Corporate board, audit committee and

earnings manipulation: does the corporate regulation matter? An emerging

economy perspective

Sattar Khan and Yasir Kamal

Abstract

Purpose–This paper aims to investigate the impact of the revised Code of Corporate Governance 2017 (CCG-2017) clauses pertaining to board independence, mandatory inclusion of female directors, audit committee (AC) chair independence and directors’ expertise on earnings manipulation.

Design/methodology/approach–Using an unbalanced panel of 323 listed companies from 2015 to 2019, this study uses panel data regression models with a robust methodology called difference-in- differences to tackle the potential endogeneity.

Findings–This study’s findings show that, as compared to the pre-CCG-2017 period, board- and AC-related variables increased significantly in the post-CCG-2017 period. Furthermore, financial experts on the board and board independence have a negative effect on discretionary accruals (DAs), whereas female directors and DAs are positively related, as is real activity manipulation. The AC-related variables, such as AC independence, expertise in AC, and AC chair independence, are significantly different from the preperiod to the postperiod, whereas their relationship is not according to the hypotheses of the study. Moreover, these results are robust to additional analysis of the alternative proxies for female directorship and the endogeneity problem.

Practical implications–The findings of this study have implications for regulators and practitioners who are concerned with the functions of the board of directors (BOD). The findings of this research study show that earnings management (EM) may be reduced by independent and expert directors. However, board gender diversity is not reducing the EM. Therefore, the decision to appoint female directors to the board should be based on their business and professional attributes rather than simply filling quotas or blindly adhering to regulations. Moreover, the findings of this research may assist the regulator in encouraging listed firms to enhance board governance via independence, diversity and competency, which are useful for effective monitoring.

Originality/value–This study fills a gap in the literature by providing the first evidence of country- specific regulation (CCG-2017), concerning the BOD and AC-related clauses on EM in Pakistan, which is missing in the relevant literature general and in Pakistan in particular.

Keywords Board of directors, Audit committee, Code of Corporate Governance 2017, Earnings manipulation, Earnings management, Corporate governance, Pakistan Stock Exchange

Paper typeResearch paper

1. Introduction

The main objective of this study is to investigate the effect of the revised board of directors (BOD) related clauses in the Code of Corporate Governance 2017 (CCG-2017) on earnings management(EM) [1]. The amended clauses in the CCG-2017 are board independence, audit committee (AC) independence, a female director and the expertise of directors on the boards of the listed companies. Furthermore, this research aims to see if there are any

Sattar Khan and Yasir Kamal are both based at Institute of Management Sciences, Peshawar, Pakistan.

Received 9 January 2023 Revised 24 May 2023 17 August 2023

Accepted 23 October 2023

significant differences in limiting EM between the pre- and post period of CCG-2017.

Duncan (2001)documented that the majority of the alleged EM practices in the USA during the last decade were due to the inadequate monitoring of the BOD and ACs, which led to well-known accounting scandals. The US Congress passed the Sarbanes-Oxley Act (SOX) in 2002 due to high-profile accounting scandals to enhance the functions of boards and ACs, and improve the quality of financial reporting (Ghoshet al., 2010). Similarly, to comply with international trends, the regulator in Pakistan enacted the CCG-2017, to improve board effectiveness by including mandatory clauses for female, independent and expert directors in the boards and ACs.

The AC is regarded as a vital part of the system of corporate governance (CG). The AC is a subcommittee of the board and consists of directors who are members of the BOD. The AC maintains the authenticity and integrity of financial reporting by monitoring managers’

financial reporting, including EM. The revised CCG-2017 required a well-independent and expert AC to promote financial transparency and the integrity of financial statements. Due to its significance, now after the revision, the ACs of listed firms in Pakistan must have an independent chairperson and at least one expert member to keep an eye on how management reports and prevent the management from manipulating earnings.

According to the agency theory, the board monitors self-interested managers to reduce agency problems between managers and shareholders (Jensen and Meckling, 1976). The inclusion of more independent directors on the board may help alleviate the agency problem. The resource dependence view assumes that organizations cannot meet all their resources internally and instead opt for external resources (Pfeffer and Salancik, 1978). As a result, the inclusion of reputed external directors on boards will result in the effective delivery of the board’s advisory and consoling roles in the functioning of companies.

Moreover, “the resource dependence view,” has been applied to diverse boards, which improves the functioning of companies. According toAggarwalet al.(2019), independent and diverse boards may have superior monitoring, resulting in improved financial performance at the firm. Similarly, board composition is one of the most essential elements of any CG system. The research by Saonaet al.(2020) suggests that external (outside) independent directors are necessary to strengthen the monitoring and effectiveness of boards. In light of the foregoing discussion, the CCG in Pakistan has been revised to focus on board-related matters to strengthen board monitoring and minimize insider control on the board. The recent amendments to the CCG-2017 also shed light on gender diversity, independence and expertise on the companies’ boards in Pakistan.

In addition, the following factors motivated us to carry out this research study: first, Pakistan offers a suitable setting to examine the role of BOD features on EM due to the revision related to BOD and AC attributes in CCG-2017 introduced by the Securities Exchange Commission of Pakistan (SECP). Second, there are many contextual studies that link the BOD features with EM (Khanet al., 2019;Khanet al., 2020;Khanet al., 2022a,2022b;Khan and Kamal, 2021;Rasheedet al., 2019;Sajjadet al., 2019;Umeret al., 2019). However, these studies linked various CG variables with a single proxy of EM with a small sample and an older data period. Moreover, studies byKhanet al.(2022a,2022b) andKhan and Kamal (2021)linked the BOD features with EM in Pakistan, but first, they linked one proxy of EM with BOD features, and second, they did not use or apply the difference-in-differences (DID) for tackling the endogeneity problem. Last, in these studies, they had taken only BOD features, while in our study, we have taken both BOD and AC revised features and linked them with two proxies of EM, namely, discretionary accruals (DA) and real activity manipulation (RAM). Third, most of the other studies linking female directorship with EM (Khanet al., 2019a,2019b,2022a, 2022b;Khan and Kamal, 2021;Umeret al., 2019) used a single measure of female directorship, while in this research study we have used five measures of female directorship and linked them with EM. Finally, as far as we know, no study in the literature has studied the role of the revised CCG-2017 BOD and

AC-related features on EM, while taking country-specific regulation (CCG-2017) into account. Nevertheless, in the concerned literature, there are pre- and post-CCG studies, likeUsman and Kamardin (2015), who investigated AC attributes with EM;Outaet al.(2017) linked CG code with EM;Khan and Rehman (2020) linked BOD attributes and operating liquidity; andWanget al.(2019) investigated CG and firm performance. However, to the best of our knowledge, no research study has been done to check the impact of BOD and AC attributes on EM, while considering the revised CCG in an emerging economy.

Therefore, this research study fills this research gap in the concerned literature.

According to the study’s findings, the mean differences of the BOD’s attributes were significantly different before and after CCG-2017. In addition, the regression results depicted that, among the BOD attributes, board independence and the financial expertise of directors had a negative relationship with EM after CCG-2017. Whereas board independence and the financial expertise of directors were not related to EM before CCG- 2017. Moreover, the results of the study show that independent and financially expert directors are more effective in mitigating EM practices in the post-CCG-2017 period as compared with the pre-CCG-2017 period, conforming to and supporting the views of agency theory and resource dependence theory. In addition, the findings of the study cannot support the study’s hypothesis that the inclusion of a mandatory female director on the board is negatively associated with EM after the implementation of CCG-2017, as gender diversity on the board is positively related to EM in full-period regression. Moreover, this study conducted additional analyses linking various measures of gender diversity in boards with EM, but the results were the same as mentioned earlier. Likewise, this study found that 50% of boards in the sample size firms have no female on the board of Pakistan Stock Exchange (PSX) listed firms. The AC-related variables, such as AC independence, expertise in AC and AC chair independence, differ significantly from the pre- to postperiod of CCG-2017, but their relationship is not according to the hypotheses of the study.

This article added to the existing body of CG and BOD-related literature in several aspects.

First, this article added to the CG literature by focusing on a new country-specific regulation (CCG-2017) relating to the BOD composition and its relationship with EM in Pakistan. Whereas previous studies have only focused on EM (Chenet al., 2020;Faisalet al., 2021;Khan and Kamal, 2021). Second, most of the previous EM studies (Barghathiet al., 2021;Khanet al., 2019a,2019b;Khanet al., 2020;Kontesaet al., 2021;Wanget al., 2019) are based on agency theory, which considers the board as an important CG mechanism to monitor management.

Although the agency role of monitoring is paramount for BOD, the advisory role (resource dependence role) of BOD is also very important. Consequently, this research study integrates the perspectives of agency and resource dependence theory with regard to the influence of BOD attributes on EM while taking industry regulation (CCG-2017) into account. Moreover, the theoretical contribution of this research study lies in the combination of both theories and the support of the theoretical views of both theories on the boards of Pakistani-listed firms. Third, this research study has contributed to the literature on board independence and financially expert directors as effective monitors and resources in Pakistan. Fourth, the board and AC characteristics are checked not only on DA but also on RAM, while taking into consideration the industry regulation of CCG-2017, which is missing in the related literature. Lastly, in this research study, we have used a robust methodology called DID. The DID is a quasi- experimental method that can be used to identify the causal impact among study variables.

The DID uses pre- and post period data to estimate the causal impact of a specific economic intervention (in our case, the CCG-2017) on some outcome variable (EM). Moreover, this study fills a gap in the literature by providing the first evidence of country-specific regulation (CCG- 2017) concerning BOD- and AC-related clauses on EM in Pakistan.

This paper is organized into five parts, or sections. This paper starts with the introduction.

The context of the article is given in Section 2, along with a literature review and the study’s hypotheses. Section 3 provides sample size and data, variable measurement, EM models

and hypotheses-testing models. Moreover, in Section 4, the empirical results of the study are given with a discussion of them, and in the last section, the paper ends with the conclusion and recommendations.

2. Literature review and hypotheses

2.1 The context of the study and various corporate governance codes

Pakistan is a common law country that gained its independence in 1947 from the British Raj.

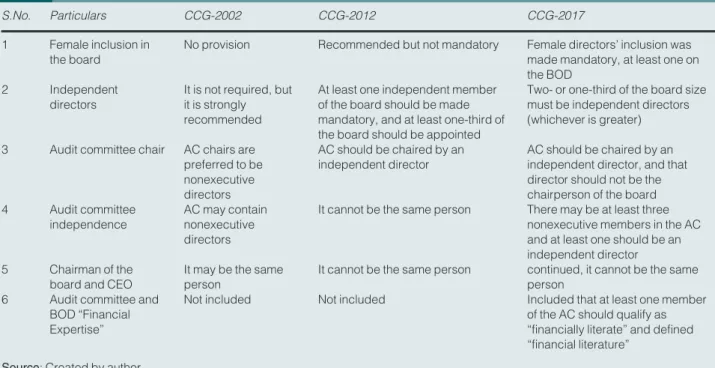

Although Pakistan is a common law country, it exhibits the features of a code law country (Yusuf et al., 2018). Pakistan has a concentrated and small, inefficient capital market, characterized by weak law enforcement, a lack of investor protection, strong political connections, the majority of businesses being family-owned and the dominance of business groups in the corporate sector (Ghani and Ashraf, 2005;Hussain, 2019;Khan, 2011;Shahid- ur-Rahman, 1998; Yusufet al., 2018). Similarly, in Pakistan, the Anglo-American model of CCG is adopted and followed. In addition, Pakistan has mostly family-owned listed firms (Khan and Kamal, 2022b) with a type II agency problem between minority and majority shareholders, contrary to the typical agency problem between managers and shareholders as prevalent in the USA and UK. Moreover, SECP regulates all nonfinancial institutions in Pakistan. The first CCG was implemented on March 28, 2002, in Pakistan. The 2002 CG code was based on globally accepted principles of openness, transparency and accountability for related firms (Khanet al., 2022a,2022b;Sheikh and Wang, 2012).

The CCG-2002 encouraged listed companies to have an independent director. It made training programs for directors’ mandatory, as well as guidelines for the formation of an AC, and the CEO and chairman could be the same person.

In addition to this, the CCG-2002 was revised in 2012 by SECP to meet international trends, practices and enhance the CG. The main objective of CCG-2012 was to strengthen information access and protect the rights of minority shareholders. Furthermore, in CCG- 2012, the dual position of CEO was banned, the minimum criteria for board independence were introduced, and board assessment programs were declared.

Moreover, the SECP revised the CCG-2012 in 2017 via the CCG-2017 due to international trends of female participation in the board, good governance practices and to strengthen companies’

boards through board diversity and independence. Furthermore, the SECP, via CCG-2017, made it mandatory to have a female director on the board to reach a minimum of 15% female representation on the board by 2020 (Khan et al., 2022a, 2022b) and to comply with international standards. In addition, following SOX, the CCG-2017 includes financially literate members in the AC as well as one mandatory independent director who should serve as the AC’s chairperson. Moreover, CCG-2017 increases the board’s independence by mandating that

“not less than two members” or “1/3 of the total size of the board” be independent.

Furthermore, the aforesaid variables of BOD, such as independence, female inclusion, expertise in AC and independence, in the CCG-2017, the limit for the number of directorships in multiple companies has been reduced from 7 to 5. In addition, in CCG-2017, an emphasize on the Human Resource Committee has been made, along with AC mandating that it be led by an independent director. Similarly, a recommendatory provision has been included in the CCG- 2017 for the companies to formulate Risk Management and Nomination Committees to tackle the dynamic market environment, continuously fluctuating corporate sector and to comply with best governance standards. The details of various CCGs in Pakistan are given inTable 1.

2.2 Theoretical background of the study

The BOD literature relies upon different theories, but in this study, the theoretical background is based on two theories, namely, the agency theory and the resource dependence theory. The board’s role in effective monitoring of the management is drawn

from agency theory, while the ability of the BOD to effectively deliver their monitoring task is a function of resource dependence theory (Mustafaet al., 2018;Orazalin, 2020). According to proponents of agency theory, it helps to comprehend the monitoring and supervisory roles of the BOD to control management. Moreover, agency theorists believe that the BOD has to protect shareholders’ interests by monitoring executives’ self-interest and opportunistic behavior (Assengaet al., 2018;Shleifer and Vishny, 1997).

On the other hand, resource dependence theory can be a substitute for agency theory in explaining the EM (Nguyen and Soobaroyen, 2019). According to Pfeffer and Salancik (2003), every organization is dependent on the external environment due to limited resources. Therefore, for an organization’s success, proper links with external resources are necessary to enhance its value. In addition to this, the resource dependence theory’s related studies maintain the argument that the BOD has an important link between the firm and external resources, which is essential for firm growth (Kiel and Nicholson, 2003;Pfeffer and Salancik, 1978). Moreover, Yeung and Lento (2020) posited that the resource dependence perspective regarding the board says that the BOD entrusts good board governance to a variety of experts to deal with uncertain and unfavorable situations.

Hence, this study is going to check the study’s hypotheses based on two theories. The agency theory, which views the BOD as an effective monitor of the self-interested and opportunistic behavior of management, and the resource dependence theory view the BOD as an effective resource for maintaining firm growth (Alhassanet al., 2021). Under the resource dependence view, the provision of BOD resources such as skill, expertise and diverse experience is likely to deter EM and enhance the quality of financial statements (reporting) (Kiel and Nicholson, 2003;Orazalin, 2020). Consequently, we can say that diverse boards with valuable resources such as information, skill and expertise can effectively curb EM.

2.3 Hypotheses development

2.3.1 Board independence and earnings manipulation. One of the most important components of board structure is independence. Board independence is regarded as a

Table 1 Various CCGs in Pakistan and their comparison

S.No. Particulars CCG-2002 CCG-2012 CCG-2017

1 Female inclusion in the board

No provision Recommended but not mandatory Female directors’ inclusion was made mandatory, at least one on the BOD

2 Independent

directors

It is not required, but it is strongly recommended

At least one independent member of the board should be made mandatory, and at least one-third of the board should be appointed

Two- or one-third of the board size must be independent directors (whichever is greater) 3 Audit committee chair AC chairs are

preferred to be nonexecutive directors

AC should be chaired by an independent director

AC should be chaired by an independent director, and that director should not be the chairperson of the board 4 Audit committee

independence

AC may contain nonexecutive directors

It cannot be the same person There may be at least three nonexecutive members in the AC and at least one should be an independent director 5 Chairman of the

board and CEO

It may be the same person

It cannot be the same person continued, it cannot be the same person

6 Audit committee and BOD “Financial Expertise”

Not included Not included Included that at least one member

of the AC should qualify as

“financially literate” and defined

“financial literature”

Source: Created by author

critical component of every CG code or law, and it is observed globally. Similarly, CG codes worldwide have a specific percentage of independent directors in the board’s composition.

According to Aguilera and Cuervo-Cazurra (2009), 196 CGs from 46 different countries covering the years 1978–2008, either explicitly or indirectly recommended a balanced ratio of independent (nonexecutive) and executive directors. The first two CCGs in Pakistan did not place a high priority on the board independence issue because of the country’s context of concentrated and family ownership. Unlike earlier CCGs in Pakistan, SECP has addressed the problem of independence in the CCG-2017, requiring every listed business to have at least two independent directors or one-third of all directors, whichever is greater.

Traditionally, in Pakistan, there is a low ratio of independent directors as compared to family directors (Khan, 2023). Moreover, PSX-listed firms have 17% board independence as compared to UK firms, which have 60% board independence (Hasan et al., 2022).

According toTran (2021), the BOD literature classified the independent director’s role into three types: first, the monitoring role (agency theory task), second, the advising and counseling role and third, the role of providing external resources (the last two are the resource dependence theory task).

Moreover, in the literature, there are two views on the BOD functions: the opportunistic view (agency theory) and the effective resource view (resource dependence theory) (Alhassan et al., 2021). Under the agency theory perspective, directors’ independence on the board is crucial to bringing down agency costs (Saonaet al., 2020;Sohailet al., 2017). In the same way, board independence shows unbiasedness in decision-making, a lack of family relationships within a company and ensures compliance with regulations. In addition to the agency theory, under the resource dependence theory, as presented by Pfeffer and Salancik (1978), independent directors are external resources (Al-Matari, 2019;Alhassan et al., 2021). Moreover, the outside directors are valuable resources; they have technical experience, sound knowledge and skills. Moreover, they effectively impact board decisions, which stimulate firm value (Rashid, 2015). Furthermore,Fernandez-Temprano and Tejerina- Gaite (2020)added that resource dependence theory supports diverse boards, and due to the diversity in boards, board functions improve in organizations, which in turn decreases EM in companies.

Having linked board independence with agency theory and resource dependence theory, the literature on board independence and EM is mixed and contradictory. Marra (2021) added that those independent directors who are nonbusy, have accounting expertise and are not appointed by controlling shareholders outclass the formerly independent directors in mitigating EM practices. In the same way, Alhebri et al. (2021) posited that board independence curbs EM in family-owned firms, they reported that the presence of independent directors in family firms reduces EM. Moreover, the role of independent directors on the board is to detect and deter EM and to ensure financial reporting quality (Brennan, 2021). In addition, the relationship between board independence and EM in Pakistani-listed firms is also mixed.Rasheed et al.(2019)state that board independence plays no role in mitigating EM in PSX-listed companies. In the same way, the findings of these studies (Rasheedet al., 2019;Sajjadet al., 2019;Umeret al., 2019) show that board independence and EM have a negative relationship in Pakistani-listed firms. This research will make the following hypothesis based on the above discussion, the results of current studies and the requirement of independent directors on the board via CCG-2017 in Pakistan.

H1. The ratio of independent directors on the boards of PSX-listed firms is more effective at controlling earnings manipulation in the post-CCG-2017 period than in the pre- CCG-2017 period.

2.3.2 Female directors and earnings manipulation.Four CG codes have been implemented in Pakistan over the last two decades. In the first two codes, 2002 and 2012, there was no clause relating to female directorship in the BOD. Female representation on the board was

made mandatory in CCG-2017 and did not change in CCG-2019. According to SECP, the female proportion was a mere 6.4% on the boards of all listed firms in 2017. Therefore, the SECP made female inclusion in the BOD mandatory due to the constantly evolving corporate sector and to cope with the global developments in CG. Moreover,Hasanet al.

(2022)reported that during the period from 2009 to 2018, in Pakistan, there was 6% gender diversity as compared to the UK, which has 19% gender diversity. In addition to this, Pakistan is a male-dominated society, and there is less representation of women in every field of life (Khan, 2023). Moreover,Khan (2023)added that there is on average 10% female representation in PSX-listed firms, while in PSX-listed family firms there is only 7% female representation on the board of Pakistani companies. Furthermore,Aminet al.(2021)added that female directors have a vital role in reducing agency costs, reducing principal and agent conflict and enhancing board monitoring, which will result in less earnings manipulation. In addition to this,Orazalin (2020)added that agency theory suggests that board independence augments internal control over the opportunistic behavior of management and executives. In this perspective, women on boards strengthen and improve board independence.

Moreover, under the agency theory, the board has a monitoring function over the management and executive, this monitoring function will be more effective when there is an independent and gender-diverse board (Carteret al., 2010). Subsequently, having a female on the board improves board performance, efficiency and reduces EM (Mnif and Cherif, 2021). Having discussed the agency theory perspective, the resource dependence theory proponents argue for a diverse board that has diverse experience, skill, knowledge, information and legitimacy (Fernandez-Temprano and Tejerina-Gaite, 2020). Moreover, according to Amin et al. (2021), the related research suggests that having women’s representation on the board alleviates the agency problem and produces the desired results. The resource dependence theory provides the foundation for this view and relationship.

Furthermore, women on boards are more risk-averse, taking more care of companies’

assets and extracting fewer benefits as compared to men on the boards (Yasser and Mamun, 2015). According toLakhal et al.(2015), EM is mitigated when there is gender diversity in the BOD and top management. Similarly, Agyei-Mensah (2020) added that female directors bring unique features to the BOD that make the board effective in better monitoring management and decision-making. In addition,Wahid (2018)claims that having female directors on boards reduces fraud and financial statement inaccuracies. Moreover, Gulet al.(2011)found that gender diversity on the board improves board discussions and the BOD’s monitoring of disclosures and financial reporting. On the contrary,Haseeb-ur- Rahman and Zahid (2021)reported that, contrary to agency theory, female directors on the board increase unnecessary monitoring, which wastes companies’ precious time, energy and may also prevent them from being effective monitors to prevent EM. In addition, gender diversity in PSX-listed firms lowers EM in Pakistan (Umer et al., 2019). Thus, gender diversity and EM literature are mixed. Pakistan’s 2017 CCG requires female board members owing to its importance. Consequently, we predict that gender diversity will have an impact on EM during the CCG-2017 postperiod. As a result, we propose the following hypothesis:

H2. The inclusion of female directors in the BODs of PSX-listed firms is more effective at controlling earnings manipulation after the implementation of CCG-2017.

2.3.3 Board expertise and earnings manipulation.In the CCG-2017, the financially expert directors have been defined. The term “financially expert” refers to a person who has membership in a SECP-recognized body of professional accountants or has a higher degree in finance from a Higher Education Commission recognized university or equivalent institution. The accounting and financial expertise (knowledge) of the BOD plays a key role in deterring management from engaging in EM. The ability to effectively control EM and enhance the quality of financial reports requires the BOD’s accounting knowledge (financial

expertise), which is essential to the BOD’s monitoring role (Siamet al., 2014). Moreover, in Pakistan, there is a dominance of insiders and family directors in the boards of PSX-listed firms; as reported byKhan (2023), there is a majority of family directors in the boards of PSX-listed firms, and every third member in PSX-listed firms is a family member. Therefore, due to the importance of independent and expert members in the boards, their inclusion in the board and AC was made mandatory in Pakistan via CCG-2017. Although the agency theory role of monitoring is paramount for BOD, the advisory role (resource dependence role) of BOD is also very important. For the advisory role, past working experience, skills and professional knowledge are important (Krollet al., 2008). As a result, a board that includes members with relevant professional and job experience will mitigate EM (Qiao et al., 2018). In addition to this, Khan and Kamal (2021) added that financial expert members in the AC effectively monitor the management and have a role in decreasing EM.

According to the findings of the study (Xieet al., 2003), EM was reduced when the BOD had financially expert directors on the board. On the other hand, a study byRuparatne and Meegaswattee (2019)found that financially expert directors may not help reduce EM, they may use their financial knowledge, skills and abilities to camouflage the financial numbers and commit EM. Moreover,Khanet al.(2022a, 2022b) added that in Pakistan, expertise directors are effectively reducing EM estimated under the DA approach. To sum up,Gerayli et al.(2021)argued that the presence of expert directors will enhance financial reporting quality and minimize the risk of EM in financial reporting. Therefore, keeping in view the latest literature on EM, this research will test the following hypothesis:

H3. The inclusion of financially expert directors in the BODs of PSX-listed firms is more effective at controlling earnings manipulation after the implementation of CCG-2017.

2.3.4 Audit committee independence and earnings manipulation.Independence is one of the key characteristics of the AC. AC’s independence is critical to limiting management’s opportunistic behavior (EM). One of the most important factors contributing to the AC’s efficacy is the presence of an independent director (Ayemere and Elijah, 2015). In addition to this, based on agency theory,Gerayliet al.(2021)andRaimoet al.(2020)argued that AC is a crucial CG mechanism that helps reduce management’s illegal activities and boost the openness and credibility of financial reporting. So, in Pakistan, due to the significance of having an independent director in the AC, the CCG-2012 was revised in 2017, and BOD and AC-related revisions have been implemented. Moreover, the CCG-2017 requires that the AC of PSX-listed firms have at least one independent director. Moreover, as chair of the AC, he or she shall ensure that financial statements are prepared using the approved accounting procedure and format. In addition, the revised CCG-2017 mandated that such an independent director not hold any other board positions. The CCG-2017 also defines

“independent director,” which implies that an individual holding the post of director in a company shall have no connections to and be independent from the administration of the company.

Moreover,Zalataet al.(2018) posited that the most prominent theory used to assess AC effectiveness is the agency theory. From the perspective of resource dependence theory, Pfeffer and Salancik (1978)added that the BOD provides resources to the company. These resources are advice and counsel, legitimacy, communication of information and assistance to management in obtaining resources. As a result, the independent directors in AC are external resources with advanced skills, expertise and information that may be useful in reducing EM.

According to the literature, AC independence is negatively related to EM. The studies of Klein (2002), Marraet al. (2011) andWan Mohammad et al.(2018) reported a negative relationship between AC independence and EM estimated via DA. According toChen and Zhang (2014), in China, the presence of independent outside directors deters management’s opportunistic behavior and provides reliable information to the stock markets. The CG is better when the AC has more independence than when it has less

independence (Xieet al., 2003). According to Xiaet al. (2015), the independence of the board as a whole did not have a more significant impact on EM in comparison to the independence of the AC on EM. Therefore, AC independence in AC is very instrumental in decreasing EM (Ayemere and Elijah, 2015;Mishra and Malhotra, 2016). However, despite the aforementioned findings, the studies ofBala and Yahaya (2014)andWan Mohammad et al.(2016)added that AC independence is positively associated with EM. As a result, the study’s fourth hypothesis is:

H4. Independent directors in the AC of PSX-listed firms are more effective at controlling earnings manipulation in the post-CCG-2017.

2.3.5 Audit committee expertise and earnings manipulation.One of the most prominent features of an AC’s effectiveness is its members’ financial expertise/literacy, and this quality of AC members has garnered worldwide recognition in academia and regulatory authorities during the last two decades (Ghafooret al., 2021). According toChaudhryet al.(2020), AC is one of the board’s most essential committees and has an important audit mechanism for high-quality financial reporting, and its members’ expertise is crucial in this regard.

Moreover, Al-Matari (2019) added that, according to resource dependence theory, financially expert directors in AC can contribute to the firm’s value due to their vast and extensive experience in the different settings or tasks, and improving firm value means enhanced financial reporting quality (Alzeban, 2019). Similarly, a competent (financially expert) and effective AC has the prospect of reducing agency costs and agency problems, which results in positive firm performance (Al-Matari et al., 2012a). Therefore, due to the prominent role of the AC in corporations, the revised CCG-2017 requires one AC member with financial knowledge in Pakistani-listed firms, like the SOX-2002, which suggested that at least one member of the AC should have financial knowledge.

Moreover,Juhmani (2017)added that it is widely accepted around the world that an AC’s primary responsibility is to review and verify a company’s financial statements. Hence, it is necessary that AC members have financial and accounting backgrounds. In addition, financially expert members of the AC have the potential to timely identify financial irregularities, enhance internal control and reduce information opaqueness (Ghafooret al., 2021). In the related literature, there are mixed results for AC expertise and EM.Inaam and Khamoussi (2016)added that the financial expertise of AC members is negatively related to EM. In the same way,Faisalet al.(2021)reported that in Pakistan, among AC attributes, only AC expertise curbs EM. Likewise,Zalataet al.(2018)reported that the proportion of AC expertise and female expert members is negatively related to EM. However, Wan Mohammadet al.(2016)studied Malaysian firms and added that expert members in AC are not associated with deterring EM practices. Furthermore, Mishra and Malhotra (2016) documented that having a financially expert member in an AC does not have any significant stimulus on EM. Considering the aforementioned literature review, this study’s hypothesis posits that accounting and financial expertise in the AC will reduce EM after the implementation of the CCG-2017 compared to the period preceding the CCG-2017.

Consequently, the final hypothesis of this study is:

H5. Financially expert directors in the AC of PSX-listed firms are more effective at controlling earnings manipulation after the implementation of CCG-2017.

3. Methodology

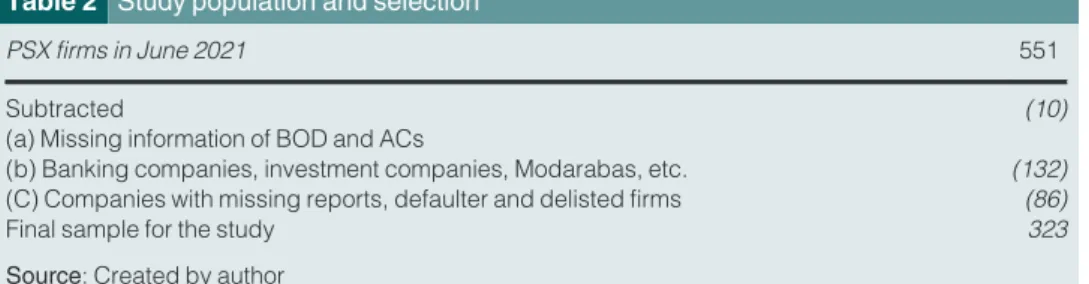

3.1 Sample selection and data

This study’s population consists of PSX-listed firms. This study’s initial sample size was 551 publicly traded companies. Financial firms (132) were not included due to differences in accrual procedures and accounting policies mentioned in the relevant literature (Chee and Tham, 2021;Khan and Kamal, 2022b). Besides that, firms with missing annual reports, were in default or were delisted were also not included in the sample (86). Moreover, ten (10)

firms did not provide BOD and AC information. The data from the remaining 323 firms was used in this study for the five-year period of 2015–2019. Moreover, this data is part of the data set that was published in the study ofKhan and Kamal (2022a).

In addition,Tables 2and3provide information on sample selection and sample distribution.

The data period is for five years, consisting of two years, 2015 and 2016 before and 2018 and 2019 after 2017, to assess the CCG-2017 influence on EM. The data was manually gathered from annual reports, the websites of the companies and SBP sources/

publications.

In Table 3, the PSX sectorwise distribution by year and industry is given. All the non- financial sectors have been taken into consideration for this study. The largest non-financial sector in PSX is the textile sector. In this study, it represents 28.13% of the total sample of firms. Furthermore, sugar and related industries are the second-largest sector, accounting for 9.02% of the sample in this study, while the chemical and cement sectors are the third and fourth largest sectors by sample size, representing 8.40 and 6.22, respectively. The smallest sectors are the woolen, leather and tanneries sector, which accounts for 0.31% of the total sample size.

3.2 Variables measurement

3.2.1 Dependent variable.In the accounting and EM literature, the Jones Model (Jones, 1991) is the most widely used EM proxy [2]. As every other DA model has been built by modifying the Jones Model (Jones, 1991), it is generally seen as the benchmark for EM models. Studies that extended the Jones Model are Dechowet al. (1995),Dechow and Dichev(2002)andKothariet al.(2005). Since,Dechow and Dichev (2002)model consists of accruals from the Jones model (Jones, 1991) and cash flow components from (Dechow and Dichev, 2002) model, it has been used in this study.

The following equation (1)provides an estimation of the Dechow and Dichev (2002) EM model:

ACCIT

LAGTAIT1¼b0þb1ðCFOIT1jLAGTIT1Þ þ b2ðCFOIT jLAGTAIT1Þ þb3ðCFOITþ1jLAGTAIT1Þ b4ðDSALESIT jLAGTAIT1Þ

þb5ðPPEIT jLAGTAIT1Þ þeIT; (1) where ACCIT stands for the accruals equal to operating cash flow less net income after taxes, CFOIT, CFOIT-1 and CFOITþ1mean operating cash flow fortyear,tþ1 andt1. In addition,DSALESITis changes in sales/revenue intyear, PPEIT is the property plant and equipment for yeartandLAGTAIT–1is the total assets lagged in yeart.

In addition to DA, RAM proxies have also been estimated under theRoychowdhury (2006) model, which is derived using the following equations:

Table 2 Study population and selection

PSX firms in June 2021 551

Subtracted

(a) Missing information of BOD and ACs

(10) (b) Banking companies, investment companies, Modarabas, etc. (132) (C) Companies with missing reports, defaulter and delisted firms (86)

Final sample for the study 323

Source: Created by author

CFOIT

LAGTAIT ¼b0þb1ð1jLAGTAITÞ þ b2ðSALESIT jLAGTAITÞ þ b3ðDSALESIT jLAGTAITÞ þeIT

(2) PRODIT

LAGTAIT ¼b0þb1ð1jLAGTAITÞ þ b2ðSALESIT jLAGTAITÞ þ b3ðDSALESIT jLAGTAITÞ þb2ðDSALESIT1 jLAGTAITÞ þeIT

(3) DISEXPIT

LAGTAIT ¼b0þb1ð1jLAGTAITÞ þ b2ðSALESIT jLAGTAITÞ þ eIT (4) The variables are described in detail inAppendix.

3.3 Hypothesis testing

The following equations tested the study’s hypotheses:

Table 3 Sample distribution by year and industry

S.No. PSX sector name Code

Years

2015 2016 2017 2018 2019 Total by industry %

1 Automobile assembler 801 12 12 12 12 12 60 3.73

2 Automobile parts and accessories 802 7 7 7 7 7 35 2.18

3 Cable and electrical goods 803 5 5 5 5 5 25 1.56

4 Cement 804 20 20 20 20 20 100 6.22

5 Chemical 805 27 27 27 27 27 135 8.40

6 Engineering 808 11 11 11 11 11 55 3.42

7 Fertilizer 809 5 5 5 5 5 25 1.56

8 Food and personal products 810 17 17 17 17 17 85 5.29

9 Glass and ceramics 811 8 8 8 8 8 40 2.49

10 Leather and tanneries 816 1 1 1 1 1 5 0.31

11 Miscellaneous 818 10 10 10 10 10 50 3.11

12 Oil and gas exploration companies 820 4 4 4 4 4 20 1.24

13 Oil and gas marketing companies 821 8 8 8 8 8 40 2.49

14 Paper and board 822 8 8 8 8 8 40 2.49

15 Pharmaceuticals 823 10 10 10 10 10 50 3.11

16 Power generation and distribution 824 14 14 14 14 14 70 4.36

17 Refinery 825 5 5 5 5 5 25 1.56

18 Sugar and allied industries 826 29 29 29 29 29 145 9.02

19 Synthetic and rayon 827 8 8 8 8 8 40 2.49

20 Technology and communication 828 13 13 13 13 13 65 4.04

21 Textile composite 829 54 54 54 54 54 270 16.8

22 Textile spinning 830 32 31 31 32 31 157 9.77

23 Textile weaving 831 5 5 5 5 5 25 1.56

24 Tobacco 832 2 2 2 2 2 10 0.62

25 Transport 833 4 4 4 4 5 21 1.31

26 Vanaspati and allied industries 834 2 2 2 2 1 9 0.56

27 Woolen 835 1 1 1 1 1 5 0.31

322 321 321 322 321 1607

Total 20.04 19.98 19.98 20.04 19.98 100

Source: Created by author

MCDAit¼uþu1BINDitþu2 BEXPitþu3BDIVitþu4ACINDitþu4ACEXPit

þX

Mpm Controlþmit (5)

RAMit¼uþu1BINDitþu2 BEXPitþu3BDIVitþu4ACINDitþu4ACEXPit

þX

Mpm Controlþmit (6)

In equation (5), the dependent variable MCDA is DA computed using the Dechow and Dichev (2002)model. RAM is the EM proxy, estimated inequation (6)by theRoychowdhury (2006)method. The BIND, BEXP and BDIV represent board independence, expertise and female representation, respectively. ACIND stands for independence in the AC and ACEXP stands for expertise in the AC. Furthermore, control refers to a set of control variables.

Appendixcontains all the details.

Moreover, for checking the impact of the revised 2017-CCG board and AC-related variables on EM. In this study, an alternative approach called DID has been used. The DID is a quasi- experimental method that can be used to identify the causal impact among the study variables.

It can be used only with panel data having particular attributes, such as a panel data set that has the data before and after the intervention. In the same way, the DID uses pre- and postperiod data to estimate the casual impact of a specific economic intervention (in our case, the CCG-2017) on some outcome variable (EM). Furthermore, the DID approach estimates the change (difference) in observed outcomes between treatment and control groups in pre- post treatment periods using a fixed effect model. The treatment group is the group that received the intervention, and the control group did not receive the intervention. Here, in this research study, the “treatment firms” (group) are those firms that have implemented the recommendations and mandatory BOD regulations after the implementation of CCG-2017, while the “non-treatment firms” (control group) are those firms that did not implement the required CCG-2017 regulation.

Many benefits are associated with the DID approach. First, it controls for time-invariant differences between control and treatment groups and eliminates the individual fixed effects.

Second, it is more robust than propensity score matching because propensity score matching only controls for observable variables, whereas the DID controls for not only observable variables but also time-invariant unobservables. So, it is preferable to use the DID over propensity score matching when there is pre- and postperiod data. Finally, the DID approach resolves the problem of endogeneity during the estimation process and estimates the true impact of an intervention, i.e. in our case, the CCG-2017. Having discussed the DID approach in this research study, before DID analysis, the following equation/model was used:

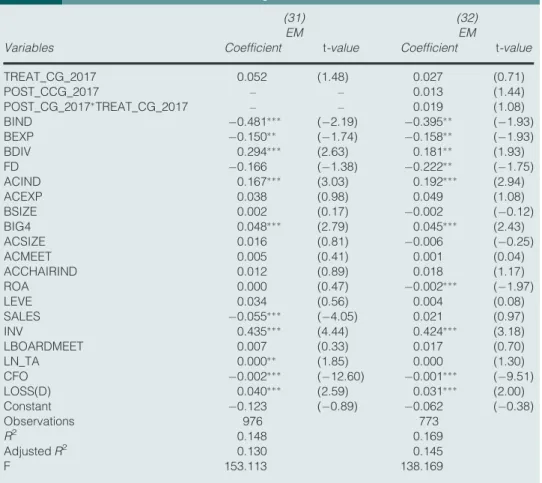

MCDAit¼uþu1TREAT CG 2017þu2BINDitþu3 BEXPitþu4BDIVitþu5ACINDit

þu6ACEXPitþX

Mpm Controlþmit (7)

In the aforementioned equation, TREAT_CG_2017 is equal to 1 if the firms have implemented the CCG-2017 recommendations and have increased board independence by 16% on average. The 16% that is board independence on average in the CCG-2017 period, as well as other BOD-related variables, are taken on the same average in this research study, while all other variables are the same as mentioned above.

Moreover, the classical DID equation to handle the endogeneity issue is given in the following equation by following the studies ofChenet al.(2020)andMoursli (2020).

MCDAit¼uþu1TREAT CG 2017þu2POST CCG 2017

þu3POST CG 2017TREAT CG 2017þu4TREAT CG 2017þu4BINDit þu5 BEXPitþu6BDIVitþu8ACINDitþu8ACEXPitþX

Mpm Controlþmit (8)

The abovementioned equation has been estimated over the years 2018 and 2019. The POST_CCG_2017 is the before (pre) and after (post) dummy variable, taking the value of 1 for the years 2018 and 2019 otherwise zero. The POST_CG_2017TREAT_CG_2017 is the interaction term of DID, and the remaining variables are the same as defined in the previous paragraphs.

4. Empirical results 4.1 Year-by-year statistics

The year-by-year descriptive statistics are presented inTable 4. It will show us the increase or decrease in the board and AC variables from 2015 to 2019, with the change of CCG in 2017. The board’s independence has increased positively from 2015 to 2019. The average value of board independence in 2015 was 16.7%, while it was 21% in 2019. Meanwhile, the average number of financially knowledgeable board members in 2015 was 31%, while it was 35% in 2019. Similarly, female directorship was only 7% in 2015 but has risen to 10% in 2019. These findings indicate that independent, expert directors’ inclusion has increased from 2015 to 2019 by 5% and 4%, respectively, while female directorship has increased by 3%.

Furthermore, AC independence has increased from a 2015 mean value of 27 to 33 in 2019.

In the same way, expertise in AC has also moved from 31% in 2015 to 37% in 2019. The most noticeable variable in AC is the chair independence of AC; the values inTable 4show that nearly 90% of AC chairs have independent directors in the year 2019, while in the years 2015 and 2016, the independent chairperson of AC had a 58% and 62% mean value, respectively. Besides, the dependent variable proxies, such as accrual MCDA and RAM, have decreased between 2015 and 2019.

4.2 The pre- and the postperiod descriptive statistics

Table 5presents descriptive statistics and at-test of mean differences between the before and after CCG-2017 periods.Table 5 shows that board independence, female directors and financial expertise changed dramatically from pre- to post-CCG-2017. Similarly, among the AC variables, compared to the pre-CCG-2017 period, AC independence, AC expertise and AC chair independence have significantly increased and changed after CCG-2017. In addition, if we compare the values of EM proxies from the pre-CCG-2017 period to the post- CCG-2017 period, we find that they are significantly different.

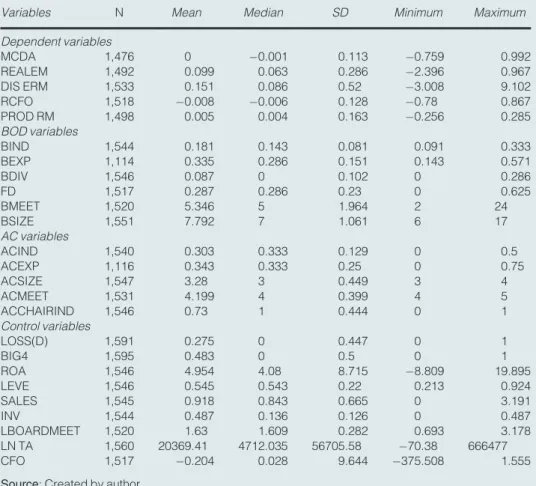

Table 6shows full sample descriptive statistics for the variables included in the study for a five years period, from 2015 to 2019. The number of observations is a minimum of 1,492 and a maximum of 1,595 due to unbalanced panel data. The average value of DA (Dechow and Dichev, 2002) is 0.005, while the aggregate RAM estimated underRoychowdhury (2006)is 0.09. Furthermore, the average board size in Pakistani firms is 7.79, with the maximum size being 17 and the minimum being six. The board’s independence is 0.18 on average, which is quite low but expected due to the concentration of ownership and family dominance in Pakistan. Board gender diversity is 0.08% on average in the boardroom, which is below the international average which of 16.90% (SECP, 2020), while board expertise is 0.33% on average in Pakistani companies’ board rooms.

Besides, the abovementioned board attributes, the AC attributes show that AC independence, as compared to board independence, is greater on average 0.30%, AC expertise is 0.34%

and AC chair independence is 73%. The last findings indicate that the majority of PSX-listed firms have an independent chairperson in the AC.

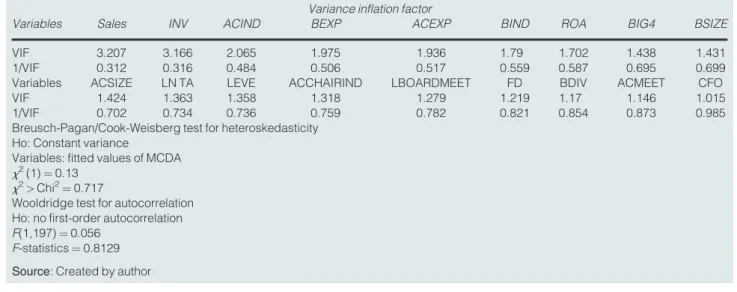

The pairwise correlation matrix result is shown inTable 7. InTable 7, no value is close to 0.7 or greater, which indicates that there is no multicollinearity problem. Besides, we have checked for the endogeneity issue by including the fitted value of R (residual) in the

Table4Year-by-yearofboard,auditcommitteeandearningsmanagement VariablesYear2015Year2016Year2017Year2018Year2019 NMeanSDNMeanSDNMeanSDNMeanSDNMeanSD Dependentvariables MCDA2920.0390.1032980.0080.0882990.0230.1143000.0210.1162870.0010.13 REALEM2840.1820.3132950.1470.2993000.0780.2673050.0250.2713080.0690.256 DISERM2990.1530.4033040.1520.4743070.1620.6253090.1180.4133140.1710.631 RCFO2970.0390.1393010.0160.1323040.0270.1343070.0430.1043090.020.11 PRODRM2860.0390.1792950.0280.1763030.0020.1543060.0240.1473080.0160.149 Boardofdirectorsvariables BIND3080.1670.0763070.1650.0743130.170.0763100.190.0833060.2130.085 BEXP2230.3130.1432220.3280.1472240.3380.1512230.3410.1552220.3540.155 BDIV3100.0780.1043090.0780.1043110.0830.1033100.0910.1013060.1070.093 FD3050.2980.233020.2930.2313060.2880.2313040.280.2293000.2780.229 BMEET3085.2692.1223085.3862.0153105.4261.9873075.3711.842875.2721.84 BSIZE3117.7811.0523097.7991.0533137.7991.0723117.7971.0573077.7821.079 Auditcommitteevariables ACIND3050.2710.1483060.2850.1343110.30.123110.3190.1183070.3380.108 ACEXP2250.3150.2482220.3240.2442230.3420.2532230.3570.2462230.3790.255 ACSIZE3093.2650.4423093.2880.4543113.2830.4513113.2860.4533073.2770.448 ACMEET3054.1930.3963074.2250.4183104.1870.3913104.2030.4032994.1840.388 ACCHAIRIND3080.5840.4943080.6230.4853110.6850.4653110.8520.3563080.9030.297 Controlvariables LOSS(D)3190.3070.4623180.2830.4513210.2520.4353200.2630.4413130.2720.445 BIG43190.4860.5013190.4920.5013190.4830.53200.4750.53180.4780.5 ROA3044.629.0953095.2629.0583095.4838.6343144.9598.3373104.4428.451 LEVE3040.5420.2193090.5310.2223090.5410.2233140.5560.223100.5570.217 SALES3041.0240.7613080.9440.6633090.7841.9463140.8860.683100.8910.709 INV3020.1460.1223090.1410.1223090.1370.2883140.1510.1313100.1460.131 LBMEET3081.6130.2863081.6370.2853101.6410.2993071.6390.272871.6210.266 LNTA30617,250.7947,885.6131218,050.9951,399.5131419,263.6253,294.1331421,905.7259,881.4631425,281.6968,467.52 CFO2970.0650.263010.0630.1293060.0330.1763051.20721.5033080.0340.145 Source:Createdbyauthor