.78 9 Kepulauan Bangka Belitung 678 0.04 474 0.03 3,340 0.17 4,231 0.22 1,261 0.08 10 Kepulauan Riau 11,832 0.67 16,464 0.89 17,519 0.91 17,190 0.88 13,964 0.86 11 DKI Jakarta 333,909 18.86 353,233 19.01 427,032 22.13 449,634 23.08 304,816 18.74 12 Jaw a Barat 285,327 16.12 326,322 17.56 337,069 17.46 399,064 20.49 321,468 19.76 13 Jaw a Tengah 143,560 8.11 147,234 7.92 126,934 6.58 99,503 5.11 81,030 4.98 14 DI. Yogy akarta 5,676 0.32 6,745 0.36 12,591 0.65 14,756 0.76 13,563 0.83 15 Jaw a Timur 246,293 13.91 290,293 15.62 305,570 15.83 273,542 14.04 230,187 14.15 16 Banten 170,851 9.65 174,015 9.36 194,914 10.10 217,004 11.14 263,074 16.17 17 Bali 27,034 1.53 33,226 1.79 47,326 2.45 53,093 2.73 41,228 2.53 18 Kalimantan Barat 1,655 0.09 1,816 0.10 3,267 0.17 4,165 0.21 2,218 0.14 19 Kalimantan Tengah 19,095 1.08 25,171 1.35 45,856 2.38 24,417 1.25 12,779 0.79 20 Kalimantan Selatan 2,777 0.16 2,777 0.15 3,602 0.19 5,438 0.28 3,784 0.23 21 Kalimantan Timur 159,119 8.99 134,843 7.26 57,406 2.97 53,611 2.75 56,777 3.49 22 Sulaw esi Utara 4,156 0.23 5,212 0.28 5,831 0.30 10,735 0.55 8,080 0.50 23 Sulaw esi Tengah 1,004 0.06 1,572 0.08 1,837 0.10 1,551 0.08 1,284 0.08 24 Sulaw esi Selatan 17,142 0.97 23,365 1.26 24,325 1.26 25,666 1.32 12,817 0.79 25 Sulaw esi Tenggara 36,896 2.08 34,445 1.85 36,385 1.89 8,811 0.45 9,484 0.58 26 Gorontalo 466 0.03 575 0.03 725 0.04 16,025 0.82 17,233 1.06 27 Sulaw esi Barat 53 0.00 86 0.00 118 0.01 651 0.03 474 0.03 28 Nusa Tenggara Barat 1,965 0.11 3,819 0.21 2,916 0.15 2,703 0.14 2,643 0.16 29 Nusa Tenggara Timur 656 0.04 531 0.03 736 0.04 885 0.05 973 0.06 30 Maluku 986 0.06 534 0.03 507 0.03 877 0.05 1,408 0.09 31 Maluku Utara 51 0.00 706 0.04 734 0.04 572 0.03 414 0.03 32 Papua Barat 1,040 0.06 1,169 0.06 1,376 0.07 1,617 0.08 1,678 0.10 33 Papua 12,020 0.68 15,539 0.84 6,490 0.34 3,717 0.19 2,765 0.17

Provinsi / Province

Premi Bruto As. Gempa Bumi Earthquake Insurance Gross Premium

*) As at 31 Dec 2010 Underwriting Year