Evaluating and Controlling Salespeople

Input system -- Behavioral-based

• Subjective evaluations

– Qualitative measures (Table 16-2) – Use rating scales -- e.g., Likert

– Can have bias & halo effects

• Generating data

– Computerized Call Reports (Fig. 16-3)

– Management by Objectives (MBO)(Fig. 16-4) • non-quantitative -- difficult in solution sales – Behavioral Observation Scales (BOS) (Fig 16-5)

Evaluating and Controlling Salespeople

Combining Input & Output Measures

Call Productivity Ratios

Calls per day = # Calls _ # Days worked

Calls per account = # Calls_ # of Accounts

Planned Call = # Planned calls

Total # Calls

Batting Average = # Orders__

Evaluating and Controlling Salespeople

Combining Input & Output Measures

Expense Ratios

Expense to Sales = Expenses

Sales

Cost per Call = Total Costs

Evaluating and Controlling Salespeople

Combining Input & Output Measures

Account Related Ratios

Sales to Account = Dollar Sales _ # Accounts

Average Order Size = Dollar Sales # Orders

Growth Ratio = # New Accounts Total # Accounts

Account Success = Accounts sold_

Evaluating and Controlling Salespeople

Models Combining Input & Output Controls

Inputs

• Attitude

• Motivation

• Skills

• Abilities

• Job Perception

Inputs

Behavior

• # Calls

• Days worked

• Expenses

• Selling vs. non-

selling time

• Quotas

Outputs

• # Orders

• Order Size

• # New, lost,

Evaluating and Controlling Salespeople

Models Combining Input & Output Controls

• Ranking Procedures

– Widely used, simple to use, easy to understand – Add ranks for overall performance measure – Alternatives to sales/salesperson

• Sales to potential -- good coverage of (limited) market

• Sales to quota -- ability to increase revenue

• Sales per order -- profitability relative to size of customer

• Batting average -- efficiency of calls

• Gross margin percentage -- ability to control price

selling best mix of products

Evaluating Sales Force Performance

Cost Analysis

• What costs are relevant?

Net Sales

Less Variable Costs: Cost of Goods Sold

Sales Commissions

Equals:

Contribution Margin

Less:

Direct Fixed Selling Costs

Evaluating Sales Force Performance

Cost Analysis

• Object affects direct vs. indirect cost class:

Cost

By Territory By Product

P-O-P display Direct Direct Salesperson

Salary Direct Indirect Product Manager

Salary Indirect Direct VP Operations

Evaluating Sales Force Performance

Product Costs

• CGS + Commissions higher for computers

– paying too much for parts

– competition has driven down selling prices

– salespeople cutting computer prices to make

deals -- possible actions:

• limit price negotiation capabilities • shift to a gross margin commission

• change commission structure to emphasize

Evaluating Sales Force Performance

District Costs

• Sales managers vary in ability to control expenses

• 3-way: district by product by cost

– watch for price cutting by salespeople

Evaluating Sales Force Performance

Account Cost to Serve

Total Cost to serve account• Cost to Serve =

• Usually decline with revenue

• Help identify best accounts

• Downsizing & Profits (T 15-7)

• Consider using DEA (Programming)

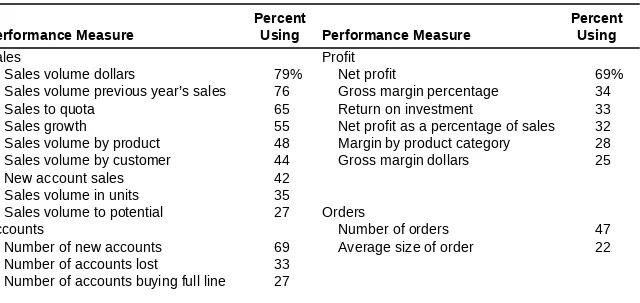

Table 15-1 Output Measures Used in Sales Force Evaluation

Performance Measure

Percent

Using Performance Measure

Percent Using

Sales

Sales volume dollars

Sales volume previous year’s sales Sales to quota

Sales growth

Sales volume by product Sales volume by customer New account sales

Sales volume in units Sales volume to potential Accounts

Number of new accounts Number of accounts lost

Number of accounts buying full line

79% 76 65 55 48 44 42 35 27 69 33 27 Profit Net profit

Gross margin percentage Return on investment

Net profit as a percentage of sales Margin by product category

Gross margin dollars

Orders

Number of orders Average size of order

69% 34 33 32 28 25 47 22

Table 15-2 Input or Behavior Bases used in Sales Force Evaluation Base Percent Using Base Percent Using

Selling expenses to budget Total expenses

Selling expenses as a % of sales Number of calls

55% 53 49 48

Number of calls per day Number of reports turned in Number of days worked

Selling time vs. nonselling time

42% 38 33 27

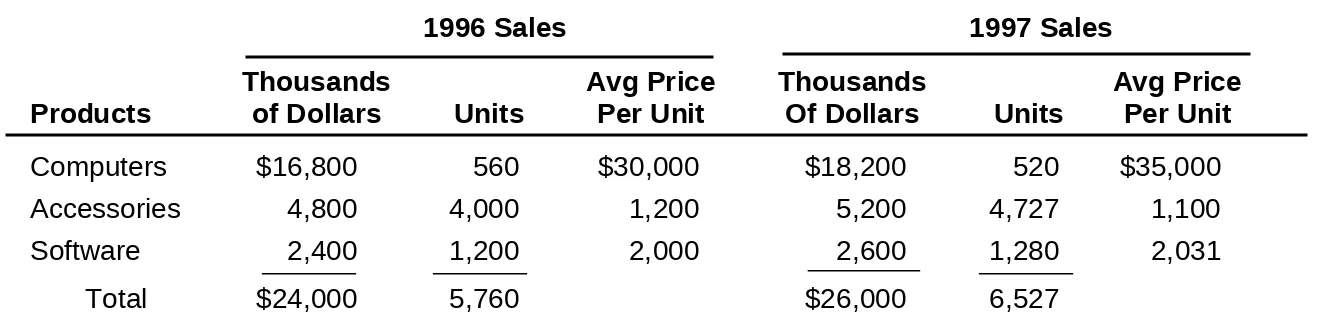

Table 15-4 Comparing Dollar and Unit Sales at the Bear Computer Company

Products

Thousands

of Dollars Units

Avg Price Per Unit

Thousands

Of Dollars Units

Avg Price Per Unit Computers Accessories Software $16,800 4,800 2,400 560 4,000 1,200 $30,000 1,200 2,000 $18,200 5,200 2,600 520 4,727 1,280 $35,000 1,100 2,031 Total $24,000 5,760 $26,000 6,527

Table 15-5 Expense Analysis by Product Line, Bear Computer Company, 1997 Products 1997 Sales (000) CGS and Commission $

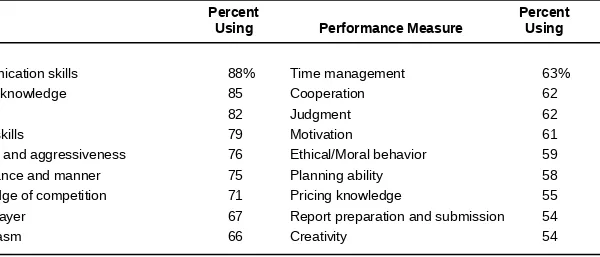

Table 15-6 Qualitative Bases used in Sales Force Evaluation

Base PercentUsing Performance Measure PercentUsing

Communication skills Product knowledge Attitude

Selling skills

Initiative and aggressiveness Appearance and manner Knowledge of competition Team player Enthusiasm 88% 85 82 79 76 75 71 67 66 Time management Cooperation Judgment Motivation Ethical/Moral behavior Planning ability Pricing knowledge

Report preparation and submission Creativity 63% 62 62 61 59 58 55 54 54

Table 15-8 Measuring Territory Profit Output for Bear Computer Company

Territory Performance (thousands)a

Jones Smith Brown West Net Sales $825 $570 $1100 $1000 Less CGS and Commissions 495 428 754 660 Contribution margin 330 142 356 340 CM as a percentage of sales 40% 25% 325 345 Less direct selling costs

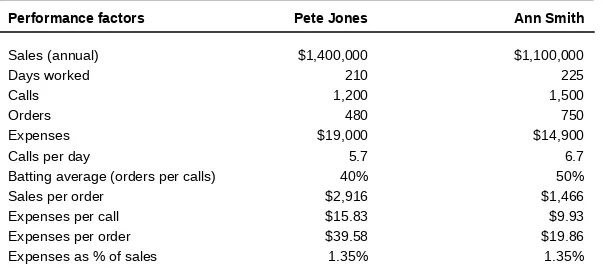

Table 15-9 Evaluating Performance Using Behavior and Outcome Data

Performance factors Pete Jones Ann Smith

Sales (annual) $1,400,000 $1,100,000

Days worked 210 225

Calls 1,200 1,500

Orders 480 750

Expenses $19,000 $14,900

Calls per day 5.7 6.7

Batting average (orders per calls) 40% 50%

Sales per order $2,916 $1,466

Expenses per call $15.83 $9.93

Expenses per order $39.58 $19.86

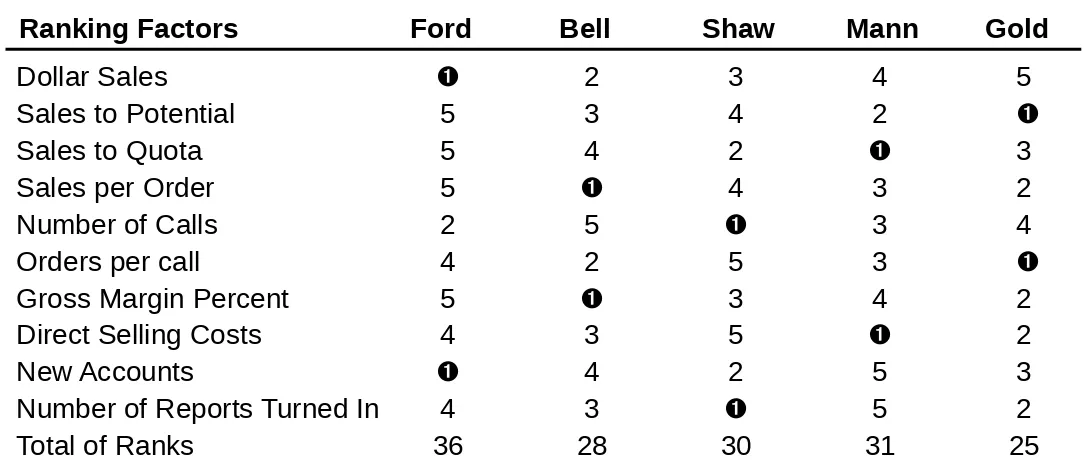

Table 15-10 Ranking Salespeople on 10 Input/Output factors

Dollar Sales 2 3 4 5

Sales to Potential 5 3 4 2

Sales to Quota 5 4 2 3

Sales per Order 5 4 3 2

Number of Calls 2 5 3 4

Orders per call 4 2 5 3

Gross Margin Percent 5 3 4 2 Direct Selling Costs 4 3 5 2

New Accounts 4 2 5 3

Number of Reports Turned In 4 3 5 2

Total of Ranks 36 28 30 31 25

Figure 15-3 Ranking Salespeople on 10 Input/Output factors 3.87 3.66 3.44 3.23 3.02 2.80 2.59 2.38 2.16 1.95 1.74 1.53 1.31 1.10 COMPROMISERS

Avg sales $3.17 Avg contribution $1.13 Avg contribution % 35.8

Age 45

Calls 1122

Number of salespeople 18

STARS

Avg sales $2.91 Avg contribution $1.09 Avg contribution % 37.4

Age 37

Calls 888

Number of salespeople 11

Avg sales $1.78 Avg contribution $ .64 Avg contribution % 35.8

Age 44

Calls 958

Number of salespeople 11

LAGGARDS

Avg sales $2.03 Avg contribution $ .75 Avg contribution % 37.1

Age 35

Calls 921

Number of salespeople 16

SLOWPOKES Millions

$

Contribution Margin (%)

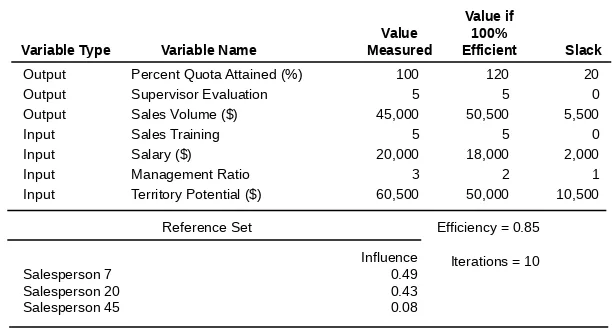

Table 15-11 Relative performance efficiency for Sales Rep 22

Value if Value 100%

Variable Type Variable Name Measured Efficient Slack

Output Percent Quota Attained (%) 100 120 20 Output Supervisor Evaluation 5 5 0 Output Sales Volume ($) 45,000 50,500 5,500

Input Sales Training 5 5 0

Input Salary ($) 20,000 18,000 2,000

Input Management Ratio 3 2 1

Input Territory Potential ($) 60,500 50,000 10,500

Influence

Salesperson 7 0.49

Salesperson 20 0.43

Salesperson 45 0.08

Reference Set Efficiency = 0.85

Iterations = 10

Figure 15-2 A Model of Salesperson Evaluation

Input-based System

Behavior Calls Reports Complaints Demonstrations Dealer meetings Display set up

Travel/entertainment expenses

Results

Sales revenues Sales growth Sales/quota Sales/potential New accounts

Contribution margins Contribution

percentage

Output-based System

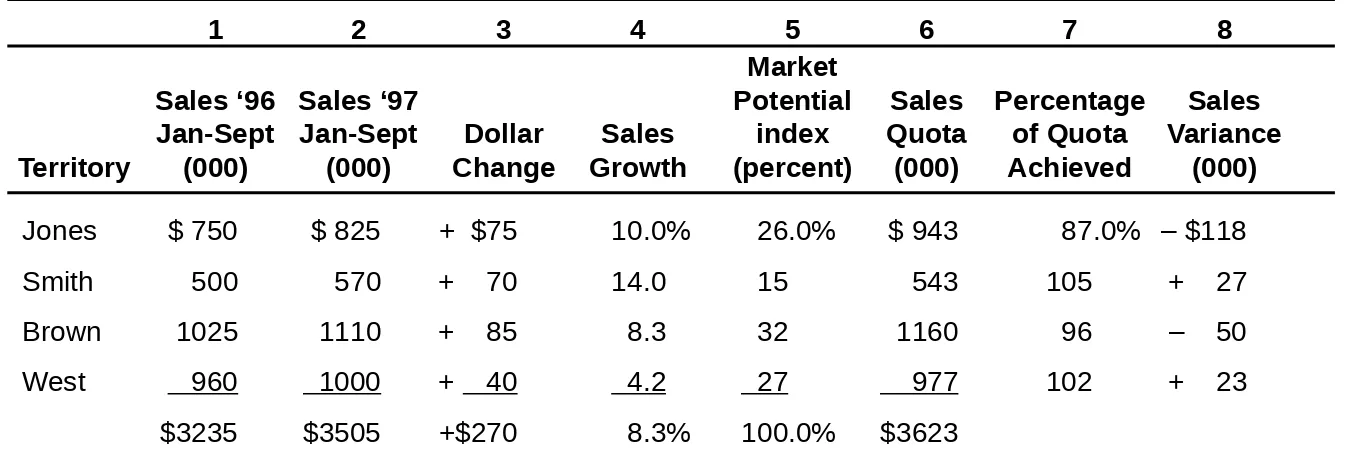

Table 15-7 Measuring Sales Force Output for Bear Computer Company

1 2 3 4 5 6 7 8

Market

Sales ‘96 Sales ‘97 Potential Sales Percentage Sales Jan-Sept Jan-Sept Dollar Sales index Quota of Quota Variance Territory (000) (000) Change Growth (percent) (000) Achieved (000)

Jones $ 750 $ 825 + $75 10.0% 26.0% $ 943 87.0% – $118 Smith 500 570 + 70 14.0 15 543 105 + 27 Brown 1025 1110 + 85 8.3 32 1160 96 – 50 West 960 1000 + 40 4.2 27 977 102 + 23

Figure 15-1: A Sales Force Evaluation Model

Set goals and objectives for sales force, including:

Revenues

Contribution profits Market share

Expense ratios

Design sales plan

Set product performance standards for: Organization Salespeople Regions Accounts Districts

Measure results against

Evaluating Sales Force Performance

Fleet Car Management -- A Motivator

• Salesperson owned car

(

per mile travel allowance)– Salesperson gets car preference

– Allowances rarely cover full salesperson car costs

• Company owned & managed cars

– Ties up a lot of cash

– Costs less than salesperson owned car

• Leased sales fleet of cars

– Frees up cash

Evaluating and Controlling Salespeople

Models Combining Input & Output Controls

• Four Factor Model

– How can sales be increased?

– Optimum Number of sales calls to maximize profits? – Who is doing best? Ann or Pete?

– What management strategies for Pete? for Ann?

$ Sales = Days worked x Calls Orders Sales $ Days Worked Calls Orders

$ Sales = Days worked x Call Rate Batting

Average

Evaluating Sales Force Performance

Profitability Analysis

Full Cost

Sales

Less: C of GS

Equals: Gross Margin

Less: Operating Expenses (Direct +

Indirect Allocated)

Equals: Profit Contribution

Contribution Margin

Sales

C of GS & Other Variables Costs

Contribution Margin

Direct Allocable

Fixed Selling Costs

Evaluating Sales Force Performance

Profitability Analysis

• “Full Cost” Approach

– charge recruiting, training, sales promo &

other marketing expenses to sales manager

– allocation is somewhat arbitrary

Evaluating Sales Force Performance

In-Class Exercise 15-1 --

“Which Profits?” 1. Why would a company that used to use onlysales as a performance criteria for its sales force wish to consider profitability?

2. What criteria should be established to construct a workable performance evaluation system?

3. What are the pros and cons of alternative profit measures?

Evaluating and Controlling Salespeople

In-Class Exercises 16-1

“I Know These Sales Figures Stink” 1. What activities should be completed in the

performance evaluation process?

2. What should take place prior to a performance review meeting?

3. What is covered in the meeting?

4. What to do if an employee disagrees with the performance ratings?

Evaluating and Controlling Salespeople

In-Class Exercises 16-1

“I Know These Sales Figures Stink” 6. How do you handle hostile reactions?

7. What additional questions should Sherrie ask of the veteran sales manager?

8. What consideration should be given to a large customer going out of business?

9. Is sales, the bottom line, the only measure that should be used for evaluating performance?

Evaluating and Controlling Salespeople

Input vs. Output Systems

Salary Compensation Commission

Evaluating and Controlling Salespeople

Using Judgment Models -- Ranking Procedures

1

. How do the six salespeople compare with oneanother? -- Rank them for 1 to 6 overall.

2. Which of the six would you promote to Field

Sales Supervisor (sales manager position)?

3. If you were opening a new territory which is

promising to be quite high in sales potential and thus both lucrative and challenging, and you had to assign one of the six to that territory, which

Evaluating and Controlling Salespeople

Using Judgment Models -- Ranking Procedures

4. If you had to reduce the sales force to only 5

salespeople, and thus had to terminate one of the

salespeople, which one would you terminate? Why?

5. If you had a $10,000 budget for bonuses for your

sales force and had to pay it all out, how much of the $10,000 would you give to each of the

Evaluating and Controlling Salespeople

Using Judgment Models -- Ranking Procedures

• Results of a sample of 242 sales managers

– How do your results compare with the

managers?

– Situation specific evaluations

– Overall evaluations

– Situation Specific Predictive Ability

Evaluating and Controlling Salespeople

Using Judgment Models -- Ranking Procedures

1

. How do the six salespeople compare with oneanother? -- Rank them for 1 to 6 overall.

2. Which of the six would you promote to Field

Sales Supervisor (sales manager position)?

3. If you were opening a new territory which is

promising to be quite high in sales potential and thus both lucrative and challenging, and you had to assign one of the six to that territory, which

Evaluating and Controlling Salespeople

Using Judgment Models -- Ranking Procedures

4. If you had to reduce the sales force to only 5

salespeople, and thus had to terminate one of the

salespeople, which one would you terminate? Why?

5. If you had a $10,000 budget for bonuses for your

sales force and had to pay it all out, how much of the $10,000 would you give to each of the

Evaluating and Controlling Salespeople

Using Judgment Models -- Ranking Procedures

• Results of a sample of 242 sales managers

– How do your results compare with the

managers?

– Situation specific evaluations

– Overall evaluations

– Situation Specific Predictive Ability

Evaluating and Controlling Salespeople

Summarizing Sales force Performance

• Performance Matrix

– Shows interaction of 3 or more variables at a time – Identifies reps for rewards and punishments

– Helps find subtle interactions

– Findings in Figure 16-6

• Reps begin career selling high margin mix of products

• Reps end career by sacrificing margins for revenue • Laggards represent a plateauing problem

• Laggards should make more contractor calls

• If looking for $$ -- reward compromisers

Evaluating Sales Force Performance

Profitability Analysis

• Residual Income Analysis

– Sales growth is desirable as long as

profits exceed cost of capital

– Most comprehensive single measure of

sales force performance

– Existing control factors all included

– Expressed in dollars makes it easier to set

sales manager incentives

Evaluating Sales Force Performance

Profitability Analysis

• Return on Assets Managed (ROAM)

Profit Contrib.

Sales

Sales

Assets Managed

• Assets under sales management control

• District Analysis

– Assets managed poorly in District 4

– Profit contribution greatest in District 1

Evaluating Sales Force Performance

Profitability Analysis

• ROAM disadvantages

– focus on lower assets (inventory + acct. receivable)

– does not consider sales level or growth

• Solution: Residual Income Analysis (RIA)

Profit Contribution

Less: Acct receivable costs

Inventory carrying costs

Evaluating Sales Force Performance

Sales Force Evaluation Model

• Sales Analysis Principles

– 80/20 -- 20% of customers yield 80% sales

– Iceberg -- sales figures tip of iceberg -- need more

• Gathering Sales Data

– DSS

– hand held computers for field

• Steps in Sales Analysis

– Pick unit for analysis - by division, district, etc.

Evaluating Sales Force Performance

• The Big Picture– Start with aggregate sales by year

– Look for changes and trends -- market share, volume

• Refining through Cross Classification

– Sales by Region

• reward areas of strength? • move into areas of weakness

– Sales by Product Line

• Are you selling what firm wants? or what

salespeople want?

Evaluating Sales Force Performance

• Refining Through Cross Classification

– Dollar Vs. Unit Sales

• When price change (inflation) distorts dollar

figures

• Good for big ticket items

– Sales by Distribution Channel

• tends to change over time

• asks who customers really are

– Sales by Customer Type

• illustrates 80/20 principle

Evaluating Sales Force Performance

• Cross Classification Techniques

– Multi-way Tables

– Varying Customer Classifications

– Product Lines vs. Product Categories

Table 15-3 Sales Data for Bear Computer Company

1 2 3 4

Company Percentage Industry Company Volume Change from Volume Market Share Year ($ millions) Previous Year ($ millions) (percent)

1997 26 + 8.3 300 8.6

1996 24 +14.3 219 10.9

1995 21 +23.5 165 15.7

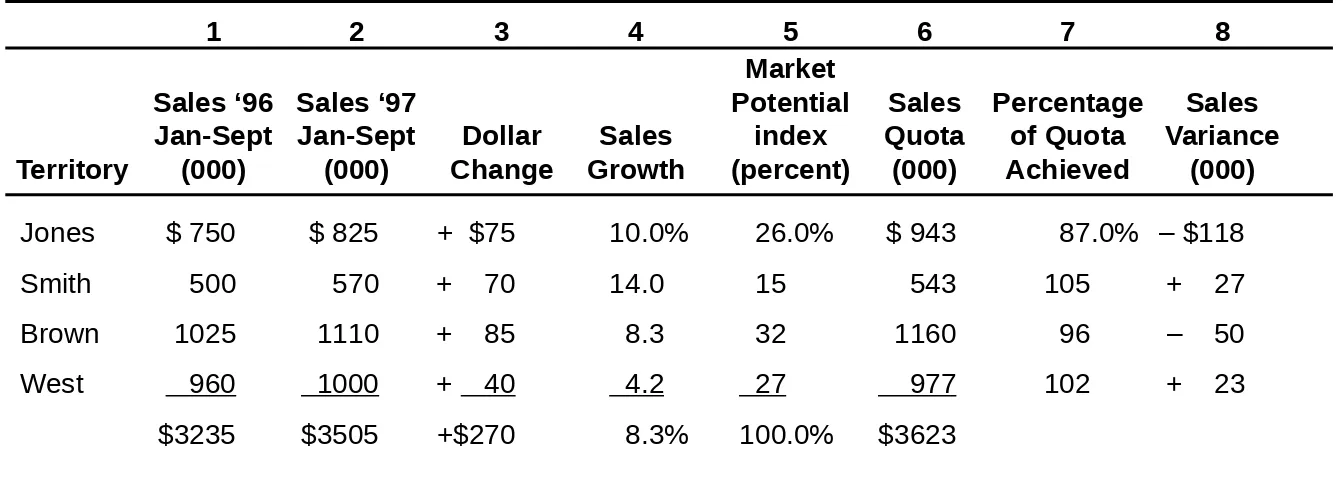

Table 15-7 Measuring Sales Force Output for Bear Computer Company

1 2 3 4 5 6 7 8

Market

Sales ‘96 Sales ‘97 Potential Sales Percentage Sales Jan-Sept Jan-Sept Dollar Sales index Quota of Quota Variance Territory (000) (000) Change Growth (percent) (000) Achieved (000)

Jones $ 750 $ 825 + $75 10.0% 26.0% $ 943 87.0% – $118 Smith 500 570 + 70 14.0 15 543 105 + 27 Brown 1025 1110 + 85 8.3 32 1160 96 – 50 West 960 1000 + 40 4.2 27 977 102 + 23

Figure 15-3 Ranking Salespeople on 10 Input/Output factors 3.87 3.66 3.44 3.23 3.02 2.80 2.59 2.38 2.16 1.95 1.74 1.53 1.31 1.10 COMPROMISERS

Avg sales $3.17 Avg contribution $1.13 Avg contribution % 35.8

Age 45

Calls 1122

Number of salespeople 18

STARS

Avg sales $2.91 Avg contribution $1.09 Avg contribution % 37.4

Age 37

Calls 888

Number of salespeople 11

Avg sales $1.78 Avg contribution $ .64 Avg contribution % 35.8

Age 44

Calls 958

Number of salespeople 11

LAGGARDS

Avg sales $2.03 Avg contribution $ .75 Avg contribution % 37.1

Age 35

Calls 921

Number of salespeople 16

SLOWPOKES Millions

$

Contribution Margin (%)