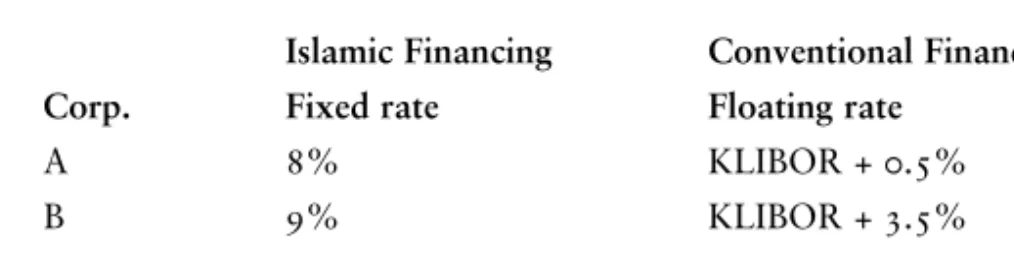

Consider the following example: Let's say two companies, A and B, face the following financing costs in the 'Islamic' fixed rate market and the conventional floating rate market (see Figure 1). In the 'Islamic' fixed-rate market, A can borrow at 8 percent per annum, while B can borrow at 9 percent, a difference of 1 percentage point. In the conventional floating rate market, A can borrow at KLIBOR (Kuala Lumpur Interbank Offer Rate) plus 0.5 percent, while B can at best borrow KLIBOR plus 3.5%, a difference of 3% points.

In addition, however, it has a comparative advantage in the floating rate market where it can borrow at a much lower rate than corporation B. Moreover, in the current dual banking system, many corporations are indifferent between borrowing in the Islamic fixed banking system. rate market or the conventional floating rate market. In our example, corporation A has a comparative advantage in the floating rate market, while corporation B is in the fixed rate market.

Therefore, corporation A will borrow funds in the floating rate market at a rate of KLIBOR + 0.5% while B borrows from the fixed rate market at 9 percent (see Diagram 2). Since A can borrow much cheaper in the floating rate market, it therefore has a comparative advantage in the floating rate market. In the gold payment system, gold should be used as a medium of exchange and as a unit of account, rather than national or international reserve currencies, for settling international trade balances.

On the ground, commercial banks that support gold accounts are capable partners in the implementation of the gold dinar system.

Implementing the Gold Dinar in Bilateral Payment Arrangements (BPAs) and Multilateral Payment Arrangements (MPAs) 19

Gold, however, has all the qualities of good money; it is desirable and highly valued in itself, homogeneous, stable, durable, divisible, movable, etc., and can neither be created nor destroyed. Thus, it can play the role of a stable international unit of account, which is sorely lacking in the current floating exchange rate system. For example, Lopez-Cordova and Meissner (2003) find that a commodity money regime and a monetary union are strongly associated with large increases in trade.

The commercial banks are viable intermediaries between importers and exporters on the one hand and the central bank on the other.

Bilateral Payment Arrangement (BPA)

Therefore, in the gold dinar mechanism, even countries with little or no foreign exchange reserves can participate significantly in international trade.

Multilateral Payment Arrangement (MPA)

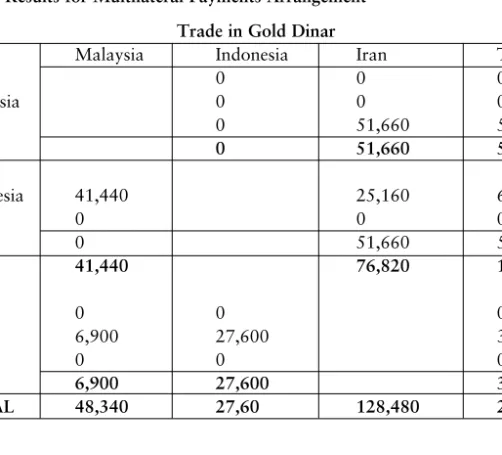

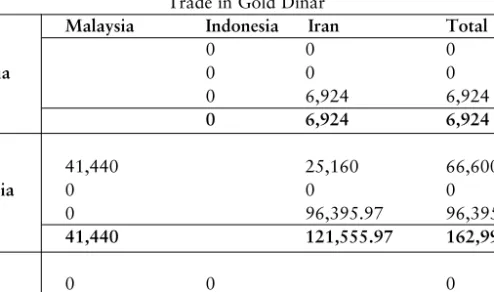

The above example answers the frequent question: are existing gold reserves sufficient to support the growing volume of international trade. Only the net balance remaining in the trade matrix should be settled in gold. Therefore, in the gold dinar system, central banks do not need to accumulate gold reserves as suggested by some international agencies.

It would be better to start small with whatever gold reserves countries have, within a small group of participating countries. Countries with small gold reserves can trade with gold producing countries like South Africa, Mali, Russia etc. That way we can solve problems while they are still small, without putting too much demand pressure on the existing gold market.

If countries rush to implement the gold dinar, this can only lead to upward pressure on the international gold price.

Determining an Efficient Trade Matrix

David Ricardo, the famous supply-side economist of the nineteenth century, wrote in his Principles of Political Economy and Taxation (London, 1817) that when money operates at its highest level of efficiency, the central bank does not need to hold gold. The model is flexible in terms of the number of participating countries and the number of products involved.

The Models 8

It should be noted that if a country wants an exact quantity of a product k; say a, then we take in the model bki=a-ε, and tki=a+ε, where ε is a small positive number, indicating the desired accuracy. To satisfy the needs of each country concerned, we must assume that the total needs of any product are less than the total available quantity of the product. If this condition is not satisfied, then .. a) the countries importing the product k must reduce tki (the maximum required quantity) and may also be bki , .. b) the countries exporting the product must reduce their export potential pki increase ,.

This inequality means that the amount of product imported by country from all other countries must be between bkj and tkj. Inequality 10 means that the amount of product k exported by a country i must not exceed its export potential in product k. The net payment between countries i and j is the modulus of the difference between the amounts owed by each country to the other:.

If , then country j must pay the amount of N ij in gold dinars to country i. If , then country i must pay the amount of N ij in gold dinars to country j. The minimum amount of gold dinars required for multi-bilateral trade to take place is:

The conditions and constraints of the model are the same, the changes are only in the objective function. The coefficient 1/2 is introduced in the objective function (17) because the amount of gold dinars paid (by the paying countries) is equal to the amount of gold dinars received (by the receiving countries) in the multilateral agreement.

An Illustrative Example: Implementing the Model

The solutions to the involved optimization problems are obtained using the software Nimbus Miettinen and Mäklä (2000). These terms express the fact that a country cannot export a product if it has no potential exports of that product, and that a country will not import a product if it does not need it. It is clear that the amount of gold needed to settle trade balances decreases as we move from gross settlement to bilateral to multilateral trade agreements, confirming that cooperation pays off.

Note that the solution to the optimization problem also provides each country with a target holding of gold (for the trading period), within the efficient multilateral trade agreement. For a larger matrix involving more countries, trade balances can be easily settled through the mediation of a clearing house. The clearinghouse role could be played by a custodian bank, such as the Islamic Development Bank (IDB) or the Bank of England, that would hold the gold reserves of the participating countries' central banks.

If we compare the results, we see that the multilateral setup requires less gold dinar than the multi-bilateral setup. In fact, only 93,980 DGs are required in the multilateral agreement, while 135,420 DGs are required in the multilateral agreement, a significant difference of 41,440 DGs.

Conclusion

This principle is similar to the application of the concepts of absolute advantage and comparative advantage in international trade. In the current global financial scenario, where major economies are faced with negative real interest rates, Islamic banking, which continues to deliver a positive real return, looks attractive even to conventional bankers. Indeed, in the global fiat monetary system, many nations, especially the developing ones, are losing their sovereignty.

The term "offshore" is somewhat misleading as it seems to imply that ringgit transactions take place outside the country's shores. In reality, speculative transactions take place within the country, with the ringgit being transferred between local bank accounts. Mundell (2002) argues that flexible exchange rates have led to increased international monetary instability and that the current system has some major shortcomings, which include the absence of an international unit of account and a mechanism to stabilize exchange rates.

There is wisdom in this, because the acceptance is despite the fact that the Prophet (peace be upon him) brought significant socio-economic transformation. Using four hundred years of wholesale price index data, Professor Jastram concluded that the stability was not because gold moved towards commodity prices, but because commodity prices eventually returned to gold. A regulation requiring that gold stock with central banks be used only to settle real transactions may be necessary.

Hassan and Choudhury (2002) provide policy recommendations for transformation to a 100 percent reserve monetary system with gold-backed micromoney. This section makes use of materials presented by Tan Sri Nor Mohamed Yakcop, the Special Economic Adviser to the Prime Minister of Malaysia, who first demonstrated the benefits of using the gold dinar in international trade, in a keynote address delivered to the 2002 International Conference on Stable and Just Global Monetary System, held in Kuala Lumpur on August 19 and 20, 2002. Micromoney and real financial conditions in the 100 per cent. System, 19.-20. August 2002, Kuala Lumpur, Malaysia.

Exchange-Rate Regimes and International Trade: Evidence from the Classical Gold Standard Era”, The American Economic Review, 93(1) March, pp. Paper presented at the International Seminar on Gold Dinar in Multilateral Trade, organized by the Institute of Islamic Understanding Malaysia on 22-23 October 2002, Kuala Lumpur, Malaysia. An Islamic View, in Proceedings of the 2002 International Conference on a Stable and Just Global Monetary System, 19-20 August 2002, Kuala Lumpur, Malaysia.